There are certain types of companies that appreciate in value when global conditions worsen: defense contractors, oil unions, and gold miners. These are classic examples whose business models inherently thrive on instability, turning risk into pricing advantage.

Circle does not belong to this category. Its token was designed to always be worth exactly one US dollar. Stability is the entire purpose of its product.

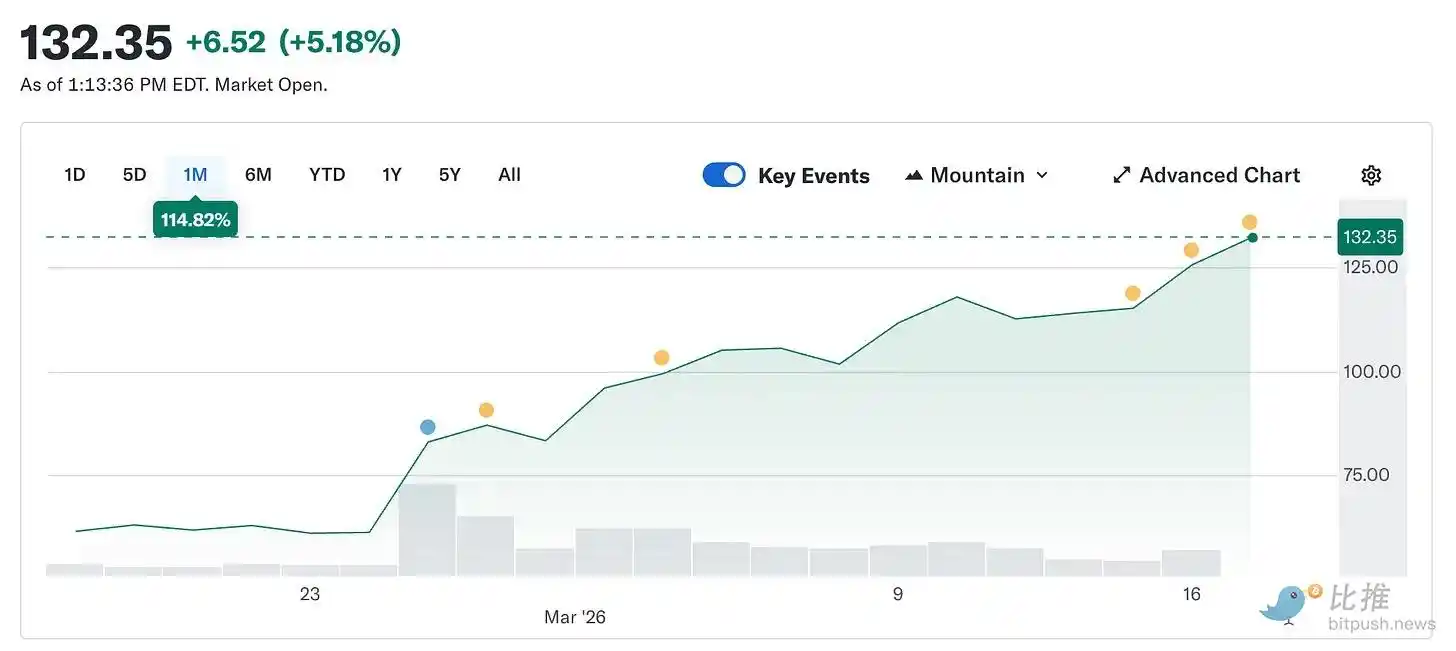

However, Circle’s stock price has surged from $49.90 on February 5 to approximately $123 today, more than doubling in just five weeks. Meanwhile, the broader cryptocurrency market remains 44% below its peak level from last October.

A company whose product aims for price stability has become the most sought-after trading asset on the market as the world becomes more volatile.

This article will explain the reasons behind this phenomenon and the difference between Circle’s true nature and its current market valuation.

What exactly is Circle? (Let’s return to the fundamentals)

Strip away the brand packaging, payment narratives, and infrastructure references, and what remains is: Circle holds U.S. Treasury bonds.

Each dollar of USDC in circulation is backed by one dollar held in short-term government bonds. The interest earned on these bonds belongs to Circle, accounting for approximately 90% of the company’s revenue in any given quarter. Once you understand this, its business model becomes straightforward: Circle is a money market fund that issues stablecoins.

This means Circle’s revenue, a key metric, is tied to the federal funds rate. When rates are high, U.S. Treasuries yield more, so Circle earns more on each circulating USDC. When rates fall, revenue contracts. Everything else is simply scale.

Here are the chain reactions that led to the stock price rebounding 150% from its February low:

According to @finance.yahoo, the conflict in Iran has driven a rise of approximately 35% since February 28. An increase of over $100 suggests excessive panic, and excessive panic means that Fed rate cuts could fuel recklessness. The decision to hold rates steady on March 18 was never truly in doubt; even before the war began, CME FedWatch showed a probability of over 90% for no rate change.

What has truly changed is the expected rate cut scenario this year. Before the conflict, the market priced in two 25-basis-point cuts by 2026. After the conflict, this expectation has been reduced to one cut, with the first now delayed until after September. The probability of no cuts at all in 2026 has roughly doubled. As interest rates remain elevated for a longer period, the revolving Treasury portfolio continues to generate income. More income means higher revenues, and higher revenues mean higher stock prices. With the outbreak of war, a stablecoin issuer has become a beneficiary—something that never appeared in anyone’s forecasting models.

Background context: The bearish logic that pushed Circle's stock price down to $49 in February was essentially a bet on interest rate cuts.

At the time, the market anticipated multiple rate cuts by the Federal Reserve in 2026, which would directly compress Circle’s interest income. Roughly speaking: at the current USDC supply level of $79 billion, a 25-basis-point rate cut would result in an annualized revenue loss of approximately $40 million to $60 million for Circle. Two rate cuts could erase nearly $100 million in top-line revenue by year-end. The war rendered this calculation obsolete overnight—not because of Circle itself, but because the broader macroeconomic context underlying the argument became irrecoverable.

How does a short squeeze begin?

While interest rate narratives support the stock price, the initial surge originated from position building.

Before Circle released its fourth-quarter earnings on February 25, approximately 17.8% of its outstanding shares were shorted. Hedge funds established significant short positions, arguing that interest rates would eventually decline, compressing domestic revenue, and that the company’s income is not dependent on the bottom line of interest rates. From a fundamental perspective, this argument is difficult to refute.

Additionally, Circ reported first-quarter earnings of $0.43, compared to the market consensus of $0.16. Revenue reached $7.7 billion, exceeding the expected $7.49 billion. On-chain USDC transaction volume surged to nearly $12 trillion quarter-over-quarter, up 247% year-over-year. Short covering ensued, sending the stock up 35% in a single day. According to 10X Research, hedge funds reportedly lost an estimated $5 billion on their short positions that day. Following this, the momentum from the earnings report carried forward.

Coinbase issue

Here is an updated portion of the narrative mentioned.

Circle's loss in 2025 was $70 million, not a profit. While the fourth quarter performed well, the full year did not. To understand why, you need to understand its relationship with Coinbase—the most important and most underappreciated fact about Circle's business.

When USDC was first launched in 2018, Circle and Coinbase formed a consortium to manage it. The consortium was dissolved in 2023, granting Circle full control over USDC issuance. However, Coinbase retained its revenue streams.

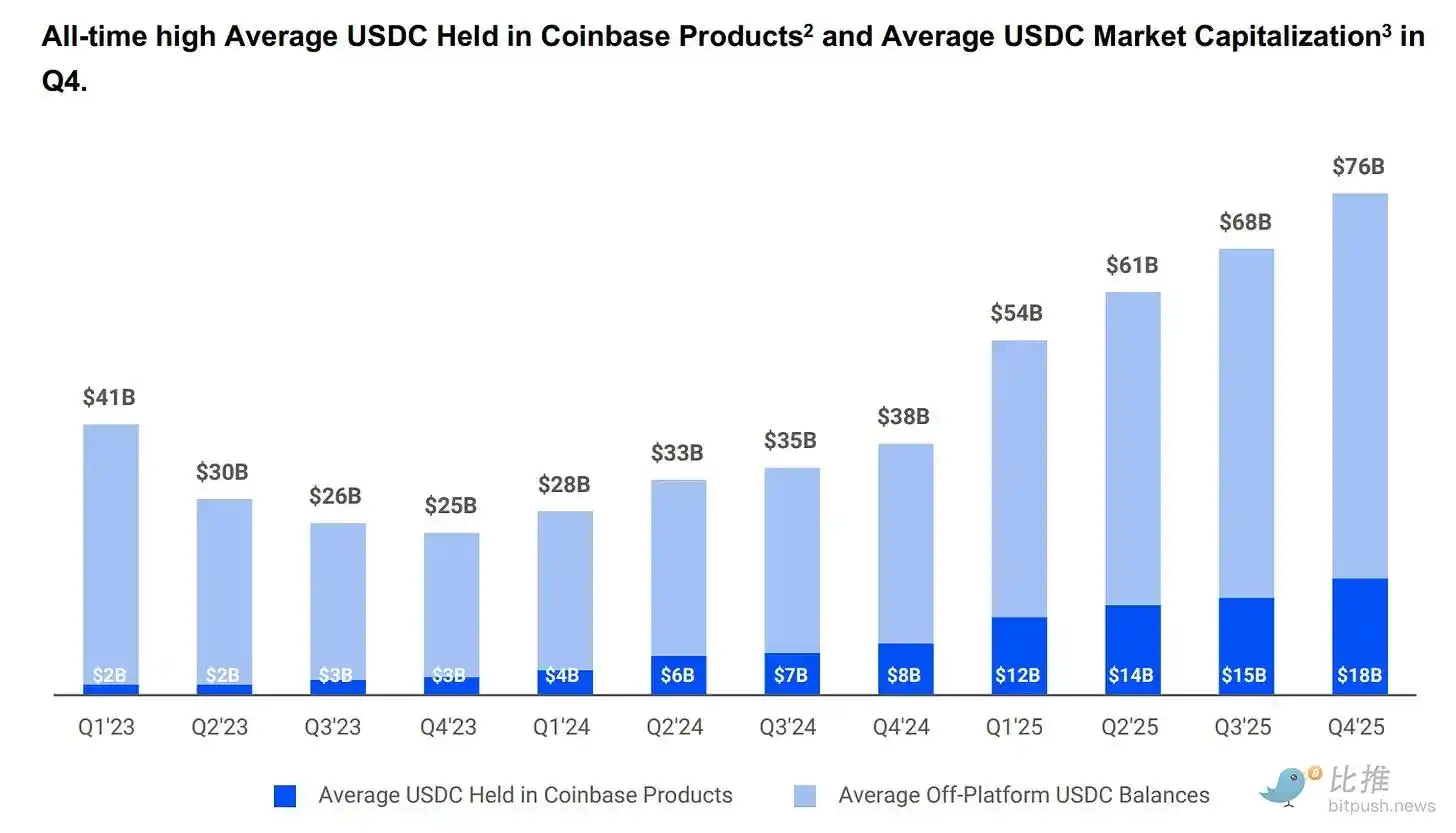

Coinbase took 100% of the reserve yield generated on USDC held on its platform, with all remaining yield split equally with Circle. In 2024, this arrangement directly transferred $9.08 billion of Circle’s total $10.1 billion allocation cost to Coinbase.

Roughly, for every dollar of Circle’s funds, 54 cents flowed to a company that neither issues tokens nor manages reserves. At the beginning of 2025, Coinbase held 22% of total USDC supply, up from 5% in 2022. The more USDC grows on the Coinbase platform, the greater the share of payments paid to Circle.

According to @q4cdn.com, the partnership automatically renews every three years, and Circle cannot terminate it unilaterally. Any outcomes from the next renegotiation will directly impact Circle’s profit margins. In the fourth quarter of 2025, allocated costs alone reached $461 million, a 52% increase compared to the same period.

The current $70 million net loss includes $424 million in share-based compensation attributable to the IPO, making the overall figures appear worse than the actual business condition. However, the core business still faces a structural cost issue that no interest rate environment can fully resolve.

The market prices the cycle as infrastructure, while the income statement reveals it as an interest rate instrument bearing high distribution costs. Both perspectives can coexist—they simply reflect different pricing logic, and now the market is paying for the "best version" of both.

Why is this not just a macro trade?

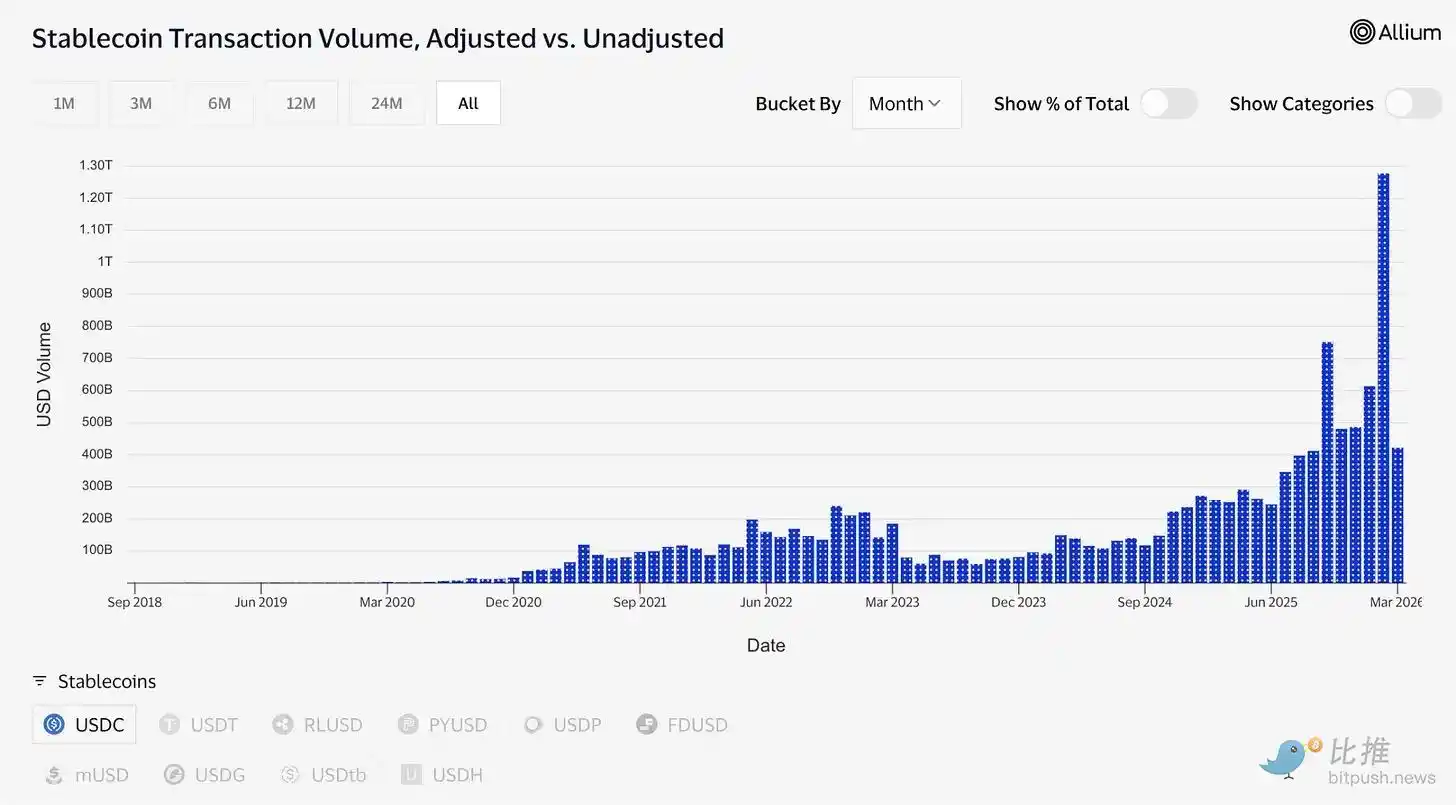

The supply of USDC recently reached a record high of $79 billion, while the broader crypto market plunged 44% from its October levels. This contrast is noteworthy: when markets decline, speculative assets typically fall too. The continued growth of USDC suggests that people are using it to move funds, rather than merely treating it as a speculative bet.

During the Iran conflict, demand for USDC surged across the Middle East precisely because traditional banking became unreliable. When normal channels were blocked, people turned to it for cross-border transfers. This is how payment infrastructure behaves under pressure: its usage increases, rather than decreases.

Transaction data confirms this. In February alone, USDC processed approximately $1.26 trillion in adjusted trading volume, compared to $514 billion for USDT. Tether’s (USDT) market capitalization remains at $184 billion, while USDC stands at $79 billion. In terms of total supply, the two are not comparable. However, USDC’s current liquidity has already surpassed that of USDT.

According to @visaonchainanalytics, "sleeping supply" and "active settlement" are distinct concepts. Previously, it showed where people held their dollars; tonight, it shows which dollars are used when value needs to be transferred.

Druckenmiller made some relevant points this week. In a Morgan Stanley interview recorded on January 30 and released on Thursday, he predicted that the global payment system will operate on stablecoins for 10 to 15 days per year, and called cryptocurrency "a solution in search of a problem."

The world’s most trusted macro investors have divided this space in two: stablecoins are the foundational base, and everything else is still seeking a reason to exist. This framework lends credibility to the bullish case.

Infrastructure deposit

Tokenized assets have grown from approximately $1.5 billion at the beginning of 2023 to about $26.5 billion today. Many of these products, including BUIDL—a tokenized U.S. Treasury fund managed by BlackRock with over $2 billion in assets—rely on USDC for subscriptions, redemptions, and settlement processing.

Prediction markets processed over $22 billion in trading volume in 2025, primarily settled in USDC (only Polymarket). Visa currently supports over 130 stablecoin-linked cards across 50 countries globally, with an annual settlement volume of approximately $4.6 billion.

Circle is building the infrastructure underlying all of this. The Circle Payments Network connects 55 financial institutions, processing $5.7 billion annually, enabling banks and payment providers to convert USDC across borders directly into local currencies.

Arc is Circle’s proprietary Layer-1 blockchain, designed to fully support institutional systems. This infrastructure operates independently of Ethereum or Solana. While Ethereum and Solana currently have negligible impact on revenue, they represent strategic, future-oriented initiatives in the event of declining interest rates.

The volume of AI systems is relatively small but structurally interesting. Data released in March by Circle’s Global Head of Spending shows that over the past nine months, AI agents have executed 140 million payments totaling $43 million. Of these, 98.6% were settled in USDC, with an average transaction value of $0.31. More than 400,000 AI agents with purchasing power are now active. While the dollar amount remains small, the trend is undeniable.

If AI agents need to make frequent, sub-penny payments to each other for compute power, data access, and API calls, they require tools that enable instant settlement with near-zero costs. Circle has just launched Nano Payments, specifically designed for this use case: enabling gas-free USDC transfers as low as $0.000001, off-chain processing, and batch settlement. The testnet already supports 12 chains, including Arbitrum, Base, and Ethereum.

This is the circle of investors willing to pay a $123 stock price: a company at the center of tokenized finance, AI agent businesses, cross-border payments, and prediction markets, backed by the regulatory strength of the GENIUS Act, with the CLARITY Act highly likely to pass before summer. Bernstein has set a target price of $190, Clear Street at $136, and Wall Street’s most bullish outlook for Harbor Global reaches as high as $280.

Persistent contradiction

Here, I want to honestly discuss one thing that bulls often overlook.

Circle's profitability depends on maintaining high interest rates. This is not a permanent condition. The Federal Reserve will eventually lower interest rates at some point. When that happens, the yield on the U.S. Treasury reserves backing USDC will shrink, and Circle's interest income will decline accordingly.

Circle recognizes this. It has been expanding businesses that do not rely on interest rate environments, such as transaction fees, enterprise services, payment networks, and Arc. However, these revenue streams are currently small. Withdrawal fees remain the primary source.

Therefore, you'll find both of these logics coexisting in the same stock price, but they are not the same bet.

The base case argues that USDC is becoming a true form of payment. The pipeline is regulated, transparent, and eager to deeply embed itself within traditional finance—a penetration that remains sticky regardless of interest rates. This argument is supported by data: digitized transaction volumes, integrations, Duquesne’s framework, and Macquarie’s characterization of stablecoins as the foundational layer of global financial infrastructure.

If this argument is correct, then Circle appears cheap in any interest rate environment, given that its potential market is the entire global payments system.

The interest rate trade thesis argues that Circle represents a leveraged bet on "higher and longer" rates, with the stock price already pricing in the expectation that the Fed will never cut rates again. If this is the primary driver of the price, then every basis point of future Fed rate cuts becomes a headwind, as the stock has already discounted fundamentals under normalized interest rates.

Both viewpoints are priced in. The war makes it difficult to determine which asset the market is actually buying.

This may be the most useful insight into understanding CRCL (Circle’s stock ticker). The key isn’t whether it will rise to $190, but rather that you’re buying into “infrastructure”—a treasury that learned to tell a great story and became a reseller. It’s a long-term position at first; then, the moment Powell changes his mind, it collapses.

Currently, it is valuable for both sides to remain alive in this struggle. The dollar is completing its most difficult and necessary task. And in the gap between these two scenarios lies the company’s true hidden insight—it figured out how to create internet-denominated currency in dollars, but now realizes it has survived the moment when the dollar no longer yields 5%.