Author: Max.s

As the geopolitical situation in the Middle East sharply deteriorates, the conflict between the U.S., Israel, and Iran is pushing global commodity markets toward a new extreme of volatility. Against this macro backdrop, a phenomenon once confined primarily to crypto-native narratives is now unfolding in reality: decentralized exchanges (DEXs) are taking over the pricing authority for tail and sudden risks in traditional commodities.

As of March 11, the trading volume of the WTI crude oil perpetual contract (WTI-USDT) on Hyperliquid, a decentralized derivatives exchange built on an application chain architecture, surpassed $1.3 billion (with a 72-hour trading volume exceeding $4.5 billion and open interest fluctuating between $169 million and $183 million). This figure not only elevated it to the second-largest trading pair on the platform after Bitcoin, but also marked a substantive expansion of the boundaries of crypto finance. Intensive coverage by institutions such as InvestingNews, The Block, and CoinMarketCap confirms that this liquidity spillover is not an accidental hype, but an inevitable outcome of global capital seeking a "24/7 safe haven" amid extreme geopolitical volatility.

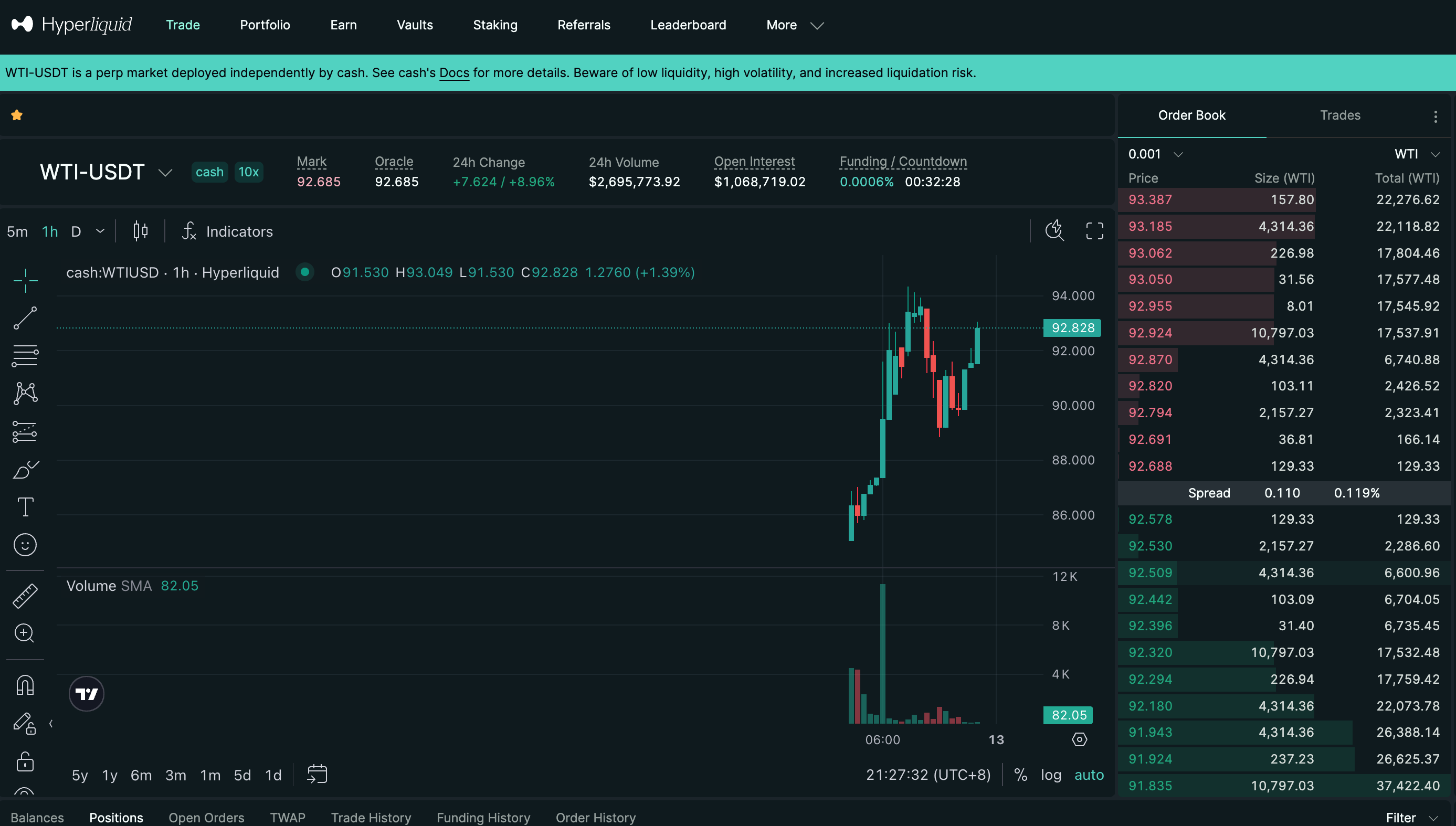

From the data snapshot of the trading terminal, we can clearly see the intensity of this capital battle: the mark price of WTI-USDT surged violently to $94.351 in a short time, achieving a remarkable 9.99% gain over 24 hours. A series of consecutive green candles rising sharply on the K-line chart, accompanied by a surge in trading volume, perfectly mirrored the panic buying seen in traditional energy markets during times of war threats.

However, what deserves our deeper consideration is: when oil, the most traditional physical asset, is heavily traded on a crypto-native DEX in the form of perpetual contracts, what hidden shift in pricing power does this signify?

Traditional commodity markets, such as the CME or NYMEX, operate on fixed trading hours, price limits (circuit breakers), and strict clearing access. This structure effectively manages risk during normal market conditions but can often become a liquidity bottleneck during sudden "black swan" events.

Geopolitical conflicts often escalate regardless of Wall Street’s trading hours. When attacks occur during weekends or market holidays, global macro hedge funds, multinational energy traders, and speculative capital suddenly face significant exposure risks without access to counterparties in the traditional financial system.

At this time, the 24/7, permissionless, and highly efficient crypto market has naturally become the "always-on alternative" for meeting these hedging and speculative demands. The emergence of high-performance order-book DEXs like Hyperliquid has precisely filled this infrastructure gap. Unlike early automated market makers built on Ethereum mainnet, Hyperliquid leverages a customized L1 application chain to deliver sub-second latency and zero gas fees, while its frontend interface—featuring depth charts, funding rates, limit orders, and take-profit/stop-loss functions—matches the professionalism of centralized exchanges and approaches that of traditional financial trading terminals.

Daily trading volume of $1.3 billion is not just a number—it’s real capital voting with its feet. It demonstrates that the infrastructure of the crypto market has matured enough to absorb macro-level liquidity in the billions. Amid the oldest macro命题 of "war and oil," cryptocurrency offers a completely new liquidity escape route.

To explore the deeper implications of this phenomenon, we must confront a core proposition: the shift in pricing power.

In traditional contexts, derivative pricing relies on the spot market. On DEXs, synthetic assets typically obtain the off-chain asset price via oracles as an index price to anchor their value. However, during extreme market conditions when traditional markets are closed, a fascinating quantitative博弈 mechanism comes into play.

When the traditional oil market closes, the spot price reported by the oracle remains stagnant (shown as 92.828), but the on-chain mark price (shown as 92.685) continues to rise due to buying pressure. At this point, the WTI-USDT price is no longer determined by spot traders in New York, but is instead driven purely by on-chain supply and demand.

When the on-chain mark price deviates from the stale oracle price, the smart contract automatically adjusts the funding rate. Long positions must pay a very high rate to short positions. For quantitative arbitrageurs, if they anticipate that traditional market oil prices will rise less than the on-chain premium after opening, this presents an excellent short arbitrage opportunity; conversely, if geopolitical tensions worsen dramatically, longs may prefer to pay high funding rates to secure early long exposure.

During this process, the DEX effectively replaced the CME as the sole globally valid price discovery center for WTI crude oil during market closures. On-chain order book depth, long/short ratios, and mark price trends formed the most accurate “forward guidance” prior to the traditional market’s opening on Monday.

The effective operation of this mechanism marks the rise of decentralized pricing power. Previously, the crypto market passively accepted the pricing of real-world assets (RWAs); now, under specific time windows and extreme liquidity demands, the crypto market is actively pricing real-world assets in return. This represents a qualitative shift from “passive mapping” to “active market making.”

In recent years, "tokenization of everything" has been one of the most ambitious narratives in the crypto industry. However, over the past cycle, the primary real-world use cases for RWA have been limited to yield-bearing stablecoins and tokenized U.S. Treasuries (such as MakerDAO and Ondo Finance). These assets are characterized by low volatility and heavy compliance, essentially bringing traditional finance yields on-chain, and fall under the category of "static RWA."

The surge in WTI perpetual contracts on Hyperliquid has launched the second half of the RWA narrative: decentralized derivatives trading for high-frequency risk assets (dynamic RWA).

The market has moved beyond the cumbersome and illiquid spot tokenization of “how to register a barrel of physical crude oil on the blockchain,” instead bypassing spot ownership entirely and reconstructing commodity exposure on-chain using smart contracts, oracles, and margin systems.

For professional financial traders, buying WTI futures is essentially about gaining cash flow exposure to rising oil prices, not about actually receiving hundreds of barrels of crude oil on the delivery date. If a decentralized application chain can offer sufficient liquidity, extremely low trading slippage (estimated slippage of 0% in the chart), and the security of decentralized self-custody, then trading synthetic WTI on-chain is financially indistinguishable from trading WTI futures on the CME.

More importantly, this model breaks down geographical and access barriers: whether institutional traders on Wall Street or independent quant traders in emerging markets, all can share the same seamless, borderless liquidity pool. This inclusivity and efficiency demonstrate that the practical value of RWA has decisively moved beyond purely crypto-native narratives and entered the depths of macrofinance.

The 2026 oil price war, triggered by geopolitical crises, unexpectedly became an epic stress test for decentralized finance infrastructure. The $1.3 billion in trading volume on Hyperliquid is not merely a striking transaction figure—it is a clarion call for crypto finance to enter the global macro pricing system.

The ancient rivalry between war and oil has found a new arena in the code of blockchain and smart contracts. As traditional financial giants return to their desks on Monday morning, they may be surprised to discover that weekend conflicts have not only altered the world map but also invisibly reshaped the global financial trading landscape. The crypto market is no longer merely a playground for tech enthusiasts—it is now undeniably serving as the global risk-pricing “24/7 backup engine.”