Author: Maria Shen

Compiled by Jiahuan, ChainCatcher

We reviewed 501 real-world income sources and cross-referenced them with currently widely adopted on-chain RWA assets, leading to the following conclusions:

Stablecoin demand has率先 brought government bonds on-chain, and the high concentration of government bonds is now attracting higher-yielding assets on-chain.

Mainstream strategies that make high-yield assets feel "instantly" tradable tend to pull returns toward the risk-free rate.

There are abundant tokenizable revenue sources. Seven opportunity clusters reveal which assets can be unlocked on-chain.

The biggest challenge lies in distribution. Of the 35 non-stablecoin RWA yield tokens with a market cap over $50 million, only two have more than 2,000 holders. This is largely intentional product design.

Despite existing friction, on-chain real-world assets will continue to grow. Even before risk-free rates landed on-chain, two-thirds of stablecoin supply remained stable. Today, the foundational scale exceeds $280 billion, and structural demand is continuously drawing new RWA onto the chain.

First, stablecoin demand is bringing government bonds on-chain, while centralization is attracting high-yield assets to the chain.

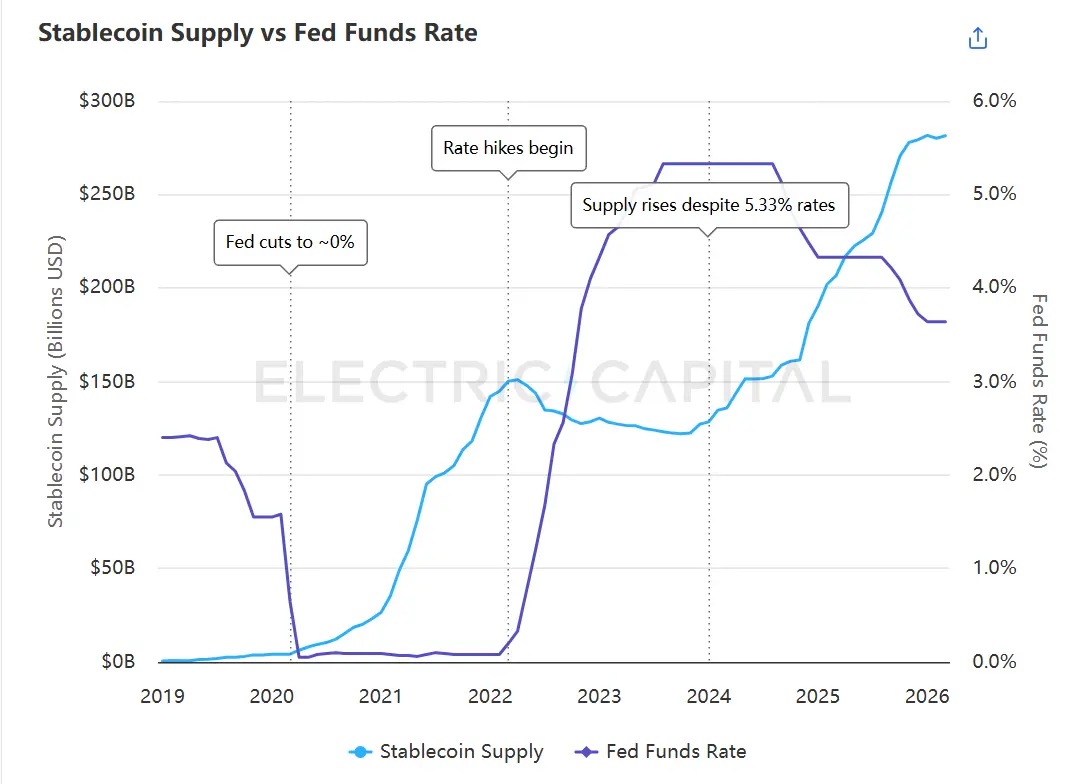

The supply of stablecoins historically had an inverse relationship with the federal funds rate—supply exceeded $180 billion when rates neared zero, and declined as rates rose above 5%. In January 2024, this pattern reversed: even as rates remained above 5%, supply began to grow again and has since surpassed $280 billion.

Stablecoin supply once moved inversely to the federal funds rate until a divergence occurred in January 2024. Source: Electric Capital Stablecoin Dashboard, Federal Reserve Economic Data (FRED).

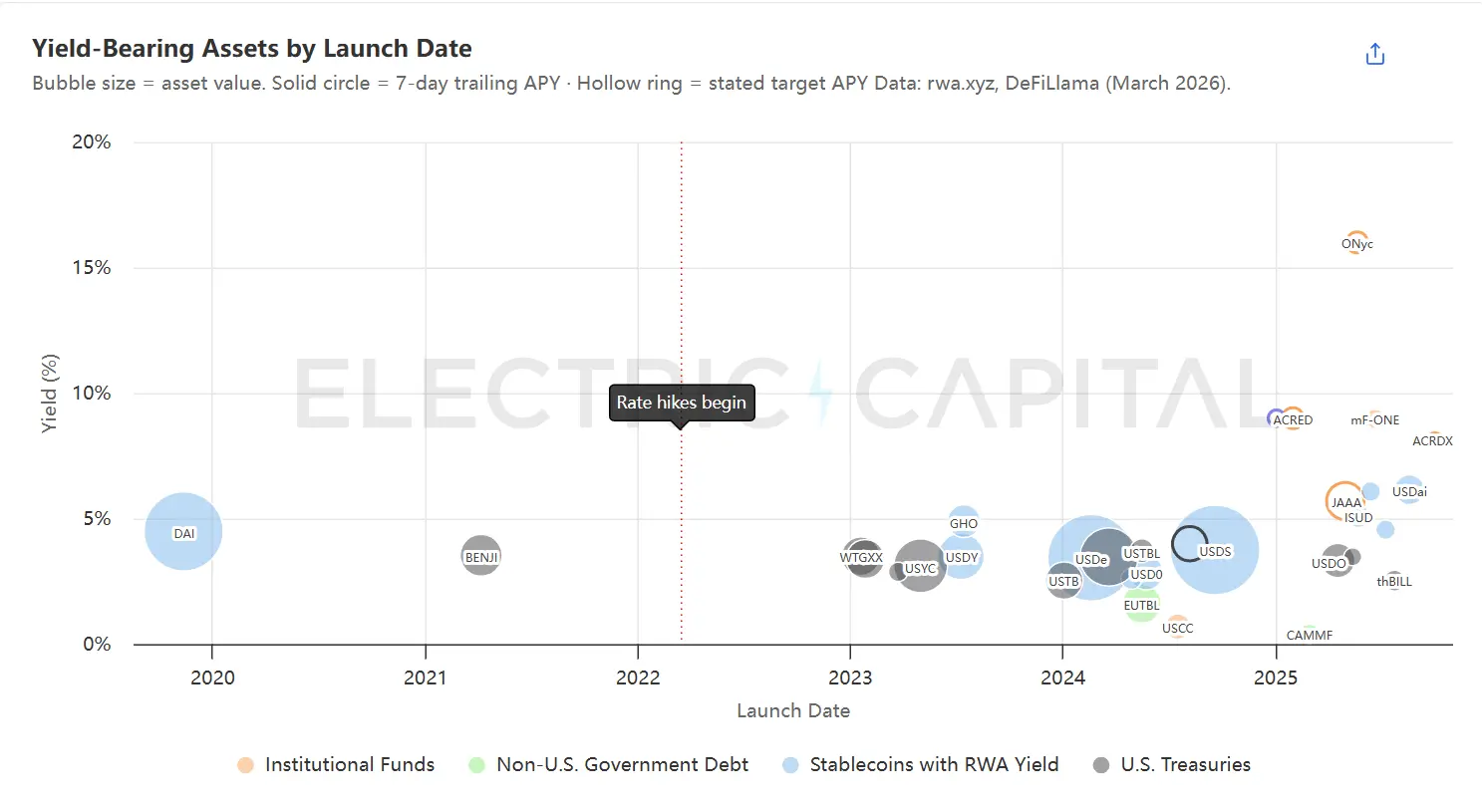

The landscape has changed with the first appearance of risk-free rates on-chain.¹ From Ondo’s early move in 2023 to BlackRock and Centrifuge expanding in 2024, issuers have begun offering treasury yield in the form of on-chain tokens. Stablecoin holders can now earn risk-free rates without leaving the crypto ecosystem.

Yield-bearing RWA assets are ordered by launch date, with bubble size reflecting total asset value. The largest assets are concentrated in the 3% to 5% yield range. Newer, smaller projects continue to extend upward along the yield curve. Data sources: rwa.xyz 7-day tracked APY and launch dates, DeFiLlama Yields API, protocol documentation.

Treasury bonds are now the largest RWA category, with a market size of approximately $11 billion. The same dynamic is bringing other debt instruments on-chain: private credit ($2.8 billion), corporate bonds ($1.9 billion), and non-U.S. government debt ($1.1 billion). The market is highly concentrated: the top 10 assets account for 64% of total value, and the yields of the 18 largest assets range between 3% and 5%.

This concentration is driving stablecoin reserves to diversify and attract higher-yielding assets onto the chain. However, higher-yielding assets are harder to bring on-chain than government bonds.

Second, every tokenized asset faces a time mismatch, and every solution requires a trade-off in yield.

On-chain capital operates 24/7, settles at second-level speeds, and can be redeployed within the same block. Off-chain assets cannot achieve this. Every tokenized real-world asset suffers from this time mismatch, which manifests along two dimensions:

Deployment lag. Funds deposited on-chain only generate returns once they are actually allocated to underlying assets. Disbursing private credit loans can take weeks, and completing real estate transactions can take months. Before the underlying assets are deployed, the funds earn nothing.

Redemption is delayed. When holders wish to exit, the underlying assets cannot be liquidated immediately. BUIDL enables daily settlement through BlackRock, but the perception of instant redemption is due to Circle advancing USDC credit lines in advance. ACRED’s underlying fund offers quarterly redemption windows.³ Real estate funds require lock-up periods of several years.

Government bonds are the fastest asset class off-chain, but to experience smoothness on-chain, various workarounds are still required. This need is even greater for high-yield assets. The cost increases as liquidity decreases: the slower the underlying asset, the more yield is consumed by the workarounds.

Currently, three strategies are employed to bridge this time gap, but all shift the cost of insufficient liquidity to the party willing to bear it:

A. Hold idle funds in liquid assets. Keep a portion of your funds in positions with lower yields but immediate accessibility. When new funds are deposited, they begin earning returns immediately without waiting for underlying assets to be deployed; redemptions also do not require waiting for short-term loans to mature. There are two specific variants:

- Deposit into DeFi lending protocols. For example, Maple’s syrupUSD pool parks unused funds in multiple DeFi protocols—including Sky and Aave—as a liquidity buffer.⁴ New deposits immediately earn yield from the buffer while awaiting loan disbursement, and withdrawals do not require waiting for short-term loans to mature. The trade-off is that each dollar in the buffer generates lower returns than if it were directly lent out, thereby compressing the pool’s overall yield.

- Use government bonds as a buffer. Example: USDai’s sUSDai uses government bonds as the underlying yield through M0, while issuing GPU-collateralized loans on top of this.⁵

B. Allocate returns across the entire pool. Integrate new deposits into the existing pool to ensure no individual depositor experiences deployment delays. New funds dilute the overall yield, but for sufficiently large pools, this dilution is negligible. The cost is that existing depositors subsidize new depositors. Example: Vaults on Morpho.

C. Obtain liquidity from third parties. Holders receive funds from others rather than redeeming from the fund, so the fund does not need to sell any assets. This strategy applies only to accelerated redemptions, not to accelerated deployment.

- Pre-fund a stablecoin pool that buys tokens at net asset value (NAV). Example: Circle pre-deposited up to $20 million in USDC into the BUIDL smart contract⁶ to provide an instant stablecoin exit for the largest tokenized Treasury product. When holders redeem, BUIDL is transferred to Circle, and USDC is simultaneously sent to the holders. Circle then completes the redemption off-chain with BlackRock. If redemption demand exceeds the pre-funded amount, holders will revert to the fund’s standard daily redemption process.

- Tokens are purchased by market makers at NAV. Example: Centrifuge’s Anemoy Liquid Network features professional counterparties (Wintermute, Keyrock, Arbelos)⁷ that provide instant redemptions for Centrifuge fund tokens, paying holders in stablecoins on the same day (up to $125 million, 7×24 hours). Market makers bear the holding cost: they hold the tokens, earn yields, and complete redemptions via the fund’s standard slow channel.

- Use RWA tokens as collateral to borrow in DeFi lending markets. If the tokens are listed as collateral in lending markets, holders can borrow stablecoins without redeeming them—even on weekends or outside fund redemption windows. The fund itself does not participate. This mechanism also supports looping, which will be discussed later in this article as a catalyst for generating new demand for RWA.

Time mismatch exists because one leg is on-chain and the other is off-chain. Bridging this gap is key to making high-yield assets truly viable on-chain.

Three: The sources of tokenizable income are extremely diverse, with seven clusters revealing the on-chain asset potential that can be unlocked.

The 34 on-chain yield sources already deployed are concentrated in familiar areas: government bonds, private credit, and corporate bonds. The vast majority of others have not yet reached a meaningful scale. Seven distinct barriers stand in the way.

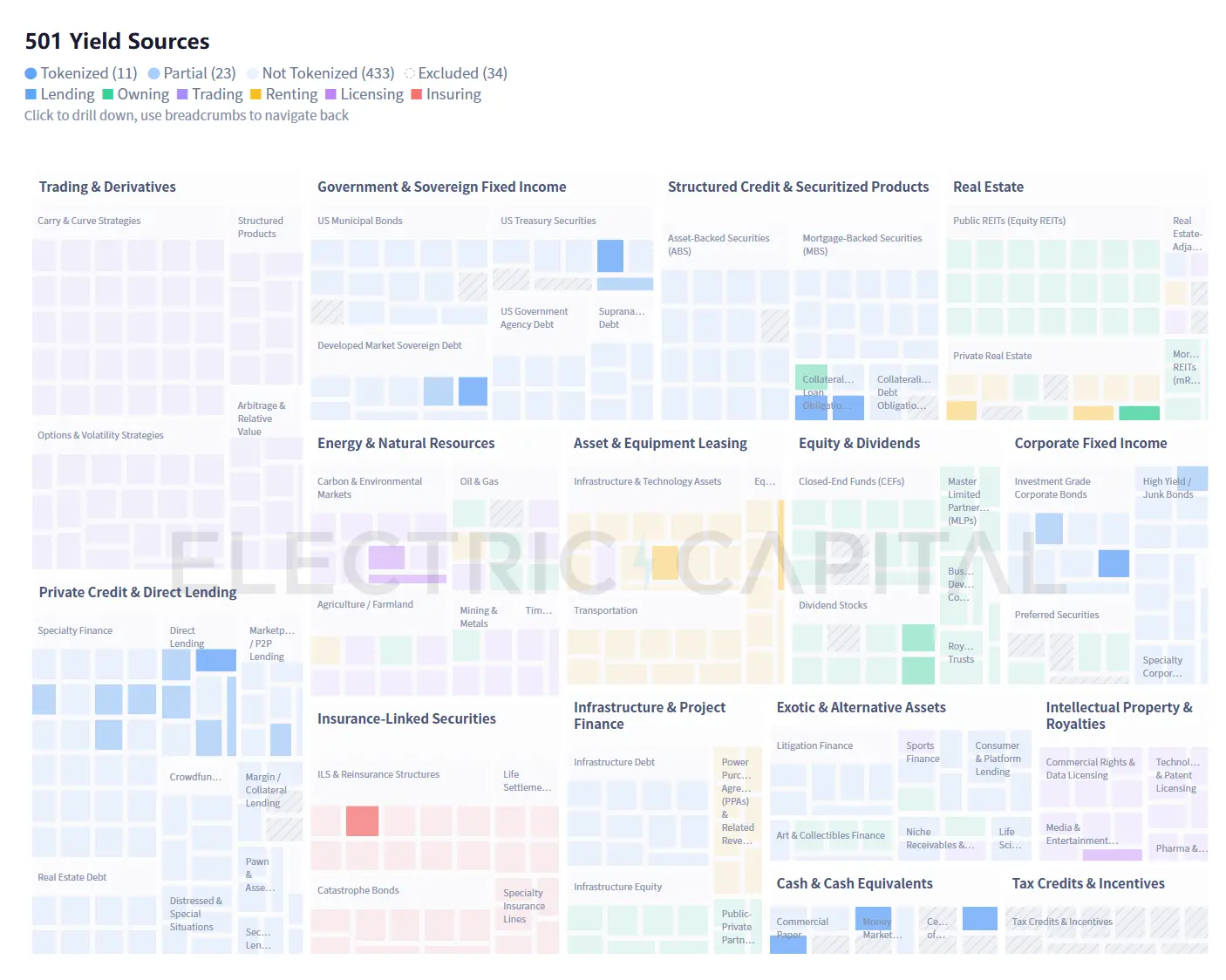

501 revenue sources are distributed across 15 categories (34 sources were excluded for methodological reasons; see note at the end). 93% of the analyzed sources have not yet achieved significant on-chain scale. Data source: Electric Capital

Download the complete 501 source classification table (CSV)

433 off-chain income sources are categorized into seven groups based on the conditions required to enter the on-chain environment. Detailed information for each source is available in the CSV file.

This dataset includes the category, source name, description, example tools, and on-chain status for all 501 income sources. It is recommended to use a large language model (LLM) to enhance the CSV by adding additional fields such as yield ranges, risk factors, liquidity conditions, access requirements, or regulatory jurisdictions.

Macroeconomic forces can accelerate the development of specific sectors. Rising insurance losses from climate events are expanding the catastrophe bond and insurance-linked securities (ILS) markets. Parametric models—which automatically trigger payouts based on measurable events like wind speed or earthquake magnitude, rather than relying on loss assessments—are naturally suited for on-chain settlement. The surge in AI infrastructure spending is driving demand for on-chain financing of GPU clusters, data centers, and energy contracts.

These seven categories of clusters also cannot encompass revenue streams that do not yet exist. It took a century for oil to evolve from a physical commodity into a mature derivatives market. GPU computing may complete the same transformation within a few years, as its secondary market has been digital from the start. Subscription revenue from Twitch streaming did not exist in financial markets five years ago, yet today, the infrastructure to tokenize it is already in place. The 467 sources we identified are a lower bound, not an upper bound.

Four: The greatest challenge lies in distribution

New yield types and strategies only matter if they truly reach capital. Today, distribution channels are extremely limited.

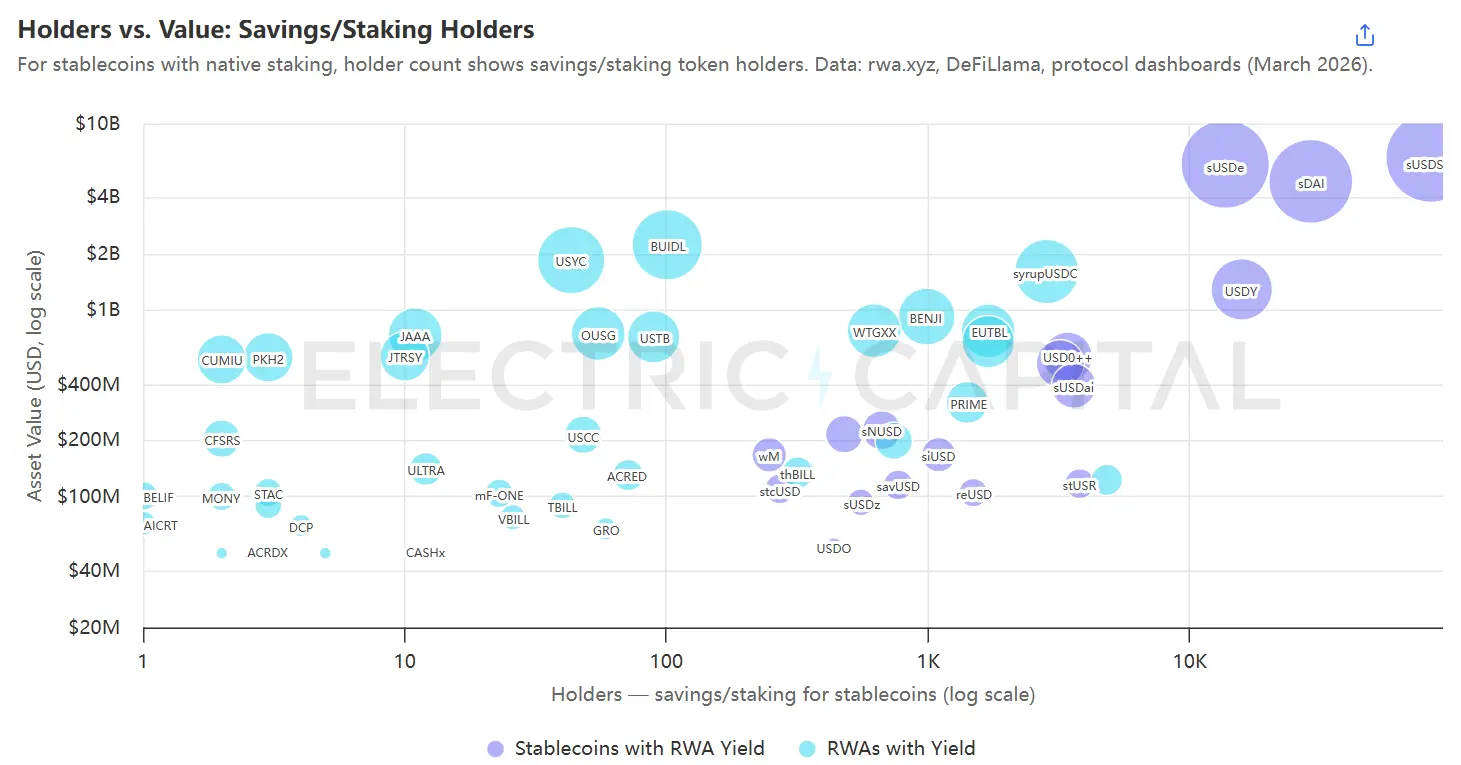

Each bubble represents a yield-bearing asset, sized by on-chain value, limited to savings/staking holders who are actually earning yields. Data sources: rwa.xyz, Etherscan, and other on-chain scanners.

The majority of yield-bearing assets are concentrated on the left side of the chart: of the 35 non-stablecoin RWA assets with market caps over $50 million, 33 have fewer than 2,000 holders. This is largely structural: BUIDL is a fund restricted to accredited investors with a minimum investment of $5 million,⁸ so having around 100 holders is by design. However, for products capable of reaching a broader user base, this low number reflects current RWA’s reliance on partner distribution channels. Exceptions appear in the upper right—staked stablecoins like sUSDe, sDAI, and sUSDS, which have far more holders than other products.

This comparison points to three distribution strategies:

A. Collaborate with deployers and curators.

Large deployers such as Sky and Ethena allocate funds to RWA, with single deployment decisions potentially moving hundreds of millions of dollars overnight. Centrifuge’s JAAA—a tokenized AAA-rated CLO with a size of $743 million at the time of data collection—derived nearly all of its AUM from a single allocation by Sky via Grove.⁹ On March 9, 2026, Grove redeemed $327 million in a single transaction, causing JAAA to lose 44% of its value in one day. Even the largest tokenized RWA, BUIDL, has its value highly concentrated within the protocol: the top 10 holders control 98% of the supply, and these holders are precisely Ethena (via USDtb), Ondo (via OUSG), and Sky (via Spark).¹⁰

Vault curators such as Steakhouse and Gauntlet determine which assets are eligible as collateral for borrowing in their Morpho vaults,¹¹ thereby opening distribution channels for thousands of depositors. Losing one curator means shutting down one distribution channel.

BlackRock and Apollo have the influence to negotiate these partnerships, while smaller issuers must compete for opportunities.

B. Master stablecoins. Embed yield-generating assets within the underlying infrastructure of stablecoins, and then identify distribution channels for the stablecoins themselves.

- Diversified yield stablecoins, such as Sky, allocated across multiple tokenized RWAs.

- Specialized yield-stablecoins, such as USDe (Ethena), reUSD (Re), and sUSDai (USD.ai), each embed a single strategy. The choice between diversification and specialization depends on the holder’s risk tolerance and expectations; single-strategy stablecoins can serve as an entry point to the market, with potential expansion into additional yield types over time.

C. Embedding into apps with existing users. Steakhouse-curated Morpho vaults power Coinbase’s USDC lending, Gauntlet provides the same service for Wirex business accounts, and Kraken’s DeFi Earn routes through Veda vaults curated by Chaos Labs and Sentora.¹² Curators handle risk and on-chain complexity, while apps handle compliance and user acquisition. Entrepreneurs never interact directly with end users, but the returns ultimately reach them. Today, every major case still routes through vault curators, making it essentially a variant of the first path—but that doesn’t mean it must always be this way.

Two paths offer long-term competitiveness: controlling distribution, or becoming indispensable infrastructure for the distribution layer.

Five: RWA will continue to grow

On-chain capital is sticky. As interest rates rose and risk-free rates had not yet become widely available on-chain, the supply of stablecoins declined but did not collapse—significant amounts remained on-chain despite the lack of access to risk-free yields. Today, with real-world yields now available on-chain, supply has grown from $130 billion to over $280 billion.¹³

Five major forces are synergistically strengthening demand for RWA:

A larger stablecoin base means a broader distribution of yield preferences.

The protocol treasury, which manages billions in funds, has vastly different goals from retail holders who temporarily park their savings there. Not everyone is satisfied with the 3% yield from government bonds: some seek 8% from private credit, others pursue 15% through leveraged strategies. These demands are now converging on the same set of products, creating intense pressure for a broader range of yield types.

B. Concentration in highly correlated underlying assets and user competition have fueled demand for diversification.

The concentration of low-yield, high-correlation assets is the demand engine that will drive the next wave of RWA onto the chain.

BUIDL from BlackRock serves as the backing asset for Ethena’s USDtb, the primary underlying asset for Ondo’s OUSG, and a direct holding in Sky’s Grove protocol.¹⁴ The three largest protocols in the on-chain yield space are all correlated to the same treasury fund.

When underlying assets are under pressure, the urgency of diversification increases. Private credit default rates have risen above 5%, and the redemption event at Grove-JAAA has revealed how quickly concentrated positions can unravel.

Risk curators and stablecoins also need to attract more users through differentiated products. If each protocol can only access the same limited set of products, there can be no differentiated competition. The pressure to win users drives the inherent need to bring more assets on-chain.

C. The treasury allows curators to absorb duration and liquidity risks that individual assets cannot bear.

Vaults lower the barrier to entry for new assets: multi-asset vaults do not require each holding to be quickly or highly liquid.

Morpho exceeds $6 billion in size due to curators like Steakhouse and Gauntlet building portfolios that combine liquid and illiquid positions.

Apollo has signed a cooperation agreement to acquire up to 90 million MORPHO tokens within 48 months,¹⁵ signaling its intent to use Morpho as a distribution channel for tokenized credit. Traditional asset management firms are viewing treasury infrastructure as a distribution channel.

The vault is still in its early stages. Current yields are partially subsidized by token incentives—a vault advertising a 12% APY may generate only 4% in organic returns, with the rest coming from token rewards. Additionally, there is no standardized rating system for curators, and depositors still have limited tools to assess risk.

D. Tiering and yield decomposition expand the buyer base for each on-chain asset.

A single income stream serves only one risk profile. Tranching splits it into multiple products, each calibrated for different buyers: senior tranches offering 4% yield with priority loss protection suit conservative DAO treasuries, while junior tranches offering 12% yield but bearing concentrated downside risk attract high-yield seekers willing to absorb losses. The same underlying asset simultaneously reaches both types of buyers. Royco Dawn and Strata are early projects building a universal tranching layer.

Pendle does something different. Instead of grading by credit risk, it splits any yield-bearing token into principal and yield tokens, allowing holders to lock in fixed rates or speculate on variable yields. When Pendle lists a tokenized RWA, it creates entirely new demand from traders and hedgers who never directly purchase that RWA.

The range of underlying assets covered by tiering and yield decomposition is still limited today, but as they mature, each newly on-chain asset can be divided into products targeting multiple buyer groups without requiring a new issuance.

E. Leverage has multiplied the demand for each on-chain asset.

Once tokenized RWA is listed as collateral in lending markets, holders can perform loops: deposit RWA, borrow stablecoins, buy more of the same RWA, and repeat. Tokenized assets yielding 5% can achieve 8% to 10% returns after borrowing costs when leveraged 2x to 3x. Gauntlet has already managed a leveraged sACRED strategy on Morpho, Centrifuge’s JAAA has been listed on Aave Horizon, and Resolv has proposed allocating up to $100 million into similar strategies. Each loop creates incremental demand for the same asset without requiring new originations.

Cyclical operations face structural limitations: on-chain borrowing is instantaneous, but JAAA subscriptions require T+3 settlement, resulting in uneven liquidation speeds under pressure. Emerging infrastructure like 3F Labs is working to close the settlement gap between on-chain and off-chain legs. As this gap narrows and more RWA assets qualify as collateral, leverage will continuously amplify demand for each on-chain asset.

Each force reinforces the others. Once an asset is on-chain, composable, and eligible as collateral, vaults, tranching, and leverage cycles each amplify demand beyond what the asset could attract on its own.

Opportunities abound from the infrastructure layer to the application layer.

- New assets being tokenized

- Infrastructure to make new assets easier to list on-chain (e.g., aggregation platforms that consolidate fragmented markets into investable products)

- Strategies to bridge the gap between deployment and redemption without compressing returns, or to completely eliminate the settlement gap between on-chain and off-chain processes

- Introducing yield exposure to on-chain synthetic products before the underlying assets are fully tokenized

- New distribution methods that break away from current reliance on large deployers and curators, or open new pathways to institutional capital

- New infrastructure to structure each RWA to serve a broader range of users

Each on-chain asset makes it easier to introduce the next asset and increases the value of the infrastructure that supports it.

Research methodology

By reviewing financial industry databases, academic literature, regulatory documents, and practitioner guides, we identified 501 distinct income sources spanning 15 asset classes. We excluded 34 sources that relied on non-transferable legal relationships (FDIC-insured CDs, 401(k) loans), jurisdiction-specific tax incentives (LIHTC, Canadian rate-reset preferred shares, 1031 exchange instruments), or lacked active markets (American Recovery and Reinvestment Act bonds matured in 2010, trust preferred securities prohibited after the Dodd-Frank Act). The remaining 467 sources form the analytical sample. A complete classification table is available in the downloadable CSV, with each excluded source accompanied by a rationale for exclusion.

On-chain status is determined as follows: Map the 727 distribution assets tracked by rwa.xyz to their corresponding revenue sources in our classification table, supplemented by on-chain products not tracked by rwa.xyz (DePIN protocols, carbon credit platforms, music royalty tokens). If at least one mapped product from a source has an on-chain size of $50 million or more, it is marked as "Tokenized"; if on-chain products exist but all are below $50 million, it is marked as "Partially Tokenized"; if no on-chain products exist, it is marked as "Not Tokenized". Tokenized commodities (gold, silver) and private equity are excluded from the revenue source mapping as they do not generate income. Tokenized stocks are limited to "Partially Tokenized" due to the lack of automated dividend distribution on-chain.

Each listing date in the timeline chart has been verified by at least one independent source: protocol press releases, on-chain contract deployment timestamps, SEC filings, or financial news reports. Three assets were removed due to inability to independently verify their listing dates: PKH2 (a Liquid Network mining note with no public block explorer), BELIF (a BlackRock segmented portfolio with limited media coverage), and CFSRS (a newly established Hong Kong fund with no independent reporting at the time of launch). All three remain in the underlying dataset and appear in other charts.