The central bank and eight other ministries jointly issued regulations related to virtual currencies and tokenization of real-world assets (RWA):People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, State Financial Supervision Administration, China Securities Regulatory Commission, State Administration of Foreign Exchange, "Notice on Further Preventing and Dealing with Risks Related to Virtual Currencies, etc." (Yin Fa [2026] No. 42) (hereinafter referred to as "Document No. 42").

The industry had previously heard rumors about new regulations being introduced. After the official document was released, its content was rich in dimensions. After reading it, Salad felt that almost all of the previous compliance explorations in the RWA field had been covered in the documents from the 8 departments and the CSRC.

Let's quickly read through it:

I. The nature of Document No. 42

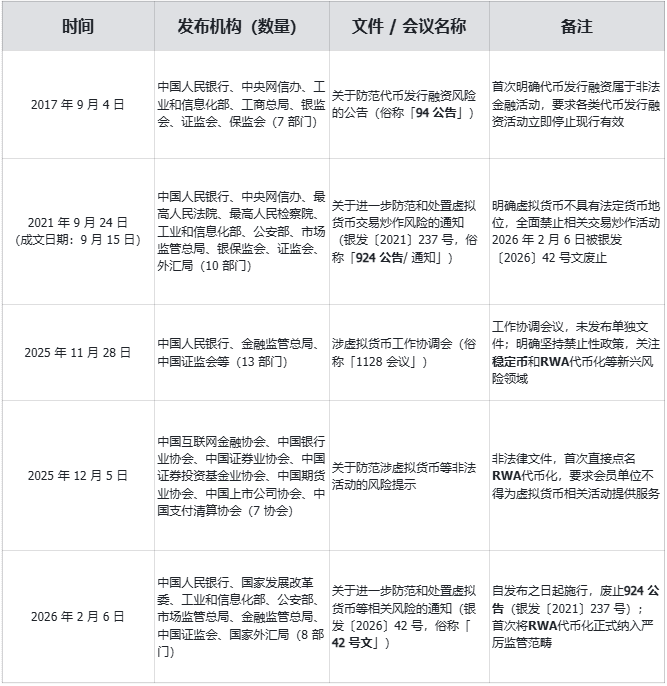

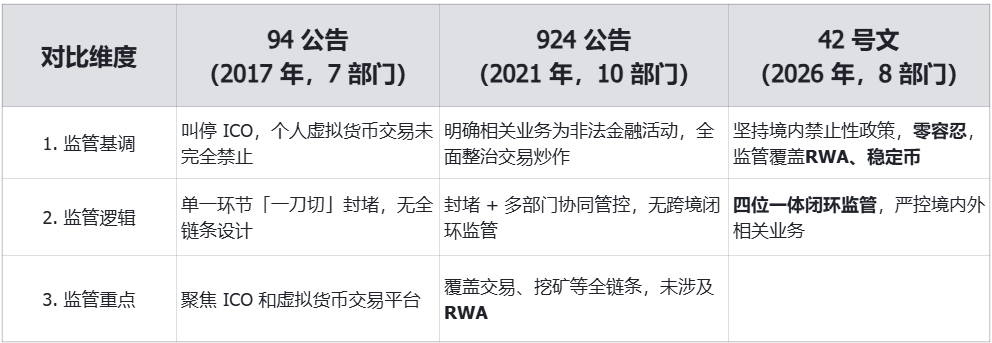

In 2017 and 2021, the regulatory authorities successively issued Announcement No. 94 and Announcement No. 924, after which there was a long period without the introduction of complete legal documents in this field; the working coordination meeting of thirteen ministries and the risk warning from seven associations at the end of 2025 do not constitute version upgrades of formal legal documents. The following is a comparison of the nature of the five core related documents:

Key conclusion: Document No. 42Is the most accurate and most complete legal regulatory document in the current virtual currency business field, the 924 announcement has been officially abolished with its implementation.

II. Core Differences Between Document No. 42 and Previous Regulatory Documents on Virtual Currencies

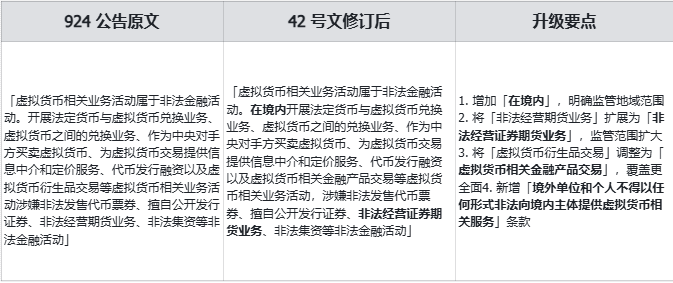

(1) Comprehensive expansion of the scope of regulated entities

- New Core Regulatory Target: Tokenization of Real-World Assets for the First Time (RWAStablecoins are included in the core scope of regulation, and the regulatory dimensions have expanded from mere virtual currency trading and speculation to "Virtual Currency + RWA + StablecoinTrinity full-chain supervision

- StablecoinRegulatory refinement: Clarify "tied to fiat currency"Stablecoin"Effectively performing part of the functions of legal tender in circulation," prohibiting "any domestic or foreign entity or individual from issuing RMB-linked instruments abroad without the approval of relevant authorities in accordance with laws and regulations."Stablecoin」

- RWAClear definition: Define it as "activities involving the use of cryptographic techniques and distributed ledger or similar technologies to convert ownership rights, revenue rights, and other entitlements or bond certificates with token (or similar) characteristics of assets into tokens (or other rights and bond certificates with token characteristics), and to issue and trade them."

(2) Issuing Department and Enhancement of Legal Effectiveness

Document No. 42Issued jointly by eight departments including the central bank and the National Development and Reform Commission, and reaching consensus with three departments including the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and approved by the State Council, the level of issuing authority and the legal effect are significantly higher than previous documents.

(3) Legal basis updated and improved

Add higher-level legal basis such as the "People's Republic of China Futures and Derivatives Law," the "People's Republic of China Securities Investment Fund Law," and the "Administrative Measures for the Renminbi of the People's Republic of China," providing more comprehensive legal support; at the same time, delete924 NoticeIn documents such as the "Regulations on the Administration of Futures Trading" and the "State Council's Decision on Clearing and Rectifying Various Trading Venues to Effectively Prevent Financial Risks," the application of laws is more precise.

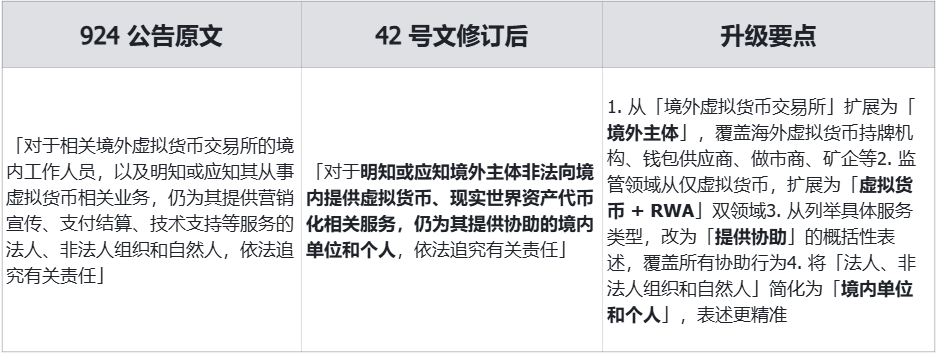

(4) Precise upgrading of the characterization statement of virtual currency

(5) A New Definition of RWA and Stablecoins

Document No. 42New specific clauses defining the nature of RWA: 「within the countryActivities involving the tokenization of real-world assets, as well as providing intermediary services, information technology services, etc., are suspected of engaging in illegal financial activities such as the illegal issuance of tokens, unauthorized public securities offerings, illegal securities and futures business operations, and illegal fundraising, and should therefore be prohibited; this does not apply to related business activities conducted through specific financial infrastructure with the approval of the relevant business authorities in accordance with laws and regulations.

At the same time, clearly.RWAOverseas Service Ban: 「Overseas entities and individuals shall not provide any real-world asset tokenization-related services to domestic entities in any form illegally..

Key Conclusion:It can be clearly understood in combination with the above provisions

1. RWAThe project is within the country, the service provider is within the country ——illegal

2. RWAThe project is within the country, the service provider is overseas ——illegal

3. Similar nature NFT projects, suspected of illegally issuing token tickets ——illegal

4. RWAThe project is overseas and is suspected of illegal fundraising within the country ——illegal

(6) Refinement of regulatory responsibilities, from multi-departmental coordination to a dual-track regulatory system

Circular 924 only establishes a multi-departmental coordination working mechanism: "The People's Bank of China, together with the Cyberspace Administration of China, the Supreme People's Court, the Supreme People's Procuratorate, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the CBIRC, the CSRC, the State Administration of Foreign Exchange and other departments, will establish a working coordination mechanism."

Document No. 42 has newly implemented a dual-lead system, clearly dividing regulatory responsibilities into two lines:

1. Cryptocurrency regulation: Establish and improve the working mechanism by the "People's Bank of China together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the Financial Regulatory Authority, the China Securities Regulatory Commission, the State Administration of Foreign Exchange and other departments"

2. RWA Regulation: "The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the State Financial Supervision Administration, the State Administration of Foreign Exchange, and other departments, will improve the working mechanism."

Key Conclusion:

1. The previous issue of poor coordination among multiple departments in implementation has no room for buck-passing or delayed handling, due to clear higher-level laws and accountability mechanisms.

2. Market entities intending to explore related businesses can clearly understand the government's list of powers and scope of responsibilities, reducing business misjudgment.

(7) Strengthening the responsibility of the department's territorial jurisdiction

On the basis of the 924 announcement, the Document No. 42 adds "specifically led by local financial regulatory authorities, with participation of branches and dispatched institutions of the State Council's financial regulatory authorities, as well as departments in charge of telecommunications, public security, and market supervision, and in coordination with internet information departments, people's courts, and people's procuratorates," clarifying the leading departments and cooperation mechanisms at the local implementation level, and further solidifying the local regulatory responsibilities.

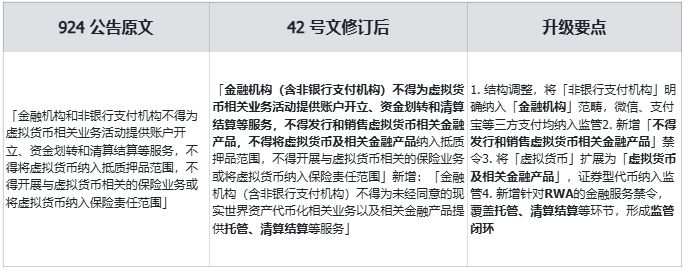

(8) Strengthening Financial Institution Management

(9) Expansion of Supervision over Intermediary and Technical Service Institutions

924 NoticeThe scope of regulation is limited to virtual currency-related services,Document No. 42Newly added: "Intermediary agencies and information technology service agencies shall not provide intermediary, technical, or other services for real-world asset tokenization-related businesses and related financial products that have not been approved.The regulatory scope was officially expanded to intermediaries and technology service providers in the RWA sector.

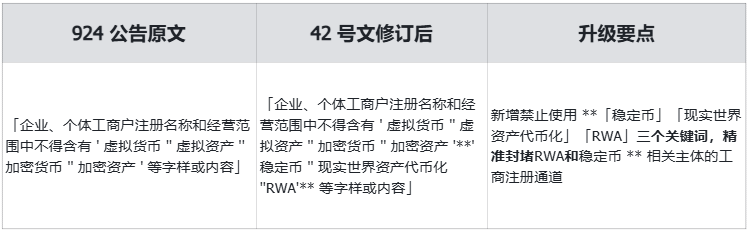

(10) Tightening of market entity registration and management

(11) Mining rectification policies intensified

924 NoticeMentioning only the "full-chain tracking and full-time information backup for the 'mining', trading, and exchange of virtual currencies," Document No. 42 lists Article 9 separately with detailed provisions, clarifying that "Mining machine production enterprises are strictly prohibited from providing various services such as the sale of "mining machines" within the country., cutting off the mining industry chain from the source; compared to the monitoring requirements of the 924 announcement, the new regulations are stricter and more enforceable, and clearly define the handling mechanism of relevant departments after receiving leads.

(12) Innovation in Overseas Issuance Regulation

Document No. 42In light of new developments in the overseas cryptocurrency sector, new additions for cross-border businessDual ban on overseas issuance:

1. Domestic entities and their controlled overseas entities shall not issue virtual currencies overseas without the approval of the relevant authorities in accordance with laws and regulations.

2. Regarding RWA: "Domestic entities directly or indirectly conducting real-world asset tokenization business in the form of foreign debt overseas, or conducting asset-backed securitization-like, equity-like real-world asset tokenization business overseas based on ownership or revenue rights of domestic assets, should be strictly regulated by relevant departments such as the National Development and Reform Commission, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange according to their respective responsibilities, following the principle of 'same business, same risk, same rules' in accordance with laws and regulations."

Key conclusion: The above provisions can be clearly combined

1. without underlying assetsNon-RWAType of Offshore Coin Issuance Behavior ——illegal

2. Security tokenization activities with characteristics similar to foreign debt, equity, ABS ——Legally under strict regulation

3. Legal RWAThe regulatory principle — referring to securities business, "same business, same risk, same rules"

(13) Strengthening of Overseas Business Supervision for Domestic Financial Institutions, Responsibilities Reinforced

Circular No. 42 added: "Overseas subsidiaries and branches of domestic financial institutions must act in accordance with the law and with prudence when providing real-world asset tokenization-related services abroad. They should be equipped with professional personnel and systems, effectively prevent business risks, strictly implement requirements for customer access, suitability management, anti-money laundering, and be incorporated into the compliance and risk control management system of domestic financial institutions," achieving penetration regulation of cross-border business.

Key Conclusion:It can be clearly understood in combination with the above provisions

1. Overseas branches (branches, offices, etc.) of domestic financial institutions may engage in tokenization-related businesses.

2. Overseas branches conducting tokenization business must comply with both local laws and Chinese regulatory requirements, and fulfillHigh prudence, anti-money laundering and other statutory obligations

3. Business information and data from overseas branches must be comprehensive.Incorporate into the compliance and risk control system of domestic financial institutions

(14) Cross-border Service Supervision Coverage of Intermediary Institutions

Document No. 42New addition: "Intermediary institutions and information technology service providers that offer services for domestic entities to conduct real-world asset tokenization business in the form of foreign debt, either directly or indirectly overseas, or to carry out real-world asset tokenization-related business overseas based on domestic rights and interests, shall strictly abide by legal and regulatory provisions and comply with relevant standard requirements.Establish and improve relevant compliance internal control systems, and strengthen business and risk management,Report on the business operations tosubmit for approval or file a report with the relevant administrative departmentsformally include cross-border service intermediaries into the regulatory scope.

Key Conclusion:It can be clearly understood in combination with the above provisions

1. Law firms, technology companies and other intermediary institutions can inwithin the regulated controlled areaProvide tokenization-related services

2. Intermediary institutions conducting tokenization business must possessA sound risk control and internal control system,Business development status needs to be reported tosubmit for approval or record-filing with the regulatory authorities

(15) Expansion of the scope of legal liability subjects

(16) Optimization of Civil Liability Clauses

924 NoticeRegulation: "Any legal person, non-legal person organization, and natural person investing in virtual currency and related derivatives that violate public order and good customs, the relevant civil legal acts are invalid"; Document No. 42 revised to: "Any entity or individual investing in virtual currencies, real-world asset tokens, and related financial products that violate public order and good customs, the relevant civil legal acts are invalid.", expanding the investment targets from "virtual currencies and related derivatives" to "Virtual currencies, real-world asset tokens, and related financial products, the regulatory coverage is more comprehensive.

Key Conclusion:All kinds of fundraising activities from domestic investors under the name of RWA, the related investment rights and interests are not protected by law.

III. Current Status and Future Trends of RWA Business

The RWA concept and projects first emerged overseas, similar to the early STO concept but with a broader imagination space, and are referred to within the industry as "Everything can be RWA." Discussions about RWA in China have gradually heated up since 2024, reaching a peak in volume from June to August 2025. This trend is closely related to the entry of major domestic institutions such as Ant Group, JD.com, and Guojun, as well as the upgraded crypto regulations, stablecoin regulations, and ongoing issuance of crypto regulatory licenses in regions like the United States and Hong Kong.

Mainstream RWA projects and underlying assets in the current market

1. New energy, computing power and other emerging operating cash flow assets

2. Traditional operating assets such as commercial leases

3. Cultural IP Value-added Consumer Goods Project

4. Real estate, antiques, artworks, mineral resources, and other physical assets

5. Other types of assets

Mainstream RWA financing solutions for industry professionals

1. In countries and regions with clear regulatory provisions, conducting activities related to the aforementioned asset categories 1 and 2Security Token Offering—— Fully legal, but with the highest regulatory requirements and highest operational costs

2. In domestic cultural exchanges, data exchanges, and industrial exchanges and other platforms, issue the aforementioned three types of assets and NFTs - with lower regulatory requirements,Not explicitly identified as illegal

3. In overseas centralized and decentralized exchanges, issuing token projects for the aforementioned asset categories 4 and 5 that lack cash flow support —— seemingly having underlying assets, but in reality areHeadhunting, hype, fundraising, stock manipulationhigh-risk behaviors have not yet been precisely defined in legal provisions.

Due to significant differences in the characteristics of underlying assets, fundraising targets, operational standardization, and project parties' values, there are numerous borderline operational methods in the RWA field, and practitioners also deliberately blur regulatory boundaries. If not strictly regulated, it is very easy to encounterthe situation where bad money drives out good,High-risk projects and mass fraud incidents will occur frequently. Currently, the participants in this field are mixed, including domestic and foreign securities institutions, issuing service providers, overseas exchanges, digital compradors, data service providers, and domestic property rights exchanges are all involved.

And withDocument No. 42The introduction of it changed everything. Through a meticulous analysis, one can discover the regulatory body's thinking and philosophy:

1. The legislators have comprehensively considered the laws and regulations of regions such as the United States, Europe, and Hong Kong, and have referenced them in terms of regulation and wording, achieving a moderate alignment with international regulation.

2. New regulations fully coverStablecoins, RWAsuch emerging fields, while filling the gaps in past areas like mining machine sales and mining enforcement.regulatory gray area

3. In areas with insufficient technological maturity and where the authority to establish rules has not been grasped, the regulatory attitude isClearly block,Prevent financial risks

4. For the necessary alignment of overseas financing regulations, especially in countries and regions with clear regulatory rules, tokenization projects implemented to strict standards remain within the domestic jurisdiction.Financial institutions, intermediary service organizationsReservedParticipation Window

Comparison Table of Core Regulatory Logic of Circular 94, Circular 924, and Document No. 42

Four, CSRC: What administrative permits do RWA projects correspond to?

The CSRC, as the regulatory authority in charge of RWA business, issued simultaneously at the first moment.Circular No. 1 of 2026 "Regulatory Guidance on Offshore Issuance of Asset-Backed Security Tokens for Onshore Assets."

This guideline clearly states:

1. The issuance of asset-backed security tokens for onshore assets offshore shall be strictly complied with.Cross-border investment, foreign exchange management, network and data securityand fulfill the procedures of approval, filing, or security review required by the aforementioned relevant regulatory authorities, in accordance with laws, administrative regulations, and relevant policy provisions.

2. If the underlying asset and the domestic entity that actually controls the asset fall under any of the following circumstances, the relevant business shall not be conducted:

(1) Where laws, administrative regulations, or other relevant national provisions explicitly prohibit financing through the capital market;

(2) If the relevant competent authorities of the State Council determine in accordance with the law that the issuance of asset-backed securities tokens overseas may endanger national security;

(3) If the domestic entity or its controlling shareholder or actual controller has committed criminal offenses such as embezzlement, bribery, property infringement, misappropriation of property, or disruption of the socialist market economic order within the past 3 years;

(4) The domestic entity is currently under a formal investigation for suspected criminal activities or serious violations of laws and regulations, and no clear conclusion has been reached yet;

(5) There are significant ownership disputes regarding the underlying assets, or the assets are legally prohibited from being transferred;

(6) The underlying assets exist in the prohibited circumstances stipulated in the negative list of underlying assets for onshore asset securitization business.

3. Before commencing relevant business, RWA project parties need to submit to the CSRC a report, complete set of overseas issuance materials, and other related materials, fully explaining the information of the domestic filing entity, the underlying asset information, the token issuance plan, etc. After the CSRC filing is completed, the filing information will be publicly displayed on the website.[Key point: For projects that tokenize domestic assets or revenue rights for financing overseas, obtaining this filing from the China Securities Regulatory Commission can be understood as a legal project]

In addition, for completed RWA projects, the CSRC will also implement mid-process management during their operation, continuous supervision, and maintain information exchange with overseas institutions.

Salad feels that with the release of the above documents, this new thing called RWA has finally gone through the weeding out of the false, and can be said to have survived, returning to the issuance and regulatory logic of security tokens. Although more detailed rules have not yet been issued, the regulatory gray areas for RWA and stablecoins over the past three years have been fully clarified. Through legislative protection, regulation now has a grip, and industry practitioners have guidance.

Special Statement: This article is an original work of the encrypted salad team and only represents the personal views of the author, and does not constitute legal advice or legal opinion on specific matters.