Author: Van1sa

The dispute between MegaETH and Monad has lasted a long time; in my view, they are textbook examples illustrating two extremes of “how to analyze TVL” and “how to cold-start a new chain.”

The structure of this article:

- Compare the DeFi TVL, stablecoins, and bridged TVL data of the two chains.

- Decomposing the method of packaging MegaETH's TVL

- Mega's TVL is inflated—does that mean Monad wins? Thoughts on bootstrapping new chains

I. Comparison of DeFi TVL, Stablecoins, and Bridged TVL data

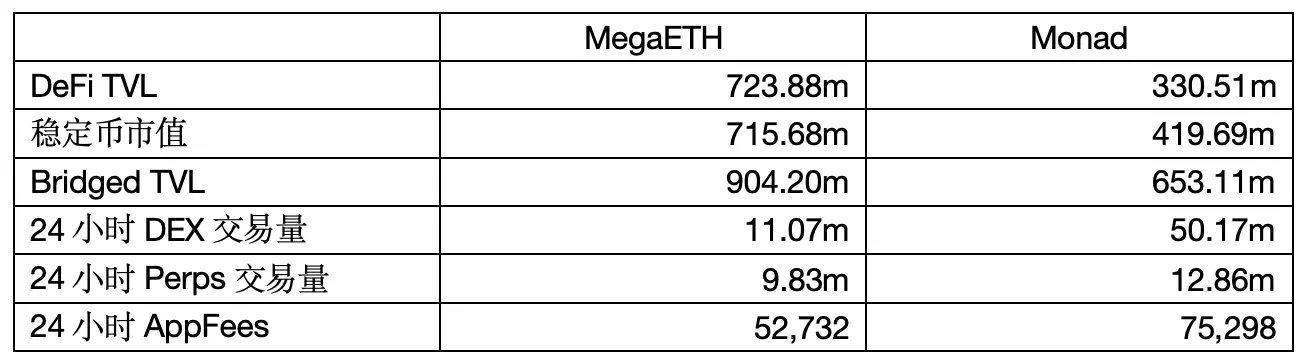

Data source: DefiLlama | Timestamp: May 6, 2026, 12:00

1. DeFi TVL

Only funds that are truly “put into DeFi protocols”—such as when users deposit crypto assets into DEX liquidity pools, lending protocols, or staking protocols—are counted toward TVL.

MegaETH's TVL is more than twice that of Monad, but there are two issues:

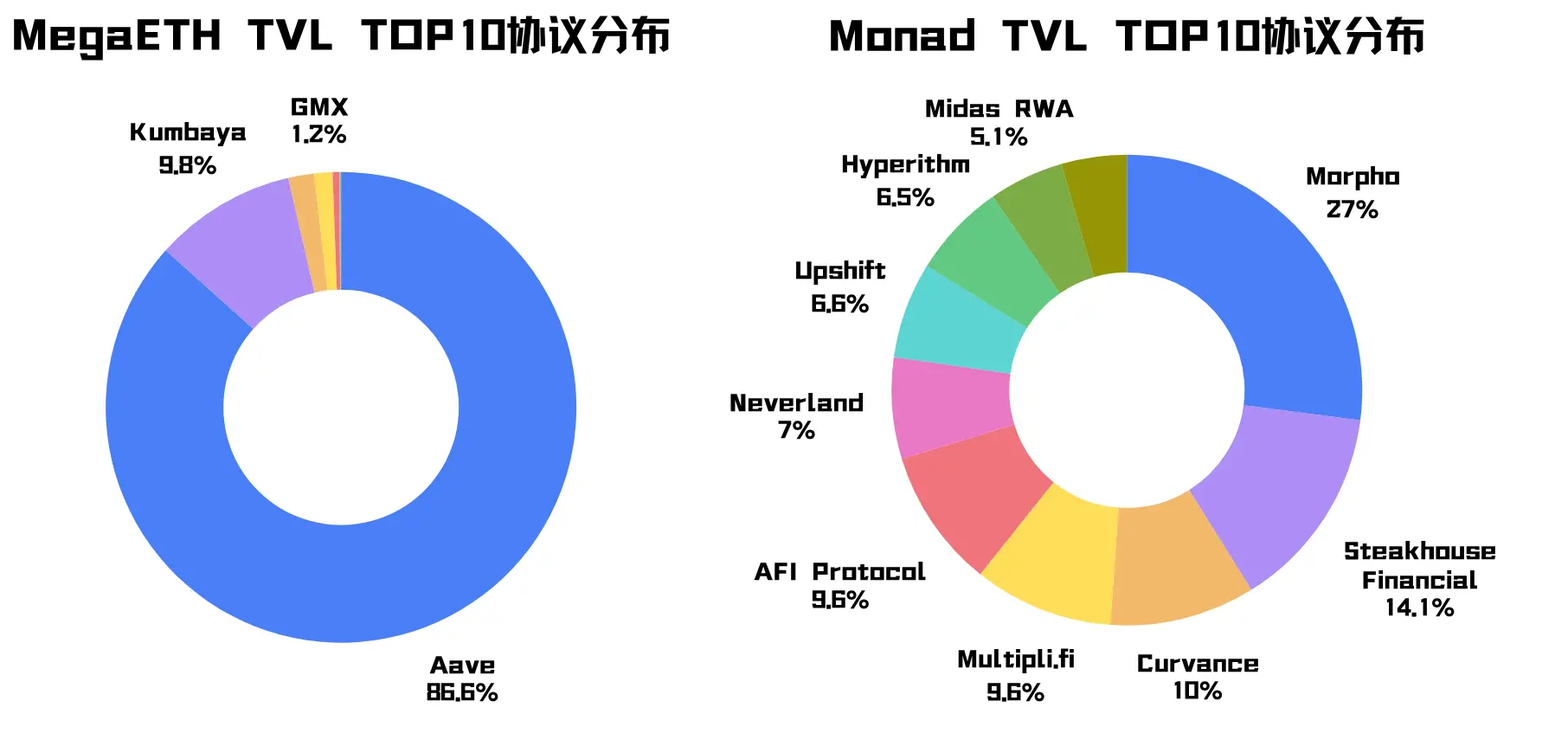

The first issue is that Mega’s TVL is highly concentrated in the Aave protocol (keep this clue in mind); aside from its native protocol Kumbaya, which has a relatively high share, the combined share of the other top 10 protocols is almost below 1%. In contrast, Monad’s TVL is distributed across various protocols.

The second issue is that Mega’s TVL is particularly high, but its 24-hour DEX trading volume and app fees are lower than Monad’s, indicating that Mega’s funds “move more slowly.” Just like reviewing financial statements, you can’t just look at the amount of capital—the speed of capital turnover better reflects the true picture.

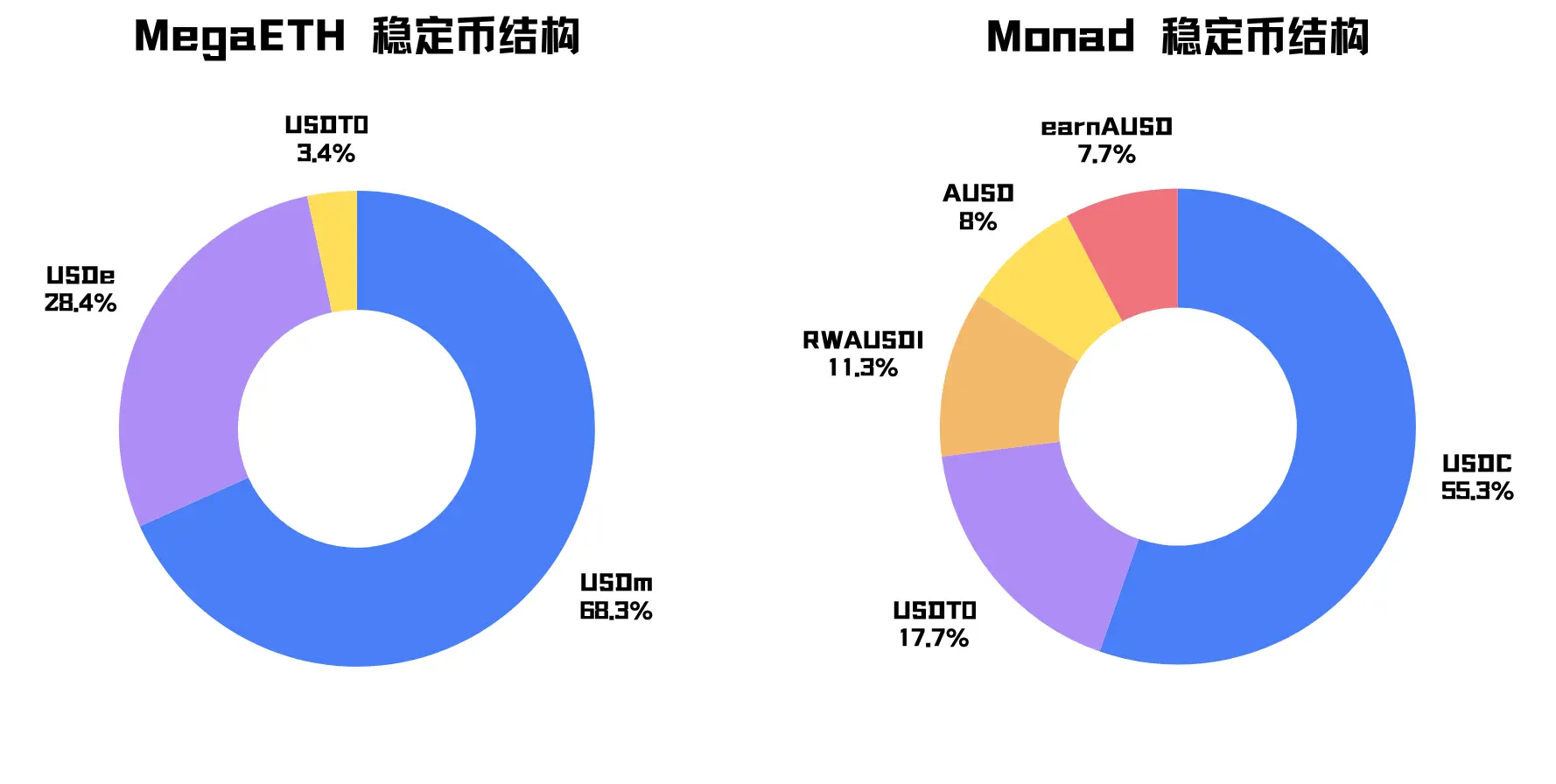

2. Stablecoin market capitalization

The total value of stablecoins issued or circulating on this chain only indicates how much USD liquidity exists on the chain and cannot directly represent the ecosystem's activity.

The market cap of MegaETH's stablecoin is approximately $715.68M, up from under $100M a week ago, closely related to factors such as Mega TGE and Terminal Points farming.

Mega's core stablecoin is USDm, accounting for 68.3% (remember this clue). USDm is Mega's native stablecoin, issued by Ethena's stablecoin stack. The secondary stablecoin is USDe, a synthetic stablecoin issued by Ethena on Ethereum and bridged in.

Mega's stablecoin has a larger scale, but its structure is highly centralized.

Monad's primary stablecoin asset is USDC, with USDT as the secondary stablecoin; both are nearly universal USD-denominated assets with more natural distribution.

3. Bridged TVL:

The total value of assets bridged in from other chains. This number is often higher than DeFi TVL, as many assets arrive via bridges but do not immediately enter protocols—they may simply remain in wallets, waiting for airdrops, events, or ecosystem launches.

I noticed that DefiLlama uses inconsistent methodologies for calculating Bridged TVL for the two chains: Mega’s data includes the native token $MEGA, while Monad’s does not include $MON. Additionally, Mega’s native stablecoin, USDm, is also included in its Bridged TVL.

So here we only look at the percentage of Third Party:

After excluding native tokens, external assets entering Mega via third-party bridges and specific asset channels account for approximately 57.0%, while for Monad, they account for 30.6%.

Liquidity provided by third-party bridges can help new chains achieve rapid cold starts. However, when analyzing the quality of TVL, a high proportion from third parties indicates that funds are more strategic and less stable, primarily following short-term incentives. (This will be demonstrated in detail later.)

Summary: Based on this data, MegaETH appears to be extremely wealthy, but the source of funds, asset types, and protocol承接 methods are overly concentrated, giving a strong impression of being fabricated.

Question the packaging, prove the packaging.

II. The Method MegaETH Uses to Wrap TVL

I previously provided two clues: Aave protocol contributed 86.6% of Mega’s TVL, and USDm and USDe contributed 96.7% of Mega’s stablecoin market cap. Let’s continue the analysis:

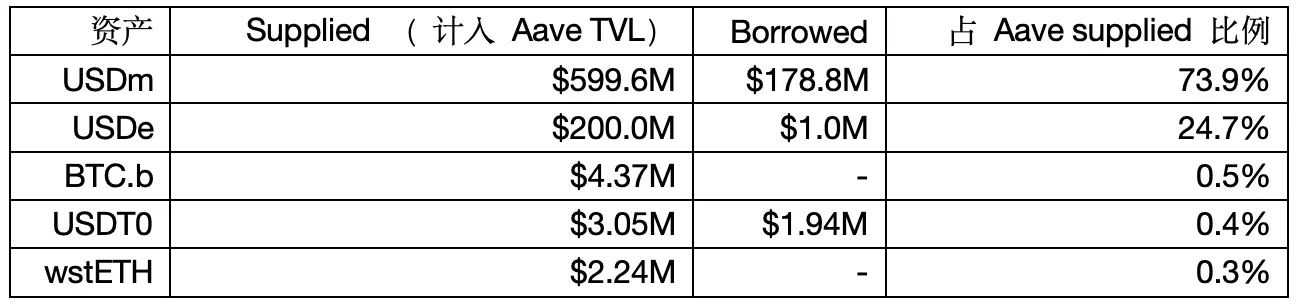

1. Composition of Aave supply and borrowing on Mega

Data source: Aave V3

Note: DefiLlama uses net asset value to calculate Aave's TVL, which may differ from the numbers mentioned above.

The Aave risk team, LlamaRisk, noted that MegaETH exhibits stablecoin leverage cycling behavior.

To cut to the chase: USDe is bridged into Mega solely to serve as collateral for borrowing USDm, which is then deposited into Aave, creating a stablecoin leverage loop that inflates Aave’s supply and borrow metrics.

Evidence 1: The Aave governance proposal explicitly recommends setting up a dedicated E-Mode for USDe on Mega with an LTV of 90% and an LT of 93%. If 200m USDe is staked in Aave, the maximum theoretically borrowable amount is 200 * 90% = 180m USDm, which aligns with the reported borrowing figure of 178.8m.

Evidence 2: By back-calculating using the health factor, if $200M USDe borrowed $178.8M USDm, the health factor = 200M * 93% / 178.8M ≈ 1.04, which perfectly aligns with LlamaRisk’s report stating that active borrowers’ health factors are concentrated between 1.03 and 1.05.

Evidence 3: MegaETH Etherscan shows that the total supply of USDm is approximately 499.5 million, with the Aave contract alone holding about 420 million, accounting for roughly 84% of USDm’s total supply. Subtracting 420 million from the supplied amount of USDm in Aave, which is 599.6 million, also equals exactly 179.6 million.

Even here, you could still call it user incentive behavior, and the $178M in leveraged cycles isn’t counted in DeFiLlama’s TVL—but something still doesn’t add up!

2. The higher the TVL of a lending protocol, the more it may indicate that your token is in low demand.

Under the net value method, the TVL of a lending protocol = Total Supplied - Total Borrowed = Funds available to be lent out.

A higher TVL in a lending protocol isn't necessarily a good thing, so we also need to look at the utilization rate.

Excluding USDm lent through circular leverage, you'll find that the fund utilization rate on Mega's Aave is nearly zero.

The Supply APY for USDm is 5.12%, with 4.76% subsidized by Mega itself, while the Borrow APY is only 1.34%, yet no one wants to borrow because they don’t know what to do with the borrowed funds.

Thus, USDm and USDe are more like display items on Aave, contributing limited real demand to protocol revenue and on-chain activity. Data such as Mega’s App Fee also illustrates this point.

3. The deposits, staking, and lending of USDm and USDe are primarily driven by large holders.

LlamaRisk states: The supply of USDm is highly concentrated, with a single address holding 80%.

Through the previous analysis, we know that the supply of USDe is dominated by a stablecoin circulation strategy, and both the growth rate and health factor distribution indicate that this is highly capital-efficient strategy-driven funding, not organic user deposits.

After removing water, USDm and USDe contributed $620M in TVL through Aave, but these funds are dominated by large holders and are highly strategic.

Summary: Mega's TVL should be viewed with a discount—it's too concentrated, overly purpose-driven, heavily reliant on a few large holders and lending markets, and lacks genuine demand.

It’s not that it’s fake, but Mega’s TVL wasn’t organically grown through its ecosystem—it was artificially crafted and displayed through USDm and USDe within the most basic lending protocols.

Three: Thoughts on Cold Starting a New Chain

MegaETH's TVL is inflated, but that doesn't mean Monad has won. I'm not writing this to criticize Mega—after all, it has made early retail participants profitable—but this article was prompted by some people mindlessly using TVL to attack Monad.

Objectively, Monad’s funding structure is healthier and more diversified.

But it also has a critical issue: on-chain applications haven't yet absorbed these funds.

Five months after mainnet launch, no killing app has emerged; 24-hour DEX trading volume and app fees still fall short of expectations. Monad’s core narrative is high-performance EVM, but what this narrative truly needs to prove is not “I can support many apps,” but “many apps must rely on my performance”—yet at this stage, this remains a hypothetical claim.

The cold start methods for the two chains are two extremes:

MegaETH has created a flywheel using USDm to attract a large number of users and funds in the short term.

Monad is still focused on building infrastructure, onboarding assets, and cultivating developers, allowing users and capital to decide for themselves whether to stay long-term.

Neither method is inherently better or worse, but the risks are completely different:

MegaETH must prove in the future that "these funds won't always rely on wrapping"; Monad needs to figure out how to "long-term retain the money once it comes in."

Funds on new chains often carry speculative expectations. Users bridge assets to new chains to experience applications, complete ecosystem tasks, or pursue potential airdrops and early rewards.

So, instead of focusing on "packaging," we should focus on "absorption." After capital enters, if there aren't enough high-quality applications to absorb it, it will remain stuck in wallets, bridges, a few DeFi protocols, and basic liquidity pools.

Although it's unfair to compare an Ethereum Layer 2 with a standalone Layer 1, I believe the "race" between them is still far from reaching its most exciting phase.

Stop focusing solely on TVL—look instead at whether DEX trading volume can be sustained, whether borrowing demand is growing organically, whether perps, gaming, and consumer applications are gaining traction, whether app fees can steadily increase, and whether TVL will expand from a few core DeFi protocols to a broader range of applications.

If these metrics don't keep up, any kind of cold start will become a ghost chain.