Author: Lüdong

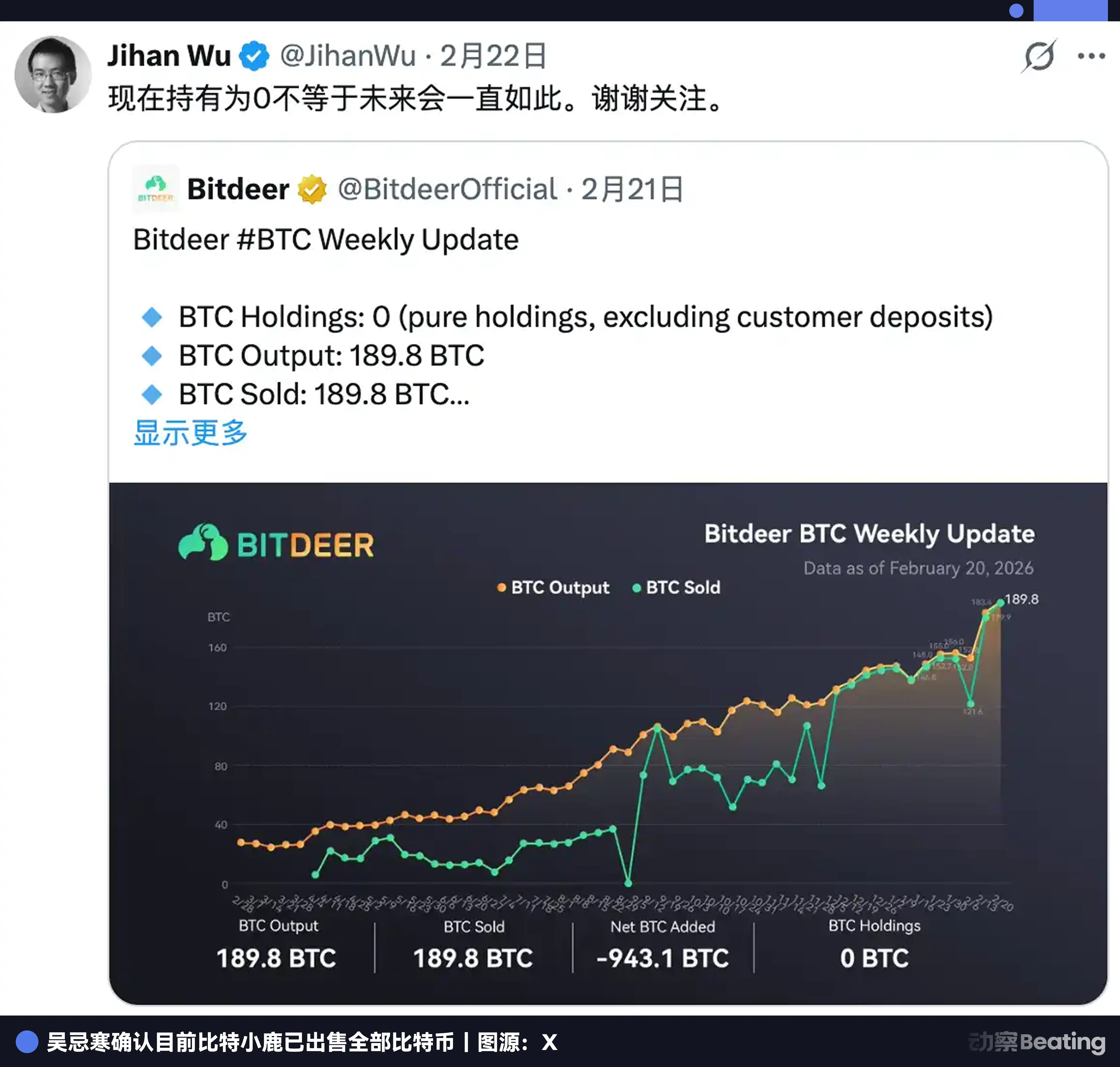

On February 20, 2026, Bitdeer posted a weekly production update on X: 189.8 BTC were self-mined this week and sold. Remaining inventory of 943.1 BTC was sold in a single transaction.

Bitcoin balance: 0.

In fact, Bitcoin mining has always been a form of time arbitrage since day one.

Exchange today’s electricity and machinery for tomorrow’s Bitcoin. No factory needed, no customers required, no brand necessary. You invest today’s costs and bet on future prices. If you’re right, time will make you money.

This logic has been running for over a decade. What Wu Jihann is doing now is changing the goal of this system.

The target has shifted from cryptocurrency prices to the long-term price of computing power under an AI-driven climate. The method has changed from using electricity to acquire coins to borrowing money to purchase land. The arbitrage object has changed, but the arbitrage structure remains the same.

In the same week it cleared its Bitcoin holdings, Bitdeer also priced $325 million in new debt.

According to Bitdeer's financial report, as of December 31, 2025, Bitdeer's book debt amounted to $1 billion. Therefore, the total debt is approximately $1.3 billion.

The debt is real, the land purchase is real, but the outcome of this tough battle may not be revealed until 2029.

One: A mining company that doesn't want to embrace AI isn't a good company.

Bitdeer, founded in 2018, began as a mining machine sharing platform. It is now one of the world’s largest publicly traded mining companies, with self-mined hash rate of 63.2 EH/s—the highest among all publicly traded mining companies globally—accounting for approximately 6% of the entire Bitcoin network’s hash rate.

But now, Wu Jihann no longer wants to sell computing power—he wants to get into electricity.

Breaking down Bitdeer’s financial report, as of early 2026, Bitdeer’s total global power capacity amounted to 3,002 MW, with 1,658 MW already operational and 1,344 MW under construction or planned. Microsoft and Google’s individual hyperscale data centers typically range from 100 to 300 MW in scale.

In other words, 3,002 MW is equivalent to packaging the power demands of 10 to 30 Google mega-data centers into a single company. Therefore, Bit Deer’s pipeline is, on paper, extremely impressive.

The primary use of the $1.3 billion in debt is to secure power and land assets globally to pave the way for the transition to AI data centers.

The first is Rockdale, Texas, at 563 MW (including 179 MW of expansion), operational, primarily for mining. This is our core business, generating stable cash flow.

Second, in Clarington, Ontario, a 570 MW facility with a 30-year lease, power contract already signed, originally scheduled for completion in Q2 2027, positioned as a core HPC/AI site. This is the centerpiece of the entire AI transformation plan—and also the largest current risk, which we will detail later.

Next is Tydal, Norway, a 175 MW facility converting its mining site into an AI data center, expected to be completed by end-2026 with 164 MW of usable IT load. Abundant hydropower ensures competitive energy costs, and the retrofit cost is significantly lower than new construction—currently the fastest and lowest-risk option available.

Land, electricity, and data centers—these three assets are referred to by the AI industry as "the hardest to replicate." Bit Deer has accumulated them through a decade of mining operations.

One rarely mentioned fact worth highlighting: SEALMINER. Bitdeer is not only building data centers but also developing its own mining chips in-house. The SEAL series has now reached its third generation—the SEAL03 achieves an energy efficiency of 9.7 joules per terahash, and the A3 Pro, set for mass production in September 2025, is already among the top-tier miners globally. The upcoming SEAL04 targets an efficiency of just 5 joules per terahash; if achieved, it will surpass all currently mass-produced miners on the market. The gross margin on these in-house chips exceeds 40%, significantly higher than the margin from mining operations themselves.

He is reenacting what he did at Bitmain: moving from buying others' shovels to making his own.

II. How much can you borrow, and how much profit can AI generate?

To fund AI initiatives, by the end of 2025, Bitdeer's book debt exceeded $1 billion. Adding the new debt of $325 million in February 2026, the total debt scale surpassed $1.3 billion.

In less than two years, multiple funding rounds took place. In May 2024, Tether invested $100 million, becoming the second-largest shareholder with warrants allowing an additional investment of $50 million. Three months later, the first convertible bond of $150 million was finalized at an annual interest rate of 8.5%. In November of the same year, a second tranche of $360 million was raised, with the interest rate reduced to 5.25%.

In November 2025, a package was issued: 400 million in convertible bonds and 148.4 million in equity issuance, both as配套 offerings. In February 2026, another 325 million in convertible bonds and 43.5 million in equity were issued, alongside the repurchase of 135 million of the earliest 2029 bonds, extending the repayment maturity to 2032.

Totaling over $1.4 billion. Funds flowed into mining equipment, data centers, and AI infrastructure, along with rolling debt refinancing.

However, each time bonds are issued, Bit Deer's stock price drops by 10% to 17%. This has become a fixed market reflex. Fortunately, the company still secures the funding each time.

The core of the debt structure is convertible bonds. These new 2032 bonds have an initial conversion price of approximately $9.93, a 25% premium over the concurrent equity offering price of $7.94. If the stock price reaches that level, bondholders will convert into shares instead of receiving cash. The company effectively doesn’t need to repay the debt—only requires the stock price to rise.

The logic behind convertible bonds is betting that the company’s stock price will rise. This, in itself, is a gamble on whether the AI narrative will be accepted by the market. At an average interest rate of 5% on a principal of $1.3 billion, annual interest payments exceed $650 million. Yet, the company’s full-year 2025 AI/HPC cloud revenue falls far short of even a fraction of six months’ interest.

Currently, this interest is being rolled over entirely through new bond issuance. It’s impossible to say the pressure is minimal.

Given such a significant investment, there must be expectations of more substantial returns. Let’s take Bitdeer and examine how much additional value AI can generate.

The AI business currently generates $10 million annually, accounting for less than 2% of total revenue. For a company with a market capitalization of nearly $2 billion, this figure is negligible.

Of course, this is not the end.

Bitdeer’s GPU count increased from 584 to 1,792 over three months, tripling in size. Utilization dropped from 87% to 41%, primarily due to rapid machine deployment; the B200/GB200 units are still in customer testing and have not yet started generating revenue. Power infrastructure is in place, and machines are being installed—the denominator is surging, but revenue has not yet caught up.

How high is the ceiling?

Roth/MKM estimates that full deployment of HPC capacity could generate an annual revenue potential of $850 million. Management is more aggressive: allocating all 200 MW to AI cloud services could exceed $2 billion annually, triple the total mining revenue for 2025.

But both figures are contingent on three conditions: timely completion of construction, securing long-term contracts with hyperscalers, and full utilization of the GPUs.

Three conditions have yet to be met.

This is the battle BitDwarf is fighting: using mining to fund AI, while AI generates visions—whether these visions can become reality depends on execution over the next two to three years.

Three, the challenge lies in how narrow the time window is.

$1.3 billion in bonds sounds dangerous. But Bitdeer’s debt structure is designed to be more stable than it appears.

Highly leveraged companies typically die for the same reason: debt matures en masse, cash is insufficient, and they are forced to sell assets at a loss.

Bitdeer has set the maturity dates for the three batches of convertible bonds to 2029, 2031, and 2032, respectively.

To some extent, this is a deliberately constructed buffer. By the time the first tranche matures, Tydal and Clarington should both be fully operational; by the second tranche’s maturity, AI revenue should be generating measurable income; by the third tranche’s maturity, the market will have its own assessment of what this company truly is. Three milestones, three opportunities to renegotiate.

But convertible bonds provided time, and Wall Street isn’t buying it. Keefe Bruyette slashed its price target from $26.50 to $14. The current stock price is around $8. The market’s message is clear: the transformation story must deliver revenue.

But all this pressure gave Wu Jihann what he needed most—and also what was most brutal: time.

The smooth path might unfold like this: By the end of 2026, Tydal’s transformation is complete, the 164 MW hydro-powered data center in Norway goes live, and European client contracts begin to flow in. In 2027, Clarington wins its legal case, and the 570 MW facility in Ohio officially breaks ground, drawing in major U.S. clients. By 2028 to 2029, both core assets operate at full capacity, driving revenue toward the $1 billion mark, as analysts reclassify Bitdeer from a discounted mining company to one with an AI infrastructure premium. When the first batch of bonds matures in 2029, bondholders, seeing the stock price, will most likely opt for equity conversion rather than cash repayment.

In each of these tough battles, Wu Jihan had to hit the exact timing.

Then there is Clarington.

In the same industrial park in Ohio, American Heavy Plate Solutions, a steel manufacturer, signed a 30-year lease for 9.9 acres of land in 2018. They have sued Bitdeer, claiming that constructing an AI data center would disrupt shared utilities—including electricity, roads, railways, and communication lines—violating restrictive covenants. They are seeking a court injunction to permanently prevent Bitdeer from breaking ground.

Clarington represents 42% of the pipeline under construction. If stalled, the entire timeline must be rewritten.

Therefore, Bitdeer's largest single point of risk is not debt, nor its stock price, but a steel mill.

The mining side hasn’t had a moment to catch its breath. In February 2026, Bitcoin’s network difficulty surged by 14.7%, the largest single increase since May 2021. With the same electricity costs, miners are now producing fewer coins. Gross margins in Q4 have dropped from 7.4% a year ago to 4.7%. Mining, once a strong pillar, is slowly weakening.

The worst-case path is clear: The Clarington lawsuit drags on for two years, halting construction; Tydal faces delays, with GPU utilization remaining stuck at 41%; the first batch of bonds matures in 2029, but cash on hand is insufficient, forcing refinancing, further share dilution, and making the conversion threshold increasingly difficult to reach.

Two paths, both genuinely exist.

Four: Sell all your Bitcoin—then what?

In the mining community, there's a tradition: holding coins is a belief, a testament to Bitcoin’s long-term value.

MARA has accumulated 53,250 BTC, Riot has accumulated 18,000 BTC, and Strategy has accumulated 710,000 BTC. The more you accumulate, the more the market believes in you.

Bitdeer is currently zero.

The official explanation is: selling coins is to provide liquidity for purchasing land. This makes sense. Peers are also moving in the same direction: Riot sold $200 million in Bitcoin to fund AI expansion, Bitfarms is stepping away from its identity as a Bitcoin company, and MARA is also investing in HPC.

But there's something more fundamental here than identity iteration.

Since its very first day, the mining industry has always bet on one thing: that some future value will be more expensive than today’s cost. A decade ago, miners bet that cryptocurrency prices would rise. Today, those buying land are betting that demand for computing power will explode.

The target has changed, but the logic of time arbitrage remains the same.

What Wu Jihan truly bought was a position where, regardless of who wins, they must pay me for the electricity.

Don’t bet on a specific赛道; just control the entrance to the赛道. Amazon didn’t bet on which internet company would win; it simply rented servers to everyone. AT&T doesn’t care what you talk about on the phone; it only cares whether you made the call.

From selling products, to selling services, to collecting rent—the evolution of industries has always followed this one path.

The only difference is whether you walk over there on your own or are pushed there.

Wu Jihan bought this window with over a billion dollars. He is waiting for AI money to catch up with his debt.