Editor’s Note: Just as the market regains upward momentum driven by liquidity, new uncertainties are accumulating on the other side. The situation in Iran has once again become volatile, with risks emerging in the Strait of Hormuz, bringing geopolitical tensions back to the core variables in asset pricing. Within just a few days, the market has shifted from a single logic of “liquidity-driven” movement to a dual dynamic of “liquidity versus risk events.”

The market is currently caught in a tug-of-war between "liquidity-driven rallies" and "risk shocks from escalating tensions in Iran." On one hand, the Federal Reserve and the U.S. Treasury have injected nearly $200 billion in liquidity into the financial system in a short period, driving a rapid rebound in stocks and risk assets. On the other hand, geopolitical uncertainty, private credit risks, and overheated sentiment continue to leave the market vulnerable.

Within this structure, Bitcoin’s role is beginning to shift. Unlike traditional risk assets, it is more sensitive to changes in liquidity and often provides early signals during shifts in the funding environment. Historically, whether through its early decline in October 2025 or its initial stabilization during this rally, Bitcoin has increasingly served as a leading indicator.

Therefore, the question is no longer just “Will the market rise?” but rather—when liquidity is still being released and geopolitical risks are resurfacing, which force will dominate pricing? If capital cannot sustainably hedge against external shocks, the current rally may merely be a temporary misalignment; however, if liquidity continues, the market could continue rising amid volatility.

Next, the key is not in any single variable, but in their relative strengths. Bitcoin may once again be the first asset to provide the answer.

The following is the original text:

"Oh, think twice, because today is another day you and I are in 'heaven.'" — Phil Collins

For traders and investors, Friday was an unusual trading day. But with Monday still some time away, the market is already brewing new uncertainties—early Saturday morning news reported a shift in Iran’s stance on the Strait of Hormuz, which could once again trigger market volatility.

In addition, Friday's rebound has pushed market sentiment indicators (see below) to a relatively fragile level, making the market more susceptible to a pullback. This has placed the market in a "tug-of-war": on one side, the large-scale liquidity injection mentioned below; on the other, uncertainty stemming from the potential for a renewed shift in the Iran conflict.

What just happened?

Liquidity’s impact on the market is being tested—against the backdrop of potentially escalating volatility from an Iranian war.

Question: What would happen if approximately $200 billion entered the financial system almost simultaneously?

Answer: Asset prices will experience a sharp "melt-up."

Recently, I have been closely monitoring four factors that have collectively suppressed the stock market: the Iran conflict, the liquidity tightening in the financial system that has persisted since January of this year, widespread market pessimism, and insufficient awareness of the true state of the private credit market.

But last week, these factors were almost entirely reversed: liquidity tightening reversed, the situation in Iran appeared to ease, and the pessimism in the market was once again proven—often a leading indicator of potential stock market rebounds.

Have we truly escaped danger? No one can be certain, as tensions in Iran are once again escalating. Additionally, if investors re-enter "panic mode," liquidity could dry up once more. And we still lack a clear understanding of what is truly happening in the private credit market.

However, for now, let’s focus on a relatively observable variable: liquidity.

Double "liquidity tsunami"

If you're wondering where the money that drove the stock market higher over the past two weeks came from—think again: the answer is the Federal Reserve and the U.S. Treasury. Together, they injected approximately $200 billion into the financial system around April 15, providing traders with a "tax day buffer."

First, let’s look at the first “barrel”—the Federal Reserve.

On April 15, the Federal Reserve injected nearly $11 billion into the market through repurchase (repo) operations, using U.S. Treasuries and mortgage-backed securities. While this amount is significant on its own, what’s more critical is that the Fed continues to inject approximately $40 billion per month into the market through its Reserve Management Purchase (RMP) program.

What truly matters is the second "barrel"—the U.S. Department of the Treasury.

According to Garrett Baldwin's analysis, the U.S. Treasury injected approximately $140 billion to $200 billion into the market during the same period. In other words, roughly speaking, without any formal quantitative easing (QE) announcement, the Federal Reserve and the Treasury together quietly injected nearly $240 billion in liquidity into the market.

It’s not hard to understand why the stock market experienced a surge.

The more隐蔽 part: the Treasury's operations

How did the Ministry of Finance accomplish this "covert operation"?

The key lies in one account—the U.S. Treasury General Account (TGA), held at the Federal Reserve. When the balance in this account rises, it typically indicates a tightening of liquidity; when the balance falls, it signals a release of liquidity.

According to Garrett’s calculations, the U.S. government’s balance in this "checking account" at the Federal Reserve dropped from approximately $837 billion to about $697 billion around tax filing season, then rebounded to approximately $924 billion on April 15.

The key point is that approximately $140 billion had already flowed into the banking system before the tax filing deadline, meaning the financial system was effectively in a state of "ample liquidity" prior to April 15.

More interestingly, the National Financial Conditions Index (NFCI, tracked weekly in this report), in its most recent data (April 10), has reversed its previous tightening trend.

We highlighted this change in our daily report on the Smart Money Passport: "The Federal Reserve injected approximately $10.5 billion into the financial system today, while the NFCI index declined for the first time since January 23, 2026. The combination of these two signals may indicate that the Fed has adjusted its stance on liquidity tightening."

The next major question is whether liquidity will take center stage, or if a new escalation in the Iran conflict will once again become the market’s key variable.

Bitcoin is becoming "active": Why it serves as a liquidity barometer

The next movement of Bitcoin is crucial.

Because Bitcoin is more sensitive to liquidity than stocks, its performance following its recent breakout above $75,000—and whether it can challenge the $80,000–$85,000 range—warrants close attention.

From a technical perspective, the resistance zone between $80,000 and $85,000 is not strong. The volume profile (VBP) in this range is thin, indicating that no significant support was formed during the prior decline. Therefore, absent any unusual circumstances, this level should not act as a strong resistance when the price rebounds.

If the price fails here, it signals two things: first, the market lacks confidence in this rally; second, there may be underlying liquidity issues. More importantly, if Bitcoin cannot break through this key range, it could indicate that the "liquidity tsunami" created by the Federal Reserve and the Treasury is rapidly fading.

If $200 billion in bank reserves were absorbed by the market within just a few weeks, it would be a warning sign—potentially indicating that private credit markets or other external risks are building up.

Don’t forget that Bitcoin’s decline in October 2025 accurately foreshadowed the stock market’s struggles in 2026. Meanwhile, Bitcoin stabilized weeks before the stock market hit its bottom and rebounded ahead of the Fed and Treasury’s liquidity injections.

Given the ongoing evolution of the situation in Iran and the persistent global risks, Bitcoin’s weakness should not be overlooked.

The $70,000–75,000 range is a key support level.

Sentiment summary: The market has suddenly shifted broadly optimistic

The CNN Fear & Greed Index (GFI) closed at 68 on April 17, 2026, in the "Greed" zone.

CoinMarketCap’s Crypto Fear & Greed Index stood at 59 early Saturday morning, indicating a slightly elevated "Neutral" level.

The Chicago Board Options Exchange (CBOE) aggregate put/call ratio is 0.65, with the index options put/call ratio closing at 0.82. Overall options market sentiment remains neutral, but is gradually shifting toward the bearish zone as bullish sentiment rapidly strengthens.

The CBOE Volatility Index (VIX) closed at 17.48, a relatively positive level. However, it could still rise above 20 in the short term, which is often viewed as a risk warning threshold.

Note that the VIX typically rises when traders heavily buy put options. Increased demand for puts forces market makers to hedge by selling stock index futures, creating downward pressure on the market.

Conversely, when the VIX declines, it indicates reduced demand for put options and a shift in market sentiment toward optimism, often leading to increased buying of call options. This prompts market makers to buy stock index futures to hedge their risk, thereby increasing the likelihood of upward movement in the stock market.

Liquidity Watch

1. Positive: Liquidity is easing

The latest reading of the Federal Reserve's National Financial Conditions Index (NFCI), released on April 10 for March 27, 2026, was -0.47, down from -0.44 the previous week, indicating a further easing of financial conditions and improved liquidity.

A decline in NFCI is generally viewed as a bullish signal, while a negative index indicates that market liquidity is relatively abundant.

2. Bond yields decline

U.S. Treasury yields declined in the latter part of this week, but may rise again in the future due to developments in Iran.

The U.S. 10-Year Treasury Yield closed below 4.3% this week, also falling below its 20-day moving average. A further break below the 200-day moving average would be considered a bullish signal; conversely, a rebound above 4.5% could push yields back toward the May 2025 high near 4.6%.

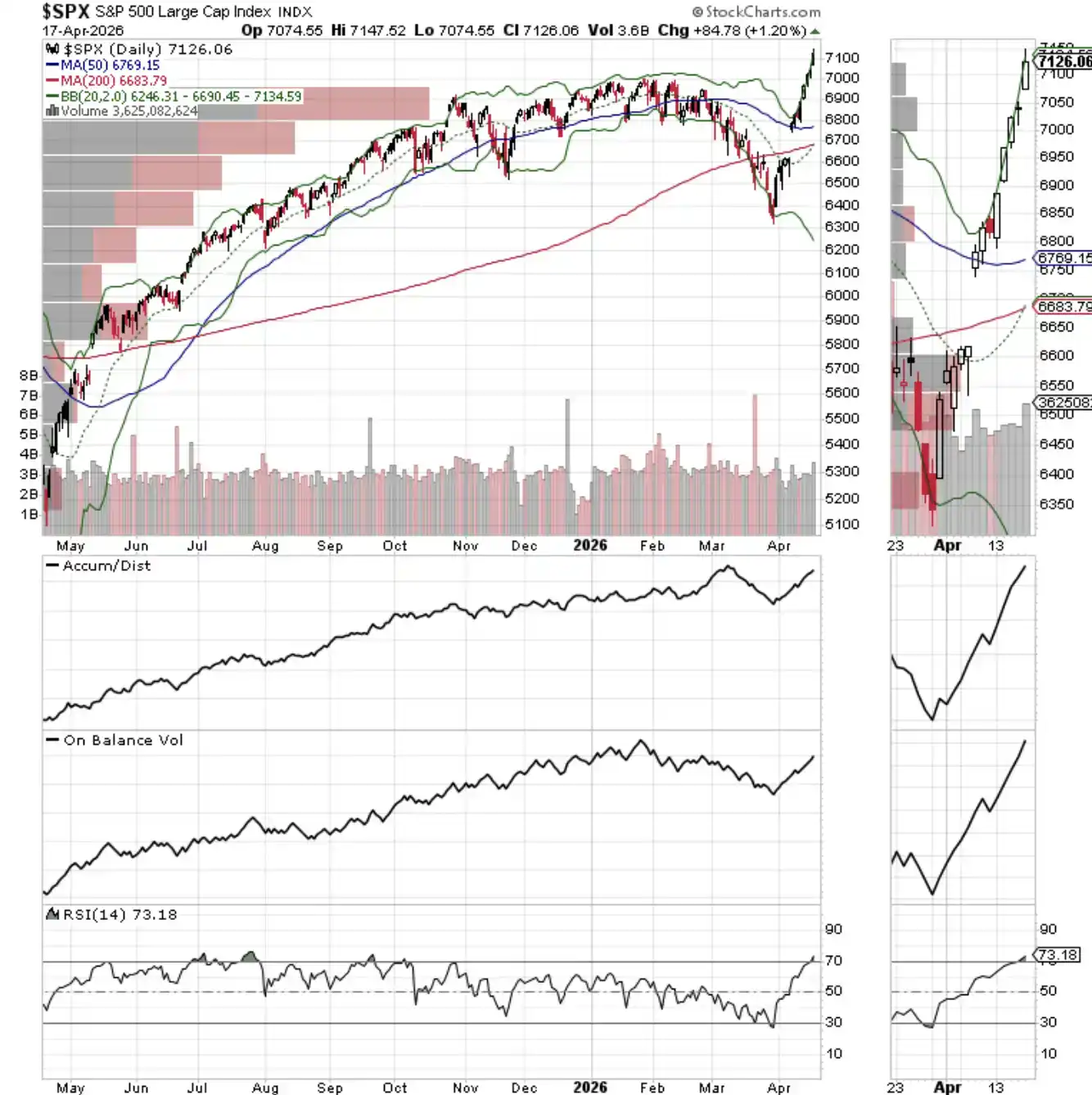

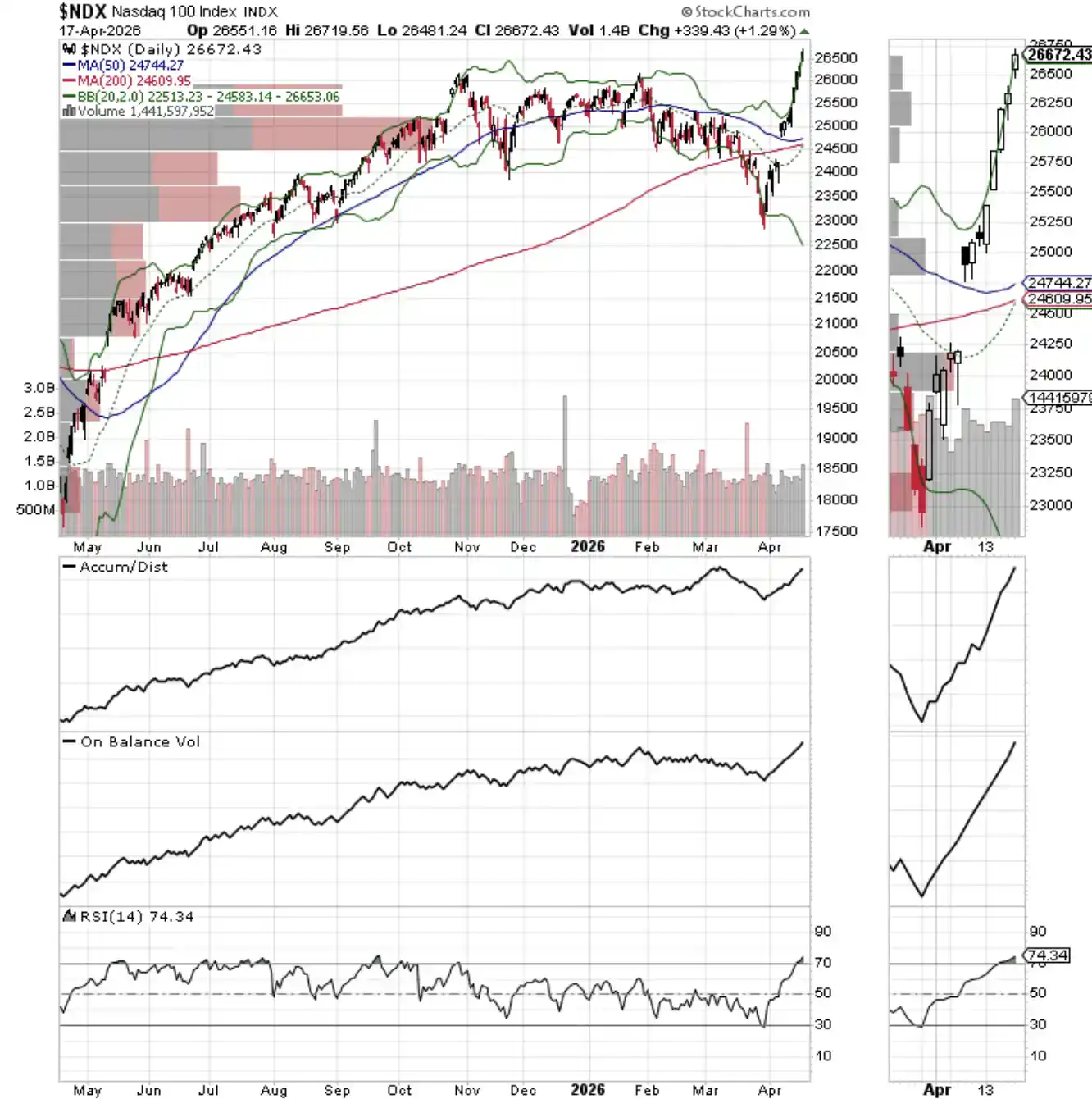

3. NYAD, SPX, and NDX all reached new highs simultaneously.

The NYSE Advance-Decline Line has reached a new high, confirming the upward trend alongside new highs in the S&P 500 Index and NASDAQ-100 Index.

The current uptrend is confirmed—but only temporarily. Once the price falls below the 20-day or 50-day moving average, market conditions could change rapidly.

The NASDAQ-100 Index reached a new high last week, and the 26,000 level has now become a short-term support level.

The S&P 500 Index reached a new high last week, breaking above the 7,000 level, which has now become a short-term support level.