Author: David, DeepTide TechFlow

In 2025, the predicted total market trading volume for the entire year is $44 billion.

Polymarket reached $3.34 billion in trading volume, while Kalshi reached $4.31 billion. One is a blockchain-based "truth engine," and the other is a CFTC-regulated "event exchange." The two have been competing all year, from betting on the U.S. presidential election to Venezuelan coups, from the Super Bowl to the Federal Reserve's interest rate hikes. By the end of the year, even the parent company of the New York Stock Exchange, ICE, entered the scene and invested $2 billion in Polymarket.

Prediction markets have become one of the fastest-growing sectors in the cryptocurrency space in 2025.

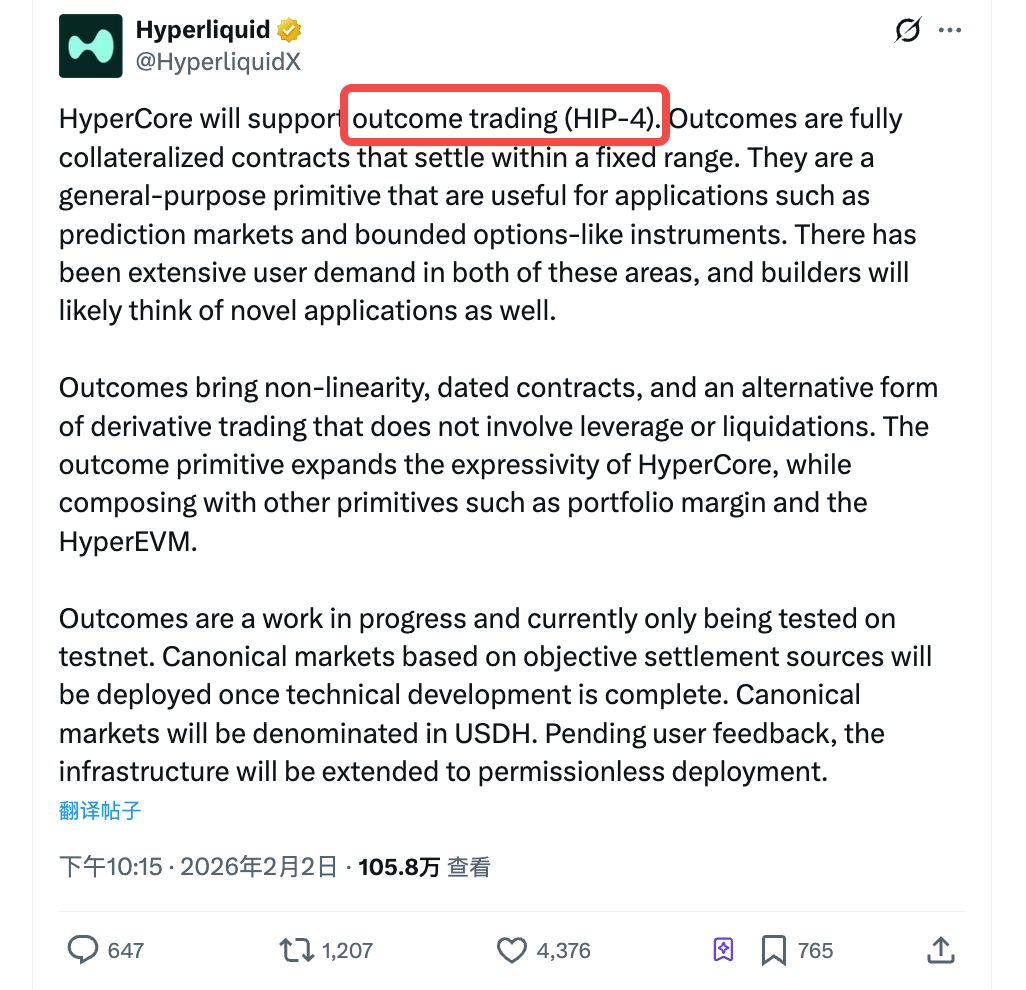

On February 2nd, Hyperliquid announced the HIP-4 testnet launch. According to the official description, it is "outcome trading," meaning trading on outcomes. These are fully collateralized contracts that settle within fixed price ranges, suitable for prediction markets and options-like products.

The news came out, and HYPE rose by 10%. It has gained more than 40% over the past week; in contrast, BTC fell to as low as $75,000 during the same period.

The market clearly views HIP-4 as positive news. However, if you only interpret HIP-4 as "Hyperliquid entering the prediction market," you may be underestimating the intention behind this move and misjudging Hyperliquid's value within the current crypto ecosystem.

First, let's explain what HIP-4 is.

Hyperliquid's core business previously focused on perpetual contracts (perps): contracts with no expiration dates, leveraged positions, and the risk of liquidation. This is the largest category in on-chain derivatives trading and the main source of Hyperliquid's revenue.

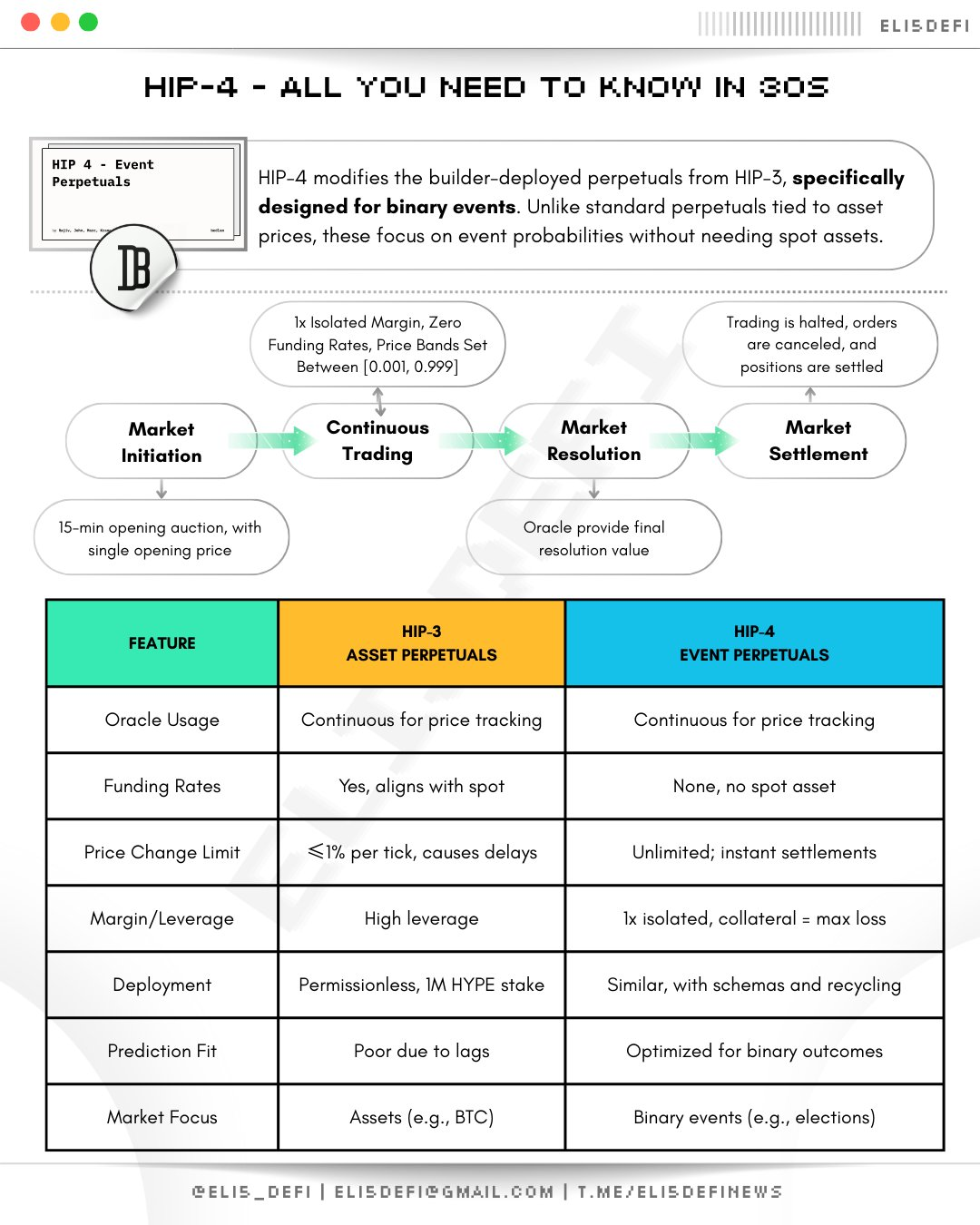

But the outcome contract introduced by HIP-4 is almost the opposite.

There is an expiration date, full collateralization, no leverage, and no liquidation.The contract is settled within a fixed price range, and the buyer can lose at most the principal amount, without owing money to the platform.

For example.

If you believe that BTC will rise above $100,000 before the end of March, you can buy a corresponding outcome contract. When the contract expires, if BTC indeed breaks through $100,000, the contract will settle at the upper limit, and you will make a profit; if it does not, it will settle at the lower limit, and your loss will be limited to the initial cost of purchasing the contract. There is no need for additional margin, and you won't face liquidation in the middle of the night.

This structure naturally fits two types of scenarios:Prediction markets (betting on event outcomes) and options-like products (expressing directional views within a fixed range).

On Polymarket, when you bet on "whether Trump will be re-elected," it's essentially based on the same logic. It requires full collateral and uses binary settlement.

HIP-4 generalizes this logic into a primitive operation, not limited to yes or no; it supports continuous price ranges.

(Image source:Sure! Please provide the content you would like me to translate from Chinese (zh_CN) to English (en_US).)

Currently, HIP-4 is still in the testnet phase.

After the official launch, the first batch of markets will be curated by the official team and priced in USDH (Hyperliquid's native stablecoin). Subsequently, we plan to open up permissionless deployment based on user feedback, meaning that anyone will be able to create outcome markets.

Does this sound like "a Hyperliquid version of Polymarket" to you?

It's not that simple.

Composability, overheard many times but the most valuable.

Polymarket is a decentralized prediction market platform.

The contracts you purchase here have no relation to your positions on Aave, your liquidity on Uniswap, or any positions on other protocols. The same applies to Kalshi. Each contract is an isolated island.

HIP-4 is different. The Outcome contract runs directly on HyperCore, sharing the same trading engine and unified cross-margin system with perpetual contracts.

After the release of HIP-4, Ignas, a well-known DeFi researcher from the international community, pointed out a classic scenario:

While holding a long ETH perpetual futures position, you can also purchase an "outcome" contract that pays out if ETH falls below a certain price on the expiration date. These two positions, under the same margin account, hedge each other. The system automatically identifies the reduced risk exposure and releases excess margin.

Translate from zh_CN into en_US.

You use one position to express a directional view and another position to hedge, and when combined, the total capital required is less than opening a single position.

This is called a structured product in traditional finance.

Investment banks help institutional clients create such portfolios and charge hefty fees. Now, Hyperliquid aims to natively implement this on-chain, eliminating intermediaries, with contracts automatically recognizing hedging relationships.

Polymarket can't do this, nor can Kalshi. They are standalone event exchanges, not derivatives engines.

Therefore, the outcome contract of HIP-4 is more of a primitive that enhances Hyperliuqid itself, rather than a product; it's a building block that can be assembled with other components.

Prediction markets are just the most obvious use of this building block.

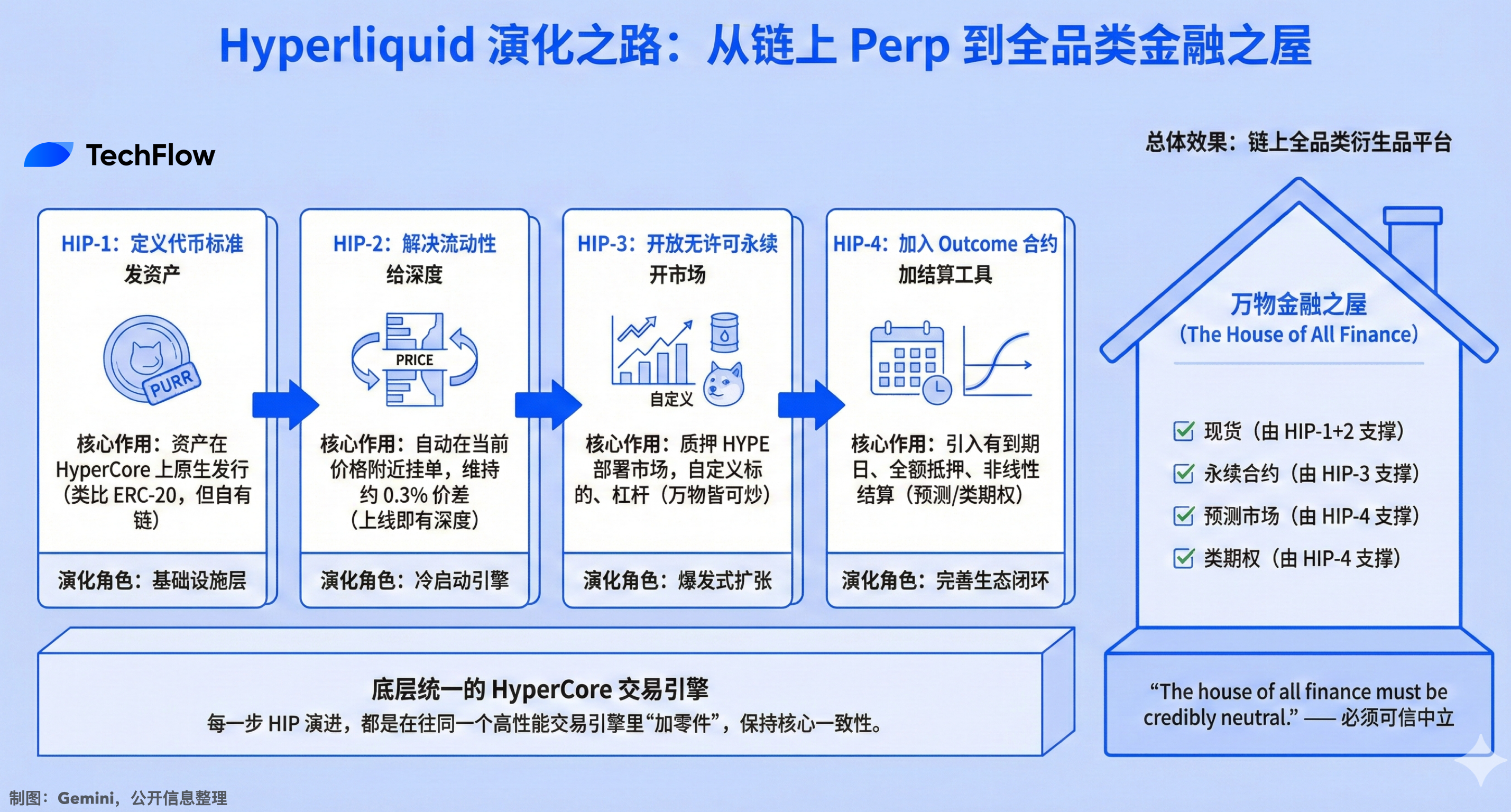

From HIP-1 to HIP-4: The Four-Step Approach to On-Chain Perpetuals

Putting HIP-4 into the context of Hyperliquid's product evolution makes the logic clearer.

HIP-1, define the token standard.

Launching in 2024, it will allow any asset to be natively issued on HyperCore. The first token minted using this standard will be PURR. It is equivalent to Ethereum's ERC-20 standard, but it runs on Hyperliquid's own blockchain.

HIP-2, solving liquidity.

Automatically place buy and sell orders around the current token price, maintaining a spread of approximately 0.3%. The token has depth from the very first second it launches, eliminating the need to wait for market makers to enter.

HIP-3, permissionless perpetual contracts.

Anyone who stakes 500,000 HYPE tokens can deploy their own perpetual contract market, customizing the underlying asset, oracle, leverage ratio, and collateral type. Since its launch, the platform has accumulated nearly $42 billion in trading volume, with an open interest exceeding $1 billion. Markets range from stocks and commodities to meme coins — you name it, someone has created a market for it.

HIP-4, add the outcome contract.

Expiry date, full collateralization, nonlinear settlement.

If you look at these four steps together, they closely resemble the continuous iteration and growth of an internet product: issuing assets, providing liquidity, launching a derivatives market, and adding settlement tools.

From this point on, Hyperliquid has evolved from a perpetual contract DEX into a comprehensive on-chain derivatives platform covering spot, perpetuals, prediction markets, and option-like products.

Each step is adding parts to the same trading engine.

Jeff Yan, the founder of Hyperliquid, once said:

"The house of all finance must be credibly neutral." — The house of all finance must be credibly neutral.

Four HIPs are more like the four walls of this house.

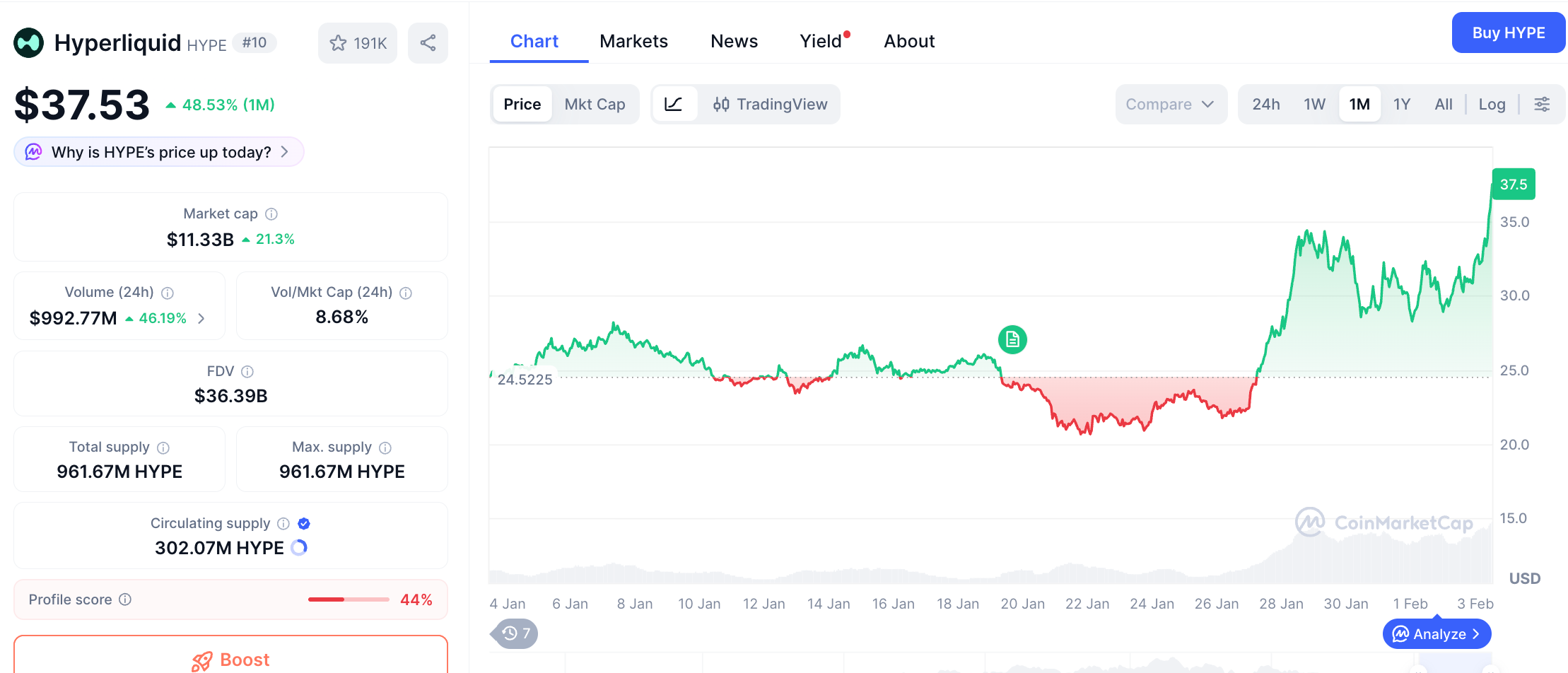

Pricing for $HYPE

HYPE has risen more than 40% in the past week. The broader market is bleeding, but HYPE is going against the trend.

This achievement is certainly not entirely due to the HIP-4 message.

Over the past few weeks, several developments have been brewing at Hyperliquid simultaneously: the permissionless perpetual contract market under HIP-3 has been consistently seeing increased volume, hot precious metal trading has generated impressive data, and the HYPE buyback mechanism has been continuously accumulating tokens. Notably, 97% of the platform's trading fees are used to repurchase HYPE.

But on the day of the HIP-4 announcement, HYPE rose by 10%, indicating that the market at least considers this information valuable.

What the author needs to emphasize is the role of USDH.

All outcome contracts of HIP-4 are settled in USDH. USDH is Hyperliquid's native stablecoin issued by the Felix Protocol, backed by short-term U.S. Treasury bonds. Its earnings are used to repurchase HYPE and incentivize DeFi activities within the ecosystem.

This further strengthens the previous flywheel:

More product types launching (perpetuals for HIP-3, outcomes for HIP-4) → increased trading volume → more trading volume generates more trading fees → fees used to repurchase HYPE → more markets settled in USDH, increasing USDH demand → USDH's treasury yield further supports HYPE repurchases → HYPE price rises → increases the actual value of staking thresholds for HIP-3 → attracts more capable builders to deploy new markets.

The cycle continues, but it's conditional on Hyperliquid's trading volume maintaining its growth. Additionally, the current cryptocurrency market environment and the projected competition are both quite intense.

Outcome of a contract depends on external data sources. Information such as who won the election, what the price of BTC is at expiration, or whether a certain event occurred must be accurately and immutably fed to the on-chain contract.

Hyperliquid claims to use an "objective settlement data source," but it hasn't specified which oracle it will use or how it will prevent manipulation. In the history of prediction markets, oracle disputes have been the most common trigger for collapses.

Regulation is also a variable.

In January 2026, a Massachusetts judge issued an injunction against Kalshi, which operates under CFTC regulation, ruling that its sports contracts constituted illegal gambling. Even compliant exchanges cannot avoid state-level lawsuits, and decentralized protocols will not remain outside the reach of regulation forever.

There is also a more fundamental issue: how large the demand actually is.

Breaking down the $4.4 billion market, Kalshi is more than 90% sports betting, while Polymarket's volume is concentrated in super events such as elections and geopolitical events. The liquidity for everyday prediction demands remains very thin. Whether HIP-4 can attract new users or is merely an additional button among existing traders, there is no clear answer yet.

But Hyperliquid clearly doesn't want to be the next Polymarket; instead, it aims to make prediction markets a native capability of its existing trading engine, as fundamental and natural as perpetual contracts.

When a Perp DEX begins to evolve, the logic of valuation may change.