Original Title: PURR』s HYPE Bid Is Not What You Think

Original author: @ericonomic

Compiled by Peggy, BlockBeats

Editor's Note: In the discussion about HYPE in the DAT PURR, the market often focuses on only one question: how many "bullets" are left in its possession to buy HYPE. However, this article attempts to point out that the key is not the balance, but the mechanism. By interpreting the S-1 filing and the issuance logic of DAT, the author reveals a commonly overlooked fact: under the premise of mNAV premium and real liquidity, ATM issuance can allow "firepower" to dynamically expand with trading volume, rather than being linearly consumed.

This also redefines PURR's behavioral motivation, where buying in is not merely consuming capital, but may be maintaining momentum and amplifying future financing capabilities. The article further explains why most DATs fail, and how HYPE avoids typical traps in asset attributes and structural design.

The following is the original text:

Most people pay attention to PURR (previously known as Hyperliquid Strategies or HSI) for one reason: it is one of the DATs of HYPE (and currently the largest one), continuously accumulating HYPE.

So, everyone's mental model is very simple: "PURR still has millions in available funds, so it can continue to hold or drive up the price."

This model is useful. But it is also incomplete.

Because in the background, there exists a mechanism that can silently convert "remaining firepower" into nearly infinite ammunition.

Once you see this clearly, you will no longer view PURR as a "wallet with a balance." You will begin to see it as something else.

Before proceeding, if you would like to learn more about PURR and its relationship with HYPE, I recommend checking out my previous one.that article, especially point 3, in which I specifically discussed this issue, some of the data of which has already become slightly outdated, but we will return to this point later.

All the information in this article is from the same source as before.Officially released S-1 documentIn addition, I will also incorporate some interview content and make a few reasonable assumptions in the text.

Let's get straight to the point.

What else do you need to know besides the fact that "PURR may still hold over $100 million in funds to buy HYPE"?

The core is actually just this: their "firepower" may not just be over 100 million US dollars; it is not necessarily limited by a fixed-size treasury; instead, it can be dynamically amplified by mNAV and market liquidity.

To understand this, we need to start by explaining the basic mechanism of DAT.

The basic mechanism of DAT

Digital Asset Treasury (DAT) is a type of company with the core goal of continuously accumulating cryptocurrency assets. Their funding sources typically mainly consist of three types:

Investors who want exposure to crypto assets at a discount provide cash, and DAT issues them shares in exchange, rather than directly giving crypto assets;

DAT pays cash to cryptocurrency holders who surrender their digital assets in exchange for exiting their crypto positions, but the transaction price is usually lower than the current market price;

Issue and sell new shares (this is critical).

The case of PURR is slightly more complicated because it is the result of a merger of multiple companies; but for the sake of simplifying the discussion, it can first be assumed that it is mainly financed through these two methods, (1) and (2).

One point that needs to be clear is that their core objective, at least in theory, should be to maximize returns for shareholders, rather than to "pump" a certain cryptocurrency.

But in reality, most DATs have taken the old path of "pump-and-dump", ultimately failing almost like a rug pull.

This is exactly where the Market Net Asset Value (mNAV) comes into play. mNAV is an indicator used to determine whether a company's stock is trading at a discount or a premium.

Take a simple example: suppose there is a DAT with HYPE as its core asset: holding 100 million USD equivalent in HYPE; no liabilities, no extra cash; a total of 500,000 shares issued, each share priced at 2000 USD.

Then its mNAV calculation is: (500,000 × 2,000) / 1,000,000,000 = 1

mNAV = 1 means that the company's stock price is reasonably priced.

If the stock price is higher, mNAV > 1, it indicates that the company is trading at a premium;

If the stock price is lower, mNAV < 1, it means trading at a discount.

Now, let's return to the previously mentioned point (3), which is the most critical and yet often overlooked aspect of the DAT mechanism: where the DAT is, and how new shares are issued. This is exactly where the story truly begins to diverge.

Fork Point: How DAT Issues New Shares

Some DATs choose to issue additional shares and sell them at a discount through OTC to specific buyers, while setting a shorter unlock period.

This often triggers the classic "death spiral": as soon as the lock-up period ends, buyers dump their shares en masse; the stock price drops; if further financing is needed, it can only be done at even bigger discounts; the mNAV falls further; and the cycle repeats.

Another category of DATs chooses to issue new shares via the ATM method when mNAV is at a premium.

An ATM (At-The-Market) offering refers to: a company gradually issuing and selling new shares in the open market, while strictly adhering to liquidity and volume constraints.

The pricing of these new ATM shares is not at a discount OTC, but rather anchored to the market price (usually based on VWAP, volume weighted average price).

There is a subtle but very important mechanistic difference, which is particularly critical in practical operation.

Since ATM offerings refer to the VWAP rather than the latest traded price, the current price often briefly exceeds the VWAP in a strong upward trend. At this time, new shares can be absorbed by the market at a slightly lower level than the current price without offering any explicit discount or special terms.

For example: If PURR rapidly rises from $10 to $12 in a day, while the VWAP is still at $10.80, then the ATM new shares are actually sold at about 10% lower than the current price. Although according to the rules, they are still considered to be issued "at market price."

As volume accumulates at higher price levels, the VWAP naturally rises and catches up to the current price.

As you might expect, PURR chose the second path. It is precisely here that things begin to get really interesting.

The next question is: When and how many new shares can PURR issue?

According to part of the interview content, David Schamis (@dschamis) mentioned that when PURR's trading price is higher than 1 times mNAV, they would consider initiating an ATM offering.

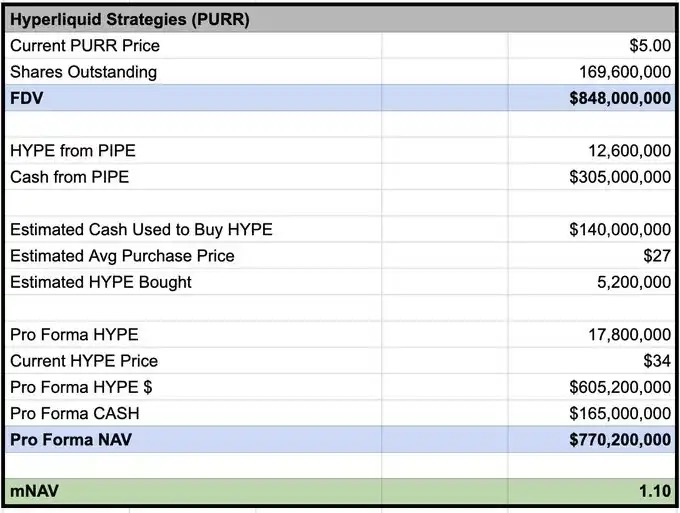

According to @Keisan_crypto's calculation, the current mNAV of PURR is approximately 1.10, which means that they already have the conditions to issue new shares if they wish.

But the question is, how much can you actually earn? Most people stop right here. But the real advantage is exactly where it begins from here.

S-1 Mechanism Not Understood by Most People

According to the S-1 filing disclosure, as an intermediary selling shares on the market, Chardan's beneficial ownership cap is 4.99%. Estimated at current prices, this means it can temporarily hold at most about $50 million worth of PURR stock.

But this does not mean that they can issue at most $50 million of new shares.

What it really means is: At any point in time, Chardan cannot "accumulate" more than this amount of shares. As long as shares continue to be sold into the market and the distribution is completed, more new shares can continue to be issued.

In addition, in practice, Chardan is also subject to trading rules and market manipulation restrictions. Normally, this limits the daily transaction share of ATM issuance to about 20% of the daily trading volume.

Take the most recent trading day as an example: PURR had a trading volume of about 7 million shares (approximately $42 million); at this pace, Chardan can sell about $8.4 million worth of shares daily through the ATM.

Key conclusion (The punchline)

In other words: If the trading volume can be maintained at the current level, PURR could add approximately $8 million per day in "firepower" for buying HYPE.

Once again, this does not mean they will buy blindly or at the top; but the incentive structure here is completely different from that of a PIPE.

PIPE financing: The funds are provided all at once, with no urgency, allowing you to hold cash and wait slowly for a selling opportunity to arise.

ATM issuance: The incentive structure will change.

If the issuance capacity expands with trading volume and momentum, and higher PURR trading volume can continuously open the ATM window, then maintaining HYPE's strong momentum may actually expand future issuance and financing capabilities.

Under this structure, aggressive buying during the upswing is no longer irrational. It can be a means to maintain liquidity, increase trading volume, and maximize the amount of capital ATM can raise over time.

This is not "placing orders with eyes closed." What it means is: under specific conditions, quickly absorbing sell orders, and even adding to the position in the same direction, is itself a rational strategic choice.

This is exactly where most people overlook.

They modeled PURR as a buyer with a continuously decreasing balance; but if the ATM is on (mNAV premium), and liquidity is genuinely present, then the real constraint is no longer: "How much money is left?" but instead becomes: How much liquidity can you continuously supply to the market while maintaining momentum and trading activity, without turning yourself into "the entire market"?

If almost all DATs have failed, why might this time be any different?

Because most DAT failures stem from structural issues and poor asset selection, rather than the idea of "DAT itself being inherently wrong."

They fail, usually because:

1. Poor distribution mechanism

Discounted OTC + short unlock period, essentially creates its own "forced sellers";

2. The underlying assets lack self-sustaining capabilities.

If an asset has (or almost has) no endogenous returns, it must rely on price increases to sustain the cycle; once prices stagnate, the narrative collapses immediately;

3. Inflationary Supply Narrative

If the underlying assets are inflationary (or have heavy emissions), it is equivalent to fighting against structural headwinds;

4. Catastrophic perceptions at the shareholder level

Issuing new shares when mNAV < 1 is self-harm: strong dilution, destroying sentiment, and making the next round of financing worse.

HYPE avoids most of the above failure paths: protocol revenue eventually translates into demand for and value capture of HYPE; under continued usage, the supply becomes deflationary rather than structurally inflationary; there are no large holders or VCs still unlocking their tokens.

This combination is crucial. Because it determines whether this is a story that can only stand on "numba go up," or a structure that can continue to function as long as the fundamentals are not bad, even if the market fluctuates.

Of course, it still has failure paths: mNAV is compressed, volume dries up, ATM halts, or the HYPE narrative weakens. But structurally, HYPE is one of the few assets where the DAT cycle is not naturally a "scam machine."

I've also been "middle curved" here before.

Finally, some people may think: PURR is a bad investment because of continuous share issuance, and additional share offerings will suppress the stock price.

I used to think like this all the time too (typical midcurve). But please remember: when traditional finance truly understands how this "barbell structure" works, things might get extremely exaggerated.

Historical case:

MSTR: 3.3× mNAV

Metaplanet: 8.3×

BMNR: 5.6×

And these targets, to be honest, aren't very good. Imagine how good a "good" one could be.

Turn on the money printer, Bobby.

Hyperliquid.