A powerful force is converging, set to reshape the financial services industry by 2026. Emerging banks are going public and applying for full banking licenses. Crypto-native companies are either partnering with or competing against the world’s largest banks. AI agents are autonomously transferring funds. These developments collectively signal a shift in how financial services are constructed and the ownership of customer relationships.

Prediction 1: Emerging banks entering new markets will steal consumer deposits from traditional banks

Emerging banks are no longer startups chasing traditional banks. A new breed of digital-first institutions is expanding globally, going public, and applying for full banking licenses, directly competing with traditional banks for primary consumer banking relationships.

The booming IPO market reflects growing confidence in the commercial maturity of these new banks. Chime completed an $864 million public offering in June 2025, setting a record for the largest IPO by a new bank in U.S. history. PicPay followed by listing on Nasdaq in January. The largest new bank by market capitalization, Nubank, received conditional approval for a U.S. banking license in January. Rather than partnering with a sponsoring bank, Nubank chose to apply for a full license independently, relocating its co-founder to the U.S. full-time to lead its new subsidiary.

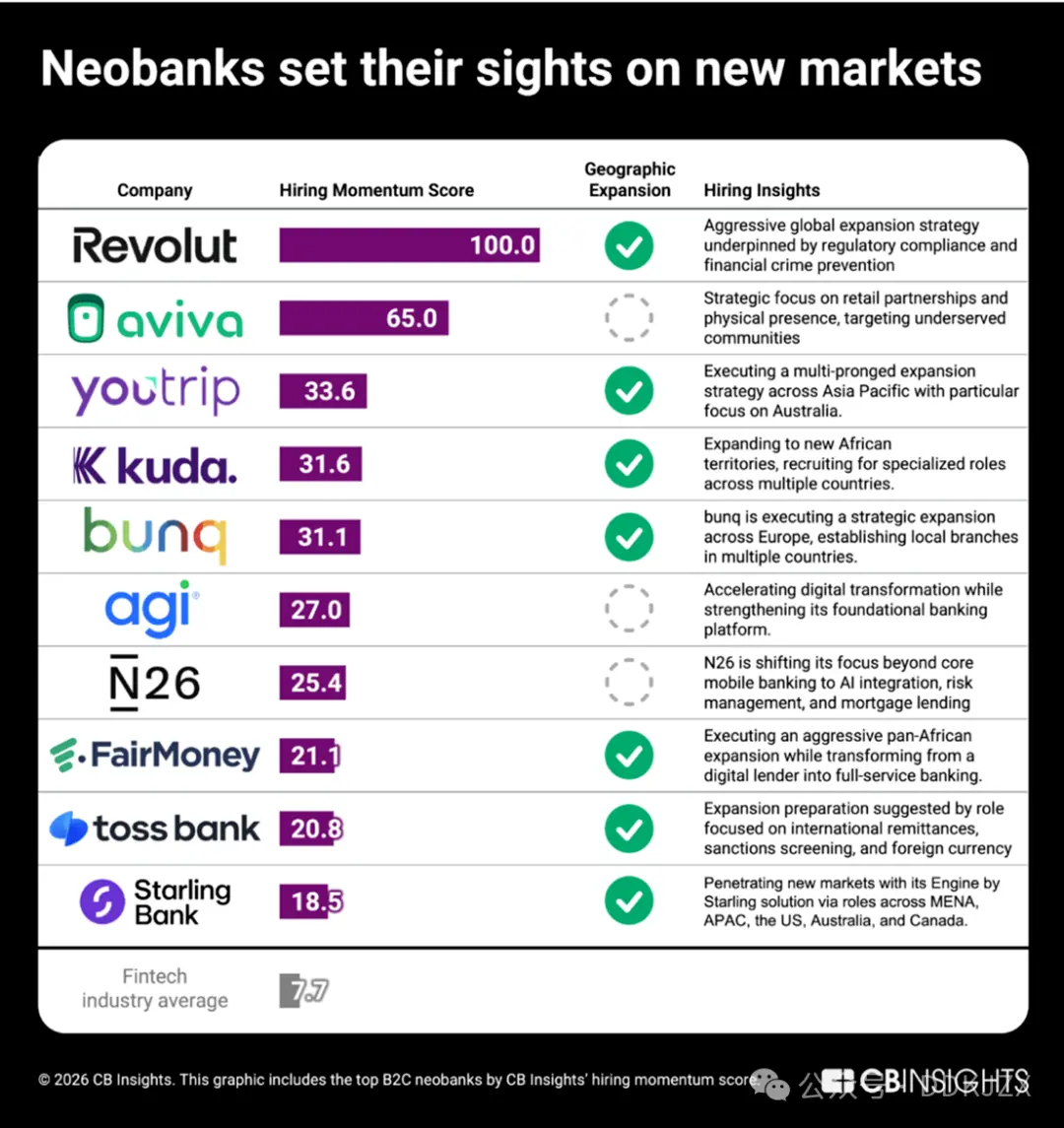

In the private sector, CB Insights’ hiring momentum scores reveal which B2C emerging banks are expanding most aggressively.

Revolut leads the way with a perfect hiring momentum score of 100. In November, the company raised $2 billion, reaching a valuation of $75 billion, becoming the highest-valued private new bank in history. A significant portion of this funding is earmarked for expansion into the U.S. market. Its recruitment strategy reflects a systematic market entry plan, such as hiring senior regulatory and compliance leaders in over 20 countries simultaneously. Other companies include:

-

YouTrip (33.6), which is expanding heavily in the Asia-Pacific region, particularly focusing on the Australian market.

-

Kuda (31.6), targeting the Nigerian market, is hiring across multiple African regions.

-

Toss Bank (20.8) is recruiting for positions related to international remittances and foreign exchange, indicating cross-border expansion from South Korea.

Even new banks not currently expanding geographically are transforming their models: FairMoney (21.1) is transitioning from a digital lending institution to a full-service pan-African bank, while N26 (25.4) is integrating AI, mortgages, and risk management to deepen its competitive position in existing European markets.

As this generation of new banks enters new markets with increasingly comprehensive services, consumer deposits at banks of all sizes face pressure from a brand-new class of competitors.

Prediction 2: The buy-now-pay-later (BNPL) bank battle

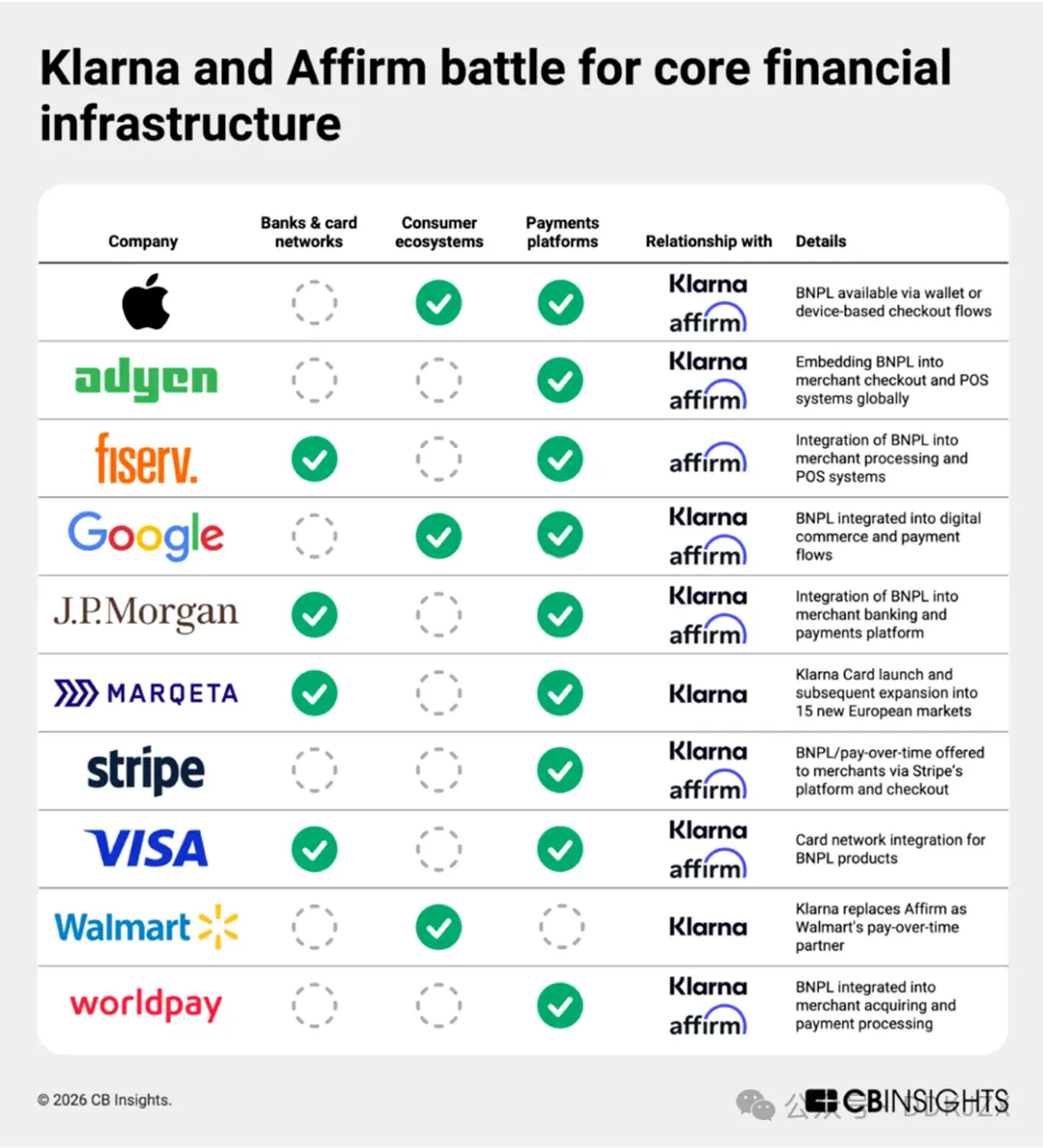

“Buy-now-pay-later” (BNPL) is no longer just a checkout feature. Klarna (expected to be the largest fintech IPO of 2025) and Affirm (with higher market capitalization and aggressive European expansion) are both constructing full-scale consumer banking services. CB Insights’ business relationship data reveals that they are achieving this through overlapping infrastructure. These two companies rank among the most active payment companies in terms of partnership numbers, sharing 27 common partners—including Apple, Adyen, Google, and JPMorgan Chase—that integrate BNPL into device-based checkout processes, digital commerce, merchant banking, and payment processing.

Recent initiatives have further deepened this infrastructure layout. Affirm’s partnership with Fiserv and Klarna’s credit card expansion via Marqeta embed BNPL services into debit cards, banking services, and everyday payments, extending far beyond installment loans at checkout. Klarna holds EU and UK licenses and announced in June a debit card pilot in the U.S. through a collaboration with Visa. Meanwhile, Affirm plans to expand its services beyond existing savings accounts (held by Cross River Bank) and submitted an application to the Federal Deposit Insurance Corporation (FDIC) in January.

Our hiring data shows Affirm is recruiting analytical leaders to develop its partnership bank debit card program. Klarna, on the other hand, is strengthening its fraud detection and risk management capabilities through dedicated roles, with a focus on regulatory compliance in the UK market.

As smart AI reshapes how consumers shop, the purely buy-now-pay-later model may lose momentum; the next stage for both companies is full-scale consumer banking services.

Prediction 3: Robinhood will become a financial super app

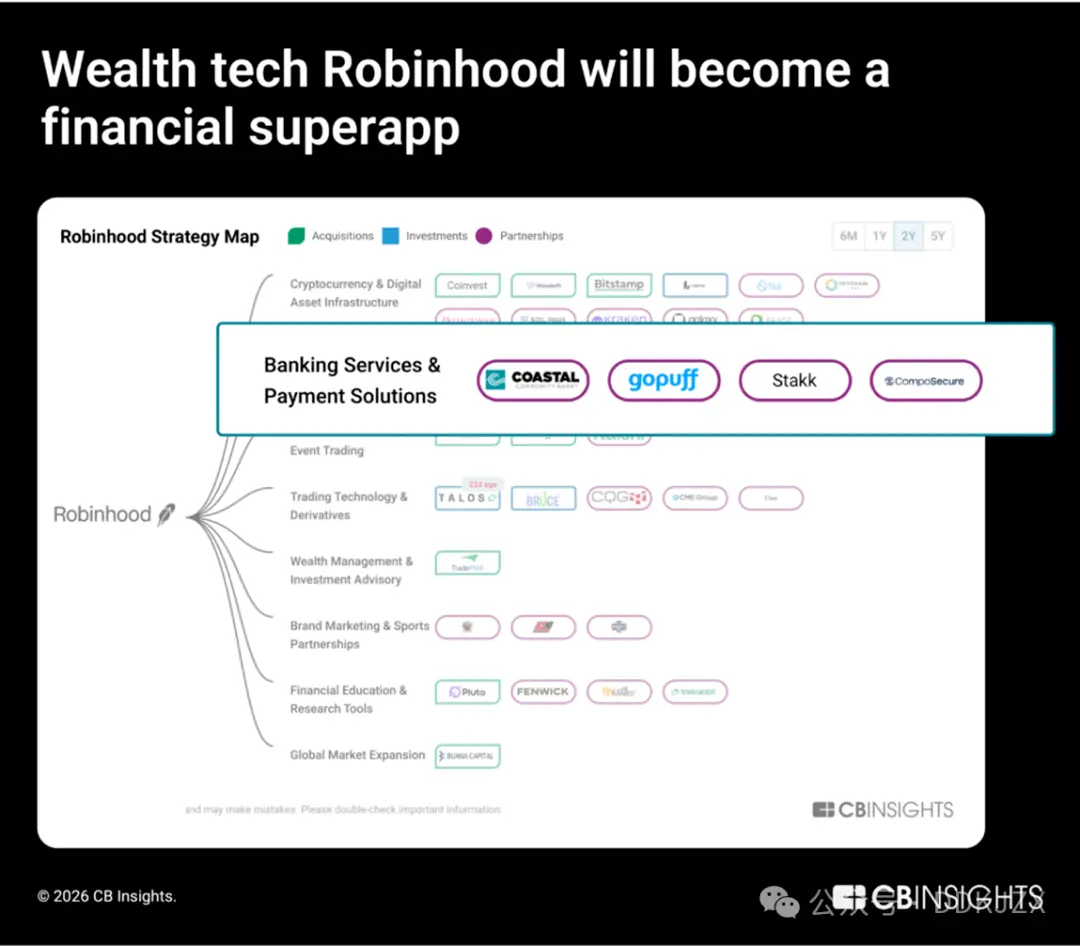

In 2025, equity funding in the wealth-tech sector grew by 90% year-over-year, marking the largest increase across all fintech sub-sectors. The highest-valued company in this space, Robinhood, is actively expanding into banking, credit, and cryptocurrency infrastructure.

In investment, Robinhood is advancing toward vertical integration. It acquired Bitstamp (an institutional-grade crypto trading platform) and LedgerX (a cryptocurrency futures platform), extending its business beyond retail brokerage. Additionally, it partnered with Offchain Labs to build an L2 chain, “Robinhood Chain,” exclusively for EU users, signaling ambitions not just in asset distribution but in owning on-chain market infrastructure.

In banking, Robinhood continues expanding its capabilities to prepare for the launch of comprehensive banking services. In November 2025, Robinhood integrated cash delivery services through partnerships with GoPuff and Coastal Community Bank; in September 2025, Robinhood acquired Stakk, further strengthening its core banking capabilities. Our hiring data corroborates this transformation, showing a growing number of positions directly related to credit cards, banking products, and credit limit enhancements.

-

Full-stack engineer and software backend engineer, credit card and banking services

-

Banking product design manager and senior product engineer

-

Credit business analyst, banking fraud

Robinhood has not merely relied on partnerships to layer functionalities but has built a vertically integrated financial system and talent pool covering areas such as trading, cryptocurrency infrastructure, deposits, and credit. Amid the booming fintech landscape, Robinhood is reshaping consumer banking under the guise of a brokerage firm.

Prediction 4: Large cryptocurrency companies will challenge major banks

Cryptocurrency companies are no longer offering alternatives to traditional banking services but are constructing the next phase of traditional banking services.

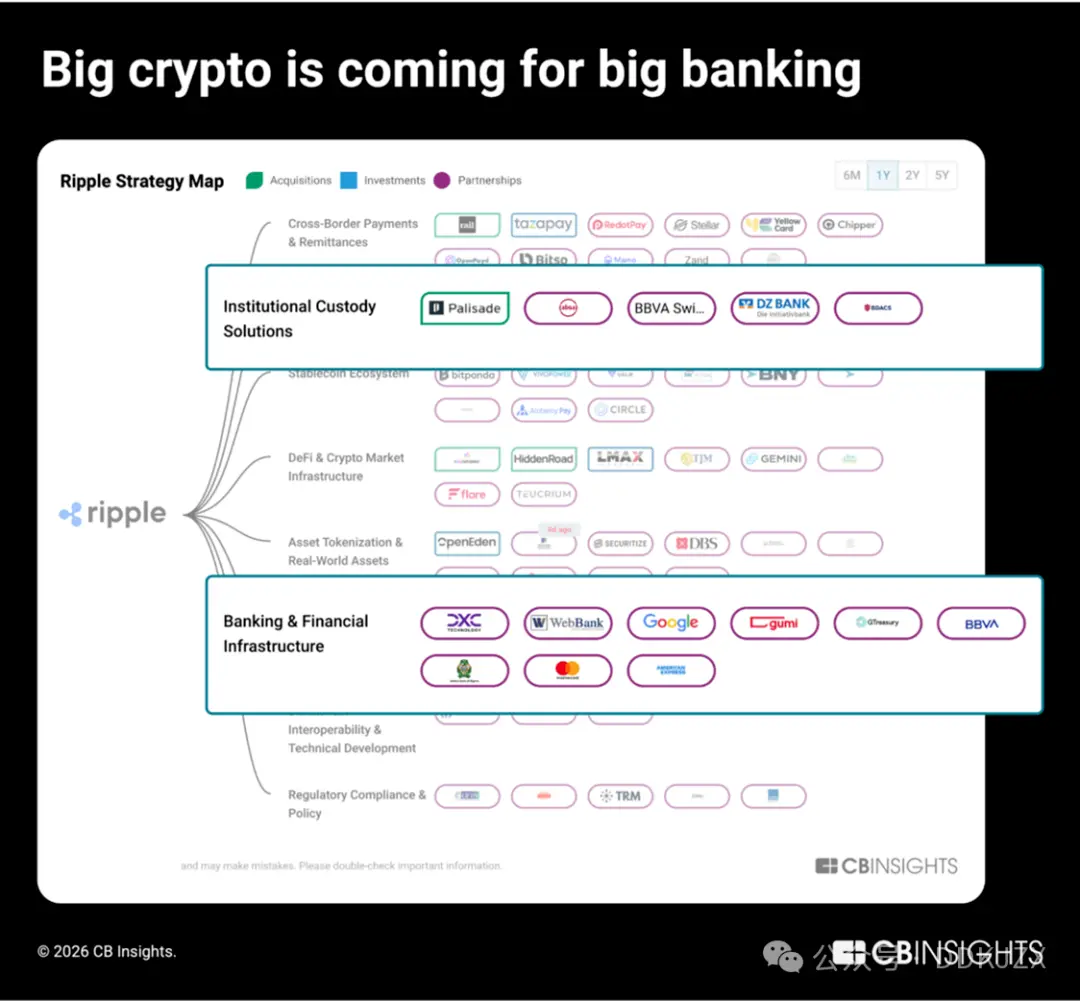

By 2025, the companies most actively expanding crypto-native business will be Ripple, Coinbase, and Circle, each establishing over 50 partnerships. According to our Business Relationship Insights report, these three leading enterprises are targeting the traditional banking system:

-

Ripple is building institutional-grade custody infrastructure for tokenizing real-world assets and digital fund management, realized through white-label solutions supported by prominent financial institutions such as BBVA and Absa Group.

-

Coinbase is expanding from retail brokerage to providing institutional brokerage, custody, and payment infrastructure services for financial institutions like JPMorgan Chase and Standard Chartered Bank.

-

Circle is directly embedding USDC into core banking systems and payment processors (e.g., FIS, Fiserv, and Finastra) to enable seamless stablecoin adoption by traditional financial institutions.

Ripple is actively advancing into institutional banking, having formed partnerships with nine of the top 100 traditional banks by asset size since 2023, including DBS Bank and BNY Mellon. Its strategic planning over the past year reveals four acquisitions in the fintech for treasury management, prime brokerage, and B2B cross-border transaction processing fields to build out its financial tech stack:

-

Palisade (acquired in November 2025) is a wallet-as-a-service custody platform targeting fintech firms and crypto-native companies for high-frequency trading, deposits, withdrawals, and wallet configurations.

-

GTreasury (acquired in October 2025 with a valuation of $1 billion) is a treasury management software provider used by large enterprises to manage cash, foreign exchange risk exposure, and payment operations.

-

Rail.io (acquired in August 2025 with a valuation of $200 million) is a B2B stablecoin payments startup providing on-/off-ramps and cross-border transaction infrastructure for enterprises.

-

Ripple Prime (acquired in April 2025 with a valuation of $1.25 billion, formerly Hidden Road) is a multi-asset institutional brokerage, clearing approximately $3 trillion annually for hedge funds and financial institutions.

In December of last year, Ripple and Circle, alongside BitGo, Fidelity Digital Assets, and Paxos, received conditional approval for a U.S. national trust bank charter. Next step: These crypto-native companies are preparing to go beyond partnerships, racing to establish full-stack banking relationships.

Prediction 5: To address the rise of cryptocurrency companies, banks will tokenize existing assets to maintain control over deposits

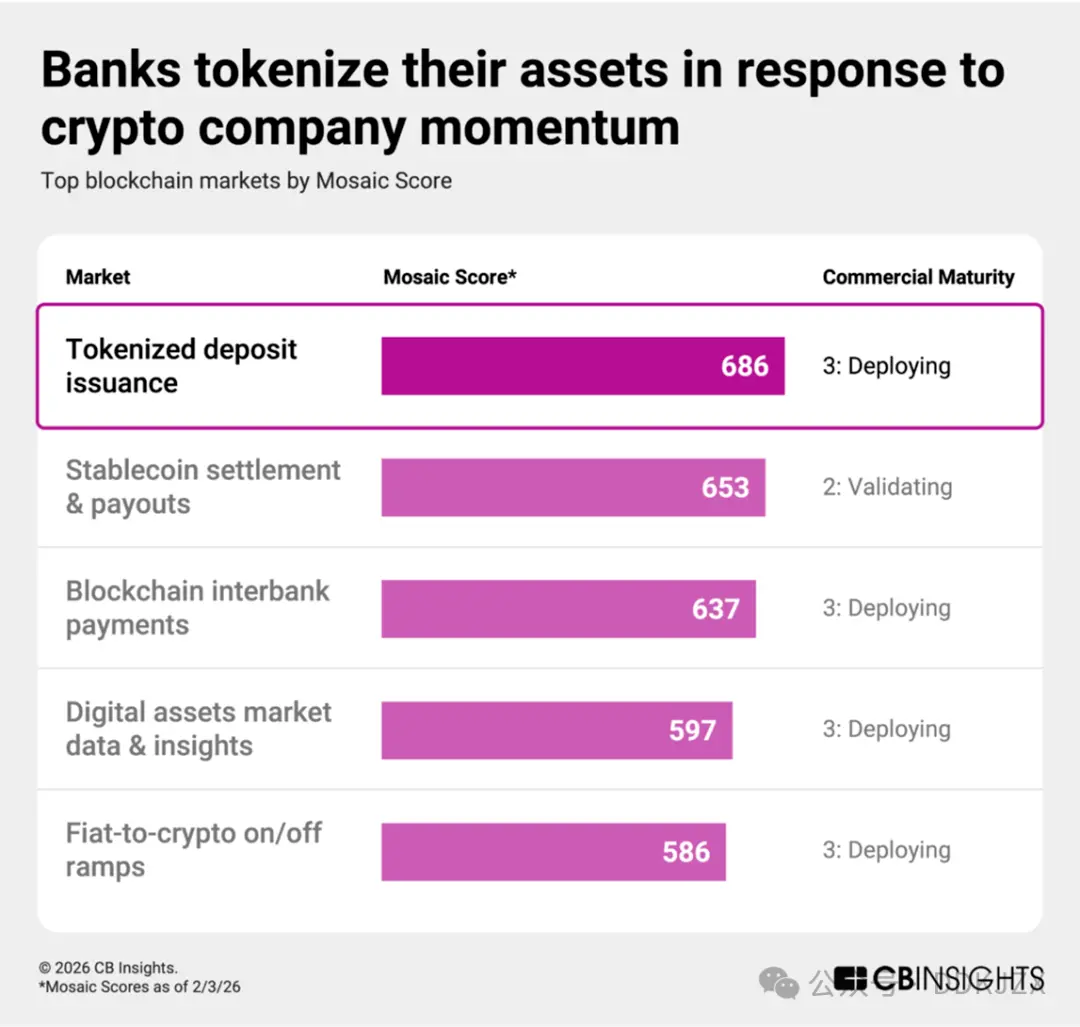

Banks are actively responding to the rise of cryptocurrency companies by converting deposits into blockchain-based tokens. Tokenized deposits are digital representations of ordinary currency held by regulated banks and remain liabilities on the bank's balance sheet, offering customers the same protections as traditional deposits. On blockchain platforms, tokenized deposits can support faster settlements and programmable transfers, while the issuing bank retains regulatory authority and core customer relationships.

Based on ratings, tokenized deposit issuance represents the blockchain market with the highest momentum currently, with an average commercial maturity score of 3 (in deployment) or lower, even surpassing the Mosaic score for stablecoin settlements and payments. According to our ESP (Execution, Strength, and Positioning) matrix, the major players include:

-

Stablecore (Mosaic score in the top 2%, scoring 747) enables banks and credit unions to offer digital asset products, facilitate transactions, and manage cryptocurrency collateral for loans.

-

Fireblocks (Mosaic score as high as 867, ranked in the top 1%) provides flexible institutional-grade technology for tokenizing fiat, money market funds, digital currencies, and real-world assets. In February 2026, Fireblocks launched Canton Network, a Layer 1 blockchain designed specifically for institutional finance.

Strategic partnerships are driving this movement:

-

JPMorgan Chase launched tokenized deposits and tokenized money market funds and began exploring the interoperability of tokenized TradFi products with DBS Bank in November.

-

Citi expanded its existing Citi Token Services solution with interbank payment capabilities in September.

-

Vantage Bank partnered with Custodia Bank in October for tokenized deposit operations, while Standard Chartered teamed up with Ant Group in December for similar initiatives.

With the growing adoption of stablecoins, banks will increasingly tokenize their balance sheets, modernizing settlement channels while maintaining deposit relationships, turning defensive measures into competitive strategies.

Prediction 6: Stablecoins will become the rails for agent-based payments

AI agents require programmable and always-available funds, a need perfectly met by stablecoins. This convergence is natural: AI agents require verifiable identities, programmable funds, and autonomous execution—all of which are natively provided by blockchain-based currencies.

The data shows that progress is already underway. According to our "Tech Trends Report," by 2025, the financial services industry will lead all sectors in AI agent collaboration, while payment processors building smart commerce rails are accelerating cryptocurrency integration: for example, Mastercard's cryptocurrency partnerships are set to increase from 6 in 2024 to over 25 in 2025.

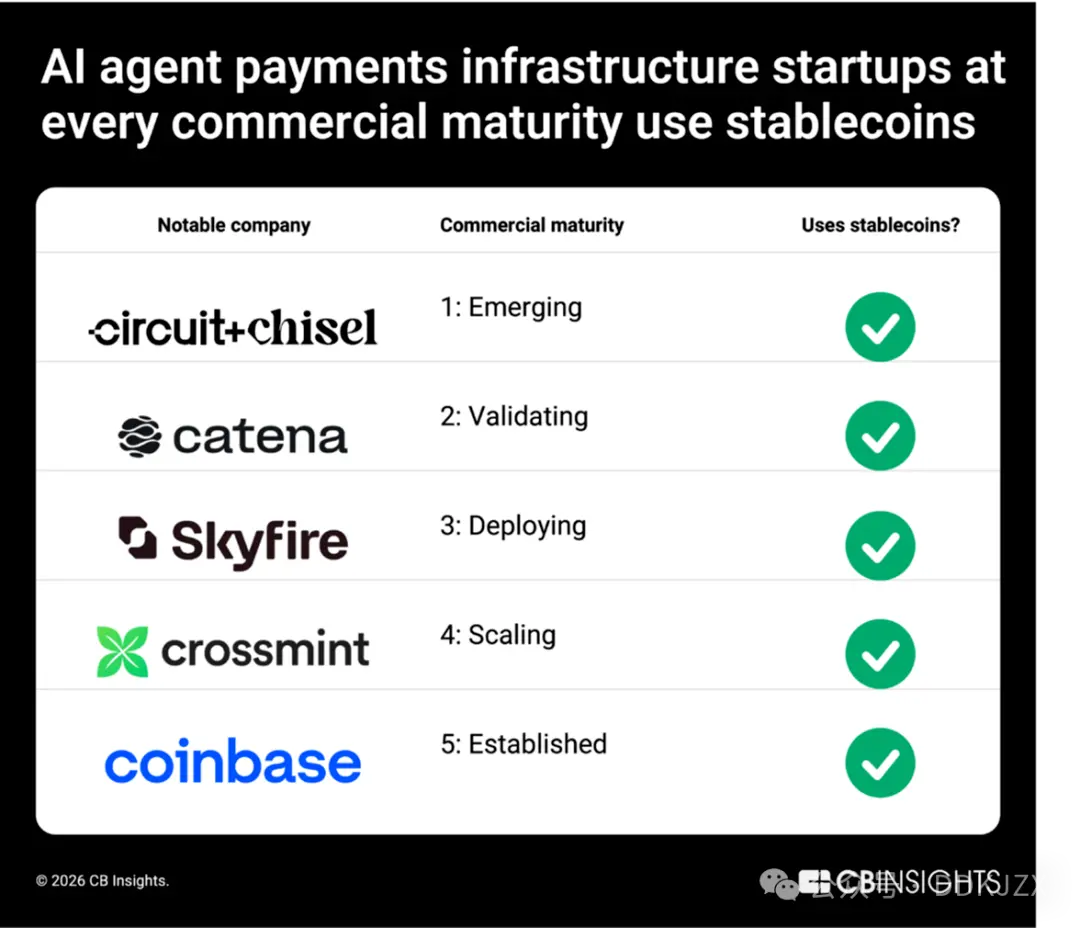

From startups to industry giants, stablecoins form the common foundation for AI agent payment infrastructure. In the AI agent payment infrastructure market we analyzed, companies at various business maturity stages rely on stablecoins, including Circuit & Chisel (CM 1), Catena Labs (CM 2), Skyfire (CM 3), Crossmint (CM 4), and Coinbase (CM 5). Investors like Coinbase Ventures and Stripe further reinforce this overlap.

As AI agents manage subscriptions, checkout processes, and post-purchase services on behalf of consumers, stablecoins will naturally transition from crypto-native tools to the settlement layer for agent-driven commerce. We predict that by 2026 and beyond, stablecoins will provide instant, programmable payment methods for online marketplaces, cross-border retail, and embedded checkout experiences.

Forecast 7: On-chain AI agent platforms are laying the foundation for an autonomous agent economy.

Stablecoins are becoming key payment channels for smart commerce. However, a parallel infrastructure layer is emerging: platforms where AI agents operate entirely on-chain.

Blockchain-based AI agent platforms provide the tools needed to create, deploy, and manage autonomous agents running natively on-chain. These agents can execute decentralized finance (DeFi) transactions, participate in governance, interact with decentralized applications, and coordinate with other agents without human intervention.

Beyond execution, these platforms enable tokenized co-ownership and monetization of agents, pointing toward an agent economy where autonomous software participants can independently earn, spend, and allocate capital.

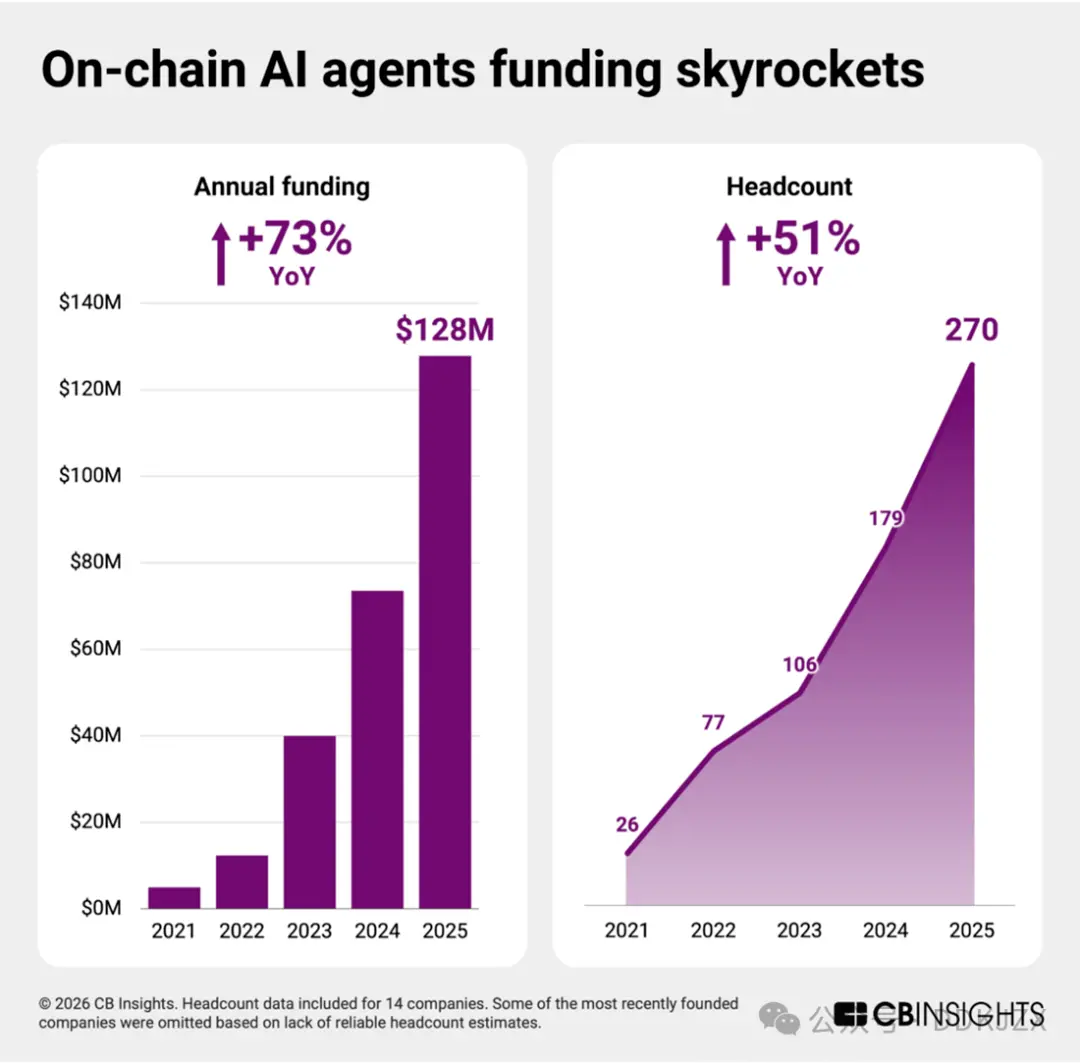

Thanks to advancements in generative AI technologies, startups in this space are transitioning from experimentation to infrastructure building. Although the average commercial maturity score stands at only 2 (validation phase), this remains an early-market sector among over 30 blockchain fields. However, it is poised for explosive growth.

From 2023 to 2025, equity funding nearly doubled year-over-year, and employee headcount grew by approximately 50%. Every independent company in this space has raised funding over the past two years, signaling strong investor confidence and heralding rapid expansion by 2026.

So far, agent payments have centered on consumer and e-commerce sectors, with Mastercard, Visa, Stripe, and Shopify planning to launch agent commerce tools by 2025.

Blockchain-based AI agent platforms are laying the groundwork for economically autonomous entities to transact and operate on decentralized networks. As agent payment infrastructure matures, this deeper coordination layer will become the cornerstone of the next phase of agent finance.

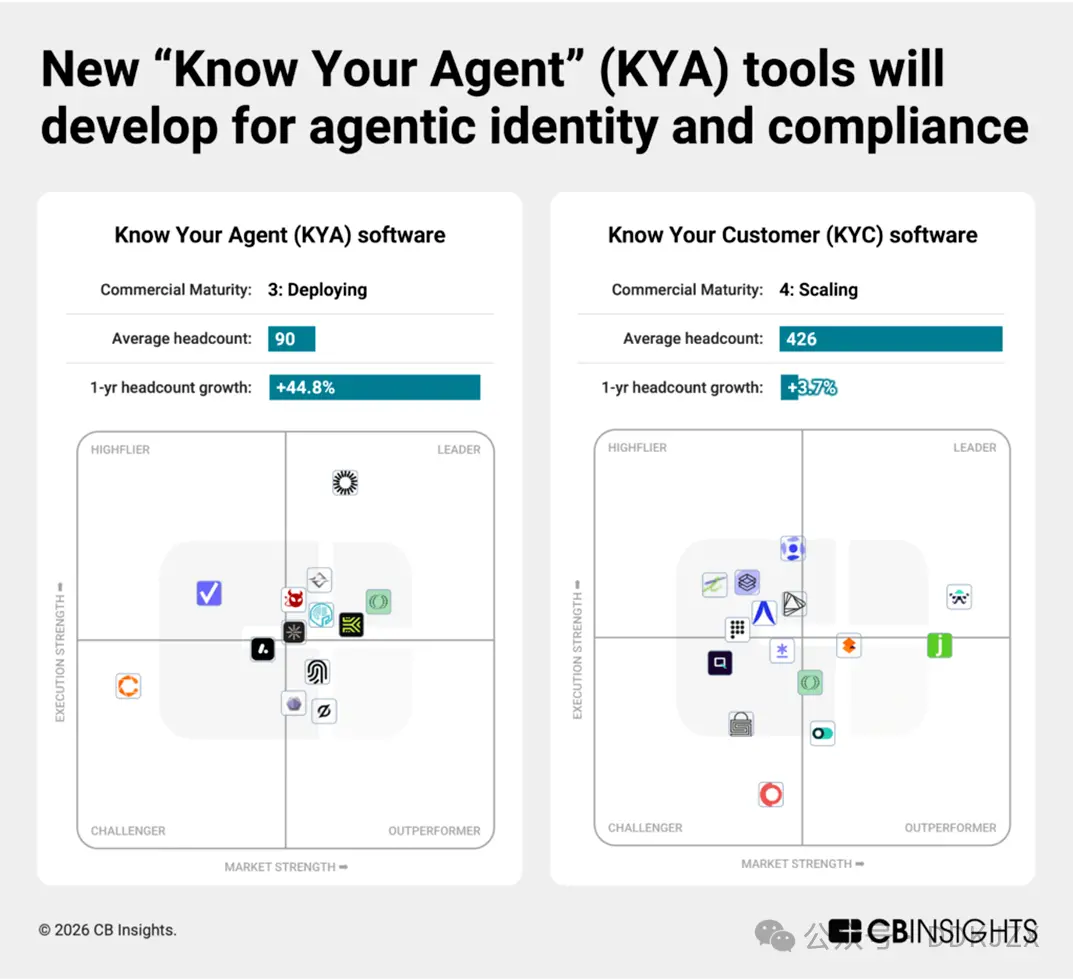

Forecast 8: New "Know Your Agent" (KYA) tools will emerge to regulate agent payment behavior.

As AI agents gain transaction rights, new compliance boundaries are forming.

Among the 96 cybersecurity markets we track, generative AI security and risk management platforms currently represent the fastest-growing segment. Unlike traditional "Know Your Customer" (KYC) providers, "Know Your Agent" (KYA) startups, despite their average commercial maturity of only 3 (still developing), saw funding growth exceed 450% over the past year.

Early-stage startups are building systems for identifying, authorizing, and behavior scoring for autonomous software agents. Although they are still in their infancy, each company below is demonstrating strong momentum, ranking in the top 15% of all companies according to our proprietary Mosaic scoring:

-

Keycard (commercial maturity 2, raised $30M in Series A funding in October, Mosaic top 2%) builds programmable identity and access infrastructure for AI agents, enabling secure authentication, wallet control, and policy-based permissions in financial applications.

-

Helmet Security (commercial maturity 2, raised $9M in Series A funding in December, Mosaic top 8%) develops compliance and risk tools native to agents, embedding transaction monitoring, policy enforcement, and auditability directly into autonomous workflows.

-

RunLayer (commercial maturity 1, raised $11M in seed funding in December, Mosaic top 6%) provides execution infrastructure for AI agents, managing credentials, environment isolation, and secure task orchestration across enterprise systems.

-

Overmind (commercial maturity 1, raised seed funding in September, Mosaic top 15%) focuses on behavior monitoring for AI agents by tracking activity patterns and implementing safeguards to prevent abuse, fraud, or policy violations.

-

T54 Labs (commercial maturity 1, set to raise seed funding in February 2026, Mosaic top 12%) scores payment agents based on a comprehensive, dynamic risk profile that covers transaction history, counterparties, and behavioral signals.

As regulators and enterprises demand accountability for machine-driven finance, KYA tools will become foundational to agent payments, just as KYC is to human banking.

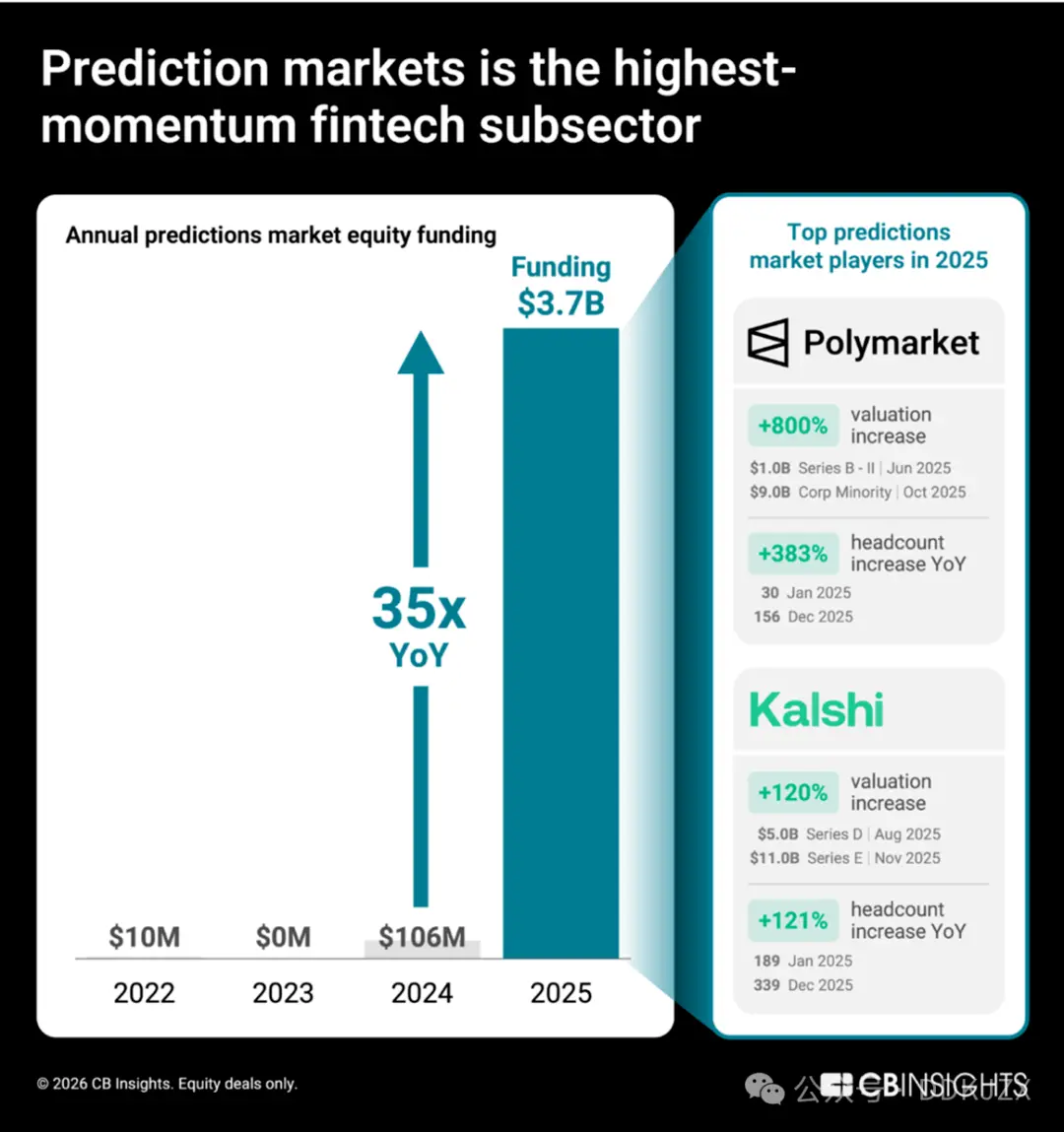

Forecast 9: Prediction markets aim to transition from gambling platforms to trusted data providers.

Prediction markets (platforms where users trade on the outcomes of real-world events) are experiencing unprecedented growth. Driven by Polymarket and Kalshi, equity funding in this sector is projected to grow 35-fold in 2025, soaring from $106M in 2024 to $3.7B. CB Insights' Mosaic data shows that among over 150 financial services and blockchain markets, prediction market platforms represent the fastest-growing fintech segment.

The changes in valuation and employee numbers indicate rapid growth for these two companies. In 2025 alone, Polymarket's valuation rose from $1 billion to $9 billion, with employee numbers increasing by 333%. Meanwhile, Kalshi's valuation grew by 120%, and its team expanded by 72%.

Our recruitment insights show that Polymarket's primary focus is building regulated U.S. exchange infrastructure and leveraging new marketing talent to extend its business beyond politics and cryptocurrency to mainstream consumer groups. Kalshi is similarly investing in marketing roles to drive mainstream consumer adoption of its products, while also strengthening connections with traditional financial platforms through multiple engineering roles.

Strategic partnership data further highlights that both Polymarket and Kalshi aim to enter the mainstream financial services sector and reposition themselves as trusted signal providers:

-

December 2025, Kalshi partnered with Harvard University to provide prediction market data to academic researchers.

-

Polymarket collaborated with Dow Jones to distribute market insights to institutional audiences.

-

Last December, Crypto.com teamed up with Kalshi to launch the National Prediction Market Alliance, expanding its user base from crypto-native audiences to mainstream financial channels. Both companies adopted similar strategies to win consumer trust: they each opened grocery store pop-up shops in New York in February 2026.

In this field, the ultimate winners are not merely the companies with the highest trading volumes, but those that can transform collective market signals into institutional-grade data products and establish partnerships with established institutions. For Polymarket and Kalshi, their ultimate goal is to evolve prediction markets from speculative tools into the core informational infrastructure for decision-makers.