Author:Dfarm

When talking aboutPolymarket is a prediction market platform built on the Ethereum blockchain, allowingMany people know that the core of Polymarket is: YES + NO = 1, but do you really understand this simple formula? Today, I will thoroughly explain Polymarket's shared order book to everyone!

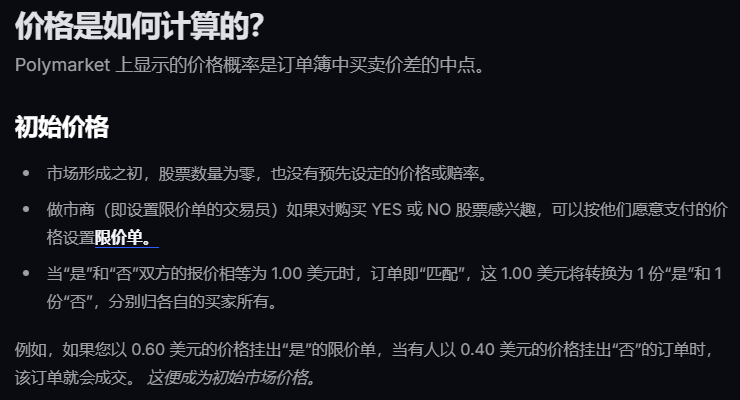

If you check the official documentation of Polymarket, you will find that the explanation of price calculation is as follows:

If you didn't quite understand it after reading, that's okay. Let me give you an example below.

A Torn One-Dollar Bill

Some friends think that YES 0.7 + NO 0.6 = 1.3 is okay? Well, can't a free market set its own prices?

This is incorrect. Although it is a free market, YES and NO are not two separate stocks; they are the same one-dollar bill cut into halves.

Imagine that Polymarket is not selling lottery tickets, but rather a voucher for the future.

The value of each voucher is always 1 dollar.

The market tore this $1 into two halves, one labeled YES and the other labeled NO.

On the settlement day, if the event occurs, YES note = $1, NO note = 0. If the event does not occur, YES note = 0, NO note = $1.

Therefore, at settlement:

- Occurrence: 1 + 0 = 1

- Does not occur: 0 + 1 = 1

Under the premise of market efficiency, where the same market and settlement conditions apply, if you hold both YES and NO for a complementary pair of outcomes, you are effectively holding an asset that is guaranteed to be worth 1 dollar at expiration.

Multi-Option Market

Many people might say that some transactions are not simply YES or NO, but have many options.

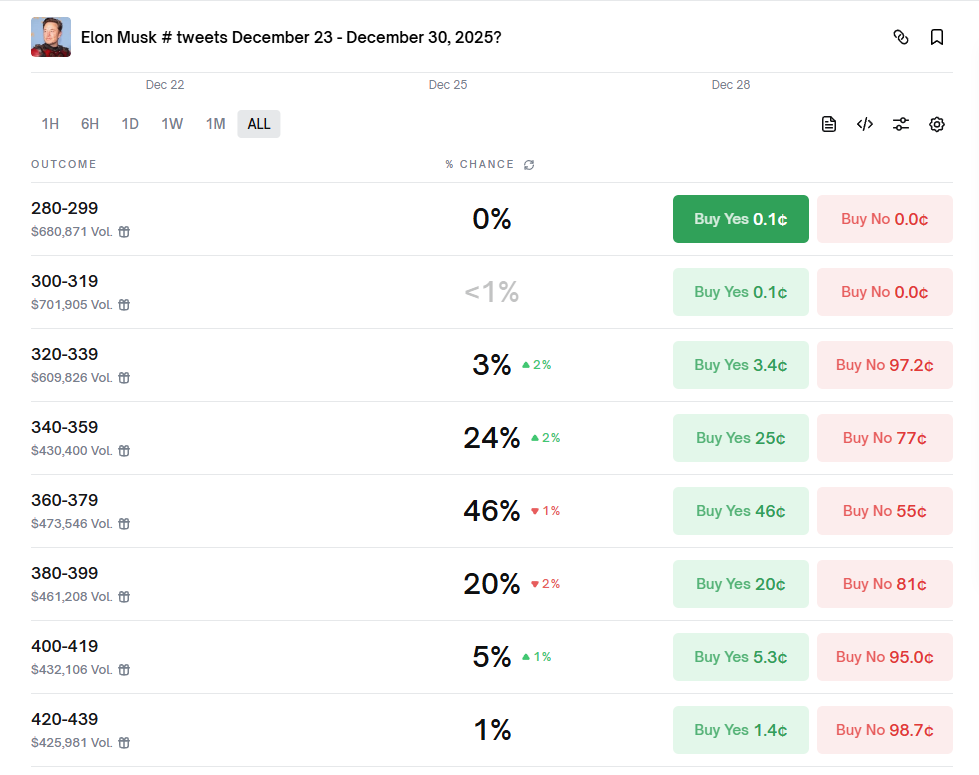

For example, predicting the price of Bitcoin involves many possible price levels, and the number of tweets by Musk also has many possible options.

In fact, if you have used the Polymarket API, you will find that each option has YES and NO, and each can be treated as an independent trade.

Taking the Musk tweet market as an example, we can see there are many options available.

In fact, looking at the API, each title is:

- Will Elon Musk post 0-19 tweets from December 23 to December 30, 2025?

- Will Elon Musk post 20-39 tweets from December 23 to December 30, 2025?

- Will Elon Musk post 40-59 tweets from December 23 to December 30, 2025?

- ...

So they also satisfy YES + NO = 1.

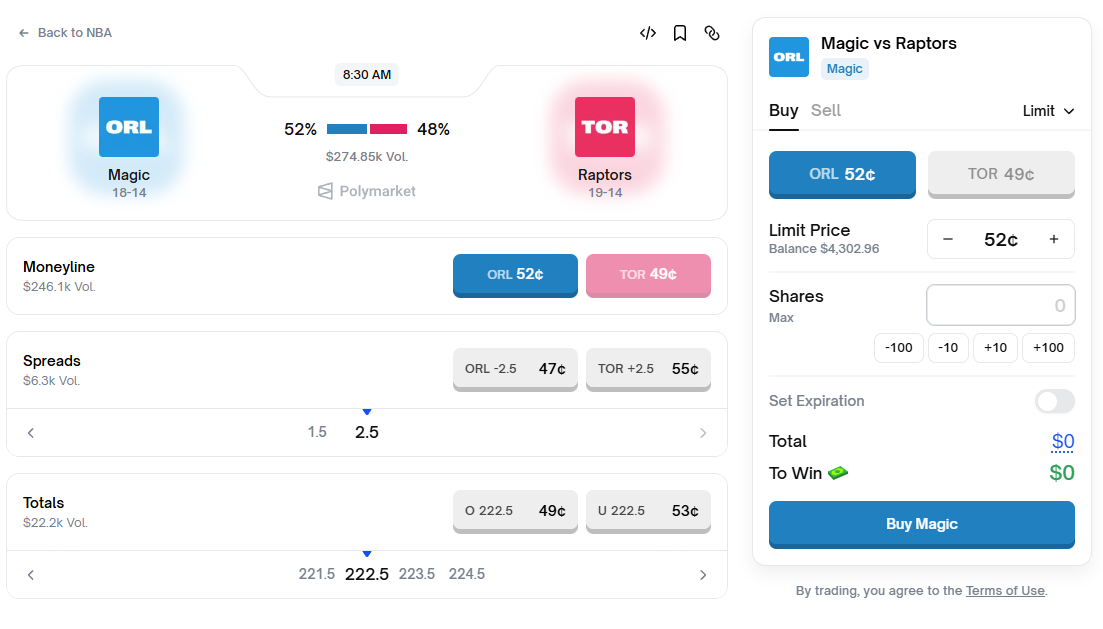

Some friends who are interested in sports betting will find that there are no "YES" and "NO" options for games like the NBA; instead, the names of the two teams are provided as choices.

We noticed that it's currently a Moneyline bet. A Moneyline bet is simply predicting which team will ultimately win. Since there is always a winner and loser in each NBA game (and in case of a tie at the end, there will be an overtime period), the home team and the away team correspond to YES and NO, respectively.

In addition, there may be a draw in the football market, so for football matches, you can buy YES and NO for the home team, YES and NO for the away team, as well as YES and NO for a draw.

Other markets are generally similar in this regard, so I won't provide additional examples. The key point is that all markets satisfy YES + NO = 1.

Shared Order Book

Many people think that the order book of Polymarket is the same as that of a digital currency trading market, but this is incomplete. There are significant differences, after all, it is a combination of YES and NO.

Let's return to the example in the official documentation. The original text states: "If you place a 'yes' limit order at $0.60, and someone places a 'no' order at $0.40, the orders will be matched. This establishes the initial market price."

How should we understand this statement: many people's intuition is that they feel they are trading and buying and selling on their own, without interacting with others. Why then does this kind of transaction matching occur?

This is the magic of shared order books. Let's try it out.

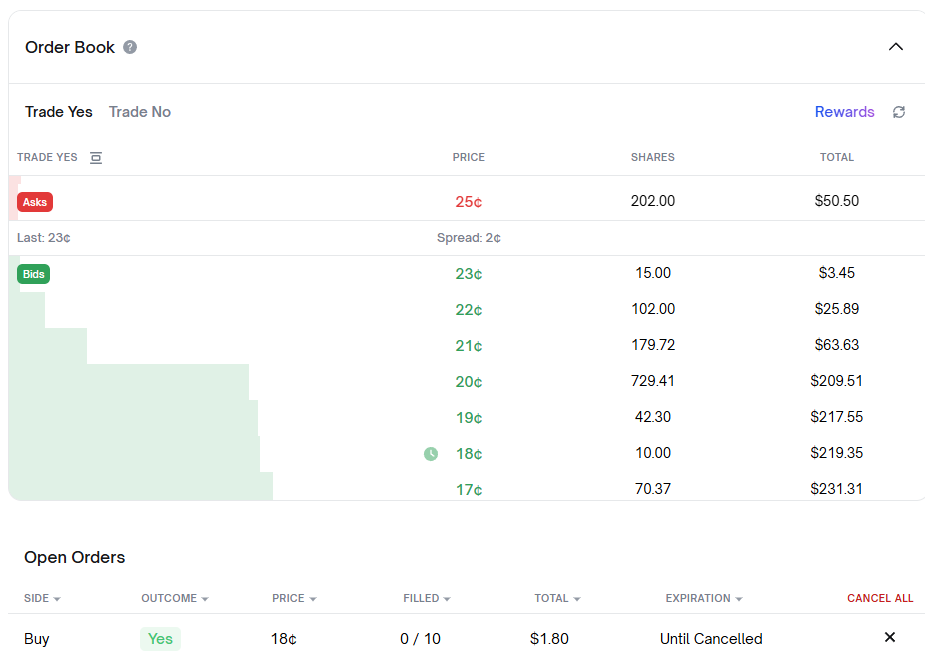

I found a market that's not as actively traded and placed a YES buy order with a price of 18 and a quantity of 10:

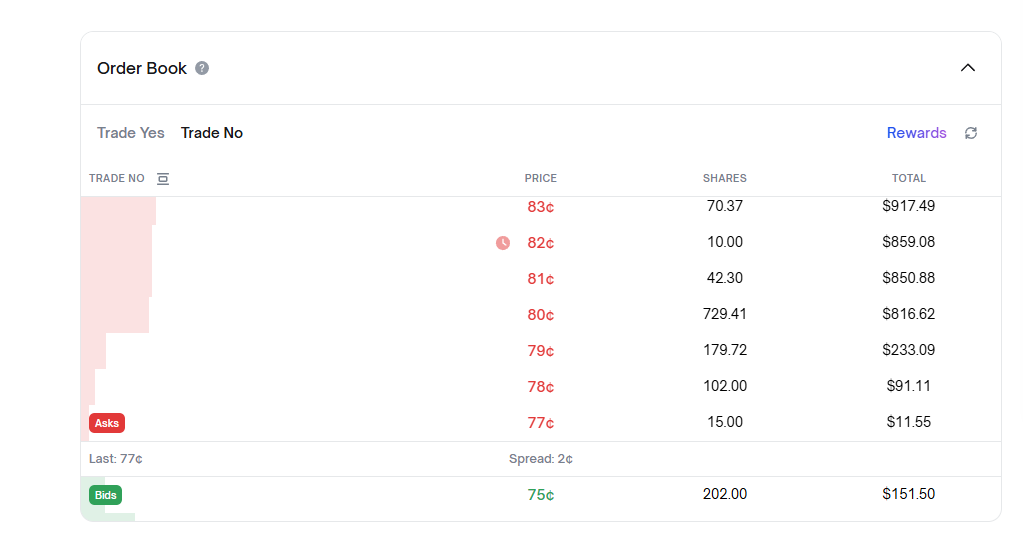

At this point, let's switch to the NO market to take a look:

What did you see? We have a sell order of quantity 10 at the NO market price of 82!

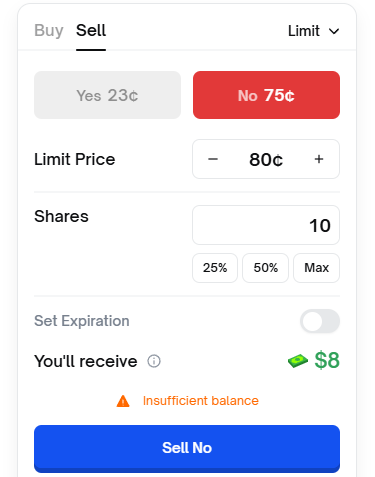

At this point, are you wondering if you can short sell in the market, just like in futures trading, by borrowing coins to sell? When you try to sell, you will be prompted with:

You are told that you cannot sell because your balance is insufficient, and you don't have any NO tickets to exchange, so naturally you cannot sell. Then why is there a sell order at the price of 82?

Please go back and look carefully at the screenshots of the YES and NO markets again. What did you find?

Have you noticed that the ask and bid prices in two markets are like mirror images!

My buy order with price 18 and quantity 10, on the other side is a sell order with price 100 - 18 = 82 and quantity also 10!

You can also match up the other price levels accordingly. The price is determined by the formula: YES + NO = 1. Naturally, 18 corresponds to 0.18, and 82 corresponds to 0.82. It is displayed as two digits here to make it easier for everyone to understand that these represent probabilities.

At this point, if you look back at the example in the official documentation: "If you place a 'yes' limit order at $0.60, and someone places a 'no' order at $0.40, the orders will be matched. This establishes the initial market price."

Can you understand now? Let me use my order as an example. I placed a YES buy order at 18. If someone sells to me, it actually means they bought away the NO order hanging at 82. After the trade, I will have 18 YES in my hand, and the seller will have 82 NO in their hand. When we combine these two vouchers, they satisfy the equation: YES + NO = 1.

You might be wondering here, why not just create two separate betting markets? Why use mirroring instead?

The answer is liquidity! Aggregating order books can concentrate liquidity, improving the efficiency of price discovery!

Arbitrage Illusion

Now you understand YES + NO = 1, and you also understand what a shared order book is.

Now let's look at many of the arbitrage strategies recommended by KOLs (Key Opinion Leaders), which suggest that in the same market, the sum of the probabilities for YES and NO is less than 1. Do you think such an arbitrage opportunity exists? You can think about this for 1 minute before moving on.

The understanding of YES + NO < 1 is: if someone sells YES for 0.4 and someone sells NO for 0.4, I buy both for a total of 0.8, and finally exchange them for 1 dollar, making a net profit of 0.2 dollars!

This strategy is fundamentally impossible in the case of shared order books.

Because when you place a sell order for 0.4 YES, the system interprets this as you wanting to buy 1 - 0.4 = 0.6 NO. (This was already explained in the shared order book section above; if you're unclear, please review the example of the shared order book again.)

At this moment, another person says I want to sell NO at a price of 0.4.

What happened here?

Your real intention is to buy 0.6 NO.

His real intention is to short sell 0.4 of NO.

The buy price is higher than the sell price! Your bid of 0.6 is higher than his sell price of 0.4.

As a result, the system will instantly match your trade, and there's no way a third party can see it.

If you haven't quite understood it yet, imagine the shared order book as a balance scale that automatically keeps itself balanced.

The rule he follows is YES + NO = 1.

If you try to break this balance, the system will directly match the orders for you, and others will not see any imbalanced orders.

Only the orders with YES + NO > 1 are left.

So don't think about the same market where YES + NO < 1; this scenario will never appear on your screen!

Some people might say, "I'm using a YES + NO < 1 strategy on Bitcoin 15m, which isn't really arbitrage—it's essentially a volatility strategy. You place an order on one side, and the moment it gets filled, you immediately take the other side. This can indeed generate profits." However, this approach carries one-sided risk. If the price moves in the direction of your limit order and doesn't come back, it could result in a loss.

Correct Arbitrage Posture

After talking about the wrong approaches, let's now discuss some correct arbitrage strategies.

In fact, if we really go into arbitrage strategies, there could be a great many approaches. Today I'll just randomly mention a few, which don't represent the quality of the strategies.

Multi-Option Arbitrage

Here, we take multiple-choice options as an example that are mutually exclusive and cover the entire range.

Let's take the Musk tweet volume trading example again. The options start from less than 20, all the way up to 580+, with one option for every 20 units, making a total of about 30 options.

These more than 30 options cover the entire range of tweet counts from 0 to over 580. The final tweet count is definitely within this range.

So if you buy all more than 30 YES options, at final settlement, only one will be worth $1, and the rest will be zero.

So if you have purchased more than 30 options, and your final total cost is less than $1, congratulations—you will make a profit equal to $1 minus your cost.

Is there such an opportunity? Yes, there is. However, it's all guarded by a large number of bots, so you definitely won't find such an opportunity manually.

Of course, you might say that it's impossible for the price to go below 20. That's just your personal opinion. You can also choose a range based on your own calculations for arbitrage, but this is no longer strictly arbitrage—it becomes a risky strategy, which is beyond the scope of our current discussion.

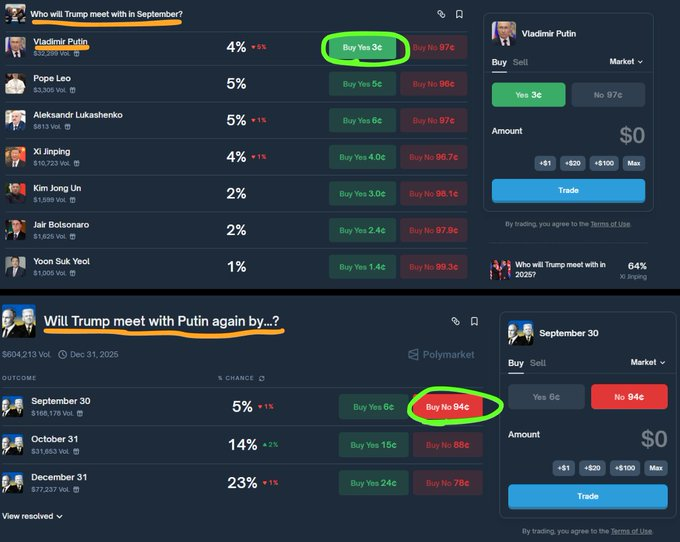

Cross-event Arbitrage

This screenshot is from X platform user: @PixOnChain

This screenshot was taken on a day in September, when the two leaders had not yet met, showing a comparison between the two events.

It can be observed that the two options for these two events are essentially semantically the same, both referring to a meeting in September.

Here, 3 + 94 = 97, which indicates that there is still a potential profit of 100 - 97 = 3 to be made. However, you might notice that this profit is relatively low, and the liquidity may also be insufficient, meaning the actual profit you can make might be minimal.

Cross-event arbitrage bots are a bit less common than the multi-option arbitrage mentioned above. This requires more rigorous judgment and has a slightly higher technical barrier.

Cross-platform arbitrage

The most common one is arbitrage between Polymarket and Kalshi. Of course, Kalshi can only be used by U.S. users, so here we are just using this strategy as an example. We can also replace Kalshi with other prediction platforms, such as Opinion.

If you can buy it:

The price of YES bought on platform A = a

The price of NO on platform B = b

And both describe the same event, and the settlement is determined based on the same facts.

Then, the maturity gain = 1 dollar, cost = a + b.

Only if a + b + all friction costs < 1, it is arbitrage with near-zero risk.

The hardest part here is the four words "same event." You need to carefully compare the settlement rules on both sides. If there are differences in time zones or sources of evidence, arbitrage can easily turn into a nightmare.

However, I've previously done arbitrage between Polymarket and Opinion, and many of the rules are exactly the same, so there's no problem.

However, you should also keep in mind the time cost. Since you have fund transactions on both sides, you won't be able to withdraw the funds before settlement, unless the prices move in your profitable direction. Otherwise, you may have to wait until after the settlement date to withdraw the funds.

Because of the high time cost, many people don't engage in this arbitrage.

Finally

Well, a quick glance shows that this article is already over 3,000 words. I don't know if you truly understand YES + NO = 1 by now. If you really get it, I hope you'll share this article with more people.

Don't be deceived by the strategies of so-called KOLs (Key Opinion Leaders) who post the same event with YES + NO < 1. They might have just used AI to generate some content. After all, I recently asked both ChatGPT 5.2 and Gemini, and neither of them understood shared order books.

Only by letting them consult the official documentation can they discover this issue.