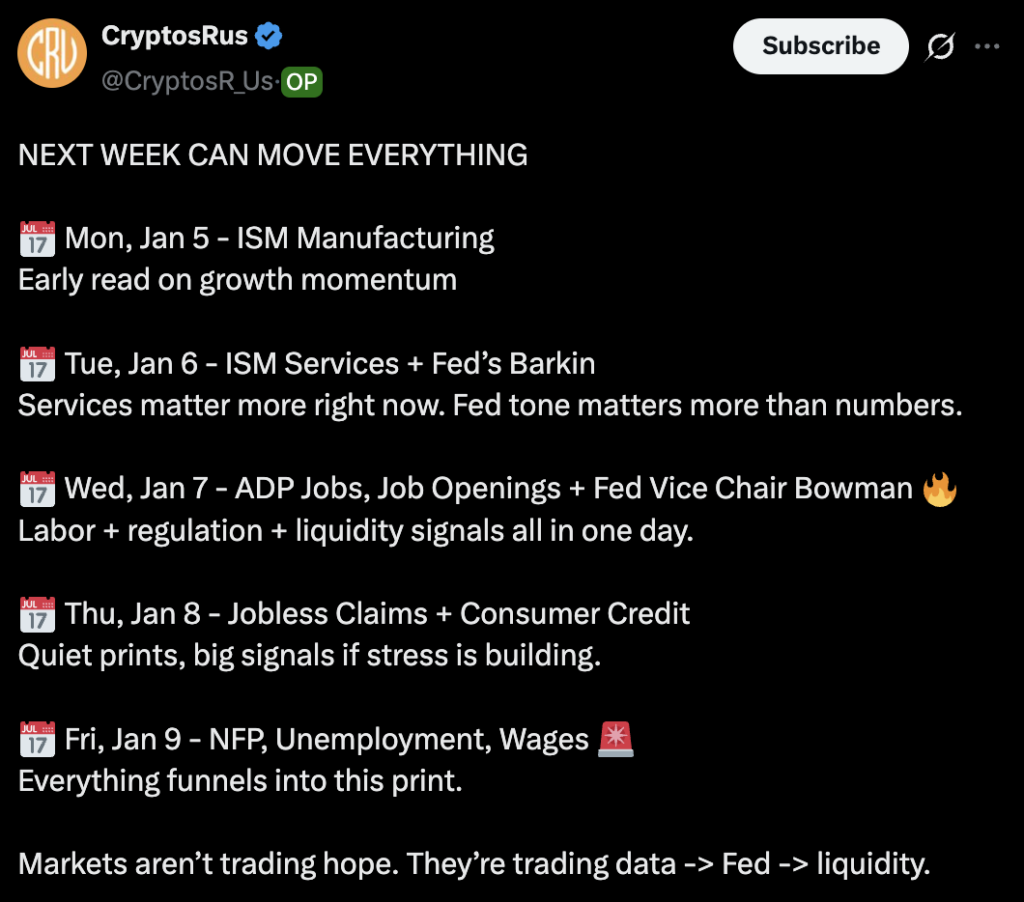

Key Insights

- Five U.S. data events scheduled from January 5-9 could shift markets.

- ISM manufacturing and services data lead off the week.

- Non-farm payrolls on Friday funnel all signals into single print.

Five U.S. data events scheduled from January 5 to January 9 could alter market direction as investors monitor economic momentum and Federal Reserve policy signals.

The sequence includes ISM manufacturing and services data, employment reports, and Fed speeches. Markets are trading on data transmission to Fed response to liquidity conditions rather than rate cut expectations.

Cryptocurrency markets exhibit 3-5x the volatility of equities to macro signals.

ISM Manufacturing and Services Data Kick Off Week

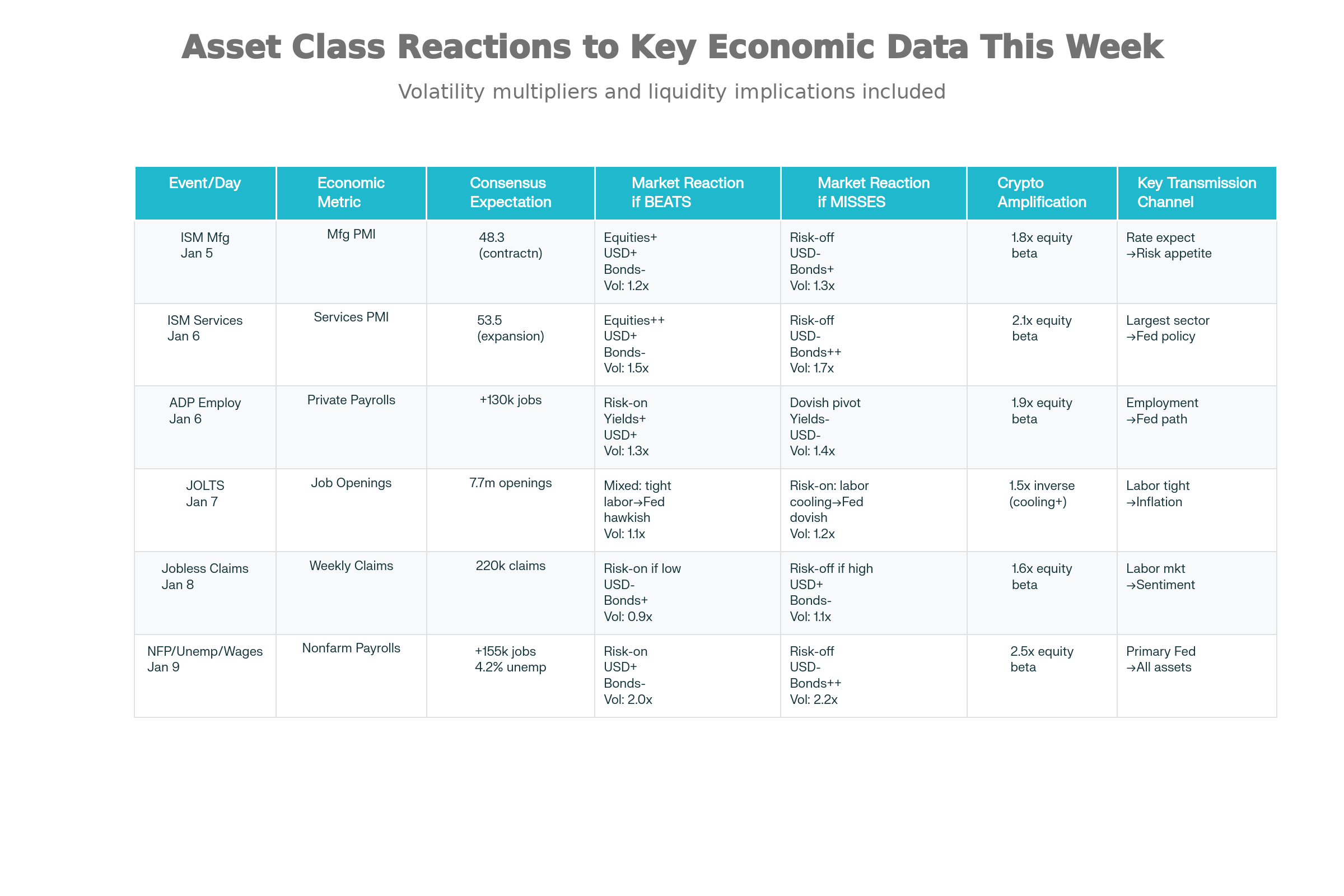

U.S. data events begin Monday, January 5, with the ISM Manufacturing PMI release. The index serves as a leading indicator of economic momentum and inflation pressure.

November’s reading came in at 48.2 and is the seventh consecutive month of contraction. The print shows 58% of the sector’s GDP in decline.

The manufacturing sector faces demand-side weakness in capital-intensive areas including machinery, metals, and semiconductors. Businesses are delaying orders due to tariff uncertainty and weak demand.

The Federal Reserve monitors ISM as a proxy for GDP growth. A reading below expectations signals early-cycle weakness that could strengthen the narrative for deeper Fed easing.

Market reaction varies by asset class. Equities move 0.5-1% on the print, while bonds move inversely with lower readings producing lower yields. Cryptocurrency follows equities with 2-3x volatility. The dollar strengthens on beats as higher growth reduces easing needs.

Tuesday, January 6, brings ISM Services PMI alongside a speech by Fed President Tom Barkin. Services account for over 80% of U.S. economic activity, making this release more significant than manufacturing data.

Employment Data and Fed Speeches Converge on Wednesday

Three critical U.S. data events collide on Wednesday, January 7. ADP Employment Change provides a private-sector employment measure that often diverges from official data.

Markets use the release as a precursor to Friday’s non-farm payrolls. A weak ADP reading below 50,000 suggests the official jobs report will miss, immediately repricing March rate cut odds upward.

JOLTS Job Openings data reveals the labor market’s underlying structure. Job openings have contracted sharply, with November data showing sustained weakness after July’s 7.18 million openings hit a nine-year low.

Declining job openings signal slower wage growth ahead and reduced upward pressure on inflation. Lower JOLTS readings increase the probability of an easing cycle.

Cryptocurrency markets show high sensitivity to JOLTS weakness. ADP misses trigger 2-4% daily swings in Bitcoin prices.

Bowman’s tone carries less immediate volatility but longer-term impact for institutional confidence. The three Wednesday releases collectively create significant market movement potential.

Jobless Claims and Consumer Credit Signal Stress Levels

Thursday, January 8, features Initial Jobless Claims and Consumer Credit releases. Jobless claims appear deceptively quiet, but they carry significant signal power.

Sustained low claims readings under 220,000 suggest layoff risk remains contained, supporting the low-hire, low-fire paradigm. Claims rising above 250,000 would signal Fed rate cuts are hitting hiring decisions.

Consumer credit measures household borrowing and spending capacity. Declining consumer credit availability in auto loans and credit cards suggests banks are tightening lending conditions. The metric serves as a classic sign of liquidity stress.

The combination requires an immediate response from the Fed through larger cuts or balance-sheet expansion. This stress test forces the Fed’s hand toward quantitative easing.

Cryptocurrency rarely reacts directly to claims but consumer credit deterioration triggers liquidations as risk-off sentiment spreads.

Non-farm Payrolls Cap Critical U.S. Data Events Week

Friday, January 9, delivers Non-Farm Payrolls, Unemployment Rate, and Average Hourly Earnings. The NFP release serves as the focal point for all weekly U.S. data events.

Consensus forecasts 55,000 jobs created in December, down from 64,000 in November. The unemployment rate is expected to decline from 4.6% to 4.5%.

The economy now requires approximately 15,000 jobs per month to maintain the unemployment rate, down from 50,000 jobs per month in prior years.

A 55,000 job print remains strong by current equilibrium standards and does not signal recession.

Accelerating wages prompt the Fed to emphasize inflation concerns and hesitate on cuts. Decelerating wages support a Fed pivot toward easing.

Markets currently price a 50% probability for a March cut. A weak NFP below 40,000 could push March odds above 70%, triggering risk-on rallies in cryptocurrency and equities.

The post Five U.S. Data Events That Could Shift Markets Next Week appeared first on The Market Periodical.