1. From Temporary Statement to Formal Rule: The Joint Letter Capitalizes on the Current Policy Window

Although the SEC’s Division of Market and Trading statement has green-lighted certain software user interfaces, its legal effect remains non-binding guidance and cannot provide developers with long-term legal certainty. The joint letter explicitly calls for the initiation of a formal rulemaking process, aiming—through the notice-and-comment procedure under the Administrative Procedure Act—to transform the current policy stance into regulatory text that can be cited in court and is resistant to reversal by a single commission. Under the current leadership of Chairman Paul Atkins, the SEC has adopted an open attitude toward digital asset innovation, sharply contrasting with the restrictive posture of the previous chair, Gary Gensler—creating the optimal policy window for codifying these rules. Once the rulemaking process begins, validators, oracles, RPC providers, and cloud service providers will have the opportunity to be explicitly excluded from the definition of “broker,” thereby eliminating the primary source of legal uncertainty in their business models.

2. For exchanges and wallet providers: Reduce compliance friction costs for non-custodial services

For publicly traded companies operating cryptocurrency trading platforms or self-custody wallets, their non-custodial interfaces have long existed in a regulatory gray area regarding whether such interfaces constitute brokerage activity. The rulemaking requested in the joint letter, if it clearly states that entities providing only software interfaces without holding customer private keys are not required to register as broker-dealers, would significantly reduce compliance costs and legal risks for these companies in the DeFi space. Currently, wallet products from multiple exchanges and third-party DeFi aggregation interfaces all face uncertainty over whether they must register with the SEC. The formal implementation of such rules would unlock quantifiable compliance capital for these business lines. Every week of delay in rulemaking means additional legal expenses and a valuation discount from investors due to perceived risks in non-custodial services.

3. Infrastructure Service Providers: The "No Registration" Benefits for Validators, Oracles, and Cloud Services

One of the most groundbreaking demands in the joint letter is to explicitly exclude validators, API and RPC providers, oracles, and cloud services from the definition of "broker." This means that under the final rule, companies operating Ethereum or Solana validator nodes, oracle node operators providing data feeds, and cloud service providers offering RPC endpoints for DeFi applications will not need to worry about being classified as broker-dealers simply for processing on-chain data or validating transactions. For technology infrastructure companies listed on Nasdaq or the New York Stock Exchange, this rule removes compliance barriers to offering node or cloud services to the crypto market. The formal adoption of this rule will foster a more predictable enterprise-grade DeFi infrastructure market.

Deep resonance between SEC policy shift and infrastructure demands: from "temporary allowance" to "permanent rules"

Yesterday’s joint letter builds upon the temporary statement previously issued by the SEC’s Division of Market and Trading, advancing the policy trajectory. While the temporary statement green-lit certain user interfaces, its fragility lies in the absence of supporting rulemaking documentation—any future SEC leadership could overturn it at any time. The deeper objective of the joint letter is to elevate this temporary “non-enforcement” stance into a formal regulation subjected to notice-and-comment procedures—not by altering the substance of the policy, but by strengthening its durability and defensibility. For validators, oracles, RPC providers, and non-custodial wallet services at exchanges, the initiation of a formal rulemaking process will be the most critical policy anchor for eliminating legal uncertainty in the second half of 2026; in contrast, the current temporary green light, reliant solely on the personal policy stance of the SEC Chair, remains vulnerable to future changes in the Commission’s composition.

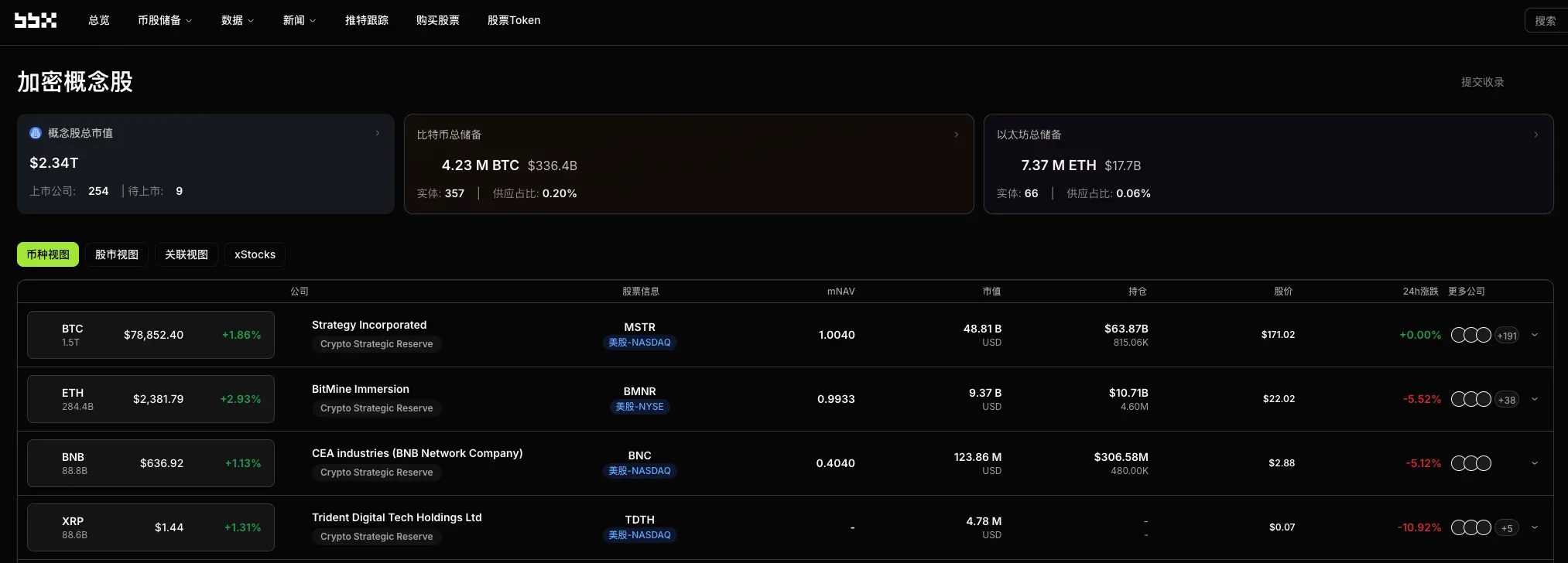

Source:https://bbx.com/Cryptocurrency-related stock news database, compiled from yesterday’s global public company announcements and SEC/TSE disclosure filings.