Excellent articles can cause the market to confuse "scenario planning" with "realistic prophecy."

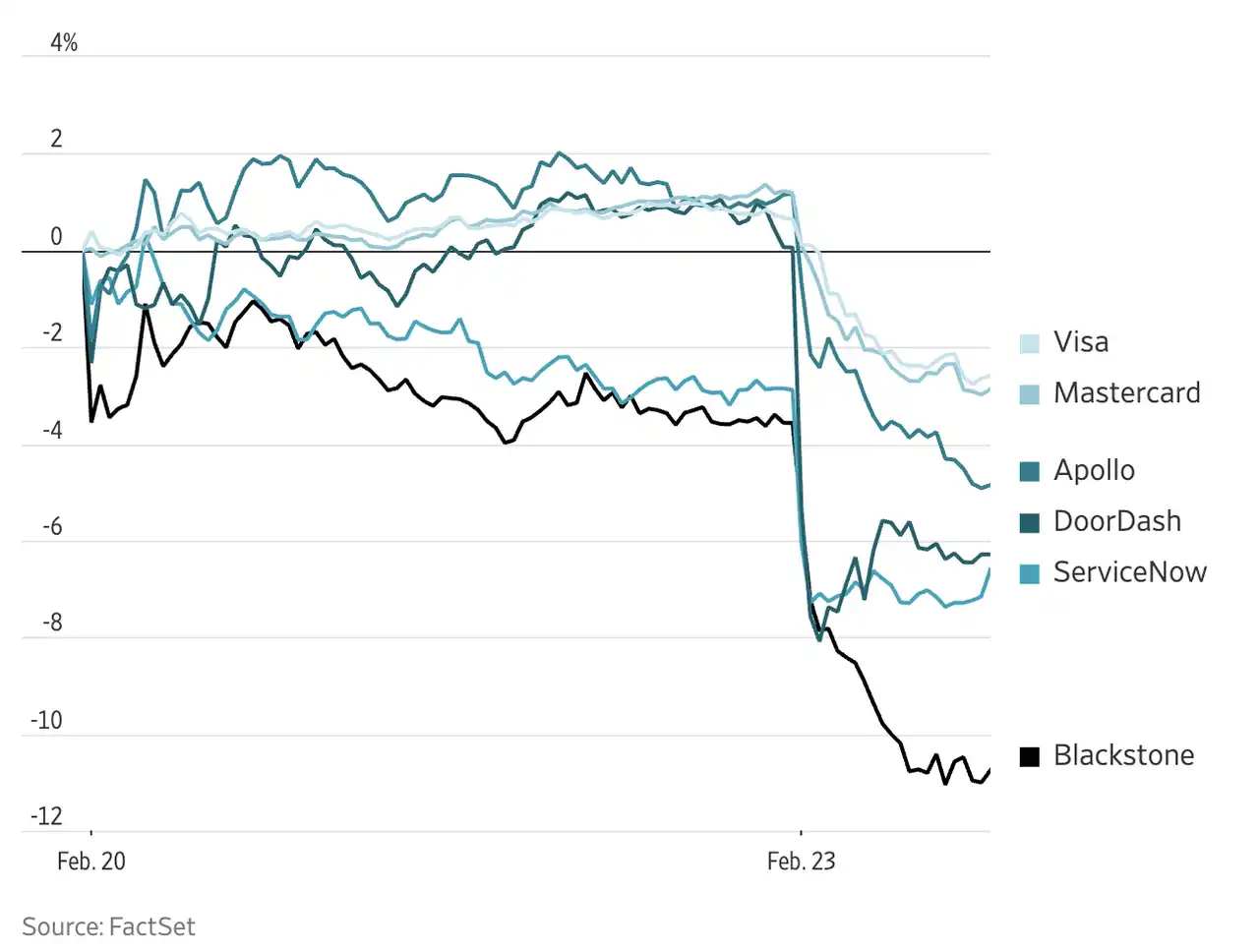

On February 22, 2026, a report titled The 2028 Global Intelligence Crisis went viral on social media and financial markets, surpassing 27 million views. On the day of its release, IBM plunged 13%, while companies such as DoorDash, American Express, and KKR all dropped more than 6%.

This report was authored by James van Geelen, founder of Citrini Research. The 33-year-old researcher has over 180,000 followers on X and ranks first among finance writers on Substack, specializing in private equity investments and global macro research with a style known for cross-asset and lateral thinking; his actual investment portfolio has returned over 200% since 2023. The report presents a fictional scenario set in 2028: AI rapidly replaces white-collar labor within just two years, triggering consumer contraction, software asset defaults, and credit tightening, ultimately pushing the economy into a distorted state characterized by "technological prosperity" alongside "social decline." Van Geelen notes at the outset: "This article describes a possible scenario, not a prophecy." But the market clearly has no patience for distinguishing between the two.

However, more noteworthy than the brief market panic is the widespread discussion this article has sparked over the past few days. From academia to the investment community, from Wall Street to Chinese internet platforms, over a dozen articles offering diverse perspectives have emerged. Rather than simply accepting one extreme viewpoint, perhaps we can piece together a clearer picture of the future by examining the “divergences and overlaps” among these various perspectives.

What did Citrini say?

The logical chain in Citrini's article is not complex: the leap in AI capabilities leads to large-scale replacement of white-collar jobs → rising unemployment triggers a contraction in consumer spending → structured financial products with SaaS as underlying assets face a wave of defaults → credit tightening spreads throughout the broader financial system → the economy falls into a distorted state characterized by coexisting "technological prosperity" and "social decline."

Each link in this chain of causality is not baseless. However, connecting them end to end and logically progressing to a crisis requires a series of rather aggressive assumptions.

There are many ways to break down this chain. Let’s examine it step by step through three core sub-arguments: the speed and scale of labor displacement, the transmission mechanism of demand collapse, and the possibility of a financial crisis—to see what different perspectives are debating at each stage.

No destruction, no creation

Citrini's scenario begins with AI大规模替代白領勞動力. In his narrative, this process accelerates sharply between 2026 and 2028, with professionals in law, financial analysis, software development, and customer service being the first affected.

Change in the share of spending by companies on AI model providers and online labor platforms, grouped by industry AI exposure level

There is empirical evidence supporting Citrini’s view. A study based on corporate spending data by Bick, Blandin, and Deming shows that after the release of ChatGPT, firms with the highest exposure to AI—those that previously spent the largest share of their budgets on online labor markets—significantly increased spending on AI model providers while reducing spending on online labor markets by approximately 15%. Notably, this substitution is not "one-for-one"—for every dollar reduced in labor market spending, firms increased AI spending by only $0.03 to $0.30. In other words, AI is performing the same amount of work at a fraction of the cost of human labor.

But Citrini may have overestimated the speed at which this shift will occur. Critics point to the U.S. real estate brokerage industry, where technology has long had the capacity to drastically reduce the number of brokers, yet the sector still employs over 1.5 million people. Institutional inertia, regulatory barriers, and internal industry interests form a far more resilient barrier than technology alone. He argues that Citrini has severely underestimated the resistance posed by "institutional momentum."

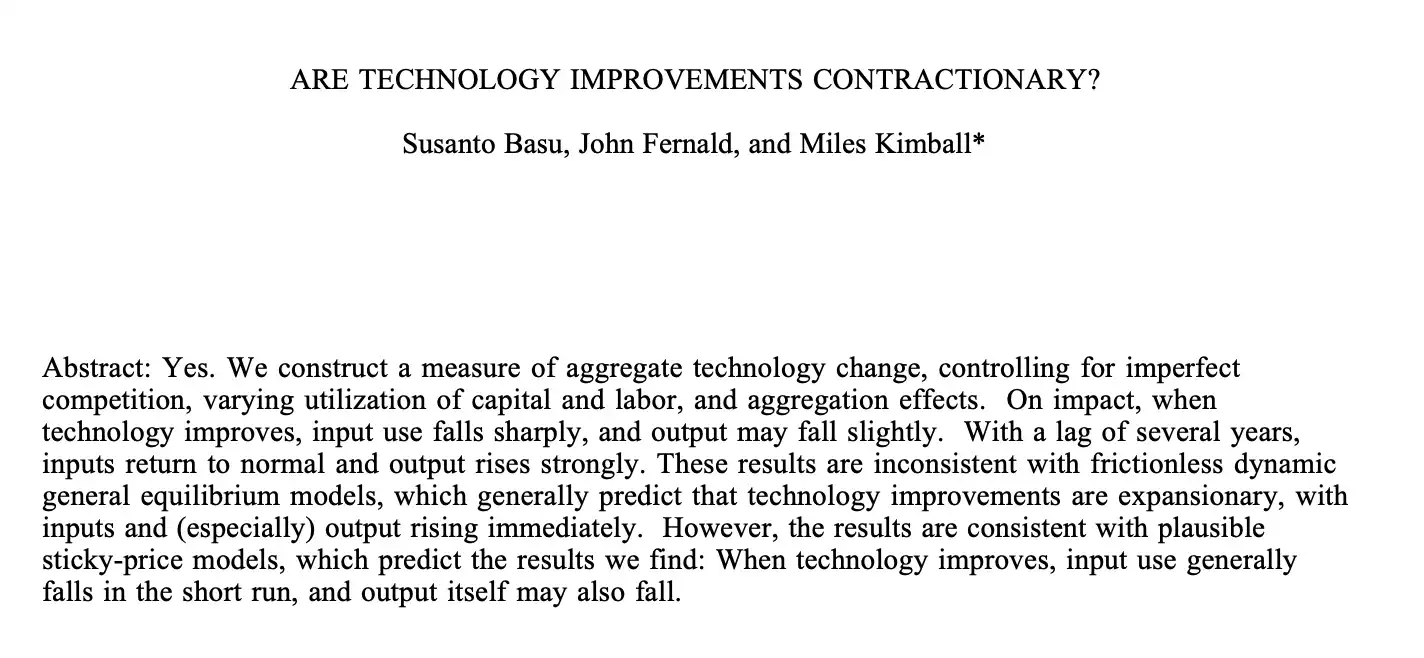

Opponents cite the 1998 study by Kimball, Basu, and Fernald, which points out that technological shocks have historically tended to act as positive supply-side stimuli—short-term adjustments in employment structure may occur, but in the long run, the output they generate far exceeds the jobs they displace.

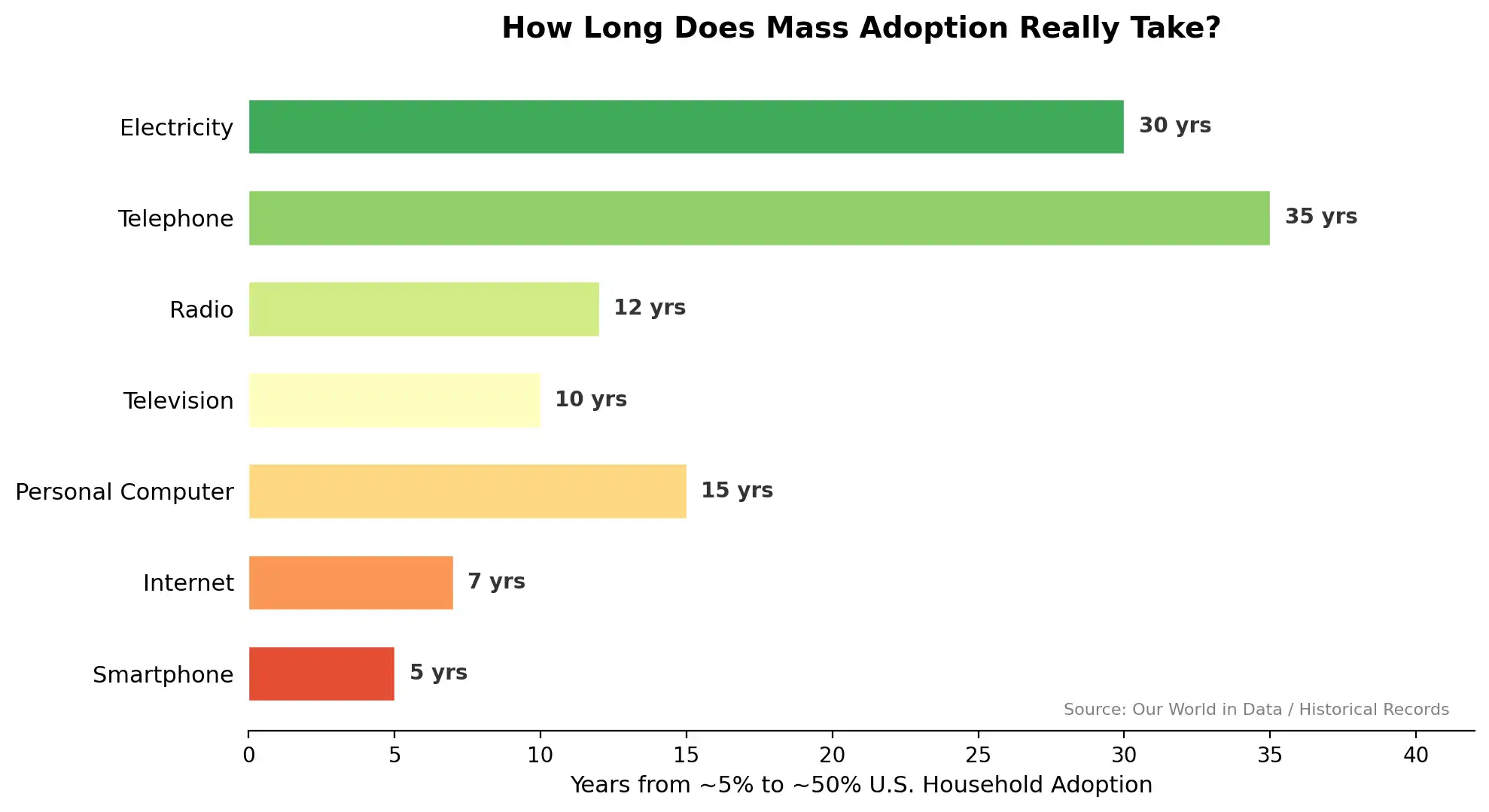

In fact, looking back at every historical cycle of general-purpose technology diffusion, the process from the laboratory to widespread adoption has always been much slower than the pace of the technology’s own maturation. Electricity took 30 years to go from 5% to 50% household penetration; the telephone took 35 years; even the fastest-diffusing smartphones required five years. While AI’s technical capabilities may already be sufficient to disrupt many industries, the gap between technical capability and institutional absorption has never been bridged by capability alone.

The second key component of the Citrini narrative is the demand-side spiral: unemployment → reduced income → contracted consumption → declining corporate profits → further layoffs.

Citrini confused demand-side deflation with supply-side deflation. The former refers to a contraction in consumers' purchasing power, while the latter reflects lower production costs driven by technological advancement—AI-driven price declines are fundamentally closer to the latter, resembling the price trajectories of electronics and communication services over the past few decades. Some analysts argue that the Jevons Paradox will still hold: when AI drastically reduces the cost of services such as legal consultation, medical diagnosis, and software development, demand previously excluded due to high prices will be unleashed, leading not to contraction but explosive growth in total volume. Meanwhile, the Moravec Paradox will also come into play. For machines, what is truly difficult is not complex logical reasoning or massive data retrieval, but rather human-ubiquitous physical movements, sensory perception, and emotional interaction. This suggests that manual labor and service jobs requiring fine perceptual skills may be more resilient than we imagine.

But the Jevons Paradox may also fail. Alex Imas, Professor of Economics at the University of Chicago, suggests that if AI automates the vast majority of labor and labor income’s share of total income plummets, who will buy the goods and services produced with such efficiency? This strikes at the very heart of the distribution mechanism. When productive capacity approaches infinity while effective demand becomes increasingly concentrated, we may be facing not a recession, but an imbalance not adequately addressed in economics textbooks—abundant material wealth that remains out of reach.

See a leopard through a tube

The most far-reaching leap in Citrini's scenario is the transmission from employment shocks to a financial crisis. In his narrative, structured financial products backed by SaaS revenue—as he calls them "Software-Backed Securities"—experienced widespread defaults amid the AI transformation wave, triggering a credit crunch reminiscent of 2008.

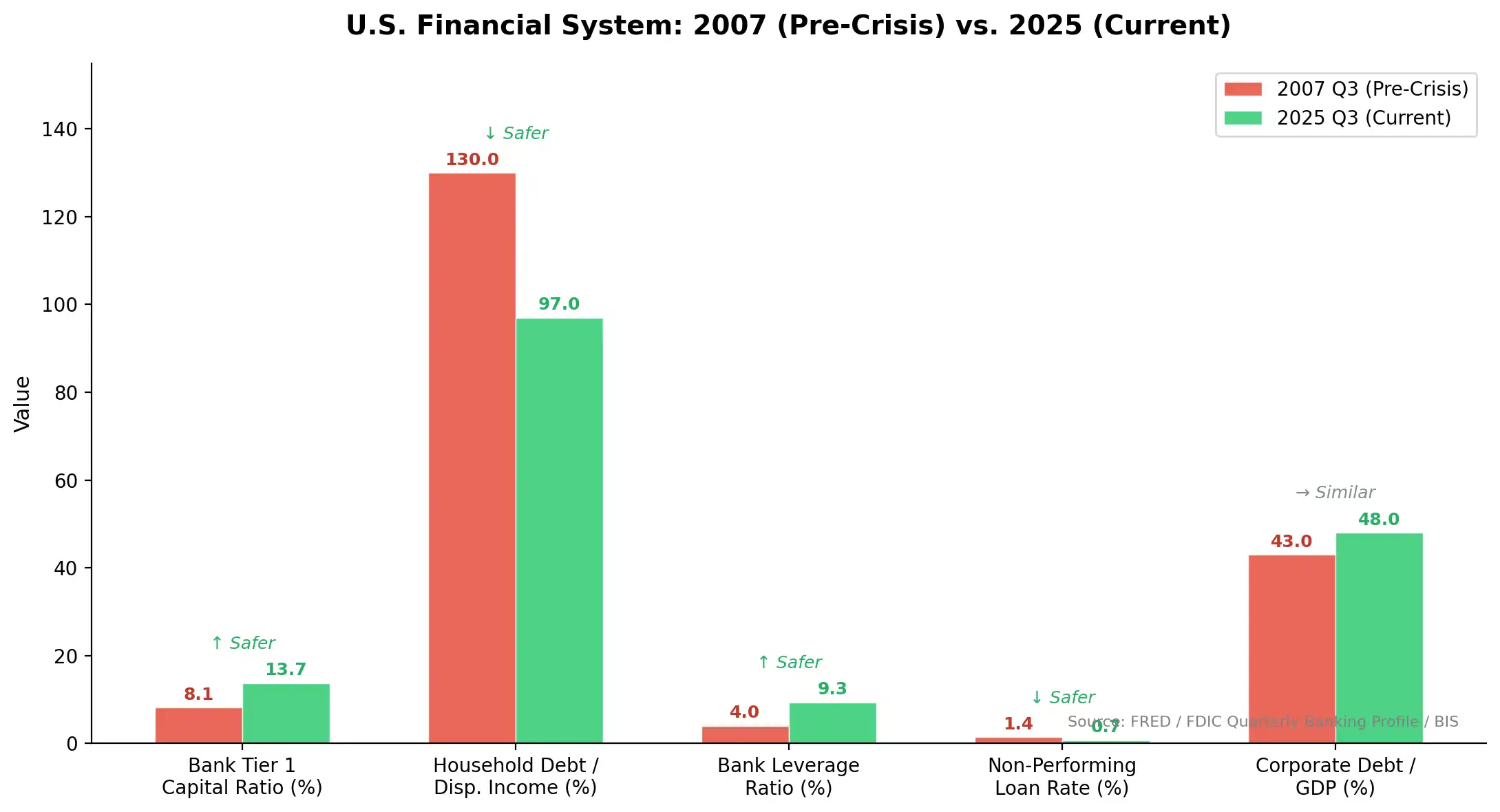

However, commentators note that the current U.S. corporate sector's leverage is far healthier than in 2008, and the banking system is much more robust following the Dodd-Frank reforms and multiple rounds of stress tests.

Compared to the period just before the 2008 financial crisis, key resilience indicators of the current U.S. financial system have improved significantly: the Tier 1 capital ratio of banks has risen from 8.1% to 13.7%, the household debt-to-disposable-income ratio has fallen from 130% to 97%, and the non-performing loan rate has declined from 1.4% to 0.7%.

Even though some SaaS companies are indeed experiencing revenue declines, their scale is insufficient to trigger a systemic credit crisis. Former Bloomberg financial columnist Nick Smith argues that Citrini has made a common mistake here: linearly extrapolating micro-level industry shocks into macro-level systemic risk. Regarding a collapse in demand, Smith’s solution is fiscal policy. If unemployment were to rise significantly, governments are fully capable and willing to support demand through large-scale fiscal stimulus.

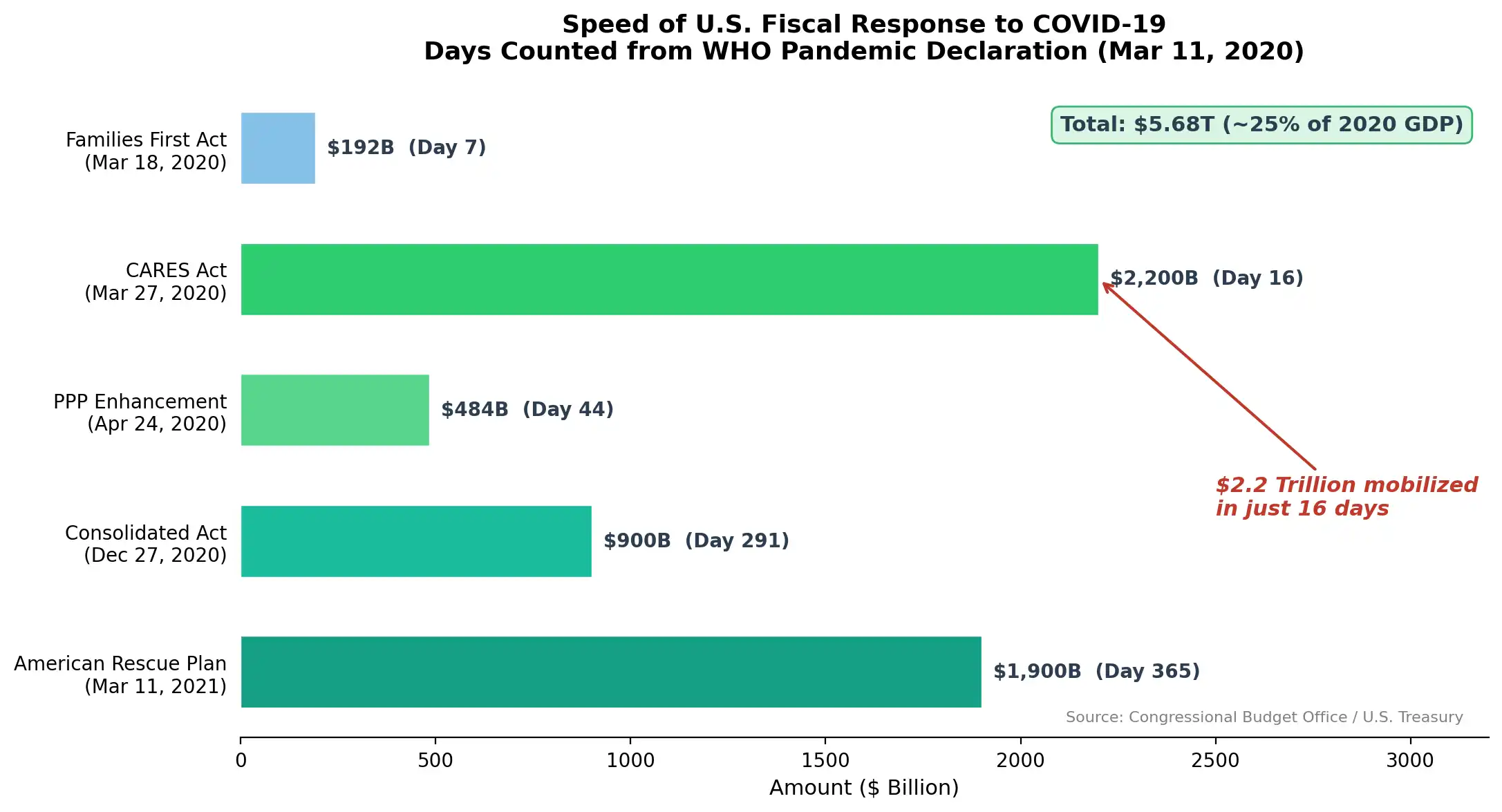

The responsiveness of institutions also appears to have been underestimated; for example, during the COVID period, just 16 days after the WHO declared a pandemic on March 11, 2020, the $2.2 trillion CARES Act was signed into law. Within the following year, the United States implemented a total of $5.68 trillion in fiscal stimulus, equivalent to approximately 25% of 2020 GDP.

If AI-driven unemployment emerges at the speed and scale described by Citrini, policy intervention is unlikely to be absent.

Other commentators have raised questions from a more fundamental level. Technological doomsaying generally stems from a lack of faith in human agency. Citrini’s reasoning treats the market as an unattended machine, allowing "cause and effect" to unfold on their own until collapse. But real economic systems do not operate this way. Law, institutions, politics, culture, and ideology profoundly shape how the real world absorbs technological shocks.

Consensus and Disagreement

We might try to highlight some areas of consensus and disagreement.

There is nearly universal agreement that AI is currently changing, and will continue to change, the demand structure for white-collar labor; the only disagreement lies in the speed and scale of this change. Moreover, the transitional pain is real and should not be obscured by long-term optimism. Additionally, the quality and speed of policy responses will largely determine the outcome.

The divergence lies in the underlying logic. Some believe that this technological shock may surpass historical precedents in speed and scope, limiting the applicability of historical analogies; others place greater trust in the adaptability of institutions and the repeatability of history.

Header

Citrini’s article contains numerous issues: its logical connections are overly tight, institutional responses are systematically underestimated, and the leap from micro-industry impacts to macro-systemic risk lacks sufficient intermediate reasoning. But its most fundamental problem may lie in an underestimation of human society: it assumes a static institutional environment in which technology overwhelms everything at an almost unstoppable pace. Throughout history, technological doomsday theories have been abundant; they are often logically impeccable, yet almost invariably ignore the variable of “humanity.” The complexity of human society, its friction, its redundancies, and its seemingly inefficient institutional arrangements collectively form a powerful, distributed resilience. We have ample time to avoid the doomsdays that are extrapolated—provided we are not paralyzed by the extrapolation itself.

What about those optimistic narratives? The Jevons Paradox is an observation about long-term trends. The Moravec Paradox tells us that manual labor is temporarily safe, but it doesn’t tell us what becomes of the displaced white-collar workers. Historical analogies are instructive, but history never repeats exactly—it only rhymes. Optimistic narratives take time to be tested, and we are just at the beginning of that test.

Apocalypse production, anxiety pays. Forge your own judgment, take risks, manage your positions—don’t get lost in those 「predictable」 articles.

Click to learn about the open positions at BlockBeats

Welcome to the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Twitter official account: https://twitter.com/BlockBeatsAsia