Nearly ten months later, there is renewed hope that the Digital Asset Market Clarity Act of 2025 will be approved. In early May, Senators Thom Tillis and Angela Alsobrooks issued a joint statement suggesting the deal is close to its final stage.

The joint statement noted,

The result is a substantially improved, consensus-based product. Our compromise prohibits stablecoin rewards from resembling interest on bank deposits, our core concern over deposit flight.

What will change?

In light of the bipartisan agreement, digital asset service providers will no longer have to pay interest or yield to U.S. customers merely for holding stablecoins thanks to Section 404 of the CLARITY Act.

Additionally, the law also prohibits any rewards that are functionally or economically comparable to bank deposit interest. In contrast to a complete ban, Section 404 permits genuine rewards that are connected to real platform use.

The statement added,

They have had a seat at the table and have been directly sharing their feedback and ideas for months to inform the final product.

Banking groups are flagging concerns, but…

This came after recent criticism from banking groups, who noted that,

The proposed language falls short of that goal. It is imperative that Congress get this right.

Supporting their claim, banking groups cited a study showing that yield‑earning stablecoins could reduce consumer, small business, and farm loans by at least one‑fifth, underscoring the need for a clear ban.

But to prevent more delays, Senators Thom Tillis and Angela Alsobrooks noted,

Some in the banking industry may not want either of these things to happen, and we respectfully agree to disagree.

Expressing excitement on this milestone, Senator Cynthia Lummis noted,

This finalized, bipartisan text is the culmination of months of hard work to deliver a compromise on yield we can all live with. We are closer than ever to getting the Clarity Act across the finish line.

In fact, Tim Scott, the chairman of the U.S. Senate Banking Committee, had also expressed optimism about the act and stated that it will pass before the August recess.

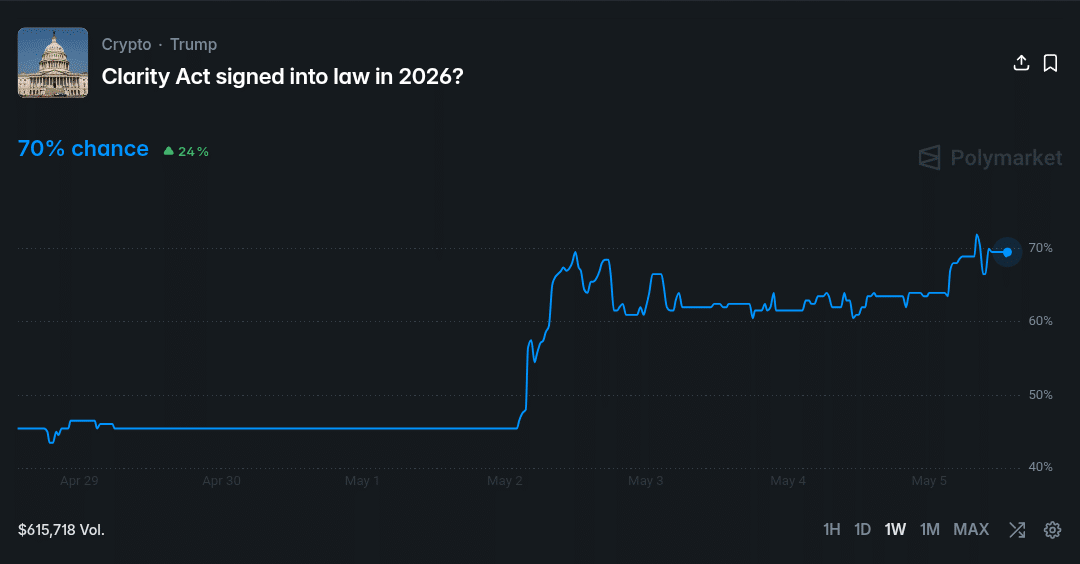

Polymarket odds and more

If approved, the CLARITY Act would finally close a perceived loophole in the earlier GENIUS Act, which barred stablecoin issuers from paying interest.

Polymarket odds stood at 70% at the time of writing, up 24% over the past week, reinforcing optimism that the CLARITY Act could become law in 2026.

Final Summary

- Senators Thom Tillis and Angela Alsobrooks have agreed to a final compromise despite the disagreements raised by the banking groups.

- The excitement that Senator Lummis and Tim Scott expressed further confirms that the compromise is a win-win for the crypto industry.