As a cryptocurrency giant listed on Nasdaq, this move marks Coinbase’s institutional custody business as it transitions from the fragmented era of state-by-state regulation into the unified era of federal oversight.

Article author, source: 0x9999in1, ME News

I. Core Event Analysis: Unpacking the Real Significance of the Approval of "Coinbase National Trust"

On April 2, 2026, the largest U.S. cryptocurrency exchange, Coinbase, officially announced that it has received "conditional approval" from the Office of the Comptroller of the Currency (OCC) to establish the Coinbase National Trust Company (CNTC). As a cryptocurrency giant listed on Nasdaq, this move marks Coinbase’s institutional custody business transitioning from a fragmented era of state-by-state regulation to a unified era under federal oversight.

To truly and profoundly understand this event, it is essential to first clarify the absolute authority of the OCC (an independent agency under the U.S. Department of the Treasury) within the U.S. financial regulatory system, as well as the fundamental distinction between “trust banks” and “commercial banks.”

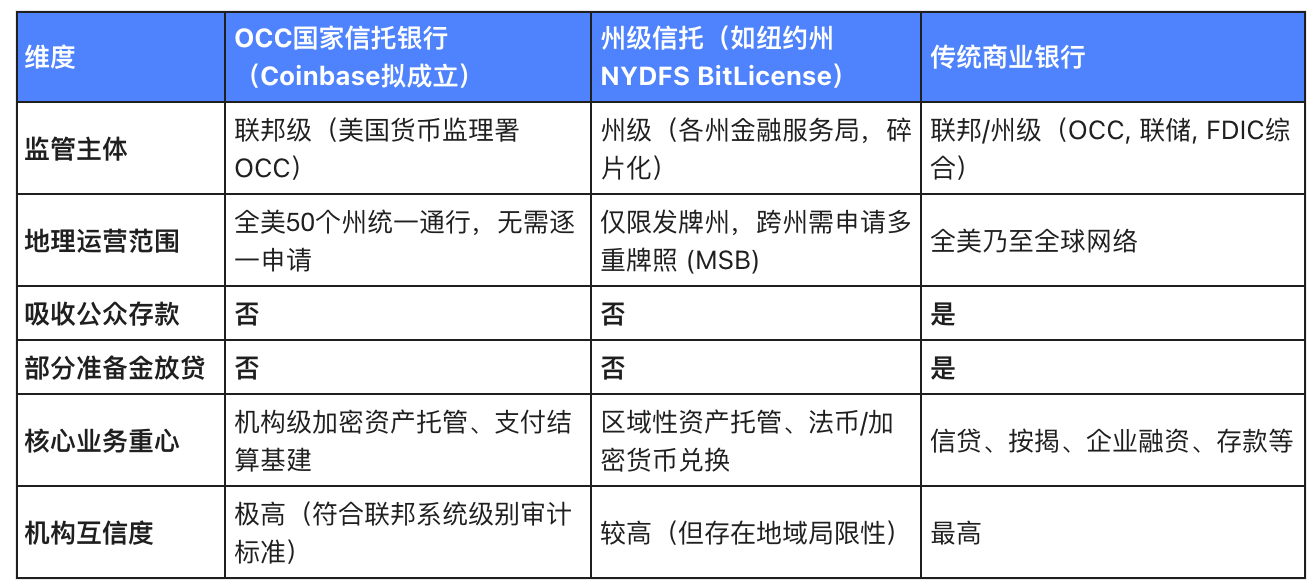

Clarify identity and authority boundaries: it is a trust, not a commercial bank.

In the public perception—and even among some market participants—obtaining OCC approval is often misinterpreted as “crypto companies becoming banks.” This is a highly misleading signal. Shortly after receiving approval, Coinbase co-CEO Greg Tusar explicitly stated that Coinbase will not become a commercial bank.

From a licensing perspective, the National Trust Charter is a special-purpose financial institution. It grants Coinbase the authority to provide asset custody, trust management, and investment settlement services across the United States, while strictly excluding the two core privileges of traditional commercial banks: accepting retail demand deposits and engaging in fractional reserve banking. This means Coinbase National Trust cannot lend out user custodial funds to earn high interest spreads, as JPMorgan Chase or Bank of America do; its core business model will remain focused on charging custody fees, settlement fees, and providing financial infrastructure services.

This delineation of the permission boundary not only aligns with the high-risk nature of crypto assets as “bearer instruments,” but also serves as an effective firewall for regulators to prevent the contagion of extreme volatility in the crypto market from affecting traditional banking balance sheets.

The meaning of "conditional approval": The final exam toward full compliance

It is important to note that the OCC has granted a “conditional approval.” This is not a blank check to begin operations immediately. Before the Coinbase National Trust can fully launch, Coinbase must still pass a series of rigorous pre-opening OCC examinations, formally establish its charter, and build a compliance and risk management system along with payment channels that meet federal standards. This typically requires months of preparation and finalization.

Table 1 clearly illustrates the key differences between this newly approved national trust and previous state-level trusts and traditional commercial banks:

II. Supporting Data and Industry Trends: Why Federal Trust Is an Irreversible Path

ME News Think Tank believes that Coinbase’s approval is not an isolated event, but an inevitable outcome of cryptocurrency finance evolving from marginal innovation into a core asset class on Wall Street. Behind this lies the practical logic of massive asset volumes forcing regulatory upgrades, as well as a profound strategic shift in the entire Web3 industry.

Regulatory focus triggered by 13% market capitalization concentration

Data is the most direct mirror reflecting deep structural changes in the industry. By the end of 2025, the total assets under custody (AUC) managed by Coinbase Custody had reached an astonishing $376 billion, accounting for approximately 13% of the global cryptocurrency market cap at the time. Furthermore, over 80% of digital asset ETFs launched globally—including spot Bitcoin and Ethereum ETFs from Wall Street giants like BlackRock and Fidelity—have selected Coinbase as their designated custodian for underlying assets.

The extreme concentration of assets has made Coinbase effectively exhibit characteristics of a Systemically Important Financial Infrastructure. Holding hundreds of billions of dollars in bearer assets on public blockchains—assets that lack the “freezing” or “retrieval” mechanisms found in traditional banking systems—creates risk exposure that state-level regulation alone cannot fully address. Therefore, the OCC’s six-month in-depth review of Coinbase (longer than the five months required to process Circle and Ripple’s applications by the end of 2025) reflects federal regulators’ cautious assessment of this systemic concentration risk and the urgency of formally bringing it under national regulatory oversight.

A paradigm shift from "evading regulation" to "fully embracing it"

Looking back at the history of the crypto industry, early companies often exploited regulatory gaps or chose offshore jurisdictions favorable to cryptocurrencies for "regulatory arbitrage," such as the collapsed FTX. However, the compliance landscape in 2026 has undergone a dramatic transformation.

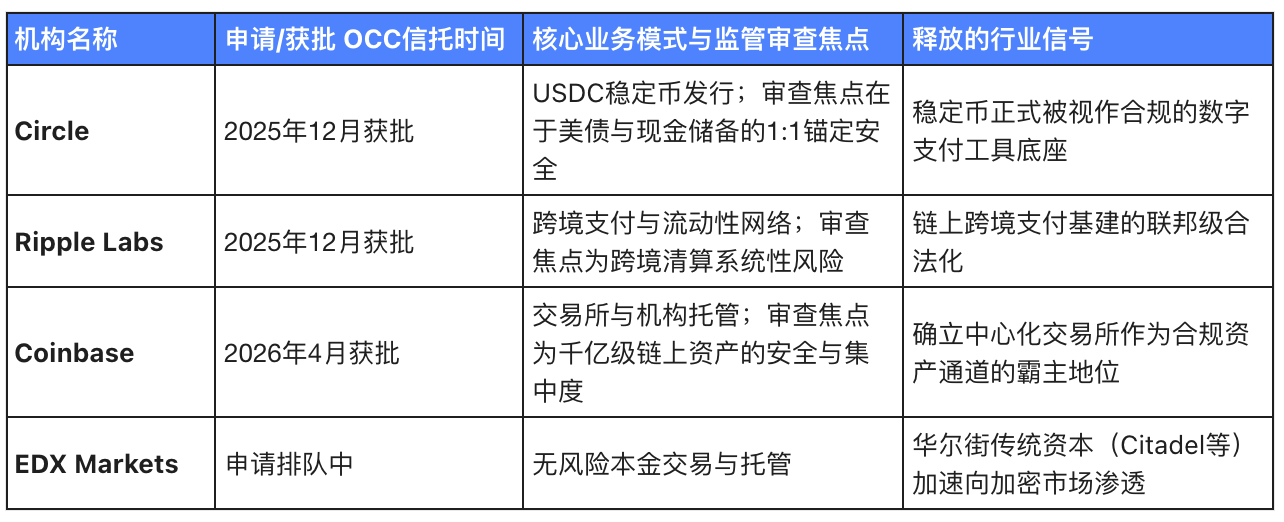

The compliance pathway centered on “embracing the system” — through the system, not around it — has become the only viable option for industry giants. In December 2025, the OCC collectively approved national trust charters for a group of crypto and payment leaders, including Circle (focused on cash and U.S. Treasury-backed stablecoin structures), Ripple Labs, Fidelity Digital Assets, and Paxos. Now, with Coinbase’s addition, the final critical piece of the federal compliance puzzle for top U.S.-based crypto firms has been filled, signaling that the industry’s competitive barrier has fully evolved from early-stage “technological first-mover advantage” to “depth of compliance and moat.”

III. A Three-Dimensional Perspective on the Profound Market Impact: What Core Signals Have Been Released?

Viewing this approval merely as Coinbase gaining another compliance badge is undoubtedly short-sighted. From an independent analytical perspective, we believe this event will generate profound ripples across three dimensions of the future financial landscape.

Signal 1: Completely break down the final "psychological barrier" for traditional finance (TradFi) giants to enter.

For a long time, the primary barrier preventing larger traditional financial capital—such as large pension funds, sovereign wealth funds, and conservative hedge funds—from entering Web3 has not been Bitcoin’s volatility, but rather the security and compliance standards of asset custody.

Many top asset management firms are restricted by internal compliance charters—such as the strict definition of “qualified custodians” under the Investment Company Act of 1940—from entrusting billions of dollars in assets to an entity regulated only at the state level (e.g., one holding only a New York State BitLicense). After Coinbase’s elevation to a federal-level national trust, its operations will be directly subject to federal standards for auditing, anti-money laundering (AML) regulations, and asset segregation rules. This is akin to granting crypto asset custody a “federal inspection exemption,” eliminating legal uncertainty caused by conflicting state laws and enabling top institutional asset managers, who have been holding back, to allocate crypto assets within a compliance framework comparable to traditional custodian banks such as BNY Mellon and State Street.

Signal Two: Advancing Beyond Crypto-to-Crypto Trading Toward the Next-Generation Payment and Settlement Network

The exchange's revenue model heavily relies on trading fees, which fluctuate with market bull and bear cycles—a long-standing pain point for institutions like Coinbase. Another significant, albeit hidden, benefit of this national trust license is that it removes legal barriers to expanding into broader financial services, particularly payments and clearing.

As revealed by Coinbase’s Chief Legal Officer, Paul Grewal, beyond asset custody, Coinbase’s long-term vision is to collaborate with the OCC to develop other infrastructure products, including payments. Holding a national trust charter enables Coinbase to directly access certain federal banking and settlement network infrastructures, significantly reducing friction costs for cross-state fund transfers. Combined with its incubated Layer 2 network, Base, and its actively promoted stablecoin ecosystem, Coinbase is fully capable of building a compliant and efficient on-chain fiat-to-crypto real-time settlement network independent of traditional SWIFT or ACH systems. This marks Coinbase’s transformation from a mere “trading platform” into the foundational clearing center of the Web3 era.

Signal three: Clear indication that U.S. regulators are reclaiming authority over cryptocurrency financial regulations

Raise your perspective to the macro-level博弈. The OCC's approval of Coinbase's trust comes at a time when Washington is deeply engaged in intense debates over cryptocurrency legislation, such as the proposed CLARITY Act and GENIUS Act concerning stablecoin regulation. For years, regulatory gaps and jurisdictional disputes among the U.S. SEC, CFTC, and individual states have caused a significant exodus of crypto innovation toward Europe (MiCA) and Asia (Hong Kong and Singapore).

By issuing a national license, OCC is sending a powerful message from a U.S. federal agency: the United States has both the willingness and the capacity to keep its most critical cryptocurrency financial infrastructure within its borders and fully subject to its national regulatory framework. This is not only a major benefit for domestic U.S. crypto companies, but also a strong signal to global markets that the U.S. is accelerating its efforts to establish federal-level digital asset regulatory standards.

Four, ME News Think Tank Independent Analysis and Strategic Outlook

Based on the above analysis, ME News Think Tank presents the following core judgment:

- The compliance-driven purge of “good money driving out bad” has been completed.

- In the future, regional exchanges or custodial institutions that fail to secure substantive regulatory endorsement at the federal level will be completely marginalized in the battle for institutional clients. Compliance costs will rise sharply, becoming the strongest barrier to entry for new players. The moat built by Coinbase through years of compliance investment will transform into a significant market monopoly premium over the next 3 to 5 years.

- The boundary between TradFi and Crypto will shift from “opposition” to “seamless integration.”

- With Coinbase and Circle receiving federal recognition, traditional banks (such as JPMorgan Chase and Morgan Stanley) and crypto-native companies will no longer be entirely opposing competitors. We will see more strategic partnerships: traditional banks will leverage Coinbase’s national trust charter to safely provide crypto exposure to high-net-worth clients, while crypto companies will tap into traditional banks’ vast capital pools to achieve liquidity.

- Potential risk warning: The dual-edged effect of regulatory compliance.

- Despite its promising prospects, becoming a federal agency comes at the cost of complete transparency and restrictions. Once officially licensed, Coinbase must meet extremely high capital adequacy and compliance audit requirements. Should any security vulnerabilities or compliance lapses arise in ongoing operations—such as failing to effectively block asset inflows from sanctioned addresses—it could face not only substantial fines but also the fatal consequence of having its federal charter revoked. Additionally, political divisions in Congress over cryptocurrency income—particularly earnings from stablecoin holdings—continue to persist. If future legislation, such as the stalled CLARITY Act, rules against interest-bearing assets, it could severely impact Coinbase’s emerging payment business built on its trust structure.

Overall, Coinbase’s “conditional approval” of an OCC national trust charter is a “D-Day” moment in the long compliance journey of the entire Web3 industry. It signals the end of the guerrilla warfare era, as crypto finance formally takes its seat at the global mainstream financial table with equal standing and controlled risk.

Source:

- Ledger Insights. (2026, April 2). "Coinbase receives conditional OCC approval for national trust charter - blockchain for enterprise."

- Crowdfund Insider. (2026, April 2). "Coinbase Approved By OCC For Conditional Charter."

- Coinbase Official Blog. (2026, April 2). "Coinbase Receives Conditional OCC Approval: Building the Future of Finance" by Greg Tusar.

- Futu News / 富途资讯. (2026, April 3). "Coinbase Secures U.S. National Bank Charter, Paving the Way for Cryptocurrency to Enter the Mainstream."

- ForkLog. (2026, April 2). "Coinbase Secures Conditional Approval for Trust Company in the U.S."