Author: 0xsammy

Compiled by Deep潮 TechFlow

DeepChaohao Summary: Over the past few months, most crypto AI projects have launched below their initial prices. However, on April 21, both OPG and CHIP launched simultaneously, backed by top-tier institutions such as a16z and Coinbase, with a 12-month investor lock-up period, and have demonstrated stable performance. This signals a return to fundamentals in crypto AI—over the next 12 months, tokens tied to real revenue streams (such as GPU financing) will become mainstream. For investors, this means focusing on projects with genuine business support rather than purely speculative token games.

This issue of Crypto AI & Robotics Communications includes three parts:

- Fragment Partner (SURF AI)

- Overview of the Crypto AI and Robotics Market

- Emerging developments

If you have any questions, feel free to contact me on X or send a message to my business account, "Khala Research".

1. Overview of the Crypto AI and Robotics Market

Three themes from this week's data:

The crypto AI space just experienced its cleanest TGE window in months: both OPG and CHIP launched on April 21, backed by tier-one institutions, structured vesting schedules, and tangible product metrics. Both performed solidly, generating optimism for upcoming token launches.

Subnet revenues are separating winners from emission farmers: Lium is up 10% over 7 days, while all other top 10 subnets are losing ground. Real GPU rental income is the catalyst.

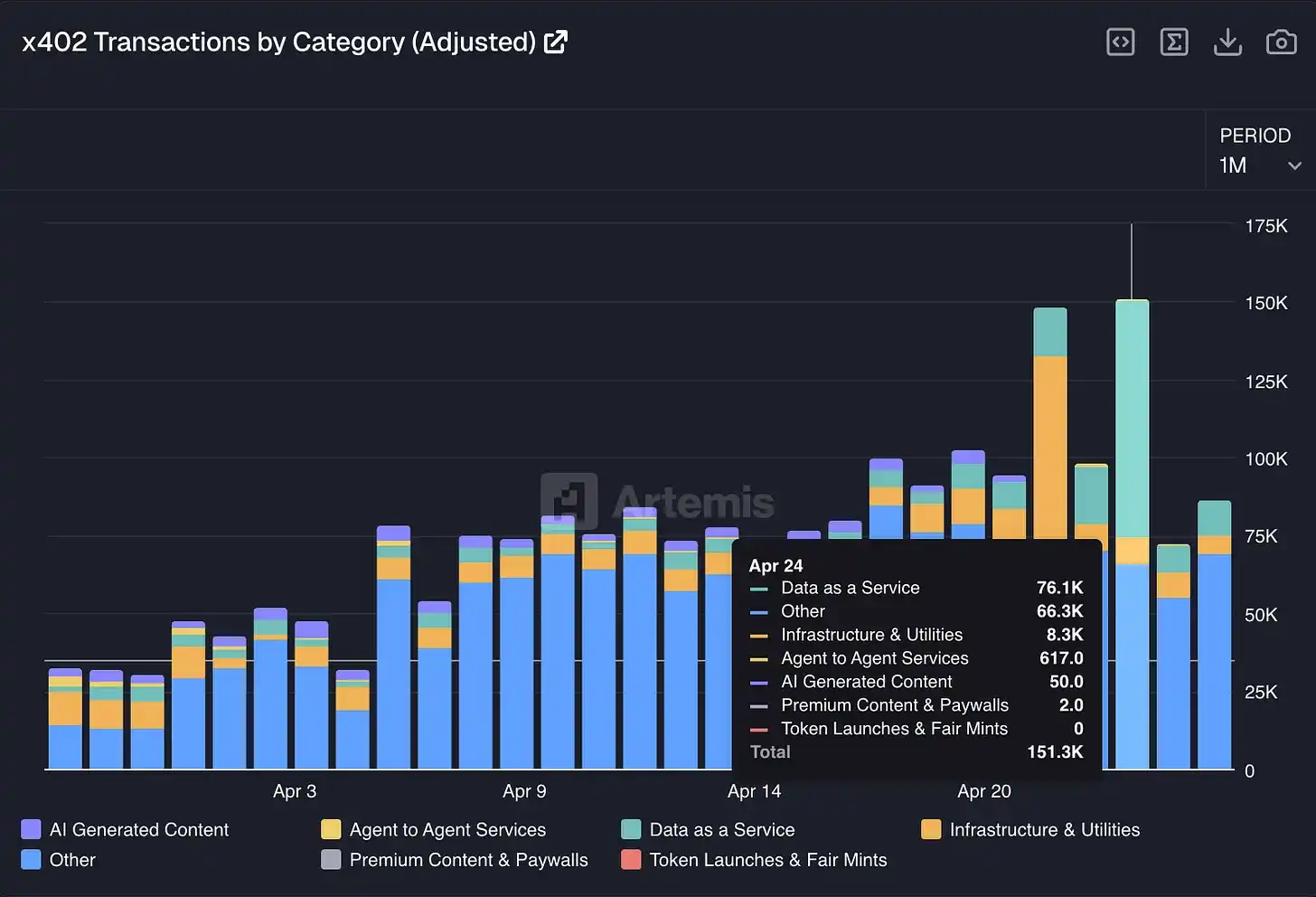

x402 event surge: Daily trading volume reached 151,000 on April 24, more than double the previous baseline. The launch of "Agentic.market" on April 20 served as the catalyst, with Data-as-a-Service emerging as the leading category.

The cleanest TGE window for crypto AI in months

OPG and CHIP both launch on April 21:

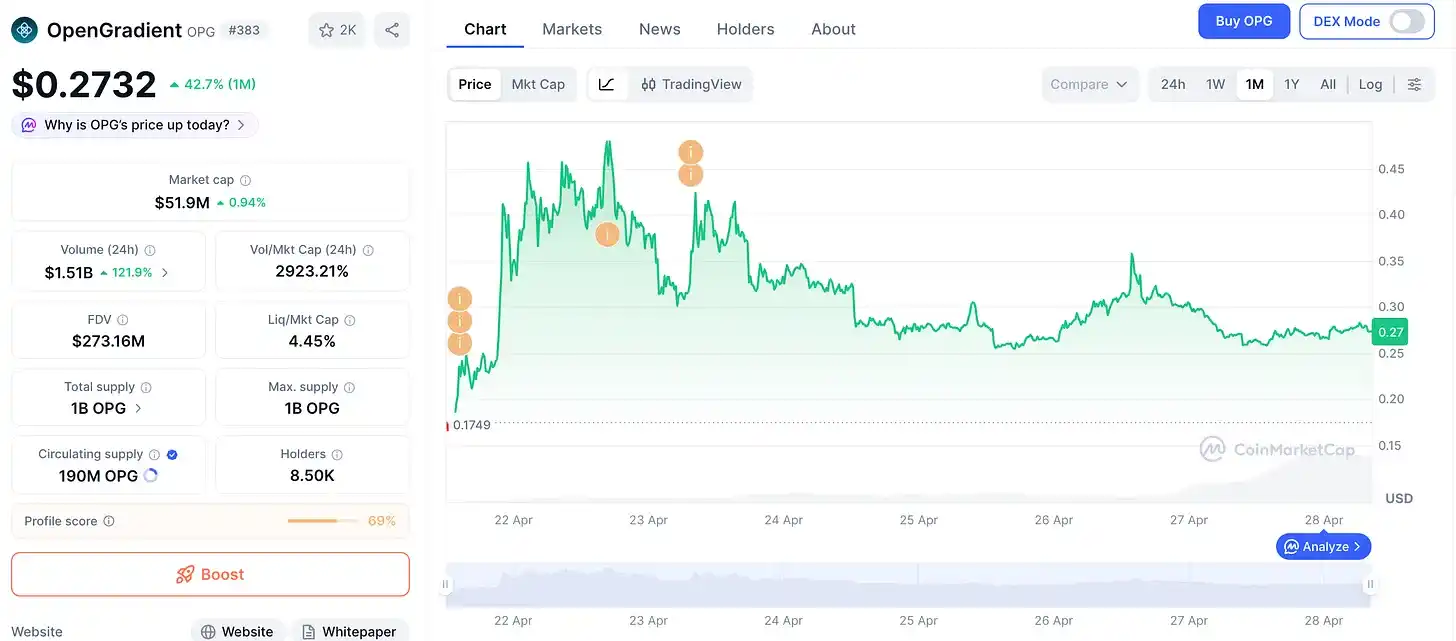

OpenGradient (OPG): Raised $9.5 million from a16z and Coinbase Ventures. 19% circulating at TGE, with a 12-month lock-up for investors, and compliance achieved via MiCAR prior to launch. Over 2 million verifiable inferences.

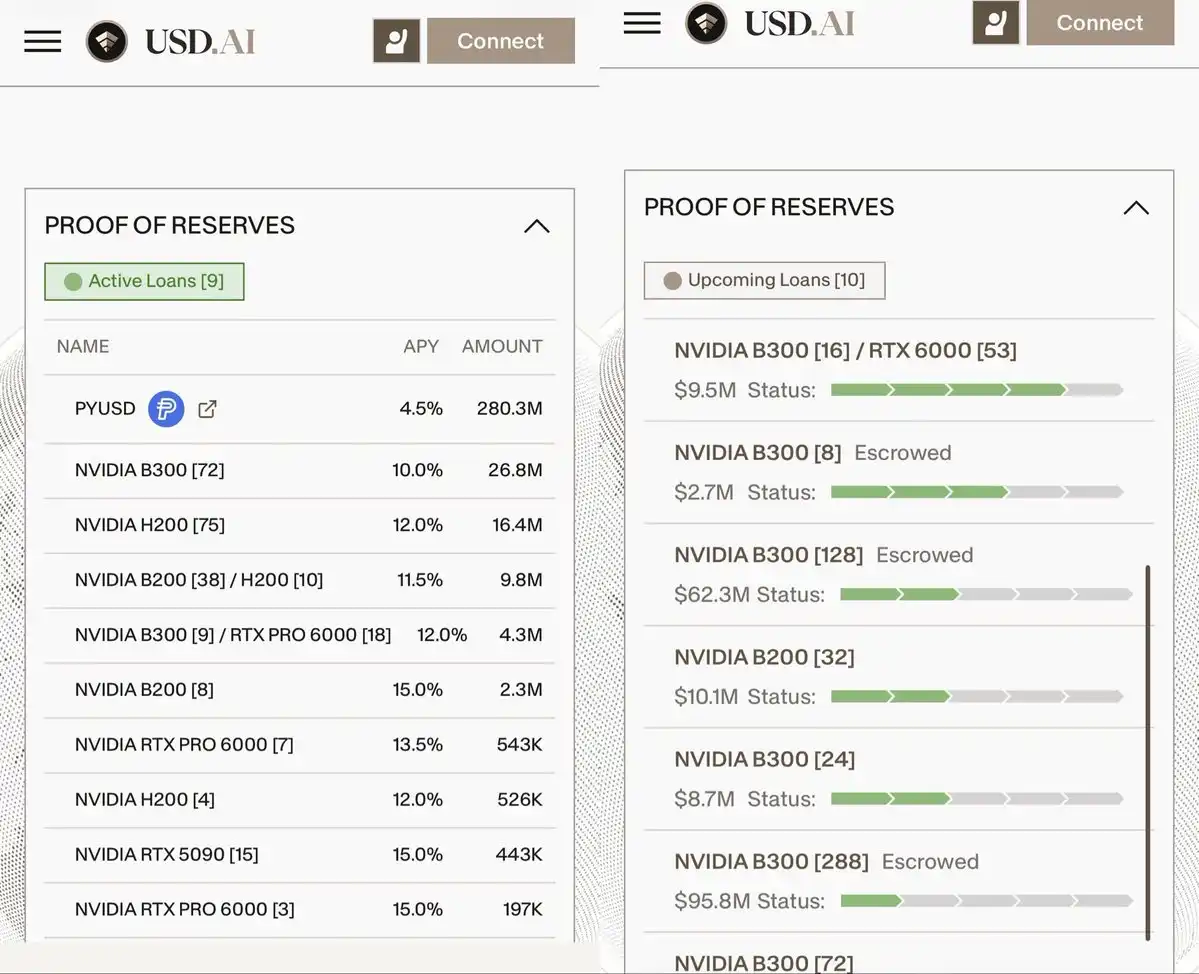

USD.AI (CHIP): Simultaneous launch on 8 exchanges. Pipeline disclosed exceeds $1.5 billion, including $500 million for Sharon AI and $500 million for QumulusAI facilities, both inaugural OBEX members. 80% locked, with a trading volume-to-market-cap ratio of 7-8x.

A larger narrative is unfolding here, one that tends to return to fundamentals.

Having a token backed by a genuinely revenue-generating product—in this case, GPU financing—with assumed revenue redistribution, will be beneficial for the token in the long term.

Over the next 12 months, we may see a broader narrative around tokenized equity or tokens linked to equity via SPVs:

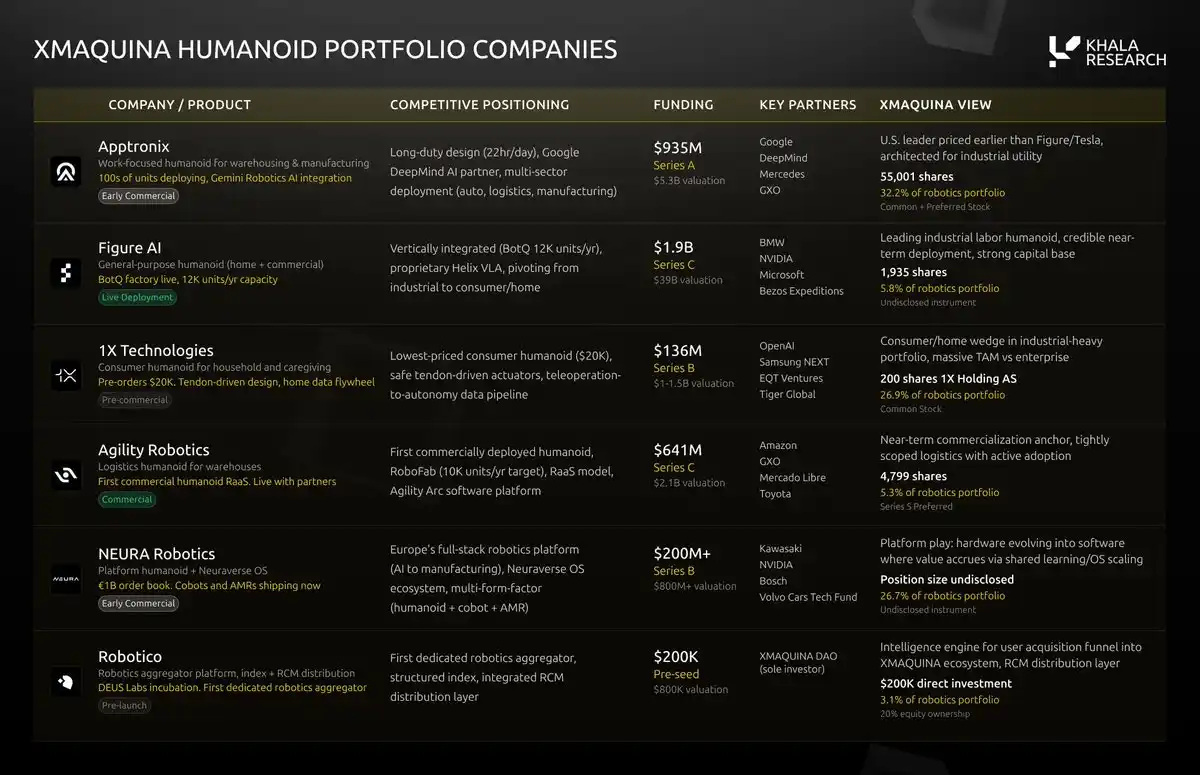

Over the next month, keep an eye on XMAQUINA, as they will conduct the TGE of their DEUS token in one month.

We will release a report on "Robotic Capital Markets" in the coming weeks, at which point individual private robotic equity (such as Apptronik, Figure, etc.) will be tradable on-chain, backed by SPVs.

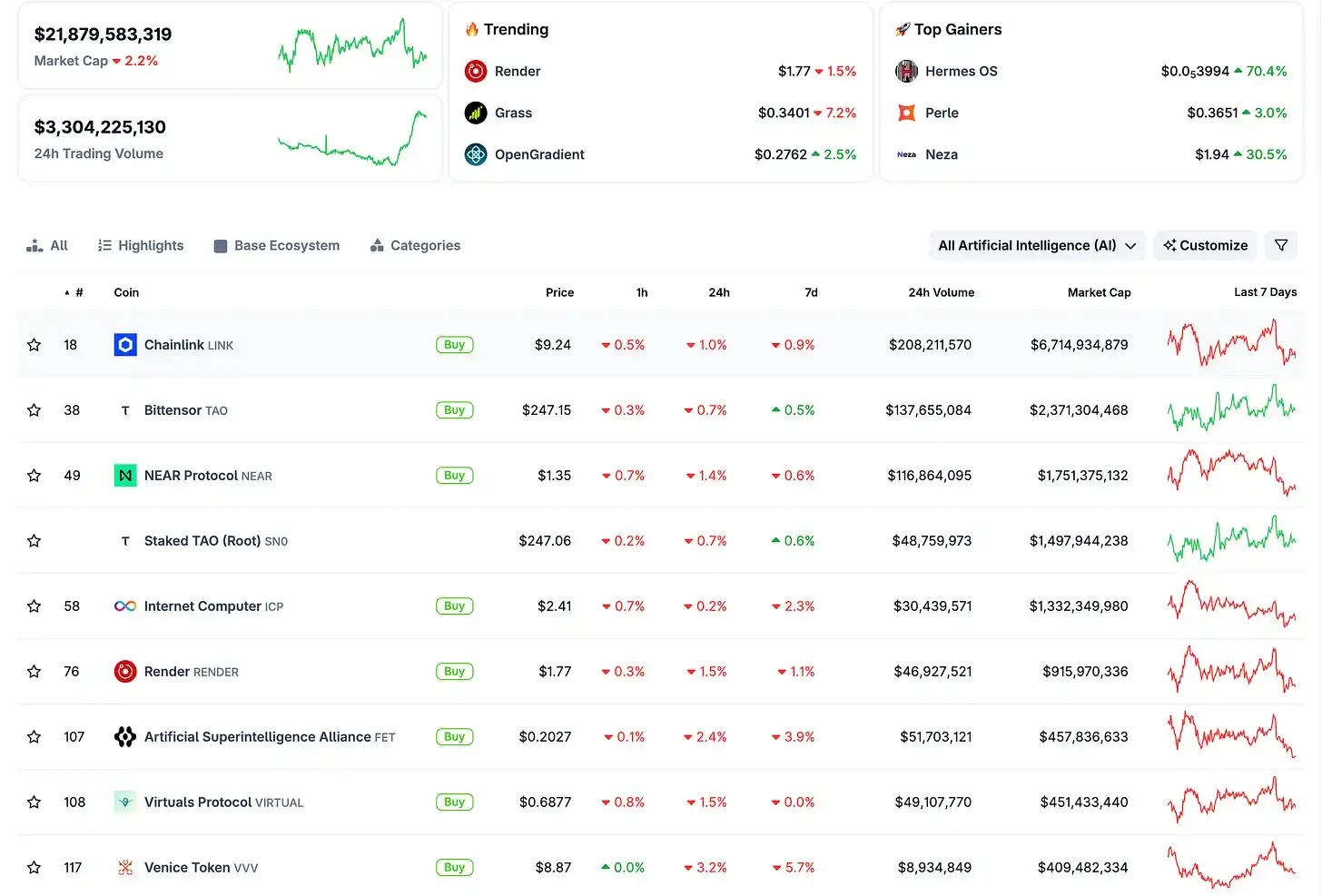

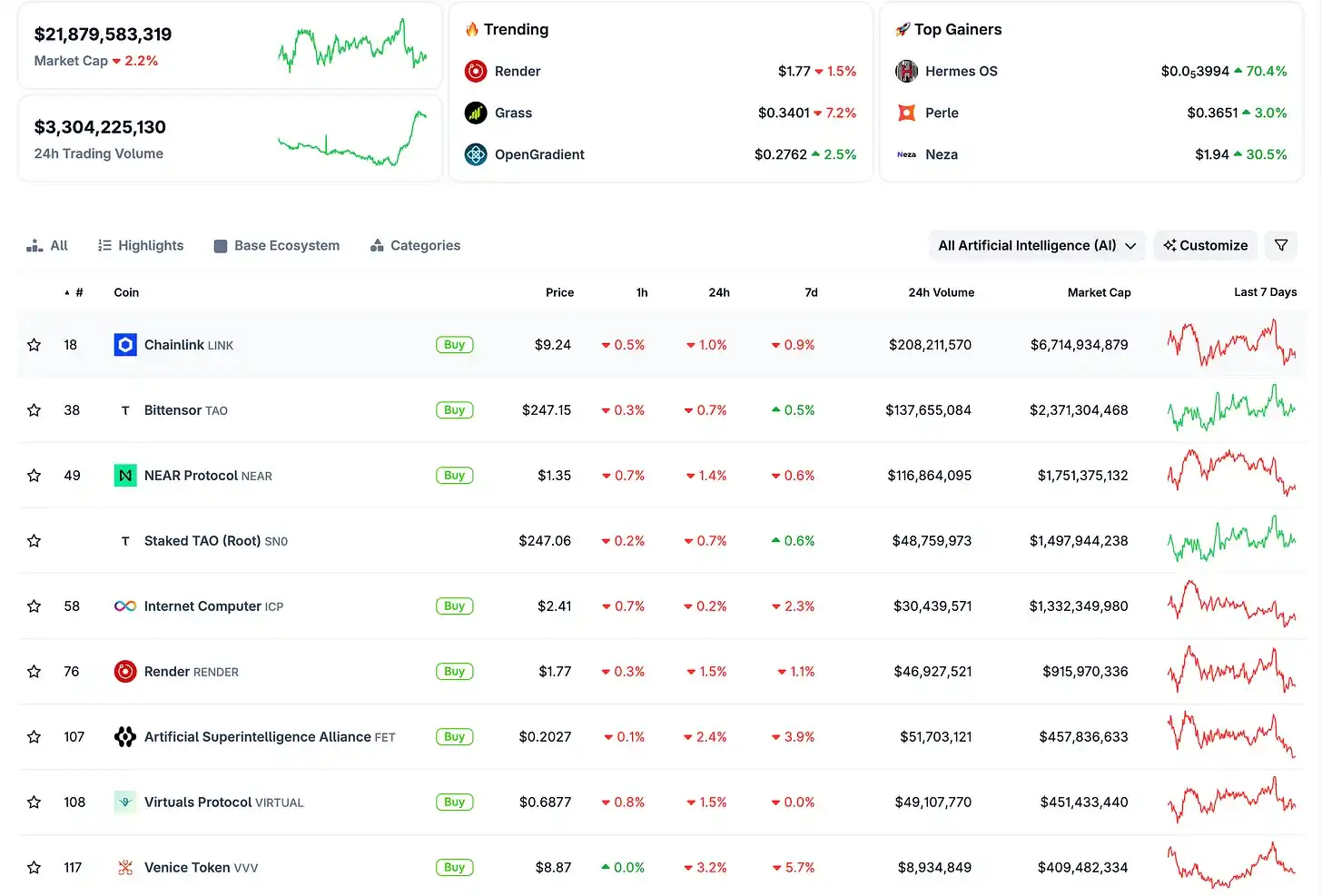

A) DeAI Market Cap Analysis

LINK ($9.24, -0.9% over 7 days): On April 23, BridgeTower leveraged the full Chainlink technology stack to tokenize $11 billion in DOM X Arizona copper-gold securities, backed by over $25 billion in natural resource assets. On April 21, Chainlink also received Deloitte SOC 2 Type 2 certification, becoming the only oracle platform to hold SOC 2 Type 2, Type 1, and ISO 27001 certifications simultaneously.

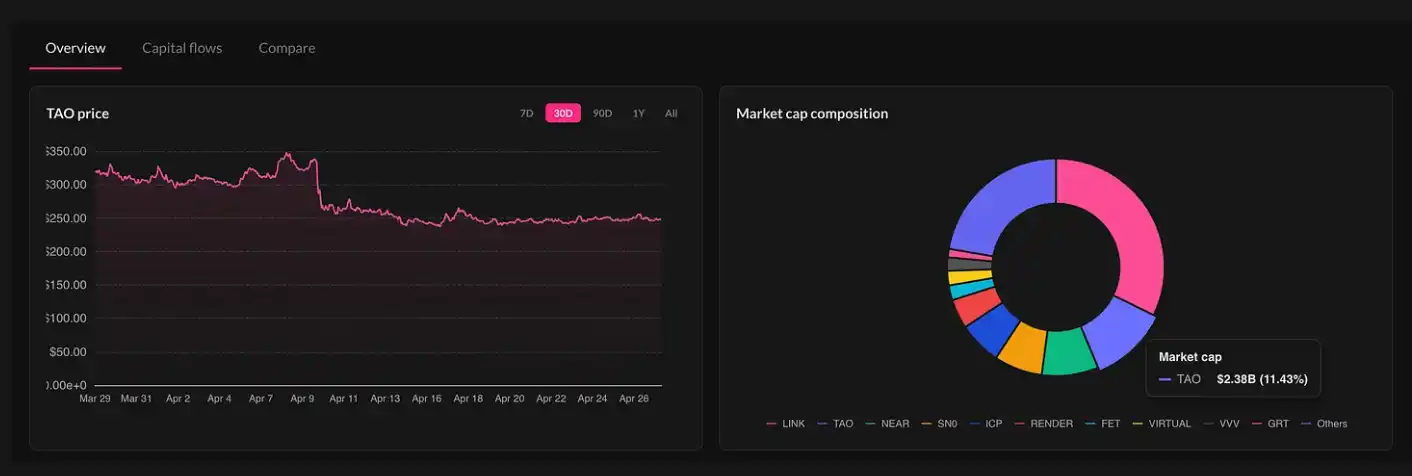

TAO ($247.15, +0.5% over 7 days): A period of calm recovery following the Covenant. 70% of the supply is staked. BIT-0011 (Belief Mechanism) voting is pending; the Teutonic 1T training run targets mid-to-late May.

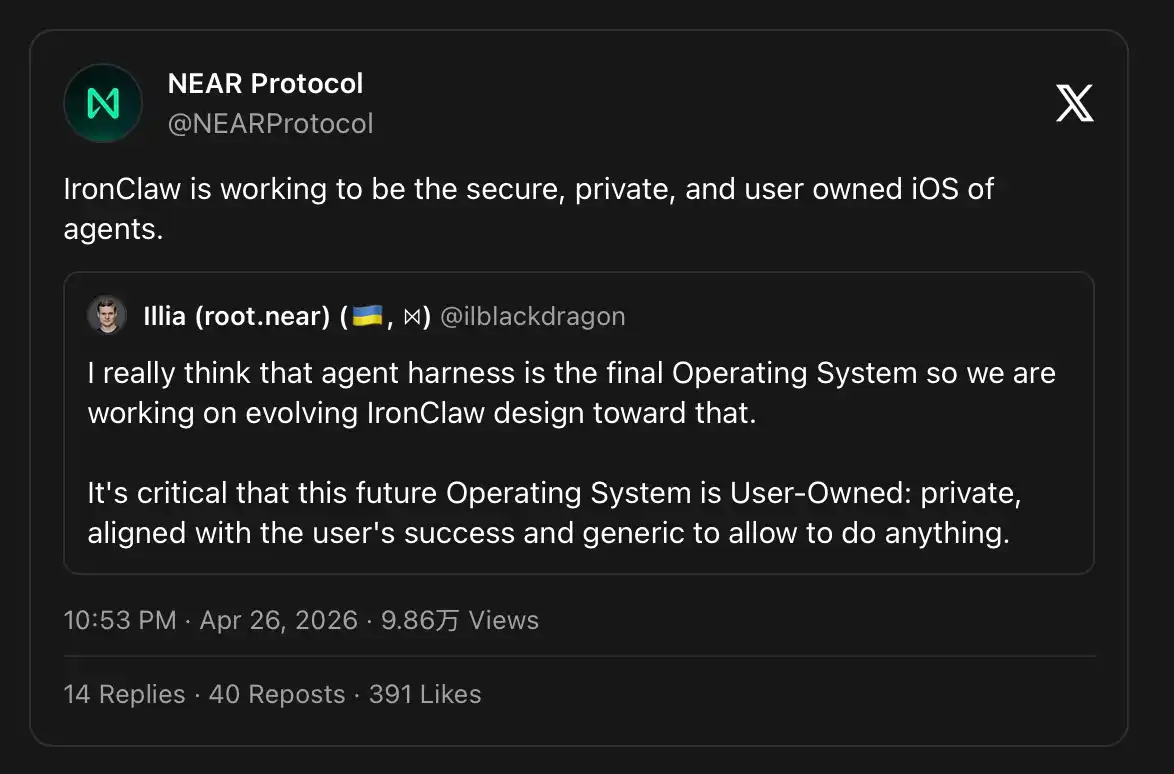

NEAR ($1.35, -0.6% over 7 days): NEAR doubles down on ironClaw as the agent orchestration framework becomes their priority:

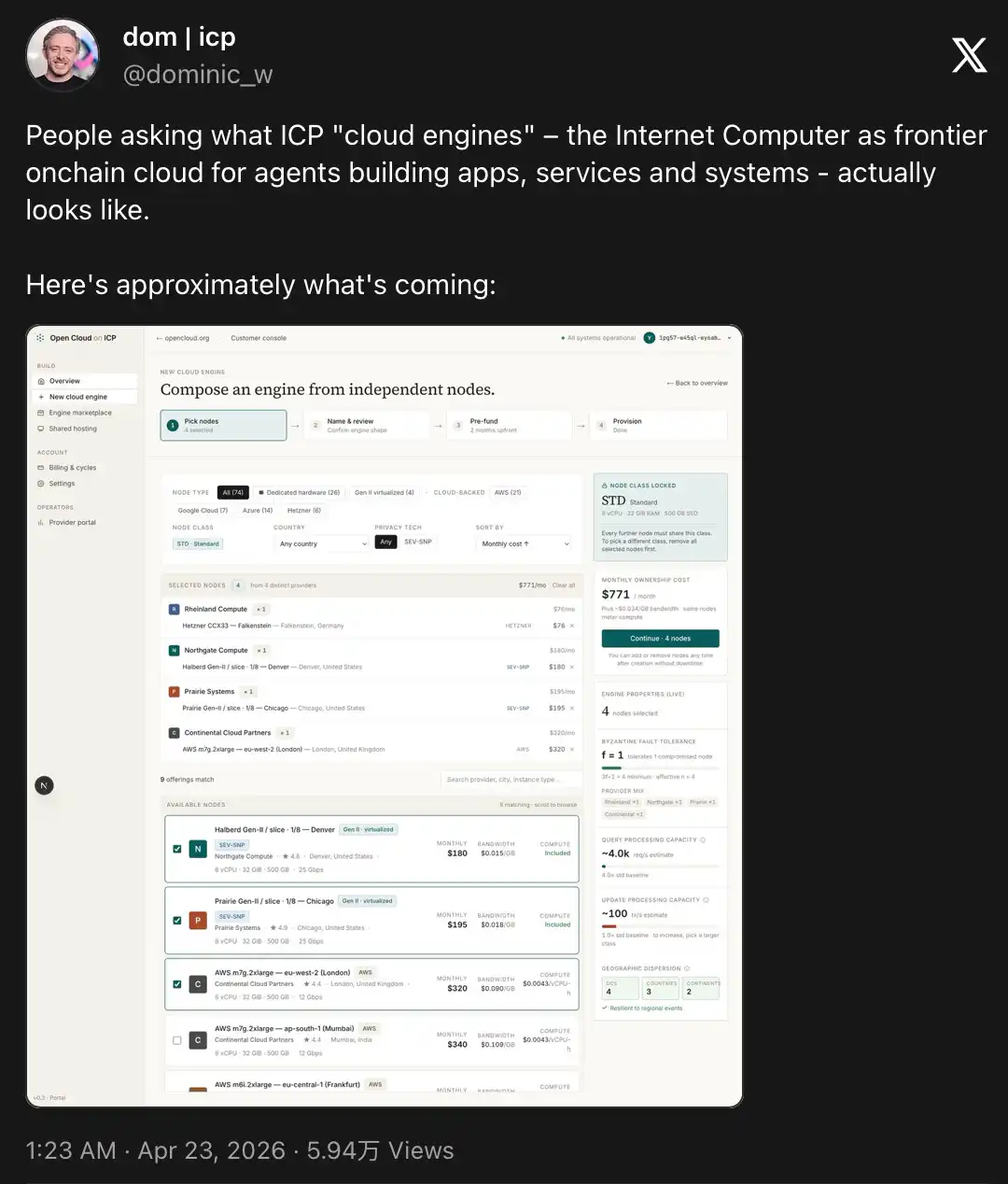

ICP ($2.41, -2.3% over 7 days): The worst-performing large-cap cryptocurrency this week. Fundamentals are improving (Caffeine v3.0 AI upgrade launched in April, 280,000 containers deployed, Mission 70 reducing inflation from 9.72% to 2.92% by year-end), but the chart is approaching historical lows. ICP Cloud Engine is coming soon:

RENDER ($1.77, 7-day -1.1%): RNP-023 was approved at RenderCon 2026 (April 16–17), integrating Salad Network as the exclusive subnet, adding approximately 60,000 GPUs to the network. The burn-mint balance mechanism routes payments through RENDER burns.

FET ($0.2027, -3.9% over 7 days): Underperformed the most over 7 days within DeAI. On April 28, 2.66 million FET ($569,000) were unlocked for AGIX migration. The ASI:Chain testnet is still pending, with mainnet delayed until late 2026 or early 2027.

VIRTUAL ($0.6877, flat over 7 days): Co-authored ERC-8183, an open standard for cross-chain agency commerce, with the Ethereum Foundation in March. Q1 2026 data: agency GDP exceeded $400 million, protocol revenue surpassed $60 million (annualized ~$300 million), with over 17,000 agents deployed + multiple updates to the Virtuals ecosystem this week.

Related tweet:

https://x.com/virtuals_io/status/2048430150619201982?s=20

VVV ($8.87, -5.7% over 7 days): Sharp reversal, but the structural narrative remains intact. Venice AI surpassed 2 million users on April 21. The April burn rate (16,600 tokens, $123,000) has exceeded the entire March total. 69% of the circulating supply is now staked; sVVV is committed to DIEM minting, with third-party protocols built around the DIEM token enabling reasoning credit rewards:

Related tweet:

https://x.com/AntSeedAI/status/2047686551509880895?s=20

Bittensor subnet ecosystem

Targon (SN4) ($14.57, +2.8% over 7 days): One of only two top-10 subnets to rise. Manifold’s $10.5 million Series A funding and Dippy’s 4 million users support the verifiable computing thesis.

Lium and subnet revenue divergence

Lium (SN51) was the only major Bittensor subnet with significant growth this week, posting a 7-day increase of 9.6% driven by rising revenue:

Approximately $432,000 in GPU rental fees per month, the highest among all subnets.

Represents 6.2% of TAO's total emission

60% of daily miner emissions are burned.

Supports multi-chain payments and fiat currencies via Coinbase.

After the Covenant upgrade, Lium's role has become even more critical. The network is being forced to demonstrate that subnets with genuine demand can maintain influence, regardless of changes in operators.

The rotation into income-generating compute and storage appears genuine—Hippius (S3-compatible storage, approximately $4.48 million in profits) and Targon are clear peers, with several other projects also showing signs of commercial viability.

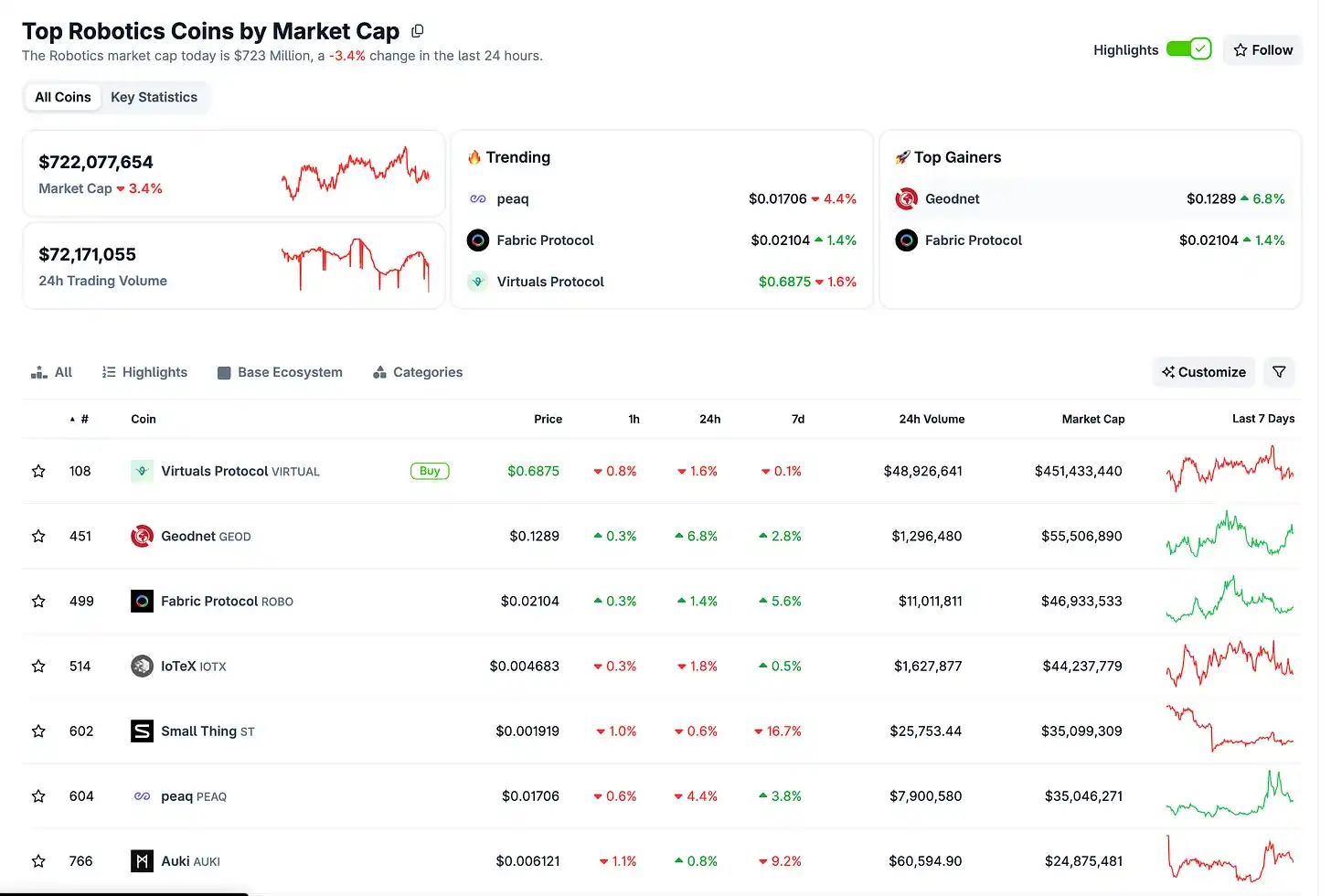

B) Robot Market Capitalization Analysis

GEOD performed strongly, rising 6.8% in 24 hours (market cap: $55.5 million), further demonstrating that revenue-generating DePIN projects can survive in a weak market. Hyfix’s $15 million funding round, led by the same founder as GEODNET, is a related positive development.

Tweet link:

https://x.com/mikeahorton/status/2044500450389725251?s=20

peaq also announced support for zero-human companies, causing a price surge in the middle of the week.

Tweet link:

https://x.com/peaq/status/2047284505614926072?s=20

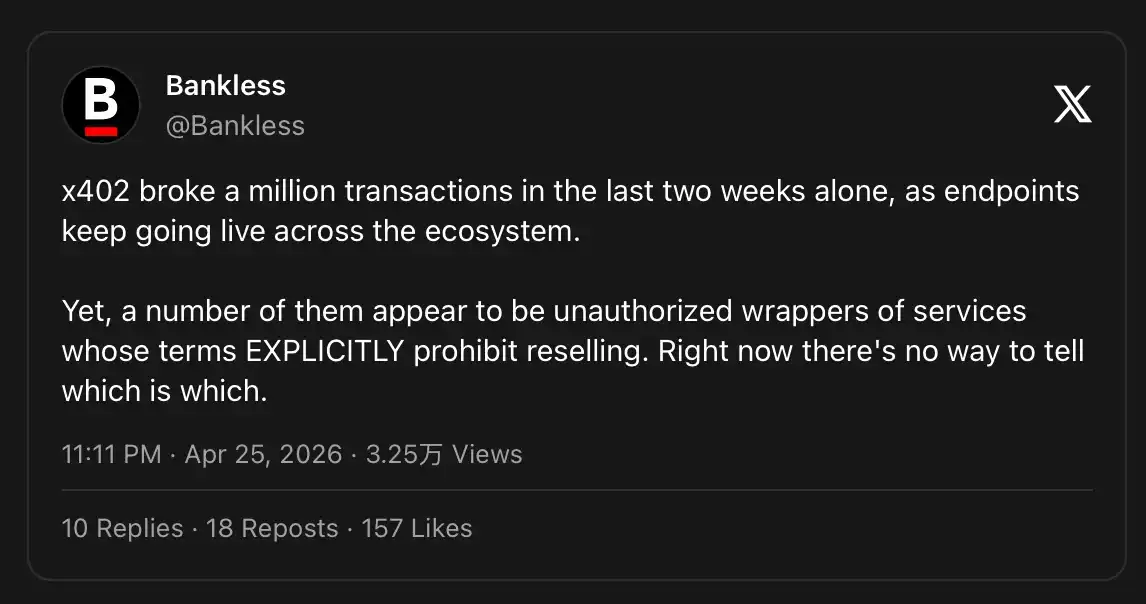

2. x402 Analysis

Trading volume for x402 surged this week. On April 24, daily trading volume reached 151,300 transactions, more than double the baseline of approximately 75,000 transactions from early to mid-April.

Data-as-a-Service surged to 76,100 transactions in a single day, up from nearly zero; inter-agent services maintained a significant share during the spike. The catalyst was Coinbase’s launch of Agentic.market on April 20.

Three specific updates to the agency market this week:

Scale: x402 has processed over 165 million transactions, with a cumulative trading volume of approximately $50 million and more than 480,000 trading agents. Agentic.market is positioned as the discovery layer on top of it.

Tweet link:

https://x.com/base/status/2046325766091116897?s=20

This replaces the API key and credential model, enabling permissionless service access for both humans and agents.

Tweet link:

https://x.com/0xSammy/status/2046482548075671561?s=20

Initial service provider list: Seven categories have been launched (Reasoning, Data, Media, Search, Social, Infrastructure, and Trading). Participants in the initial launch include OpenAI, Bloomberg, CoinGecko, AWS Lambda, LinkedIn, Alchemy, and Venice. A unified discovery interface is now available for multi-step agent workflows (Data → Reasoning → Trade Execution → Logging).

Pricing model: Most services use a pay-as-you-go model, with some providers adding a "proxy surcharge" for automated bot access. Bazaar’s CDP Facilitator automatically indexes any x402 endpoint with the discovery extension enabled, without requiring separate registration.

The Artemis chart is the clearest evidence that the discovery layer is working:

Data-as-a-service surged before inter-agent transactions, indicating that agents input structured data into their workflows before trading with each other; this sequence is logical.

ACP still accounted for over 99% of x402 trading volume in certain weeks, with Agentic.market expanding its upper funnel rather than replacing it. The 30-day baseline starting April 20 is a metric worth tracking.

3. AI Agent Development: Innovation and Market Dynamics

Here are this week's developments in crypto AI and robotics:

Tweet link:

https://x.com/0xSammy/status/2048761483270479968?s=20

That concludes Episode 174 of Sammy's Snippets. Hope you enjoyed it.

Leave any questions or thoughts here—I’ll reply to everyone!

If you find this interesting, consider subscribing to this Substack and following me on X for more related insights.

If you're interested in a formal report on crypto AI and bots, Khala is my research product.

Disclaimer: The content of this communication is for informational purposes only. Nothing herein constitutes financial advice or a recommendation to buy or sell any asset. Please conduct your own research before making any investment decisions.

I hold positions in many of the assets discussed in this newsletter. For a full disclosure list, please visit the Khala Research website.