On Friday evening, U.S. stocks and CME futures closed, but information impacting the market continued to flow in.

A trader stares at the screen, juggling three simultaneous assessments: he believes the market is underestimating the probability of a drop followed by a rally in BTC due to weekend geopolitical rumors; he thinks the next Fed decision has not yet been priced in; and he wants to buy weekend gap insurance for his crude oil or precious metals positions.

The problem is that these three tasks used to require going to three separate places: betting on long or short positions on a futures exchange, betting on events on a prediction market, and hedging on an options exchange, with margin split across all three. The underlying insight is one unified view, but the positions are fragmented.

Hyperliquid's new market framework, HIP-4, addresses this fragmentation.

What is HIP-4?

HIP-4 turns the "outcome" itself into a tradable, standardized asset, allowing judgments such as "whether something will happen" or "whether a price will reach a certain level at a specific time" to enter Hyperliquid's trading system in the form of standardized assets. It launched on the Hyperliquid testnet on February 2.

A community member recently reverse-engineered the core contract of HIP-4 from the compiled code deployed on the testnet, allowing us to glimpse its architecture ahead of the mainnet launch.

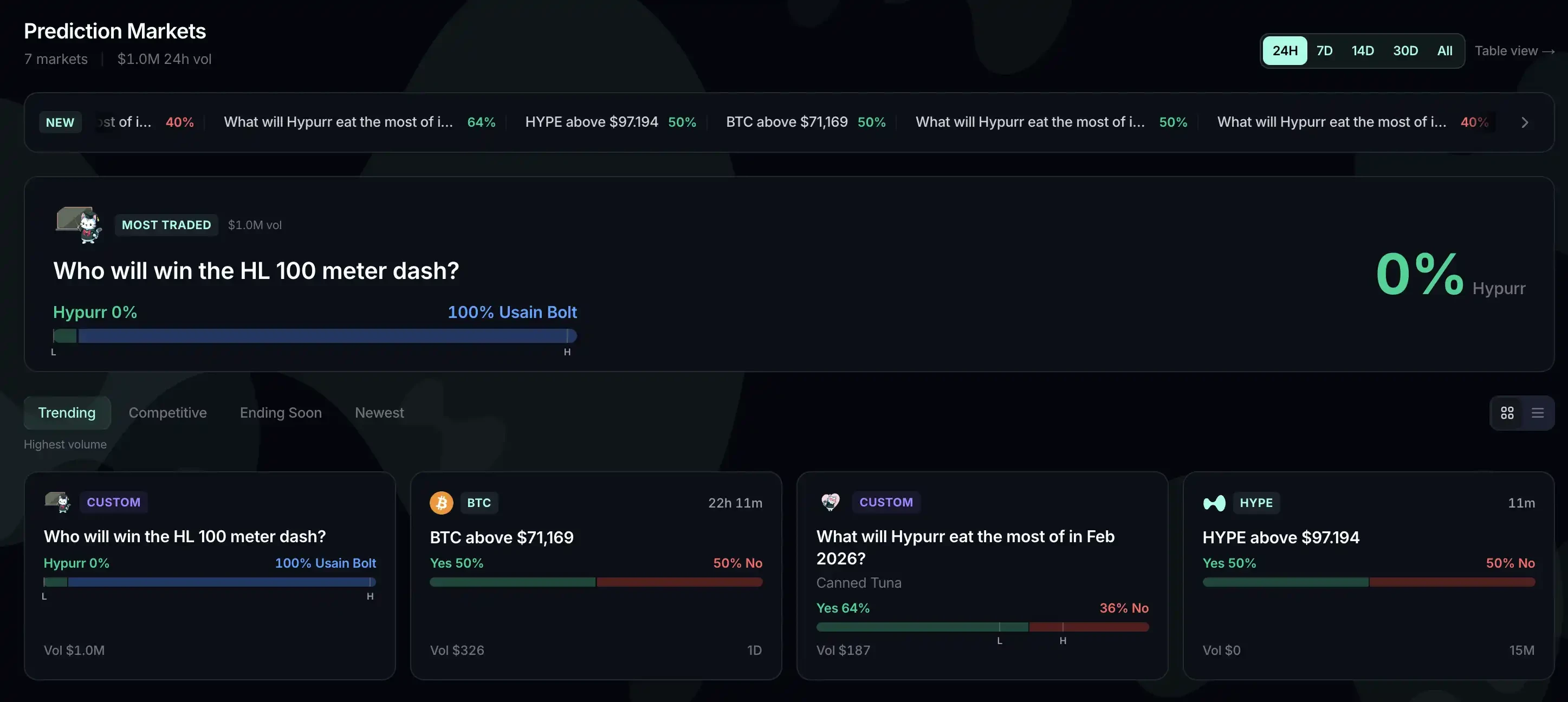

HIP-4 frontend simulated based on the testnet contract

HIP-4 frontend simulated based on the testnet contract

HIP-4 employs a two-layer architecture. Trades occur on HyperCore, while fund custody, prize pool management, and partial settlement take place on HyperEVM. The first layer handles high-frequency matching, while the second manages the more complex contract logic of prediction markets, with clear division of responsibilities between the two layers.

Through HIP-4, abstract "events" can be transposed into truly tradable assets.

Suppose someone creates a market for "Who will win the 100-meter sprint" with event ID 9, where outcome 0 represents "Hypurr wins." This outcome will be mapped to the HyperCore token "#90," which is then listed on the order book for trading. Traders buy and sell it just like a spot asset.

For example, markets similar to options, such as "Will BTC reach a certain price within 15 minutes?", will be settled directly on HyperCore using real-time price data at expiration, without requiring an external oracle.

The settlement rules for event contracts such as "Who will win the 100-meter sprint" have not yet been clearly defined.

Overlapping user profiles with Polymarket

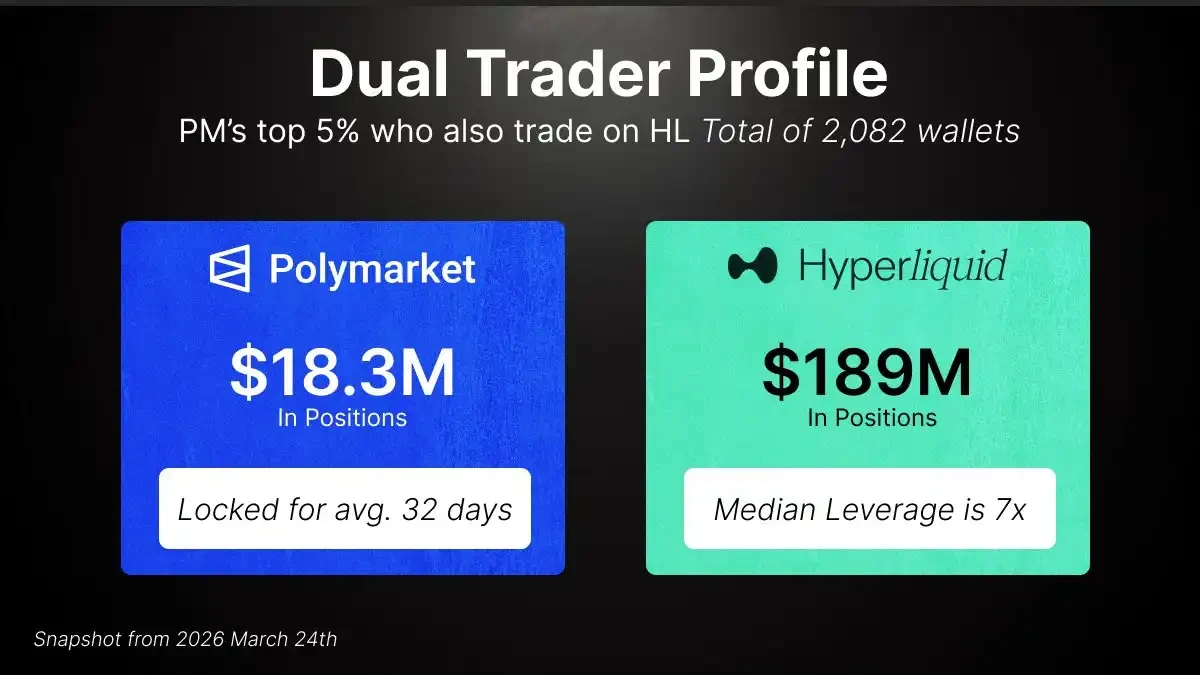

A study analyzing nearly 15,000 active Polymarket addresses found that a group of top traders were also active on Hyperliquid.

These overlapping users generated approximately $1.43 billion in trading volume on Polymarket and held a total of $189 million in contract positions on Hyperliquid, with a margin usage of about $29 million. Their Hyperliquid accounts show a nearly balanced long-short distribution, primarily trading major assets such as BTC and ETH; on Polymarket, they tend to hold longer-term positions on events like elections and Fed decisions. This indicates a group of typical sophisticated traders.

Today, these two positions remain isolated in two separate systems. The $18.3 million in prediction market exposure cannot enter the futures margin system; based on the average leverage of approximately 7x for these overlapping users on Hyperliquid, this theoretically translates to over $120 million in additional trading capacity.

Targeting TradFi's Weaknesses, New Possibilities in On-Chain Finance

HIP-4 envisions greater possibilities in composability.

The community has outlined several categories of potential new products:

Weekend Gap Option: The traditional market has a long gap between Friday’s close and Sunday’s open; HIP-4 can turn this gap directly into a weekend gap option. Traders holding positions in crude oil, silver, or stocks within HIP-3, who are concerned about a sudden gap at Monday’s open, can purchase an option that pays out based on the difference between Friday’s closing price and Sunday’s opening price to hedge against this risk.

Internal-external pricing discrepancy: Compensation for the maximum deviation between internal pricing on HIP-3 exchanges and external oracle prices, hedging against liquidation risk.

Funding Rate Options: Enable traders to hedge against negative funding rates.

These structured tools are precisely what sets HIP-4 apart from traditional prediction markets. The latter often lack natural counterparties, with markets primarily dominated by insiders who continuously exploit uninformed retail traders and market makers.

In contrast, such structured products under HIP-4 have native hedging demand, going beyond mere gambling functions. Market makers’ pricing logic, liquidity quality, and market depth will all enter a new level.

Understanding is never linear, neither should your position be.

The same account, the same margin, and the same settlement system—HIP-4 brings Hyperliquid one step closer to its vision of the “House of All Finance.”