IOSG Weekly Brief | The Payment Moment for AI Agents: Who Will Become the Stripe of the Machine Economy? #324

Original authors: Yiping, Turbo, IOSG Ventures

Core narrative

· Agent Payment is transitioning from PoC to the infrastructure competition phase

· x402 processed 3.3 million transactions in 30 days, with an ATV of $0.46 (Visa’s average is ~$50). Estimated real Agent payment monthly transaction volume is < $30M.

· TradFi giants are accelerating: Visa is launching Intelligent Commerce + Trusted Agent Protocol, Mastercard is opening Agent Pay to all U.S. cardholders in November 2025, and Stripe is partnering with Tempo to launch MPP on March 18, 2026.

· Strong M&A signals: Seven acquisitions totaling $8.05B were completed between 2025 and 2026 (Capital One acquired Brex for $5.15B, Mastercard acquired BVNK for $1.8B, Stripe acquired Bridge for $1.1B). Giants are choosing to buy rather than build.

The Facilitator layer is a highly worthwhile investment opportunity today. Its position is similar to Stripe in the early days of e-commerce, connecting upward to protocols and downward to applications.

The facilitator directly controls the agent's signing key and spending policy, serving as an unavoidable trust anchor. It receives both custody fees and order flow revenue, making it the most profitable role in the entire stack.

· MCP (Model Context Protocol) is becoming the standard interface for agents to call payment tools. Whoever has their payment MCP server natively integrated into Claude, ChatGPT, and Cursor will secure a position similar to the "default search engine" in Chrome.

Cryptocurrency infrastructure and card networks are not mutually exclusive; the winners are unified gateways that bridge both pathways.

· A shopping agent requires ACP (Stripe) for merchant checkout, x402 for API micropayments, and AP2 (Google) for authorization auditing. No single protocol covers all scenarios.

· Stripe MPP launches in March 2026, marking the first time a single protocol simultaneously supports stablecoins (Tempo chain) and fiat (Stripe SPT). Partners include Visa, Mastercard, Anthropic, OpenAI, and Shopify. This is the first productized signal of the convergence trend.

Protocol-driven markets push value upward; giants won't dominate everything.

· x402 and MPP are becoming open, commodified infrastructure. Visa and Stripe will dominate the clearing and settlement and card network side. The identity layer, agent app store, wallet policy engine, and credit infrastructure are still missing.

Market Overview

What is Agent Payment?

Agent Payment refers to AI agents autonomously holding funds, authorizing expenditures, and completing transaction settlements without direct human intervention. This goes far beyond simply having an agent “click a payment button.” Achieving this requires a comprehensive financial infrastructure encompassing identity verification, wallet management, spending policies, and settlement processes, enabling the agent to function as an independent economic entity.

Traditional payment systems assume both parties are KYC-verified humans linked to bank accounts. Agents break this assumption: they have no ID, no bank account, no credit history, yet need to purchase API calls, pay for cloud computing power, buy data, and even place orders on Amazon on behalf of users. This fundamental architectural mismatch has given rise to the entire agent payment sector.

Three core modes

The core process of Agent Payment is divided into three types:

Tokenized Card (virtual card). The agent receives a virtual Visa/Mastercard number via API, with spending limits, merchant category restrictions, and an expiration date; transactions are settled through traditional card networks. Ramp Agent Cards, AgentCard.sh, and Slash use this model. The benefit is that merchants need no changes; the cost is that the card must be linked to a human account, and card networks charge 2-3% in fees.

x402 Stablecoin (HTTP-native micropayments). The server returns an HTTP 402 status code with payment details (wallet address, chain, amount); the Agent's Facilitator automatically signs and completes an on-chain USDC transfer, attaching the transaction hash as a credential in the request header. No API key, no account, and no human approval required—transaction cost is only L2 gas (approximately $0.001 per transaction on Base).

Session-based Streaming (MPP mode). The agent pre-authorizes a spending limit, incurs continuous charges during the session without on-chain settlement for each transaction, and settles all charges in a single batch at the end of the session. Ideal for high-frequency scenarios involving hundreds of API calls per session. Stripe MPP with Tempo chain uses this mode.

How does an agent pay everyday bills?

For regular bills such as SaaS subscriptions, cloud services, and data sources, the Agent now has two options:

1. Card spending. Generate virtual cards via Ramp Agent Cards or Slash and link them to SaaS platforms. Corporate finance sets monthly spending limits and merchant whitelists; agents automatically renew subscriptions within authorized limits. Compatible with traditional providers such as AWS, Google Cloud, and Notion.

2. Go x402. For vendors supporting x402 (Neynar, Hyperbolic, Token Metrics, etc.), Agents pay per invocation without upfront fees or subscriptions—each request is automatically settled via USDC micropayments. The issue is that very few vendors support x402, and they are concentrated in crypto-adjacent services.

Market size

Be honest about the scale: from $6.3M at the beginning of 2026, annualized to about $126M, this is still a fraction of Visa’s $14.6T transaction volume in 2024. However, x402 ATV has risen from an early micro-payment level of $0.09 to $0.46 (verified by Artemis data). It remains within the micro-payment range, and the commercial inflection point has not yet been reached. The market is still extremely early, but the economic foundation is already in place.

Tailwinds

· TradFi legalization (strong). Visa launches "Agentic Ready," Stripe partners on MPP, Mastercard and AmEx join the x402 Foundation. Visa’s CPO calls it “the biggest thing since e-commerce.” The market is validated as real, and investment risk is reduced.

· Protocol standardization accelerated (strongly). The x402 Foundation has migrated to the Linux Foundation, with 20+ founding members including Visa, Stripe, Google, AWS, and Microsoft. Resistance has vanished; x402 is becoming a standard at the HTTP level.

· AWS excels at building production-grade infrastructure. Amazon Bedrock AgentCore has been released and natively integrated with x402. CloudFront + Lambda@Edge provide a merchant-side reference implementation. An end-to-end Agent-to-Merchant payment闭环 has been completed on AWS (March 2026). AWS is releasing a reference architecture, and enterprise adoption will follow.

· MCP service explosion (strong). Over 11,000 MCP servers, with less than 5% monetized. ToolOracle has already enabled monetization via x402 on 73 servers and 708 tools, creating natural demand for payment infrastructure.

· Surge in AI agent count (strong). Over 1 million registered agents (2026); all major LLMs are pushing agent capabilities. Timeline: 12–24 months.

· Stablecoins are accelerating adoption (strong). Total market cap: $246B (2025). Stripe, Visa, and MC are all integrating USDC. It’s already happening.

· Subscription model decline (medium). Developers providing skills/data need to pay per usage. Timeline: 12–24 months.

· Regulatory clarity (mid-term). The EU’s MiCA has been implemented, the U.S. stablecoin bill is advancing, and the CFTC chair stated that “AI needs blockchain.” This will unlock institutional adoption. Timeline: 12–24 months.

Target users

The payment infrastructure service caters to five types of buyers, each with distinct pain points, willingness to pay, and purchasing authority. Currently, the strongest interest comes from three groups: AI application developers (who cannot launch Agent products without paying), corporate finance teams (driven by compliance and constrained budgets), and skill/data providers (whose monetization is directly blocked by the lack of pay-per-use infrastructure). While real financial flows exist between consumers and Agents (M2M), they are still immature and exhibit low short-term willingness to pay.

Core institutional players and merchant outreach

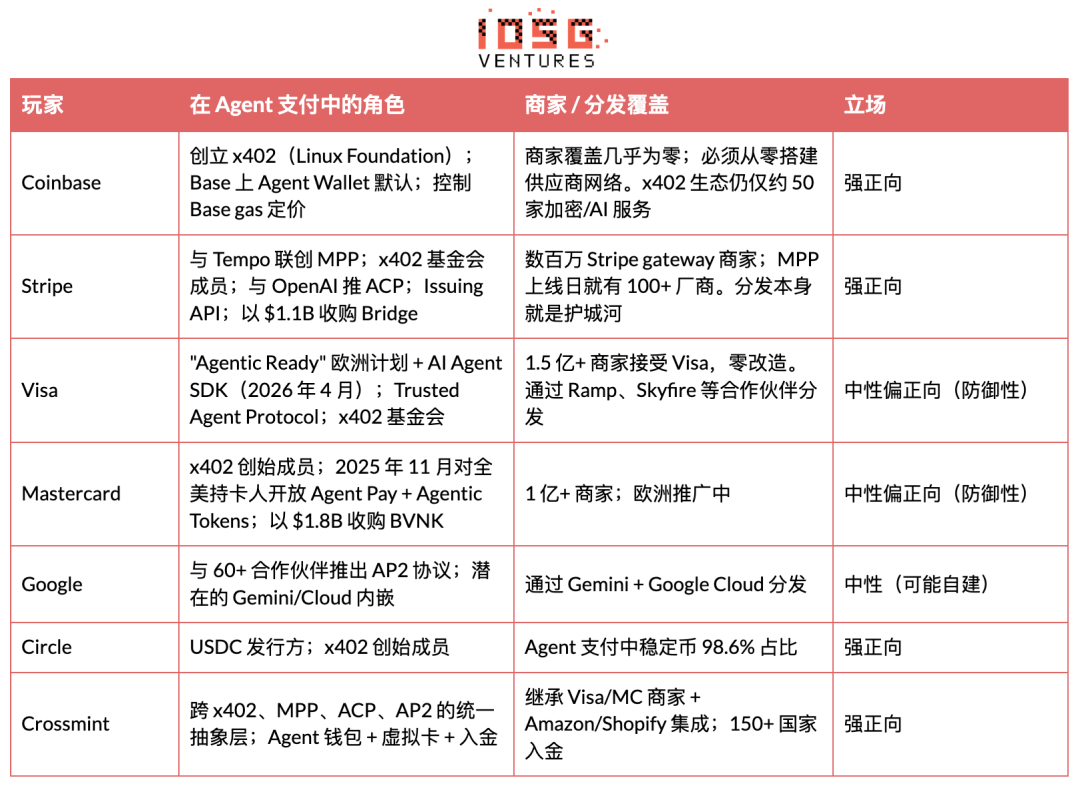

Agent Payment is primarily driven by eight institutions, including two crypto-native players (Coinbase, Circle), three card networks/payment giants entering the space (Stripe, Visa, Mastercard), one AI platform (Google), and two aggregation-layer companies (Crossmint, Tempo).

There is a chicken-and-egg problem in reach. Card networks command overwhelming merchant coverage (Visa 150M+, MC 100M+), requiring no modifications from merchants. x402 has only about 50 crypto/AI services. Without more merchants, transaction volume won’t grow; without transaction volume, merchants won’t onboard. Stripe MPP breaks the deadlock by leveraging existing merchant relationships (SDK upgrades rather than full integrations); Crossmint breaks it by aggregating both tracks through a single API.

Several unresolved issues currently

· The security threat model is new and unresolved

Key threats include prompt injection, agent behavior失控 (recursive loops exhausting budgets), key leakage, agent impersonation, and third-party SDK supply chain risks.

The most dangerous failure is not unauthorized access, but abuse after authorization.

The policy engine at the infrastructure layer is necessary, but most wallets do not have it.

· Lack of standardized Agent identity

· There is no reliable way to verify who the Agent is, what permissions they have, or whether they have been compromised.

ERC-8004 has been deployed to the Ethereum mainnet, featuring three types of registries (Identity, Reputation, and Validation based on ERC-721), but adoption is still in early stages.

· NIST has accepted the proposal on AI Agent Identity and Authorization (April 2026). EIP-11419 proposes adding an Agent Permission Validator to modular smart accounts.

· Without identity, each Agent transaction relies purely on trust.

· Lack of a dispute resolution mechanism

Stablecoin payments are designed to be fast and irreversible, with no chargebacks, no banks to complain to, and no recourse mechanisms.

Smart contract escrow and on-chain reputation systems are under exploration but have not yet been standardized or reached production readiness.

Institutions will not adopt at scale without clear error handling, overpayment, and fraud response frameworks.

· Inadequate compliance infrastructure

An increasing number of jurisdictions are applying the Travel Rule (FATF) to stablecoin transfers.

KYC, AML, sanctions screening, and audit trails are not optional for financial applications, but most agent payment tools treat compliance as an afterthought.

Teams that don’t incorporate compliance design on day one will face significantly higher costs for later modifications.

· Cross-chain complexity

· The agent must operate on multiple networks (Base, Solana, Stellar, Canton, and other permissioned chains).

· Strategy execution must be consistent regardless of where the trade is settled.

No single chain has won the race for agent payments, so infrastructure must be cross-chain, increasing engineering and security overhead.

Track overview and value chain

Agent Payment is not a single market, but an ecosystem with a seven-layer stack.

The facilitator (L2) and wallet (L1) capture disproportionate value because they control the agent's private key.

Whoever holds the key controls the economic sovereignty of the Agent. The protocol layer (L0), as an open-source standard, does not generate revenue directly, but companies that establish the standard—such as Coinbase via x402 and Stripe via MPP—monetize indirectly through surrounding facilitator services.

It’s like internet history: HTTP is free, but Cloudflare and Akamai, which control access to HTTP traffic, are billion-dollar companies.

In-depth analysis of the track

Payment Protocol (L0)

x402

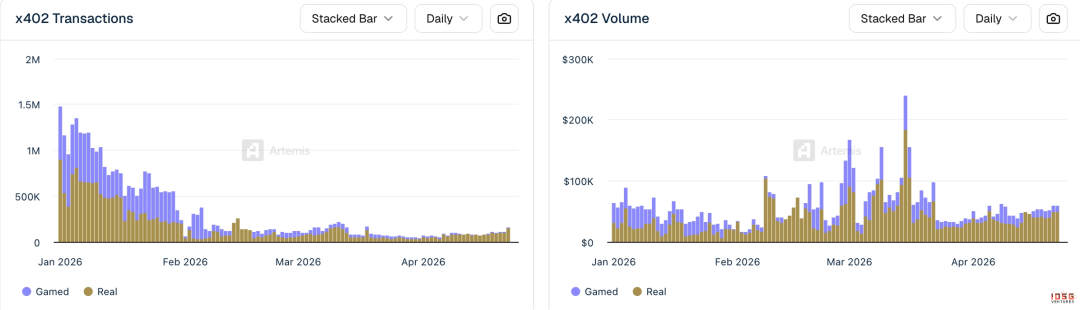

The situation with x402 is slightly more complex, as the Base chain accounts for the majority of transactions.

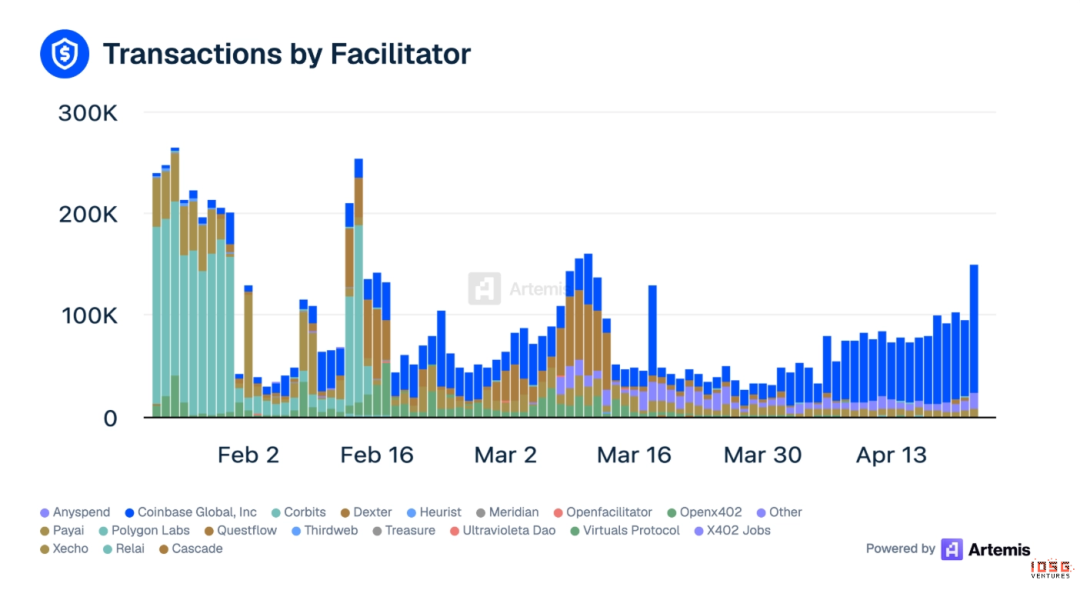

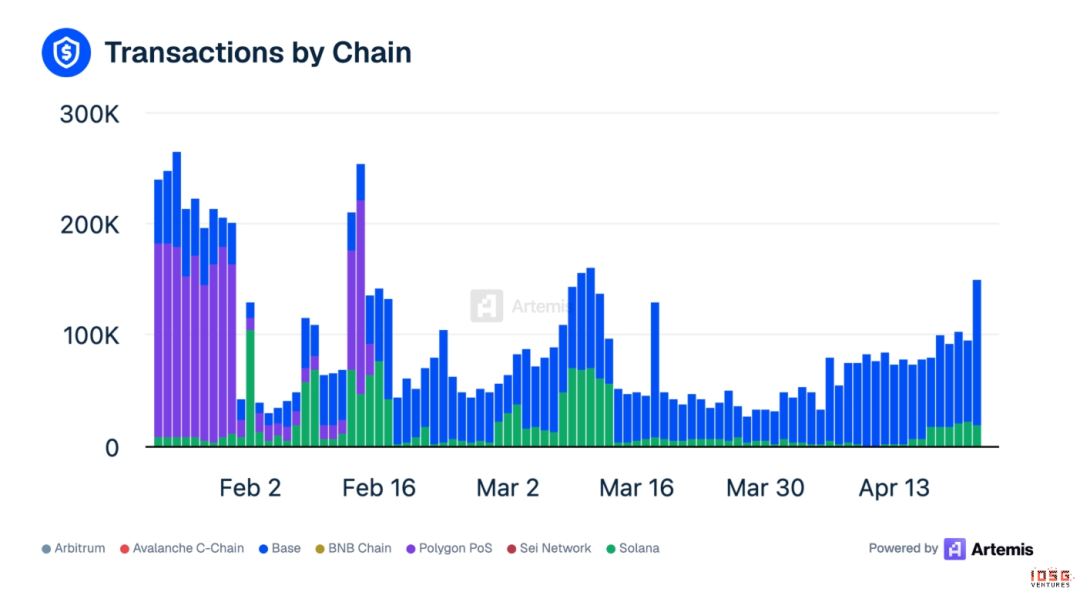

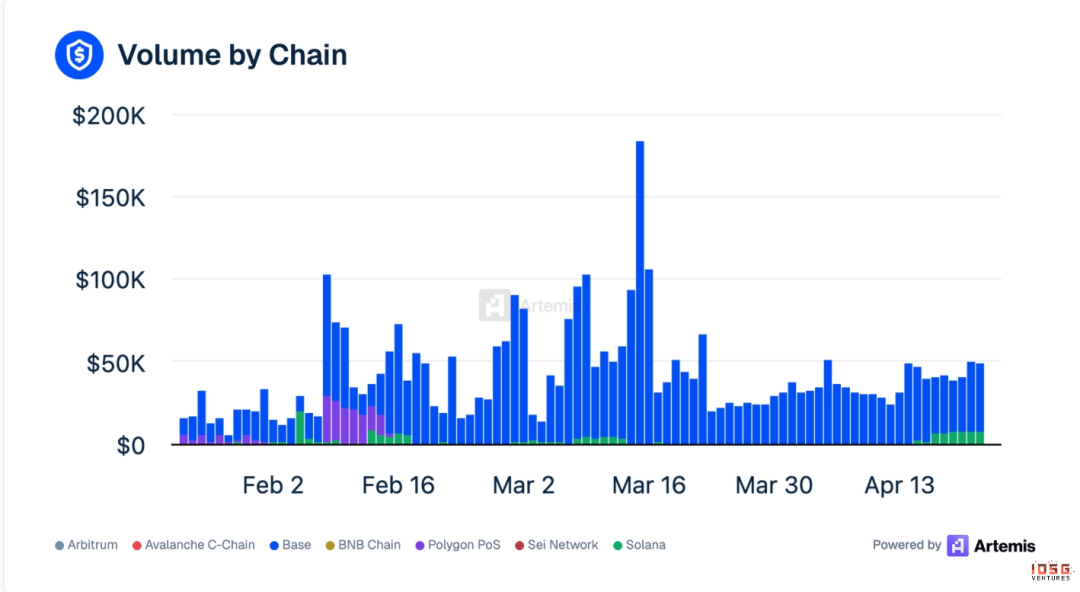

· Daily active data (March average): 110,000 transactions, approximately $51K in trading volume

· Base dominates: 82% of transactions occur on Base, 99% of trading volume is on Base

· Top Facilitator: Coinbase Global #1 (41%), PayAI #2

· Wash trading accounts for a significant portion: 36% of x402's March trading volume was fabricated (wash or incentive-driven), inflating the apparent number of trades and overstating actual Agent demand

▲ Source: Artemis

x402 Ecosystem Data (Artemis, April 2026)

· Supported chains: Base, Ethereum, Polygon, Solana, Avalanche, Sui

The x402 Foundation, jointly governed by Coinbase and Cloudflare (founded in September 2025), has now moved under the Linux Foundation and has 20+ founding members.

· Stripe integrated x402 on Base in February 2026

· Minimum viable payment: $0.001

· End-to-end payment time: approximately 2 seconds

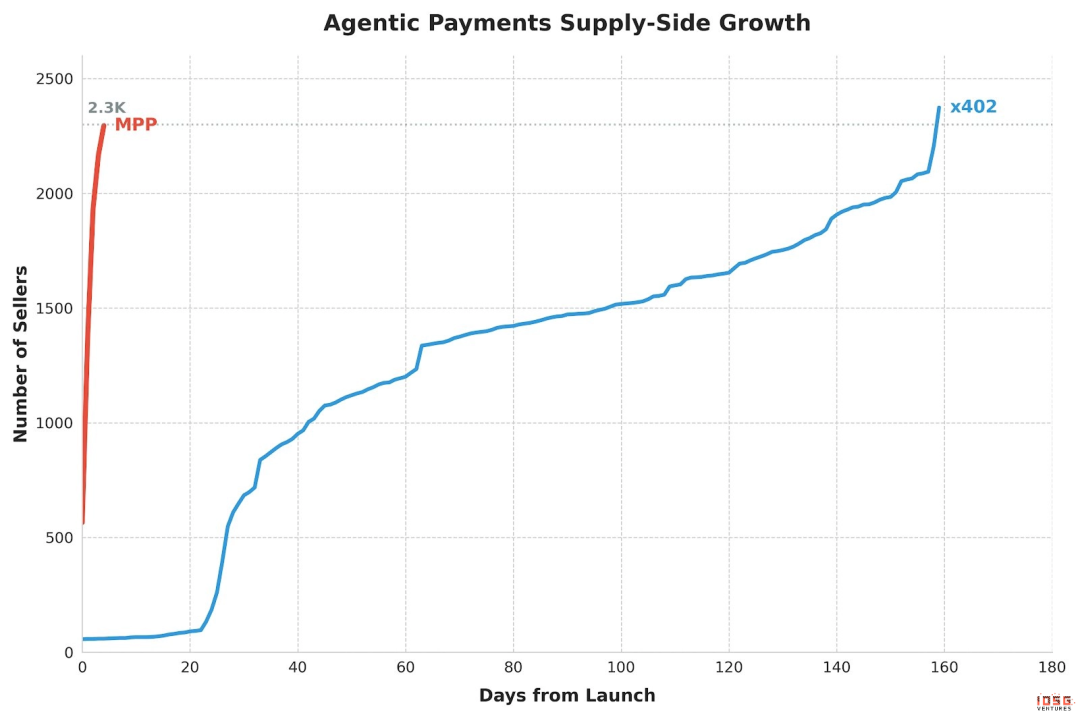

· Cumulative sellers over 5 months: approximately 2,300

5-step payment process

1. Users/developers fund the Agent strategy

2. The agent sends a request to the vendor's API and receives an HTTP 402 response (containing the merchant wallet, supported chains, asset type, and price).

3. The facilitator verifies whether this payment is within the spending policy authorized by the agent.

4. After approval, the Facilitator executes the on-chain USDC transfer.

5. The agent includes the transaction hash as proof of payment in subsequent requests; the merchant verifies it and provides the service.

Merchant coverage is currently the biggest limitation: Neynar, Hyperbolic, Token Metrics, Pinata (IPFS), Heurist, Prodia (image generation), Firecrawl (web scraping). Almost all are crypto- or AI-native services. Traditional e-commerce platforms (Amazon, NYT) have not yet been integrated.

Traditional e-commerce (Amazon), mainstream SaaS (Notion, Slack, AWS), and content platforms (NYT, Spotify) have no integration with x402.

The agent has limited capabilities on x402: purchasing GPU compute, calling APIs, and storing files. Tasks such as placing orders on Amazon, renewing Notion, or paying for Uber still require payment networks.

Merchant integration is widely regarded as the final and most challenging part of the Agent payment stack. The API proxy model (where the Agent calls restricted APIs on behalf of the user) may violate merchant Terms of Service and introduce additional legal risks.

Early concerns centered on the $0.09 ATV being insufficient to support the facilitator's P&L, with the bottleneck remaining micro-payment economics and the breadth of merchant coverage.

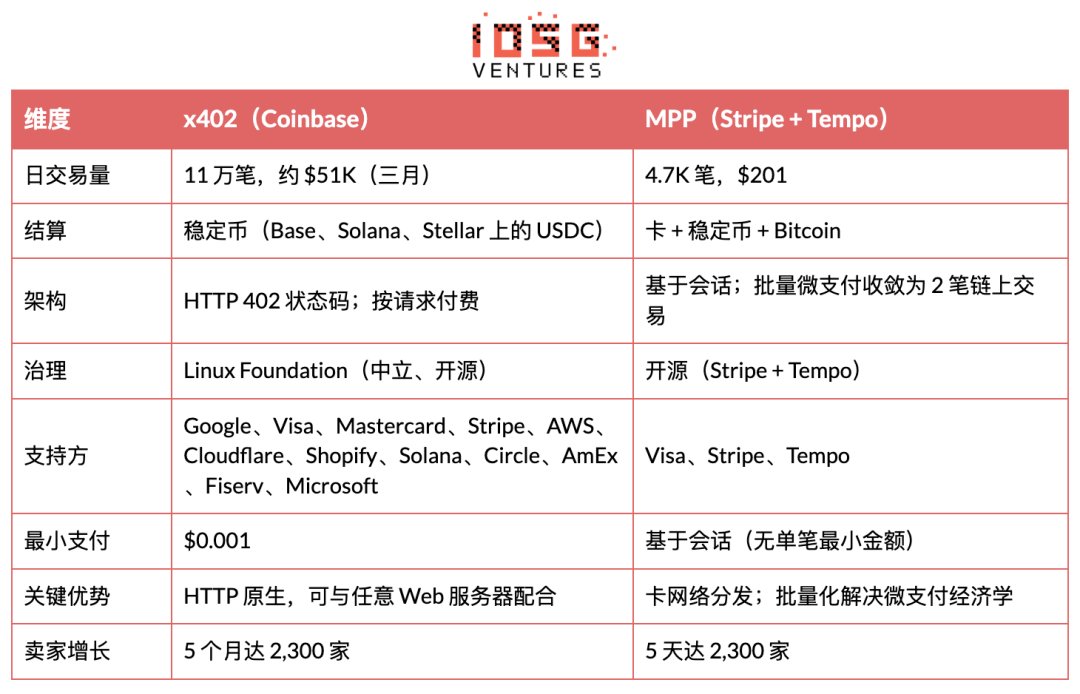

MPP (Machine Payments Protocol)

MPP just launched but is growing rapidly, reaching 2.3K sellers in just 5 days.

MPP, introduced by Stripe and Tempo, enables any client (agent, application, or human) to pay for any service within the same HTTP request. Developers use MPP to have their agents pay for services, while service operators use MPP to accept API payments.

· Daily active data: 4.7K trades, $201 in trading volume

· x402 took 5 months to reach 2.3K sellers, while MPP achieved it in just 5 days

Architecture

· Session-based: Agent pre-authorizes spending limits, enabling streaming micropayments within the session without on-chain settlement for each transaction

· Settled via the Tempo chain (with $5B bridged), sub-second confirmations

· Supports Stripe SPT (fiat), Visa cards, stablecoins, and Bitcoin (via Lightspark)

· Over 100 vendors have integrated as of the launch day

The strategic significance lies in MPP being the first substantive fusion product in the crypto vs. card battle. Stripe’s distribution capabilities (millions of merchants worldwide) combined with Tempo’s stablecoin settlement efficiency could create a two-pronged challenge to pure crypto solutions (x402) and pure card solutions (Visa IC).

Risk

It has been live for only a few weeks and lacks production-grade data. The Tempo chain itself is new, and its ecosystem has not yet been validated.

x402 vs MPP comparison

Integration trend

They are converging, not competing.

· Stripe is a founding member of the x402 Foundation, and MPP explicitly supports both stablecoins and cards.

· Visa is hedging its bets: it contributes its card rail specifications to Stripe’s MPP while advancing its own Intelligent Commerce and Trusted Agent Protocol. Framing x402 and MPP as opposing camps ignores the fact that the largest card networks are design partners for both.

The architecture is complementary:

· x402 Handling payment negotiation at the HTTP layer: How the server uses the 402 status code to tell the client “Pay me”

· MPP handles transaction execution via sessions: it consolidates unlimited micropayments into just two on-chain transactions (opening + settlement)

· The session model directly addresses the scalability issue of micropayments. Instead of aiming for 12 million transactions per second at $0.09 each, batch thousands of micro-interactions into a single settlement.

Stripe's distribution channels enabled MPP to match the number of sellers that x402 accumulated over five months in just five days, validating the assessment that "distribution > protocol."

Visa Intelligent Commerce

Visa announced the Intelligent Commerce framework in April 2025, launched "Agentic Ready" in Europe in March 2026, and released the AI Agent Developer SDK on April 2, 2026.

Core components:

· Trusted Agent Protocol (TAP): Distinguish legitimate Agents from malicious bots

· Tokenized credentials: AI-ready card credentials with spending limits, merchant categories, and approval requirements

· Pilot partners: Ramp, Skyfire, and other undisclosed parties

The biggest advantage is merchant coverage: the Visa network spans over 150 million merchants worldwide, allowing agents to use a single Visa card number to make purchases on Amazon, Uber, or any SaaS platform—without any modifications required by the merchants.

The biggest drawback is that it must be tied to a human account. Visa’s trust model is “backed by KYC-verified humans,” which fundamentally conflicts with the long-term vision of an autonomous agent economy.

Other protocols

· ACP (Agentic Commerce Protocol): Designed for instant checkout within conversational interfaces, such as within ChatGPT. Targets the consumer checkout layer, not the API settlement layer. ACP complements x402.

· UCP (Unified Commerce Protocol for ATXP): Aims to unify all Agent payment protocols under a single interface

· MoonPay Agents: Bridge traditional checkout flows with AI agents, converting human checkout processes into programmatic payments executable by agents via API

Wallet and Key Management (L1)

More than a dozen wallet providers are competing in this market, resembling the early mobile wallet landscape before Apple Pay.

Use case:

· Lending and Credit: AI-driven underwriting is entering the consumer crypto lending space. 3Jane fully automates credit underwriting via smart contracts, using verifiable financial records to set interest rates and enforce loan covenants without human review.

· Creator and gig economy settlements: Agent handles routing, wallet management, and currency conversion across platforms. Audius directly distributes 90% of revenue to artists in real time when content is consumed, with no monthly settlement cycles and no intermediary fees.

· Fund Management: An agent-based fund system that reasons across real-time market conditions, rebalances positions in real time, enables cross-border settlement without waiting for business hours, and deploys idle funds into interest-earning tools.

Facilitator Layer (L2)

The Facilitator layer sits between the protocol (x402, MPP) and applications. Coinbase Global remains the largest facilitator by cumulative volume, accounting for 41% of all x402 transaction value (source: Artemis).

Why this layer is the monetization layer for Agent economics: Agents must pay to make purchases, and the Facilitator is where these payments are actually settled. Model companies are unlikely to handle this themselves, as they won’t run GTM for long-tail scenarios, leaving the monetization opportunity to independent operators.

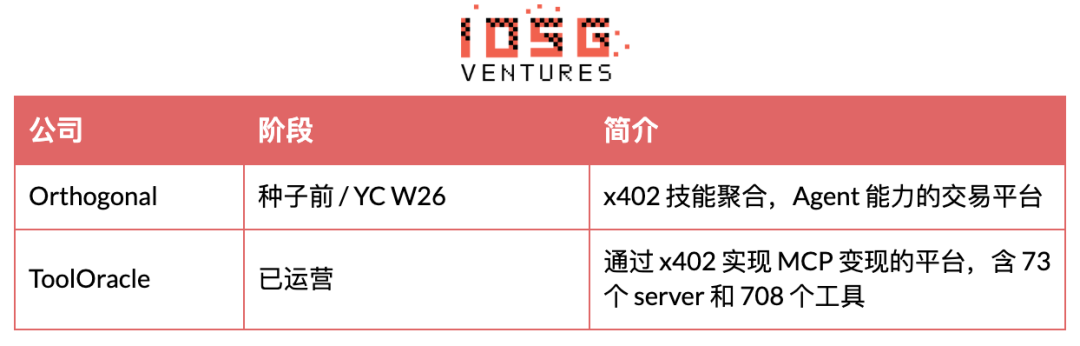

Facilitator startup

Other facilitators (open-source tools, non-funding startups): x402-rs (Rust library), OpenX402 (permissionless facilitator), OpenFacilitator (free shared endpoint), B402 (BSC-specific fork), CodeNut (agent infrastructure), RelAI (x402 API marketplace), AurraCloud (decentralized compute, AURA token).

Use case

· Pay-per-query data access: The most high-volume facilitator use case today. Trading agents require real-time market data, compliance agents need sanctions screening, and credit agents require credit checks. The facilitator enables these agents to pay per request, without subscriptions, API keys, or vendor contracts. Spraay already offers 70 x402 endpoints covering oracles, analytics, AI reasoning, and search, with single calls ranging from $0.001 to $0.10.

· API Monetization for Developers: Facilitator abstracts blockchain interactions, allowing any developer to gate their API with x402 payments without running a node or understanding cryptography. The AWS CloudFront + Lambda@Edge reference architecture enables x402 support for any HTTP application at the edge.

· Subscription Management: The Agent autonomously handles cancellation workflows and offers real-time, usage-based negotiation to retain you. As the software transitions to a pay-as-you-go pricing model, the Agent’s value in optimizing what you pay will significantly increase.

· Cross-chain payment routing: Facilitator handles swaps, bridging, and settlement, enabling Agents to pay on any chain using any token, while merchants receive the assets they want. AnySpend supports 19+ networks. This is the pipeline neither Agents nor API providers want to build themselves.

Tokenized Card (L3: Governance and Strategy / Identity and Authorization, Virtual Card)

Virtual card issuance process

· Card program setup: Platforms (such as Ramp or AgentCard.sh) establish a virtual card program through card-issuing partners (Visa/Mastercard issuing banks).

· Create card via API: Developers generate virtual cards via API for each Agent or spending scenario, setting parameters:

· Spending limits (per transaction / daily / monthly)

· Merchant Category Code (MCC) whitelist/blacklist

· Validity period (one-time or lifelong)

Geographic region restrictions

· Agent receives card details: The agent obtains a 16-digit card number, CVV, and expiration date, which can be used at any merchant that accepts Visa/Mastercard.

· Transaction Authorization: When a merchant initiates a transaction, the card network validates it in real time according to predefined rules.

· Settlement: Deducted from the business funding account after settlement through traditional card networks (T+1 or T+2).

Main Card API Provider Comparison

The core limitation of the card mode

1. Must be linked under a parent account: All Agent cards must ultimately be linked under a KYC-verified individual or business account as the funding source.

2. Fees: The card network charges 2-3% in interchange fees, which is not economical for micro-payment API scenarios.

3. Settlement speed: T+1 to T+2, insufficient for real-time settlement between agents.

4. Limited merchant control: Agents may be incorrectly flagged as fraudulent.

Identity and Reputation (L4: Governance and Strategy / Identity and Authorization - Identity Side)

Identity is infrastructure, not a standalone use case—it underpins every other layer.

Skill Discovery & Store (L5)

Use case:

· In-game rewards: Web 3 gaming platforms deploy agents to manage in-game economies, distribute rewards, and handle asset transactions. Virtuals Protocol has tokenized AI agents as in-game NPCs, trading bots, and research assistants, enabling the community to jointly own and govern them.

Agent Coordination (L6)

Use case:

· Agent-based trading: The shift from algorithmic trading to agent-based trading has changed the unit of competition from latency to intelligence. Classic algorithmic trading: Execute Y when price crosses X. Agent-based trading: Reason across market conditions, liquidity, risk parameters, and portfolio positions to determine optimal actions.

· Agent group: The next phase is a coordinated group of agents. When a financial agent executes a transaction, compliance and risk agents operate in real time to verify, flag, and audit.

Data and Compliance (L7)

TRES Finance, Chainalysis, and Allium are also positioned at this level, but they originate from a broader blockchain analysis context.

Compliance Agent team: Institutions deploy Compliance Agents as parallel workforces to monitor transaction flows in real time, flag anomalies, conduct sanctions screening, and autonomously generate regulatory reports.

Crypto-native vs. Card Network Battle

Crypto-native camp

Stablecoins are the agent's "native currency" for three reasons:

1. Extended trust structure: Stablecoin wallets can be linked to anything—social accounts, domain servers, autonomous smart contracts—enabling agents outside the traditional financial system to trade.

2. Native internet global settlement: An agent workflow spanning U.S. LLM endpoints, European data providers, and Southeast Asian compute clusters should not require three separate payment systems.

3. Cost structure: On Base, gas cost per x402 transaction is approximately $0.001, compared to card networks’ 2-3% interchange fees. Even if the x402 ATV rises to $30, stablecoin gas costs remain two orders of magnitude cheaper.

Card network camp (represented by Visa / traditional FinTech)

The Agent card can be used right away for three reasons:

1. Merchant coverage: Over 150 million merchants already accept Visa/MC, requiring no modifications.

2. Consumer protection: Chargebacks, fraud detection, and dispute resolution represent 50 years of accumulated infrastructure. Stablecoin transactions are irreversible.

3. Compliance maturity: PCI DSS, KYC/AML, and consumer protection legal frameworks are well-established.

Practical conclusions

· Short-term (1–2 years): Card rails dominate. Stablecoins are limited to crypto-adjacent API micropayments.

· Medium-term (2–4 years): Convergence. Stripe MPP has demonstrated that a single protocol can simultaneously support stablecoins and fiat currencies.

· Long-term (5+ years): If stablecoin regulation is implemented and merchant adoption increases, crypto could become the default.

Framework payment support with MCP

Current framework integration status

Currently, no major AI framework has built-in native payment capabilities; all frameworks integrate payments through external tools, primarily MCP servers.

MCP is the de facto standard

MCP is rapidly becoming the universal interface standard for agents to call external tools. Microsoft uses MCP in Copilot, and all major agent frameworks support it.

Published payment MCP server:

· ATXP: 14+ tools (payment_make, web_search, web_browse, etc.), compatible with Claude, LangChain, CrewAI, and OpenAI SDK

· FluxA: fluxa-agent-wallet (X402 payment + USDC withdrawal + payment link) and fluxA-x402-payment skill are now available on LobeHub

· Clink: clink-mcp-server, open-source TypeScript implementation

· PayMCP: A provider-agnostic payment layer for MCP tools (MIT open source)

· Ramp: Ramp MCP integration is available on Composio

· AgentPay (OpenClaw): AgentPay skill, supporting wallet purchases requiring human approval

Strategic implication: Whoever’s payment MCP server becomes the default configuration for mainstream clients like Claude Desktop, ChatGPT, and Cursor will secure the “default entry point” for agent payments—just as Google pays Apple $26 billion annually to be the default search engine in Safari. ATXP currently leads in framework coverage, but Coinbase (via CDP MCP server) and Stripe (via MPP) have platform-level distribution advantages.

Competitive landscape and moat

Analysis of winner-takes-all in sub-sectors

The strength of the moat is bimodal. L4 card governance (Visa/Mastercard duopoly) and L3 routing (Circle + Bridge) are already locked in by network effects. L1 wallets have real switching costs and are moving toward centralization. L2 facilitators and L4 identity are the contested battlegrounds where startup returns are actually being generated.

Upstream and downstream opportunities

Industry lifecycle

The lifecycle stage is early to mid-stage. Expected to enter the early growth phase within 12–18 months. Two indicators: standardization converging to 1–2 dominant protocols, and at least one agent payment project achieving monthly transaction volume exceeding $10M.

Investment analysis

7 Powers Framework

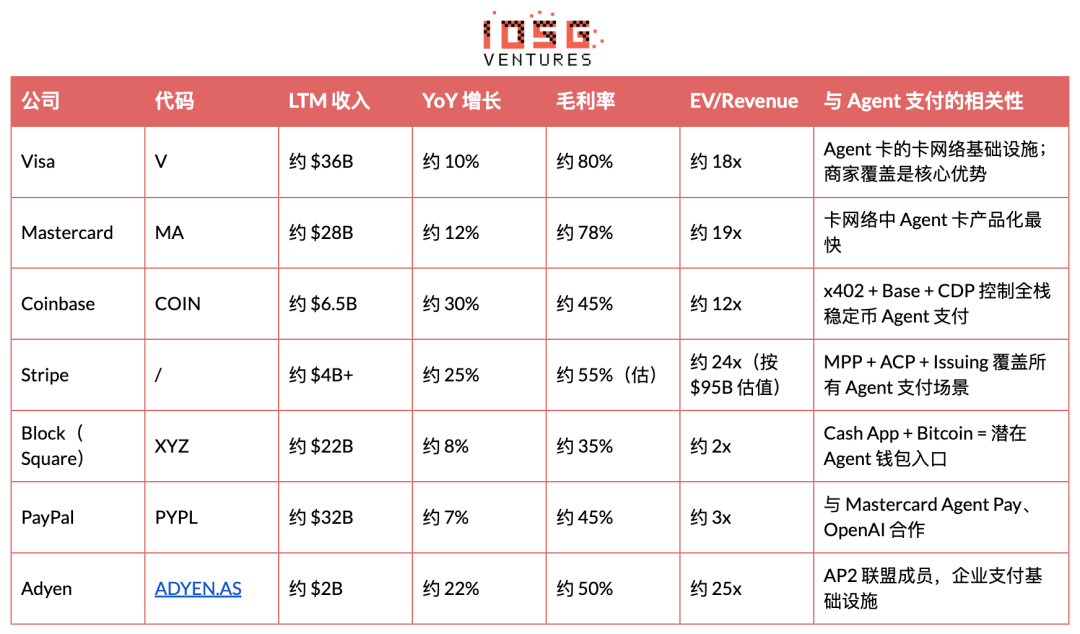

The most critical power right now is reverse positioning. In the early stages of an industry, startups can only leverage reverse positioning and network effects. Economies of scale and brand strength naturally belong to giants. Visa cannot fully embrace stablecoins without sacrificing $32 billion in annual interchange revenue—this is the only structural advantage window for startups.

Power evolution forecast: If Visa adapts to stablecoins within 2-3 years (via VTAP), the reverse positioning advantage disappears, and switching cost becomes the only remaining Power for startups. This means the most investable opportunities today are facilitators that can build high switching costs within the reverse positioning window—namely, deep API integration + key custody + spending strategy lock-in.

Investability of sub-sectors

Investment priority (high to low)

· Facilitator layer (value capture, score 8/10)

The value paid by the Agent does not belong to the protocol layer, but to the person who finds real use cases and serves real users. The Facilitator completely abstracts away the complexity of the chain and the Agent.

· x402 and MPP are open, commoditized pathways. The Facilitator sits between the protocol and users, handling payment verification, on-chain settlement, and cross-chain bridging.

· Control the Agent's signing key and spending policy (an unbreakable trust anchor). Also receive托管 fees and order flow revenue.

· The exit path through acquisition is clear, with Stripe's $1.1B acquisition of Bridge as the benchmark.

· Key to success: Execute solid grassroots marketing in a specific vertical (prediction markets, pay-per-query data, API monetization). Achieve chain-agnosticity early. Build a developer-friendly SDK. Compete on reliability and settlement speed, not price.

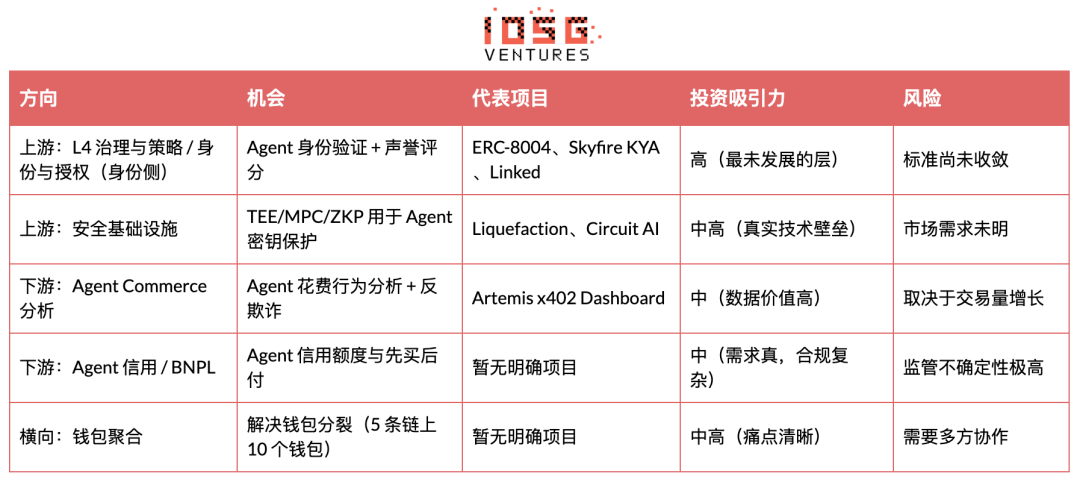

· L4: Governance and Strategy / Identity and Authorization Identity Side (Highest alpha, score 7/10)

· There is a complete absence of a trust layer for Agent business. There is no standardized way to verify who the Agent is, what permissions they have, or whether they are trustworthy.

· ERC-8004 and the Metaplex Agent Registry are early but trustworthy. The ZKID prototype is expected to enable Agent verification with privacy preservation.

· NIST has begun addressing AI Agent Identity and Authorization, indicating that this will become a regulated category.

Whoever controls the trust graph becomes the default identity layer, and the winner takes all.

· Key to success: Build a cryptographic identity (a signed credential binding the Agent to the principal and its scope of permissions), not just an OAuth wrapper. Capture the trust graph early to trigger network effects. Integrate at the wallet/infrastructure layer—prompt injection cannot override it.

· L6: Agent coordination (score 7/10)

The next phase is coordinating the group (finance, compliance, and risk agents working together).

· Key to success: Implement cryptographic verification for Agent outputs.

· L7: Data and Compliance (Score: 6/10)

· Audit trails are themselves a dispute resolution mechanism.

· Key to success: Enable real-time cross-chain transaction reconstruction. Integrate Travel Rule compliance directly into the payment flow.

· L5: Skills Discovery and Store (Rating 6/10)

· 11,000+ MCP servers, monetization rate < 5%. This is the 'App Store' moment for Agent capabilities.

Whoever becomes the default discovery layer simultaneously controls routing and payments—the position of Google combined with Stripe.

Key to success: Aggressively aggregate supply and build a payment-native discovery mechanism.

· L1: Wallet and Key Management (Score: 7/10)

· 10+ players, but may concentrate quickly.

· Fleet management (Sponge) and framework-agnostic support (LobsterCash/Crossmint) are differentiators.

· Key to success: Secure framework-level default integration with LangChain, CrewAI, and Claude Code. Launch a strategy engine featuring a "five-pillar" framework, including spending limits, counterparty whitelisting, trade type restrictions, time-based controls, and upgrade thresholds.

Unit Economics (Facilitator Layer)

Model the P&L for a typical Facilitator startup across three stages:

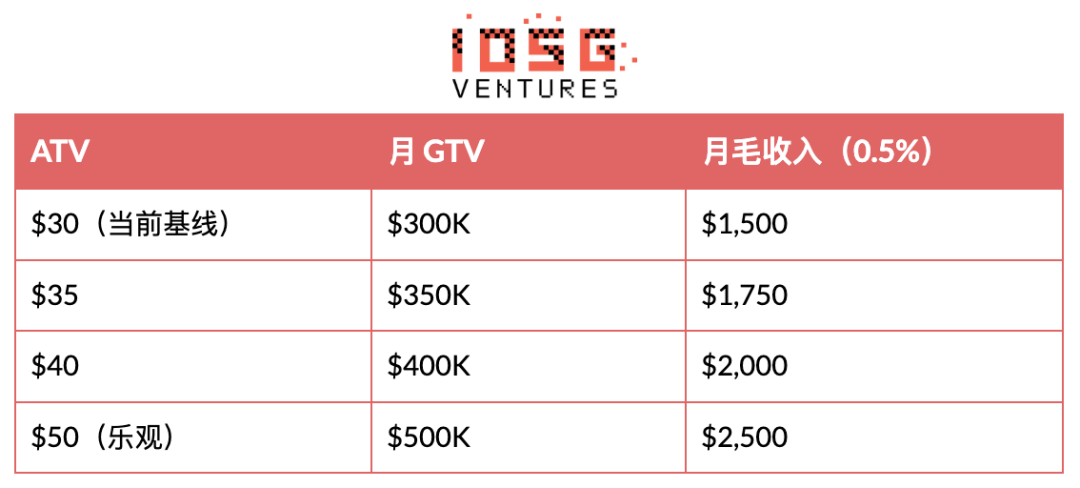

ATV Sensitivity Analysis (Y1, 500 Agents × 20 Transactions per Month):

ATV is the lifeblood of the entire business model. The era of $0.09 microtransactions is over. Agent shopping/self-purchasing is becoming the primary use case. The next inflection point is ATV rising from $30 to $50+. Leading indicator: Which payment MCP server becomes the default integration in Claude Code, LangChain, and CrewAI.

Minimum viable trading volume test. At a 0.5% take rate, a Facilitator would need $200M annual GTV to achieve $1M ARR, or $550K per day. The current daily GTV of the entire x402 ecosystem is approximately $2.7M (Artemis, April 2026), implying a theoretical ARR ceiling of about $4.9M (if a single Facilitator captures 100%):

The entire x402 ecosystem, with a 0.5% take rate and daily GTV of $2.7M:

· Annual Facilitator Income: $2.7M x 365 x 0.5% = $4.9M

· Has surpassed the $1M ARR threshold

· $10M ARR: Requires twice the current trading volume

· $100M ARR (growth stage): Requires 20 times the current trading volume

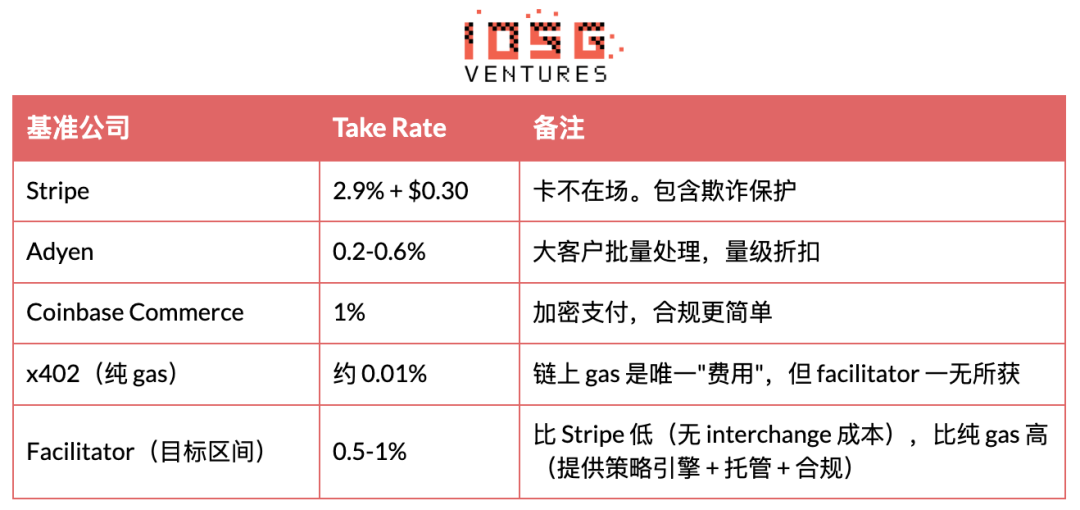

Take Rate Benchmark:

Mature company comparison

Publicly traded payment companies trade at EV/Revenue multiples between 12x and 25x. An agent-based payment startup that achieves $50M+ in ARR with 50%+ growth could be valued at over $1B based on a 20x revenue multiple. However, no company in the industry has disclosed revenue data, and valuations are currently based entirely on narrative premiums.

Forecast

Decision tree

Core issue

Can Agent Payment reach $1B in annual transaction volume before 2028? This splits into two paths.

Path 1: Achievable (55% probability). Trigger: Stripe MPP validation of PMF combined with Visa Agent card coverage for millions of users. Under this path, two sub-outcomes:

· The stablecoin rail has become the default (accounting for 30% of this branch). Coinbase and the x402 ecosystem capture the most value, the card network is bypassed, and Facilitator valuations fall in the $500M to $1B range.

· Card channels still dominate, with stablecoins serving as a M2M supplement (accounting for 70% of this segment). Visa, Mastercard, and Stripe capture the main volume. Pure crypto solutions have become niche, with facilitators either acquired by Stripe or marginalized.

Path 2: Not achieved (45% probability). Catalysts are Agent reliability failing to meet payment-grade trust, or ongoing standard fragmentation. Two sub-outcomes:

· Slow growth to $200M to $500M (60% of this segment). The market exists but faces valuation pressure, requiring startups to have a longer runway.

· Base model companies build their own payment systems (accounting for 40% of this segment). OpenAI and Google natively integrate payments, eliminating third-party facilitators.

Growth timeline

Reverse stress testing

Risk 1: Giants build their own payment systems, rendering middleware obsolete

OpenAI, Google, and Apple control over 90% of AI agent user entry points, enabling native closed-loop payments (ChatGPT + card linking, Gemini + Google Pay, Siri + Apple Pay).

When Google AP2 launched, it claimed a "full闭环 Agent payment within the Google ecosystem" with 60+ partners. The OpenAI Operator is already capable of completing web purchases. Apple Pay has historically eliminated numerous third-party mobile wallets.

Risk two: The market timing is still 3 to 5 years away; investing now is too early.

Unreliable agents, lack of standardized merchant APIs, and insufficient consumer trust are all hard barriers. Seed companies have a 18- to 24-month runway, and the market may not keep up.

The AI payment protocol supported by Coinbase faces a narrative of "demand hasn't arrived yet." Agents frequently lie when executing tasks. Most agents still aren't earning a single dollar.

Stress test results

Of the two risks, timing risk is the most deadly and hardest to refute. Unit economics arithmetic doesn’t lie—the market is still far from investable scale. The platform risk has been partially mitigated by the argument that model companies aren’t good at compliance, but this defense is weakening by 2026: OpenAI has acquired a KYC provider, Google owns Google Pay, Apple has Apple Pay plus Apple Card, and Anthropic’s shareholder roster includes traditional financial investors. Compliance capability is no longer a moat for model companies’ credibility.

The single largest and non-negotiable risk is timing. Moving from the introduction phase to early growth depends on ATV transitioning from micropayments to commercial-grade usage, which in turn depends on two external variables beyond the investors' control: Agent reliability and merchant coverage.

Three adjustments to the investment strategy:

Allocate 60% of the Agent's payment exposure to the seed round to reserve sufficient follow-on funding for the bridge round (to hedge against timing risk).

2. Prioritize facilitators that are currency-agnostic (supporting both stablecoins and cards) to hedge against regulatory risk.

3. Set an 18-month kill switch: If no facilitator achieves monthly trading volume exceeding $5M by Q4 2027, consider impairment or discounted disposal.

Investment advice

Agents require payment capability as a logical necessity, but the current market is extremely early (only $6.3M since early 2026), with severe wash trading, fragmented standards, and giants ready to crush startups at any moment. The argument is not “this market is big now,” but “this market will grow, and the valuation window before it does is favorable.”

Geographically, the focus is in the United States, compliance hedging is done in Europe, and Asia is a wildcard.

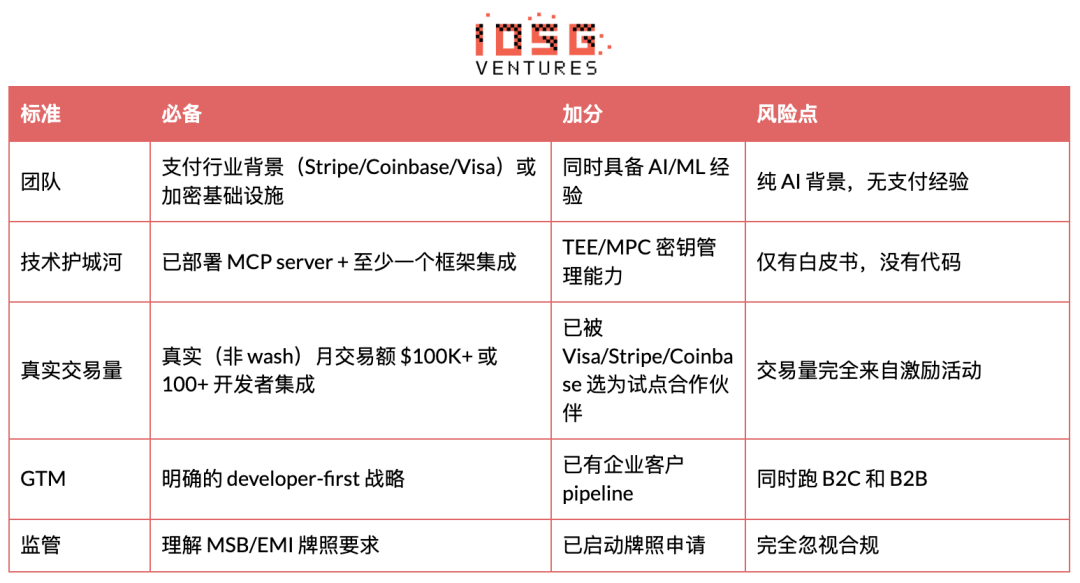

Teams worth investing in have a payment industry DNA (Stripe, Coinbase, Visa) or crypto infrastructure background, have deployed an MCP server with at least one framework integration, generate real, non-wash monthly transaction volume of $100K+ or have 100+ developer integrations, plus a clear developer-first GTM strategy.

Points to avoid include projects with only an AI background and no payment experience, projects with only a whitepaper, trading volume entirely driven by incentives, simultaneously operating B2C and B2B models, and complete disregard for MSB/EMI licenses.

Original link

Click to learn about the open positions at BlockBeats

Welcome to the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia