Written by: Pine Analytics

Compiled by Saoirse, Foresight News

TAO is currently trading at approximately $275, with a market capitalization of $2.6 billion and a fully diluted valuation of $5.8 billion. The project has received institutional backing from Grayscale (which submitted an ETF listing application to the NYSE in December 2025) and public endorsement from NVIDIA CEO Jensen Huang. Additionally, the token supply narrative is highly compelling: a fixed supply cap of 21 million tokens, following a Bitcoin-style halving mechanism. After the first halving in December 2025, daily issuance will decrease from 7,200 to 3,600 tokens. Within a year, the number of subnets increased from 32 to 128, and Templar’s Covenant-72B training has demonstrated that decentralized compute can power large language models with benchmark-level competitiveness.

This report does not deny the above facts. We aim to explore whether the network’s economic model can generate real external revenues sufficient to support its current valuation, and how competitive it is against centralized service providers and self-hosted computing power.

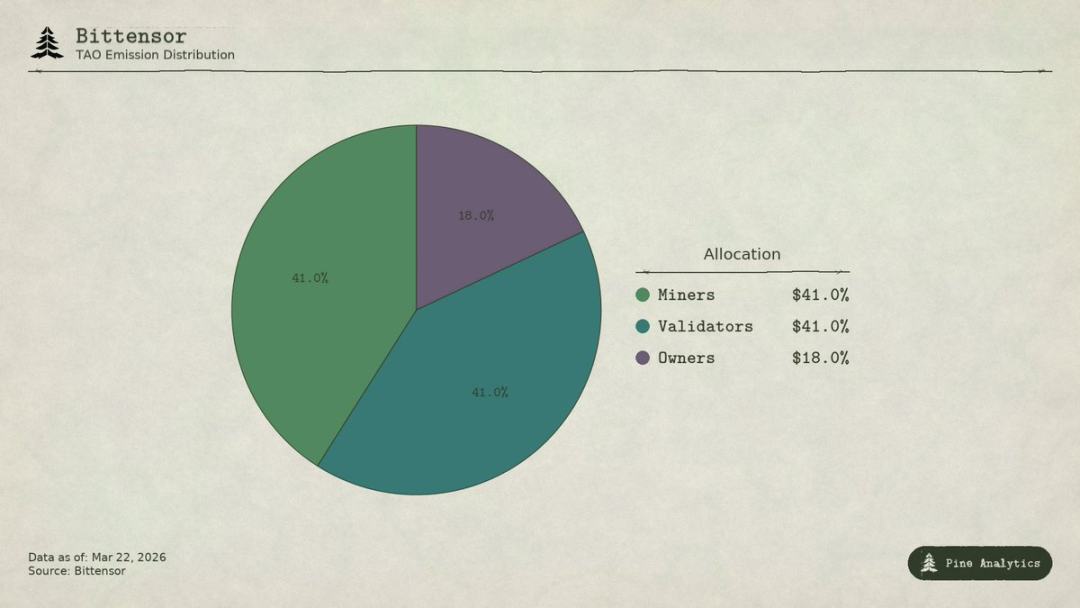

Bittensor (TAO) Token Issuance Allocation Ratio

How does network value flow?

Bittensor has four types of participants:

- The subnet owner establishes a professional AI marketplace and receives 18% of the TAO emission reward for the subnet;

- Miners perform AI tasks (inference, training, data processing) and earn 41%, totaling approximately 1,476 TAO daily, with an annualized value of about $148 million;

- Validators score miners' outputs and receive 41%;

- Stakers deposit TAO into the subnet liquidity pool in exchange for subnet-specific tokens.

Under the Taoflow model, a subnet's reward share is determined by the net inflow of TAO staking; a negative net inflow results in no reward. The top ten subnets control approximately 56% of the total network issuance.

TAO is a universal token across the network: miners must use TAO for registration, validators must stake TAO, subnets require TAO for token purchases, and services are paid for in TAO. In theory, subnet activity generates structural demand for the underlying token.

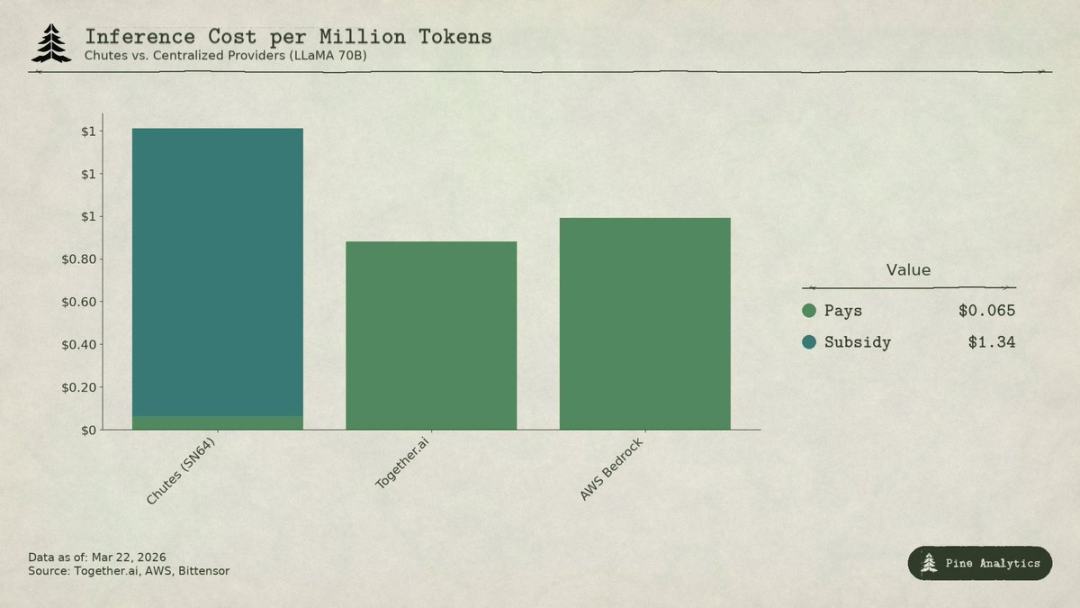

Comparison of inference costs between Bittensor subnet Chutes (SN64) and centralized service LLaMA 70B model

Current state of demand-side

Supply transparent vs. Demand opaque

Bittensor’s supply side is highly transparent: 3,600 TAO are programmatically distributed daily, with halving rules hard-coded; staking rate (approximately 70%), allocation ratios, and liquidity data are all on-chain.

However, demand-side activity is completely opaque. There is no unified dashboard to track external revenue by subnet, and actual AI service calls—such as inference, computation, and training—all occur off-chain and are not recorded on the blockchain. Investors can only infer demand through indirect metrics like staking flows, subnet token prices, and project-reported data. This opacity is structural, not temporary. The blockchain records token transfers, not API calls.

Here is the most comprehensive demand-side profile as of March 2026.

Chutes (SN64): Low prices are entirely supported by subsidies

Chutes accounts for 14.4% of the total supply across the network, the highest among all subnets. Developed by Rayon Labs, it offers open-source, serverless inference services at prices 85% lower than AWS and 10–50% lower than Together AI. Its usage metrics dominate the ecosystem: over 400,000 users (including over 100,000 API users), more than 5 million daily requests, and a cumulative processing volume of 9.1 trillion tokens, with average daily token generation rising from 6.6 billion to 101 billion in just three days. It is also a top inference provider on OpenRouter, with some models outperforming centralized competitors.

But this low price comes from subsidies, not operational efficiency.

At a 14.4% share, Chutes receives approximately 518 TAO daily, equivalent to an annualized value of about $52 million. However, its external annual revenue is only around $1.3–2.4 million (the higher figure is self-reported by the team and has not been independently audited). The protocol subsidizes this subnet at a ratio of approximately 22:1 to 40:1—meaning for every $1 paid by users, the network releases $22–40 in TAO through inflation to subsidize it.

Without subsidies, and based on its daily processing volume of approximately 10.1 billion tokens, the cost price is about $1.41 per million tokens. Current centralized market prices:

- Together.ai's LLaMA 3.3 70B Turbo is approximately $0.88 per million tokens;

- DeepSeek V3 is approximately $0.40–$0.80;

- Small models start as low as $0.18.

This means that, after removing subsidies, Chutes' price will be 1.6 to 3.5 times higher than centralized solutions. The claimed 85% cost advantage is completely reversed—its low price is fundamentally funded by inflation paid for by TAO holders, not by structural efficiencies from decentralization.

When the next halving arrives (expected by late 2026 or 2027), either the price will double, miners will exit, or the gap between subsidies and revenue will widen further.

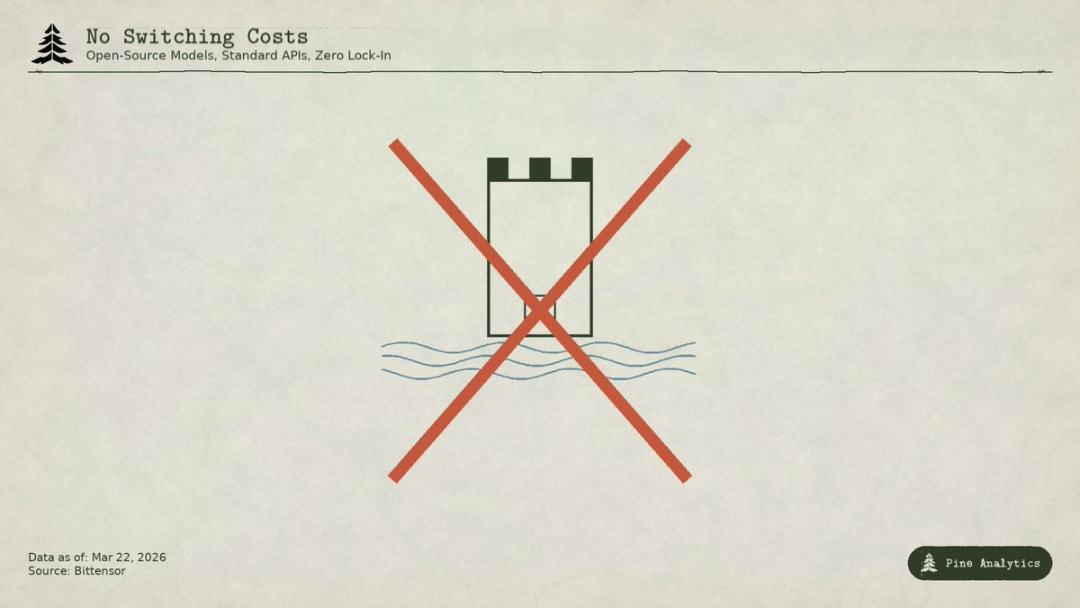

Some compare this to early internet subsidies for customer acquisition, but Uber, DoorDash, and AWS built switching costs during their subsidy periods: proprietary platforms, driver networks, and enterprise ecosystems. Bittensor subnets, however, have no barriers: models are open-source, interfaces are standardized, and users can switch providers at zero cost. Once subsidies fade, there are no lock-in mechanisms to retain users.

Rayon Labs also operates SN56 and SN19, collectively controlling approximately 23.7% of the total supply, with no external revenues disclosed. A single team controls nearly a quarter of the network’s incentive distribution.

Targon, Templar, and other subnets

Targon (SN4) is the highest-revenue subnet, operated by Manifold Labs, providing confidential GPU computing services to enterprises, with an estimated annual revenue of approximately $10.4 million and a valuation of $48 million, resulting in a price-to-sales ratio of about 4.6x—the most solid valuation within the ecosystem. However, the $10.4 million figure is a projected estimate cited by multiple reports and has not been audited.

Templar (SN3) has completed the Covenant-72B training, with a market cap of $98 million, but zero external revenue. The training API and enterprise sales are still in progress, and no paid product has been launched yet.

The other 120+ subnets either have no public revenue or are still in early product stages, primarily relying on token issuance subsidies to sustain operations.

Overview

The total annual demand-side revenue confirmed across the entire network is only approximately $3 million to $15 million. The annualized subsidy for just the Chutes subnet (approximately $52 million) exceeds the upper limit of the entire network’s external revenue.

At a market cap of $2.6 billion, its revenue multiple is approximately 175–200x; at a fully diluted valuation of $5.8 billion, it approaches 400x. In contrast, centralized AI compute companies have seen recent funding valuations of only 15–25x forward revenue, and high-growth SaaS companies rarely sustain multiples above 50x for extended periods. Bittensor’s valuation multiple is 4–10 times that of even the most aggressive industry peers.

The large gap between valuation and fundamental demand indicates that the market is pricing TAO almost entirely based on supply-side scarcity (halving, staking locks), institutional catalysts (Grayscale ETF, exchange listing expectations), and AI sector sentiment—rather than actual economic output. While these are legitimate price drivers, they are entirely distinct from the logic that Bittensor creates sustainable value as an AI services network.

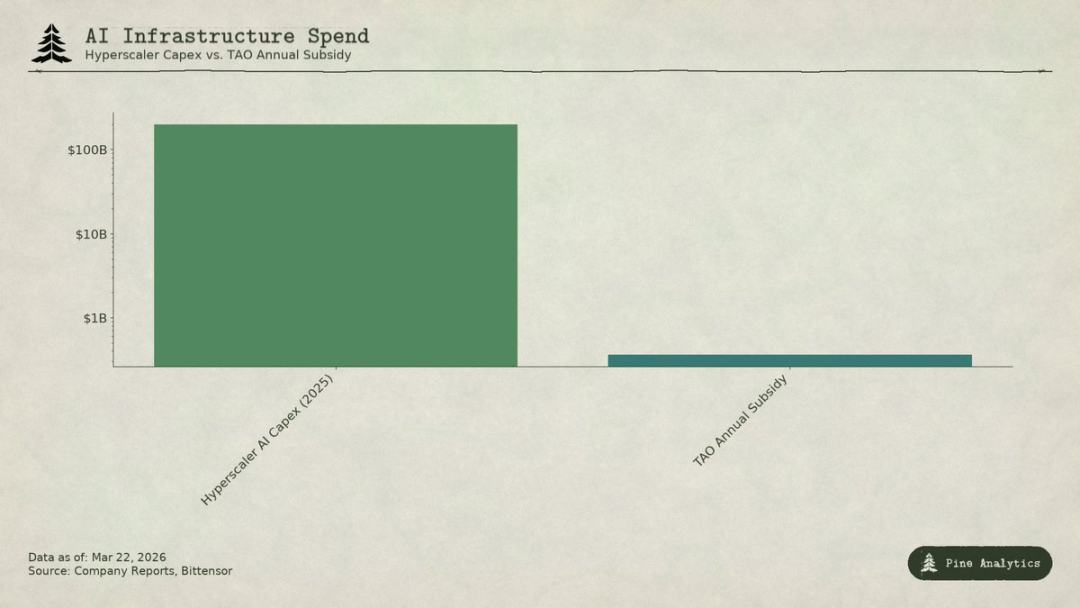

Compare the AI capital expenditures of hyperscale cloud providers with the annual subsidy scale of Bittensor (TAO)

Pricing Dilemma: Squeezed from Both Sides

The subnet is facing pressure from both sides:

- Top: Self-custody cap

All models on the platform are open-source with publicly available weights; running a 70B model on a single H100 costs only $40–50 per day in total. Tools like vLLM and Ollama make local deployment extremely simple. NVIDIA’s next-generation chips will further reduce inference costs. Institutions with sufficient usage will find self-hosted deployment even more cost-effective.

- Below: Cloud giants squeeze

Microsoft, Google, Amazon, and Meta will collectively spend over $200 billion on AI capital expenditures in 2025, enjoying priority access to hardware, dedicated data centers, enterprise customer relationships, and the ability to subsidize AI with cash flows from other businesses. Bittensor’s annual incentive budget (approximately $360 million) is less than Microsoft’s weekly AI infrastructure investment. Professional service providers are also using VC funding to subsidize low-price competition on open-source models.

Subnet pricing is compressed into an extremely narrow range, yet still bears the inherent costs of decentralization: token friction, validator node expenses, subnet owner splits, network latency, and more.

Moat issue

Even if a subnet provides valuable services, the underlying models and methods are inherently open: Covenant-72B uses the Apache license, and its technical papers are publicly published. Any competitor can directly replicate them without participating in the TAO ecosystem.

Traditional moats (proprietary technology, network effects, switching costs, brand) do not apply:

- Open-source technology;

- Network effects belong to TAO, not to individual subnets;

- Model weights are consistent, and the user switching cost is zero.

The community believes that the incentive mechanism is the moat, but it relies on continuous large-scale token issuance, and each halving continuously reduces the incentive budget.

What is TAO actually trading?

At a $2.6 billion market cap, TAO’s price does not reflect demand fundamentals—annual revenues of $30–150 million cannot be sustained under any traditional framework. The market is pricing in: Bitcoin-like scarcity, Grayscale ETF expectations, AI sector rotation, and the long-term option value of decentralized AI. These are all valid speculative factors, but they originate entirely from supply-side dynamics and market sentiment.

If you hold TAO based on scarcity and narrative, you may still profit even with weak demand; however, if you believe Bittensor will become a truly scalable AI service network, there is currently no evidence to support this, and it faces significant structural barriers. Investors should clearly distinguish their investment rationale.