The Great Attrition of Crypto VCs

Original author: Catrina

Peggy, BlockBeats

Editor’s Note: As the notion of “launching a token equals exiting” no longer holds, crypto venture capital is also losing its once most reliable framework.

Over the past three cycles, tokens have been the core pathway for capital recovery and yield amplification. Built around this premise, the industry developed a familiar rhythm: early funding, narrative expansion, listing and circulation, price realization. However, with on-chain revenue becoming a new barrier, meme coins diverting liquidity, and retail capital spilling over into a broader range of risk assets, this mechanism is breaking down.

More directly, the expected returns for token projects have been compressed, while equity pathways have regained appeal. Early investors are becoming more cautious about projects pursuing a "token exit," while later-stage capital is shifting toward "Web2.5" companies with real revenue and merger & acquisition potential. Crypto venture capital is no longer operating in a relatively closed competitive environment but is instead forced to compete alongside traditional fintech funds.

During this process, a deeper question emerges: What can VCs offer when capital itself is no longer scarce?

Over the past few years, some of the most prominent projects have bypassed institutional capital entirely, building network effects and revenue models directly. This means that funding is no longer a "key" to accessing high-quality projects. For founders, whether to bring on a VC depends on whether the investor can provide clear brand validation and tangible added value—not just capital on paper.

Under the new market structure, crypto venture capital firms need to redefine their "product offering"—otherwise, they risk being eliminated in this cycle.

The following is the original text:

Crypto venture capital is at a pivotal moment. Over the past three cycles, token exits have been the primary source of outsized returns, but this model is now undergoing a significant reset. The definition of what makes a token valuable is being rewritten in real time, yet a unified industry-wide evaluation framework has yet to emerge.

So, what exactly happened?

This round of changes in the cryptocurrency market structure is the result of multiple forces, never before seen together in a single cycle:

1/ The emergence of HYPE has disrupted the entire token market from the side, proving one thing: token prices can be supported by real revenue, with over 97% of its nine- to ten-digit revenue generated on-chain. This case quickly triggered a collective disillusionment in the market toward governance tokens driven purely by narrative but lacking solid fundamentals—such as early L1 tokens and governance tokens primarily used to circumvent securities regulations yet unable to directly distribute revenue. Overnight, HYPE reshaped market expectations: revenue-generating capability is no longer a bonus—it has become the minimum threshold.

2/ A chain reaction followed for other projects: before 2025, a project with on-chain revenue was often classified as a security; after HYPE, without on-chain revenue, most hedge funds view a project’s collapse as merely a matter of time. This has left the vast majority of projects—especially non-DeFi ones—in a difficult position, forcing them to hastily adjust their strategies.

3/ PUMP delivered a severe "supply shock" to the system. The meme coin frenzy triggered an explosive increase in token supply, fundamentally disrupting market structure—attention and liquidity became severely fragmented. On Solana alone, the number of newly issued tokens surged from around 2,000–4,000 per year to a peak of 40,000–50,000, effectively slicing the same pie into roughly 20 times more pieces without a corresponding increase in liquidity. The same capital and attention previously chasing high yields shifted from holding altcoins to engaging in short-term meme coin trading.

4. Alternative destinations for retail risk capital are also growing rapidly. Products such as prediction markets, stock perpetual contracts, and leveraged ETFs are directly competing for the portion of capital that previously flowed into crypto altcoins. Meanwhile, the maturation of asset tokenization technology enables investors to leverage blue-chip stocks—assets that do not face the risk of total loss like most altcoins and are subject to stricter regulation, greater transparency, and reduced information asymmetry.

These changes together have led to one outcome: the token lifecycle has been significantly compressed. The cycle from peak to trough has been drastically shortened, retail investors' willingness to "hold long-term" has sharply declined, and is being replaced by faster capital rotation.

Core issue

Under these circumstances, nearly all venture capitalists are repeatedly reflecting on several core questions:

1/ Are we investing in equity, tokens, or a combination of both?

The greatest challenge is that there is currently no established paradigm for how token value accumulates. Even leading projects like Aave continue to face ongoing debates between DAO governance and equity structures.

2/ What are the best practices for on-chain value accumulation?

The most common practice today is token buybacks, but "common" does not mean "correct." We have long opposed the mainstream buyback logic: this mechanism is toxic and puts truly revenue-generating projects in a difficult position.

The problem is that its motivation was wrong from the start.

Traditional companies repurchase shares typically when growth investment opportunities decline or when the stock is undervalued; in contrast, crypto project buybacks are often forced into immediate execution due to pressure from retail investors and market sentiment—pressure that is inherently emotional and unstable. You might have just allocated $10 million toward a buyback, money that could have been reinvested, only to have it completely wiped out the next day due to a market maker being liquidated.

Public companies repurchase shares when they are undervalued; however, token buybacks are often front-run and executed at local peaks.

If your business operates on a B2B model primarily generating off-chain revenue, such buybacks are futile. In my personal view, there is almost no justifiable reason to conduct buybacks to appease retail investors when annual revenue is below $20 million—these funds should be prioritized for growth.

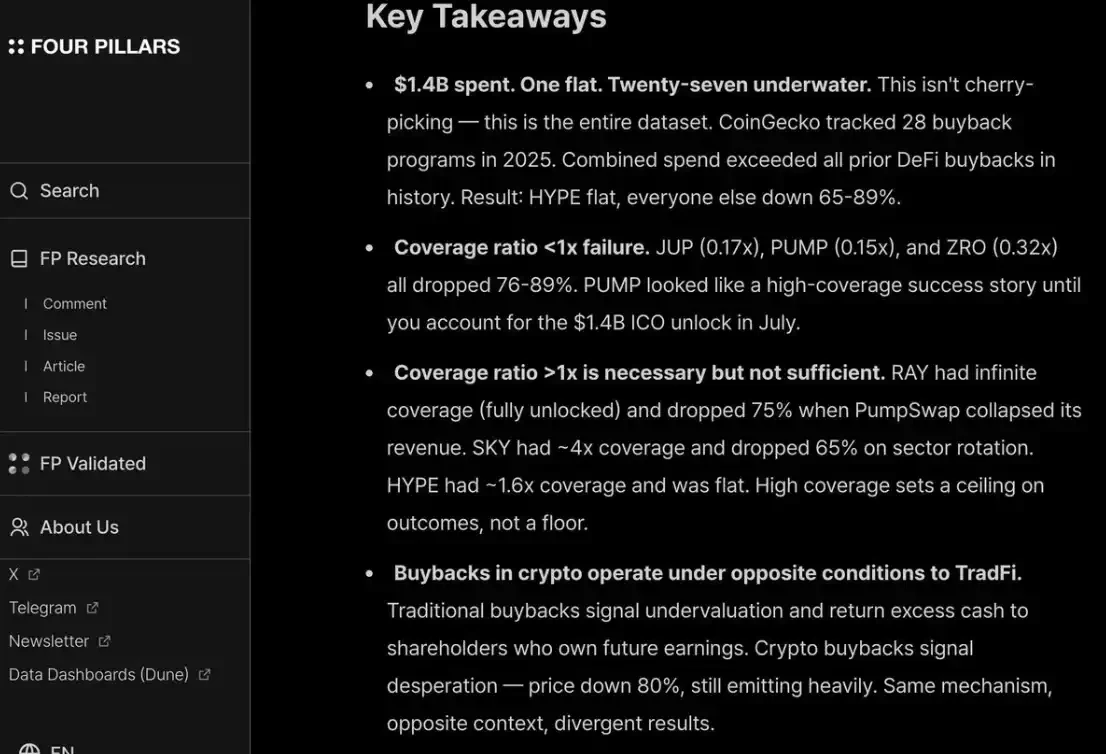

I strongly agree with a report/screenshot from fourpillars: even buybacks in the billions of dollars struggle to create a meaningful long-term price floor for a project.

In addition, to please both retail investors and hedge funds alike, you must consistently and transparently conduct buybacks, like HYPE. Failure to do so will result in market punishment, as seen with PUMP, which has a fully diluted valuation (P/F) of only 6x because the market “does not trust” it—despite the fact that it has already burned $1.4 billion in revenue that could have gone to the treasury.

3. Will the "crypto premium" disappear completely?

This means that, in the future, valuations of all projects may revert to a range similar to that of traditional public companies—roughly 2 to 30 times revenue.

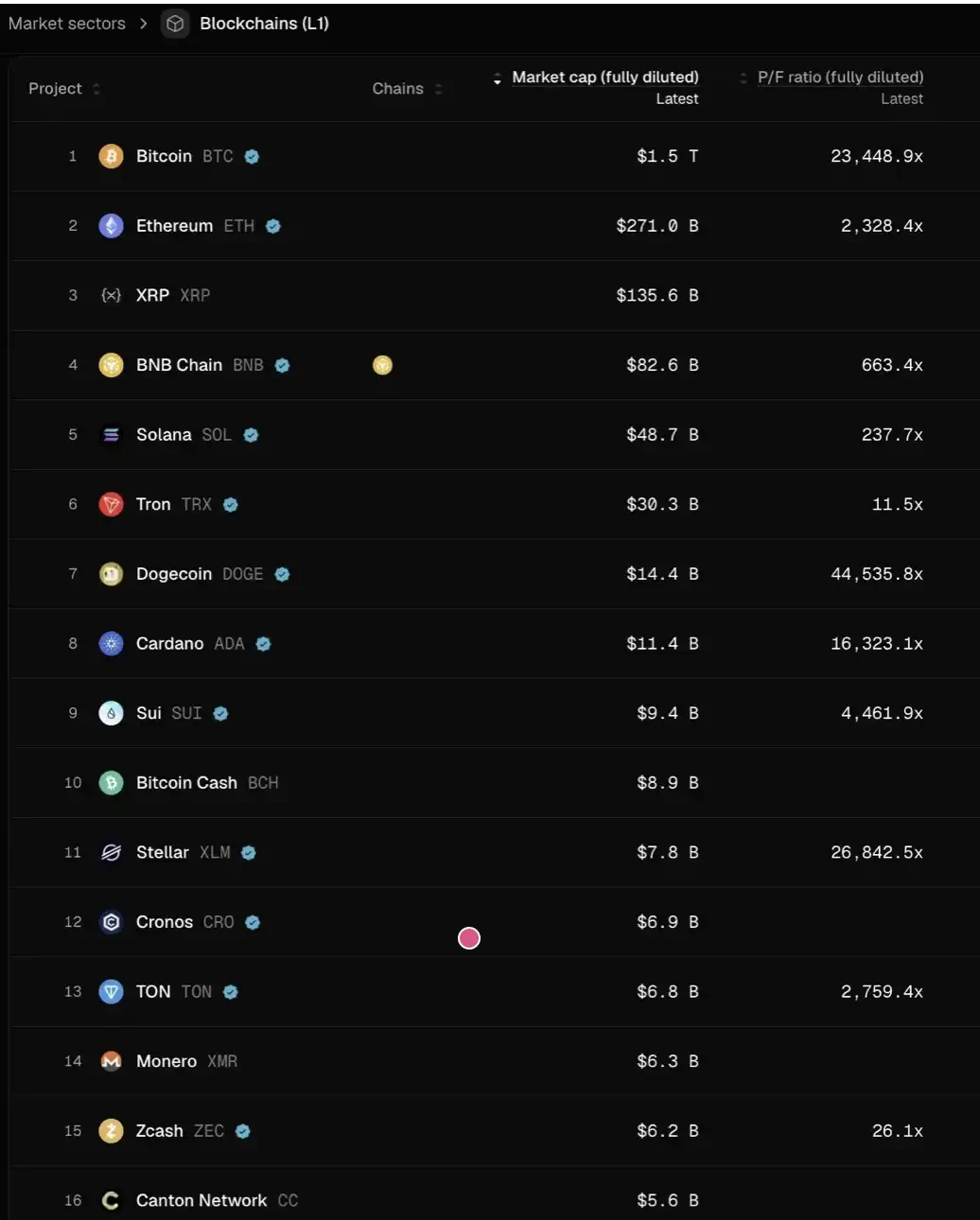

Take a moment to consider the implications: if this assessment holds true, then from current levels, the prices of most L1s would need to fall by more than 95% to align with this valuation framework. Only a few exceptions—such as TRON, HYPE, and other DeFi projects with genuine revenue—can maintain relative stability.

This does not even account for the additional selling pressure from token vesting.

I don’t personally believe things will go that far. HYPE has actually created an “outlier-style” market expectation, causing investors to become overly impatient about whether early-stage projects can achieve immediate revenue or user growth upon launch. Such expectations are reasonable for “sustaining innovations” like payments and DeFi; however, for “disruptive innovations,” it naturally takes time to build, launch, grow, and eventually reach a true revenue inflection point.

Over the past two cycles, we shifted rapidly from excessive tolerance for “disruptive technologies” and eight to nine rounds of funding around highly abstract narratives like new L1s, Flashbots/MEV—driven by “patience + faith (hopium)” —to the opposite extreme: only betting on DeFi projects. This is essentially an overcorrection.

But the pendulum will eventually swing back.

For DeFi projects, pricing based on quantitative fundamentals is indeed a sign of industry maturity; however, for non-DeFi sectors, qualitative fundamentals remain equally important: including culture, technological innovation, disruptive ideas, security, degree of decentralization, brand value, and industry connectivity. These dimensions cannot be simply reflected in TVL or on-chain buyback data.

So, what happens next?

The expected returns for token projects have clearly contracted, while equity-based businesses have not experienced a comparable cooling. This divergence is particularly evident in early-stage and growth-stage investments:

In the early stages, investors have become more price-sensitive toward projects with a token-based exit strategy; meanwhile, interest in equity-based projects has risen significantly, particularly given the currently favorable merger and acquisition environment. This contrasts sharply with the period from 2022 to 2024, when token-based exits were the default path, underpinned by the assumption that "token valuation premiums would persist."

In the later stages, investors with brand advantages and resource capabilities within the crypto-native ecosystem are gradually moving away from purely “crypto-native” projects and instead betting more on “web2.5” companies—whose valuation logic is increasingly anchored in real revenue growth. This brings them into a new and unfamiliar competitive arena: one where they must directly compete with cross-domain funds and traditional Web2 fintech funds (such as Ribbit Capital or Founders Fund), which have deeper expertise in traditional finance, portfolio synergies, and access to early-stage opportunities.

The entire cryptocurrency venture capital industry is entering an "attribution period."

Who stays depends on whether they can find their own product-market fit (PMF) in the founders' eyes—where this "product" is not just capital, but also a combination of brand identity and tangible empowerment capabilities.

For high-quality projects, VCs must instead “sell themselves” to founders to earn a place on the cap table. Especially over the past few years, some of the most successful projects have relied minimally on institutional capital (e.g., Axiom) or have raised no funding at all (e.g., HYPE). If a VC can offer nothing but capital, it is almost certain to be marginalized.

True VCs worthy of staying at the table must clearly answer two questions:

First, what is its brand identity—why would the best founders come to it voluntarily;

Second, where does its value increase lie—ultimately determining whether it has the capability to win that transaction.