Original | Odaily Planet Daily (@OdailyChina)

Author | jk

On February 28, 2026, the U.S.-Israel joint airstrike on Iran had already begun. This was less than two hours after Trump posted an 8-minute video on Truth Social, and Iran’s official authorities in Tehran had not yet acknowledged Khamenei’s death.

On Polymarket, the contract "Will the United States launch a strike against Iran before February 2026?" is trading at $0.98.

From February 28 to April 30, Polymarket contracts surrounding the U.S.-Iran conflict generated over $300 million in trading volume. During this period, the market experienced multiple high-volatility events—including the outbreak of war, the blockade of the Strait of Hormuz, the announcement of a ceasefire, the breakdown of the ceasefire, and the extension of the ceasefire—each major event triggering significant repricing of the contracts.

In this article, Odaily Planet Daily analyzes four accounts that significantly profited during this period—the core question is simply: What was the public information environment when they placed their bets, and was this judgment supported by evidence at the time?

Case 1: All-in on Fire, single-day gain of 3,503%, profit exceeding $450,000

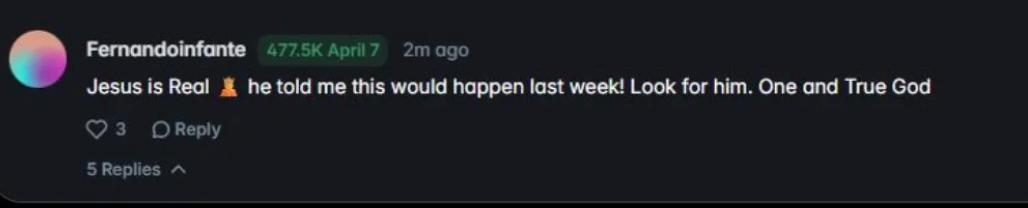

Account: Fernandoinfante

On April 7, Trump announced a ceasefire between the U.S. and Iran on Truth Social, causing the contract "U.S. and Iran will cease fire before April 7" to surge from single digits to nearly $1. The trader who profited from this move is Fernandoinfante, who previously bought 477,543 Yes contracts at an average price of 2.8 cents, for a total cost of $13,200.

Single trade return of 3,503%, settled same day, profit of $450,000, equivalent to over 3 million RMB.

Before April 7, public information on the ceasefire negotiations was as follows: On April 5, Pakistan proposed a two-week ceasefire draft, which Iran formally rejected, presenting a counterproposal of 10 points requiring troop withdrawal, compensation, and full sanctions relief. On April 6, Trump threatened to expand strikes to include power and bridge targets but later postponed them by five days, stating “negotiations are underway.” At midnight on April 7, market consensus pricing for a ceasefire remained extremely low, with 2.8¢ implying a probability of less than 3% that a ceasefire would be reached that day.

From a public information perspective, Iran has just rejected Pakistan’s draft, Trump is still threatening bombardment, there are no formal channels for negotiations, and the Strait of Hormuz remains blocked. No major media outlet reported on the evening of April 6 that a ceasefire was imminent.

What is the basis for this judgment?

First, information asymmetry. Polysights pointed out on Twitter that this trade was placed two days before the ceasefire announcement. If true, the purchase occurred around April 5, when Trump had already begun softening his rhetoric (delaying the power strike by five days), Pakistan’s mediation channels remained open, and some Washington observers were already discussing on April 5–6 that “Trump needs a result.” A trader closely monitoring negotiation channels might have picked up on Pakistan’s diplomatic moves faster than the market priced them in—but this still requires exceptional access to information or insider channels.

Second, extreme odds betting. A price of 2.8¢ means that even with only a 10% probability of a ceasefire, this still represents a positive expected value bet. Traders’ strategy is: in the final stages of geopolitical contracts, systematically buy all low-priced Yes contracts, using a small capital base to cover multiple expiration dates, waiting for one to trigger.

Fernandoinfante has had other failed predictions, such as anticipating the Strait of Hormuz returning to normal, a permanent peace agreement being reached, and the collapse of the Iranian regime—all of which failed—confirming this logic. He placed bets on multiple outcomes, and the ceasefire was merely one that happened to be correct.

Of course, his own explanation is "Jesus told him."

He claimed to have received divine revelation.

Is there anything to learn from that?

This person did not bet on a specific outcome, but rather on the broad direction of "de-escalation of the conflict." He bought positions in ceasefire, permanent peace, restoration of Hormuz, and regime change, executing a diversified bet on this directional trend.

Only the ceasefire event resulted in a win; all others incurred losses, but a single 3,500% return was enough to cover all losses and generate hundreds of thousands of dollars in net profit.

The logic of this structure is that the market pricing systematically undervalues the probability of geopolitical sudden shifts in low-liquidity tail contracts. When an event’s probability is priced at 2–3%, but the actual probability may be 10–15%, bulk purchasing such contracts is statistically rational in terms of expected value, even though most will expire worthless.

Case 2: Consistently losing at the bottom, then hitting all correct picks on the final day: The "Steadfast Choice" Strategy

Account: Vivaldi007

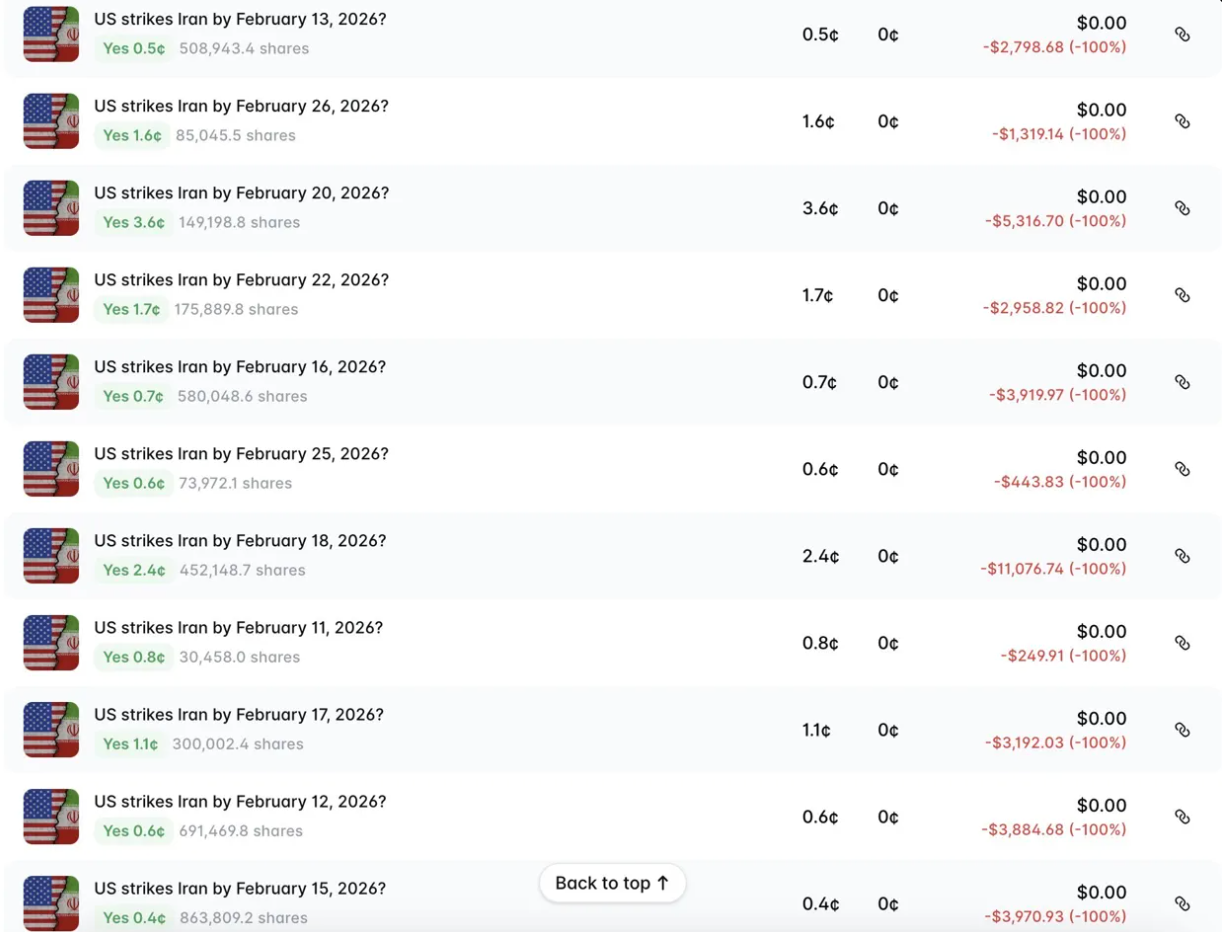

Vivaldi007 registered on Polymarket in February 2026, less than three weeks before the outbreak of the geopolitical conflict. From the first day of registration, he did only one thing: bet on the U.S. Congress going to war with Iran.

His trading history was extremely unusual: Starting on February 11, he bought Yes contracts for every expiration date—11th, 12th, 13th, 15th, 16th, 17th, 18th, 20th, 22nd, 25th, and 26th—averaging prices between 0.4¢ and 3.6¢. Each trade expired worthless, resulting in total losses of approximately $39,000.

Strategy of persisting despite repeated failures

Then on February 28, the U.S.-Israel joint airstrike began, and Khamenei was killed that day.

He held 504,416 Yes shares on the contract expiring February 28 at an average price of 12.7¢, investing $63,986. He ultimately earned $437,930, a return of 684%. Combined with his positions on the same day for “Will Khamenei Step Down?” (bought at 53¢, +88%) and “Will Israel Strike Iran?” (bought at 14.9¢, +571%), his total profits from the three contracts in a single day exceeded $629,000, covering all prior losses and netting him $511,098.

Timeline position and the information environment at the time

In early February, when Vivaldi007 registered their account, several important events occurred at the public information level:

On February 6, indirect negotiations between the U.S. and Iran resumed in Muscat, with Witkoff, Kushner, and CENTCOM Commander Brad Cooper listed on the U.S. delegation—military direct involvement in negotiations is itself an unusual signal. On February 13, Trump ordered the Gerald R. Ford aircraft carrier strike group to head toward the Middle East. On February 17, Khamenei publicly stated that the U.S. Navy could be sunk. On February 20, Trump set a 10-day deadline and publicly threatened military action. On February 24, in his State of the Union address, Trump claimed Iran had restarted its nuclear program. On February 26, the third round of talks in Geneva collapsed, with the U.S. delegation leaving “disappointed.” On February 27, multiple embassies began evacuating non-essential personnel from Tehran.

Of course, the Trump administration previously had a precedent with Venezuela, which is also an essential consideration.

From February 11 to February 27, the market never priced in more than 15¢ for the possibility that the U.S. would strike Iran within February. Buying all these expiries at once was extremely low-cost, as the market overall still favored the expectation that negotiations would continue.

The logic of this strategy

Vivaldi007's strategy does not predict specific dates, but instead covers a range of possible expiration dates within a time window, using extremely low unit costs to cover as many dates as possible, waiting for one to trigger.

This strategy has several structural prerequisites: First, he had a strong conviction that “the U.S. would ultimately strike,” otherwise he would not have maintained his position from early February to late February. Second, he accepted sustained losses totaling $39,000. Third, his position on the February 28 contract was significantly larger than on other dates ($63,986 versus $250–$11,000 per trade on other dates), indicating that he increased his bet on this specific date at some point, rather than allocating evenly.

Case 3: $2.1 Million Bet on “Nothing Will Happen”: The Conservative Strategy of Large Funds

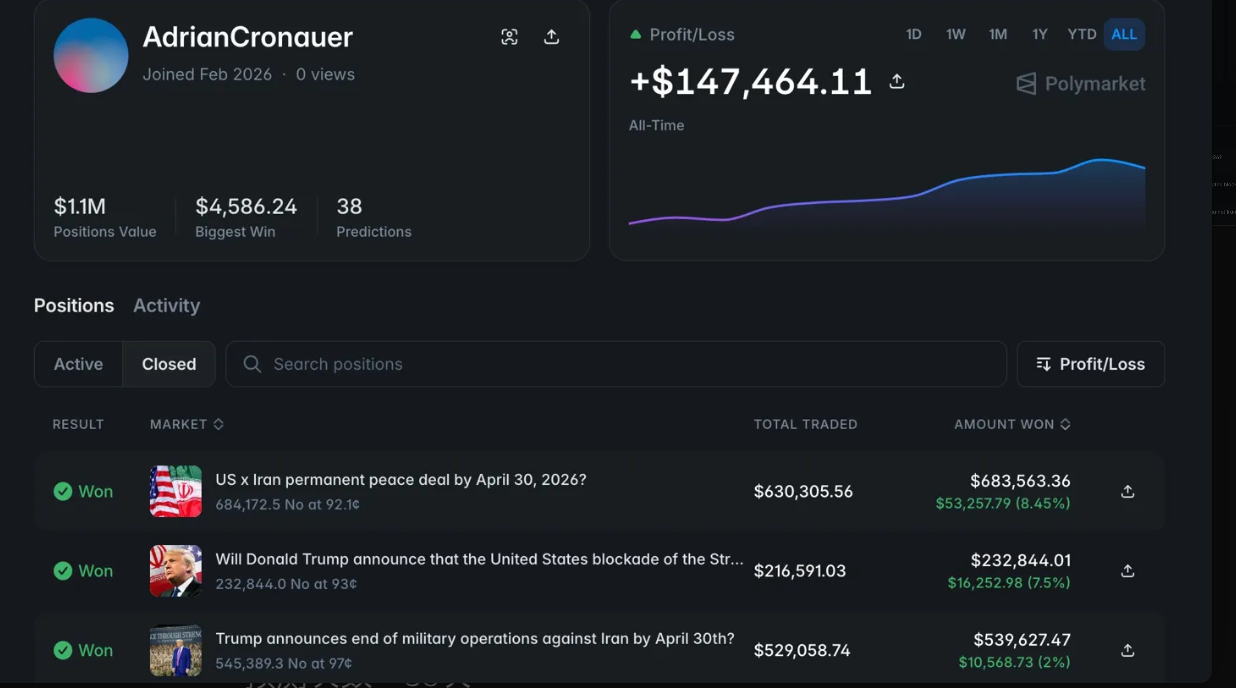

Account: AdrianCronauer

The operational logic of this account is completely different from the previous two cases. Fernandoinfante and Vivaldi007 bet on “what will happen,” while AdrianCronauer bet on “nothing will happen.”

He uniformly bet No on all major Iran-related contracts before the end of April: no permanent peace agreement would be reached, Trump would not announce the end of military operations, Iran would not surrender enriched uranium, the Strait of Hormuz blockade would not be officially lifted by the U.S., and no diplomatic meeting would be held before the deadline. Every bet was No—and every one won.

The return rates are not very high compared to the top two; the highest was only 8.45%, and the lowest was 0.44%. However, the scale of the principal compensates for everything. Just the bet on "a permanent peace agreement reached before April 30" involved an investment of $630,305 and yielded a profit of $53,257. The bet on "Trump halts military actions before April 30" involved an investment of $529,058 and yielded a profit of $10,568. With 38 predictions, a 79% win rate, and a total deployed principal exceeding $2.1 million, the cumulative net profit amounted to $147,464.

Timeline position and information environment

The buying nodes for this batch of transactions were concentrated from early April to mid-April, following the announcement of the ceasefire but before the breakdown of negotiations.

When the ceasefire was announced on April 7, the market briefly priced in higher probabilities for a "permanent peace agreement" and "end to military operations." Adrian Cronauer’s No position was partially established during this window: as the market grew optimistic due to the ceasefire news and pushed the Yes outcome for "permanent peace agreement by April 30" up to 7–8¢, he bought No at 92¢, locking in the counterparty’s optimism premium.

From April 11–12, negotiations in Pakistan lasted 21 hours and ended without an agreement. JD Vance publicly stated that Iran “rejected our conditions.” On April 13, the United States announced counter-blockades against Iranian ports. On April 17, Iran announced the reopening of the Strait of Hormuz, only to close it again on April 18. By April 21, when Trump extended the ceasefire, only nine days remained until the April 30 deadline, and negotiations between both sides had effectively stalled.

Under this informational backdrop, pricing the events "a permanent peace agreement reached before April 30" and "Trump halts military action before April 30" at just 7–8¢ is still overvalued to AdrianCronauer.

The core judgment of this strategy

Adrian Cronauer's approach is based on a relatively simple but continuously verifiable judgment: in highly uncertain geopolitical stalemates, major breakthroughs within short deadlines are always overestimated by the market.

He wasn't betting on specific negotiation outcomes, but rather on "not enough time." Events such as a permanent peace agreement, a declaration ending military operations, or the handover of enriched uranium—even if they eventually occur—are extremely unlikely to happen within weeks. When the market prices the Yes outcome of such contracts at 1–8¢, the corresponding No outcome is priced at 92–99¢, yielding only 1–8% returns but with extremely low risk. He used scale to amplify returns, spreading $2.1 million across more than a dozen related contracts, systematically harvesting the market’s optimism premium.

Where are the risks?

The fatal flaw of this approach is the black swan event. If Trump actually announces the end of military action before April 30, his $529,058 No position will go to zero. He bought No at 97¢, implying he believed the probability of this event occurring was no more than 3%. Yet Trump’s decisions have historically been unpredictable.

But judging from the overall information environment in April, this assessment is supported: the breakdown of negotiations, extremely low bilateral trust, internal leadership divisions in Iran, and the repeated opening and closing of the Strait of Hormuz — any one of these factors makes the probability of reaching a formal agreement within 30 days negligible.

Case 4: How can a small capital achieve the results of Case 3? High-frequency trading strategy

Account: 0xcd7..0d127

This account has no story of a single massive win. 2,000 trades, $25.9M total volume, $7,900 average position size, 75.5% win rate, cumulative profit of $292,000.

The PnL curve begins in June 2025 and slowly, steadily, and nearly linearly climbs upward to the right, with no noticeable jumps or significant drawdowns.

The essence of the strategy: Systematically shorting market panic

Analyst Jay Godiyadada on X observed this account with sharp insight:

The Iranian regime has historically withstood external shocks with a success rate of about 95%, but under market panic, the "regime collapse" Yes outcome is priced at around 20%, causing the corresponding No outcome to be undervalued by 15–20¢. Whenever an event (such as war, assassination of a leader, or breakdown of a ceasefire) drives up the price of Yes, this account takes a large position buying No, capturing the excess panic pricing; then, once the situation stabilizes, it realizes profits.

Take the example of "Will the Iranian regime collapse before June 30?" At the outset of the conflict, when conditions were most chaotic and uncertainty was highest, the price of "No" was suppressed to around 91¢, implying a market-embedded probability of regime collapse close to 10%. He entered the position at this point. As a ceasefire took effect and the situation stabilized, the market reassessed the likelihood of regime collapse, causing the "No" price to rise from 91¢ to 95¢, resulting in a paper profit of 4% on his position.

Overall, this account is trading swings in the prediction market.

What is the difference between this account and Case Three?

The two strategies appear similar on the surface, but there is a key difference: Adrian Cronauer employs concentrated capital, low frequency, and large positions—single trades of $500,000–$630,000, a few contracts, with only 29 total trades. In contrast, 0xcd7 uses diversified capital, high frequency, and moderate positions—an average of $7,900 per trade, 2,000 trades total, spanning multiple market categories (Iran, Greenland, Federal Reserve Chair), operating continuously for nearly a year.

AdrianCronauer's approach is closer to single arbitrage, while 0xcd7 aligns more with market-making logic: systematically identifying overvalued Yes contracts driven by sentiment, shorting them consistently, and accumulating profits through frequency and win rate.

$25.9M trading volume, $7,900 average position size, 2,000 trades

This means the account maintains a significantly high turnover rate for the vast majority of the time. This style is highly meme-oriented, with traders not waiting for settlements but instead continuously scanning the market and entering positions when they identify pricing discrepancies offering even a 5–10% profit potential. A 75.5% win rate based on 2,000 trades is statistically significant and unlikely to be due to luck.

The core competitive advantage of this account, in Jay’s words, is “status quo bias”—a systematic bet that the current state of affairs will persist. In geopolitical markets, major changes are always overestimated, while gradual stalemates are consistently underestimated.

Knowing this, and having sufficient capital and discipline to consistently execute, is enough.