Author: ChandlerZ, Foresight News

When the market experiences a sharp decline, narratives often quickly seek out an identifiable source.

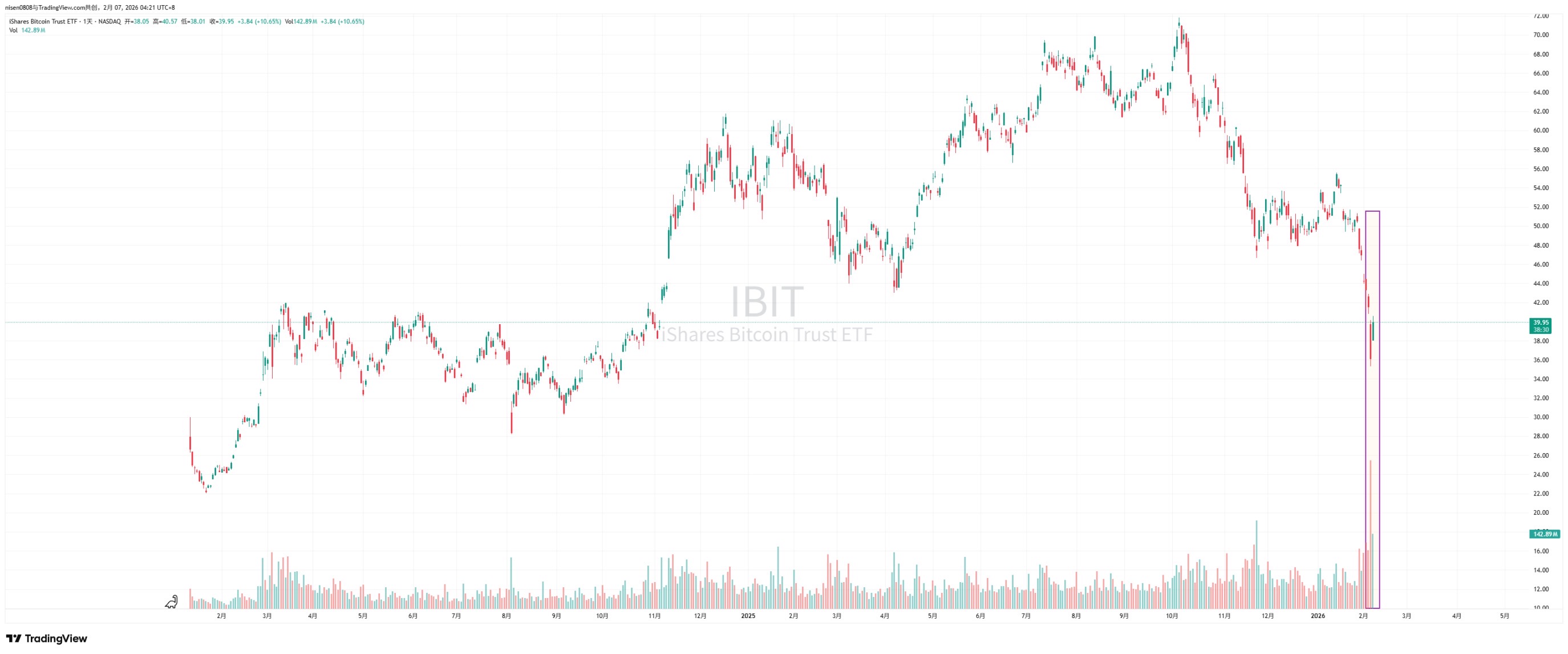

Recently, the market has begun in-depth discussions about the crash on February 5 and the rebound close to $10,000 on February 6. Jeff Park, a Bitwise advisor and Chief Investment Officer of ProCap, believes that this volatility is more closely linked to the Bitcoin spot ETF system than imagined by the outside world, with key clues concentrated in the secondary market and options market of the iShares Bitcoin Trust (IBIT) under BlackRock.

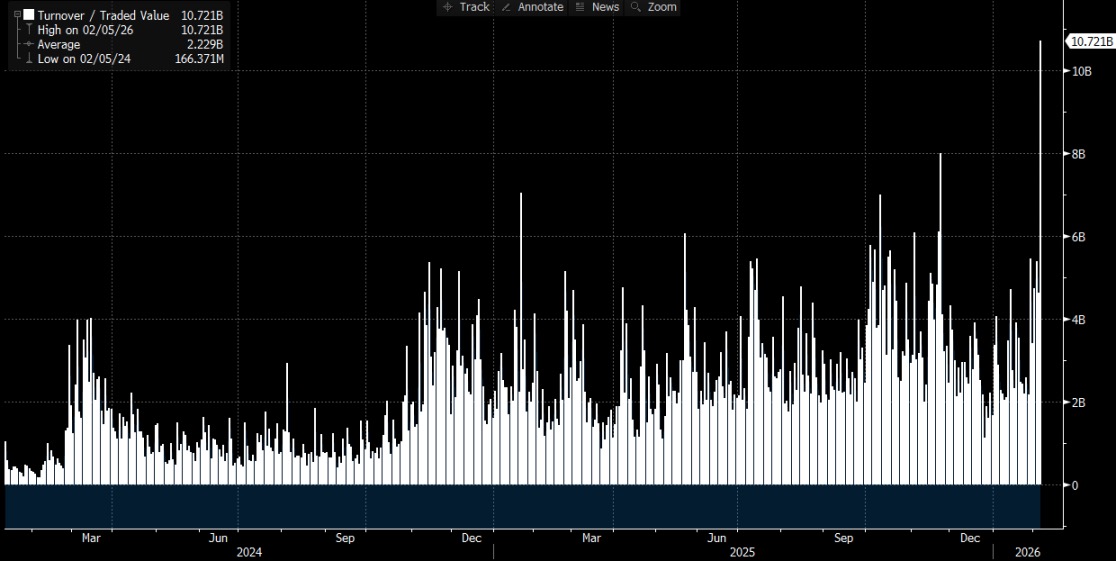

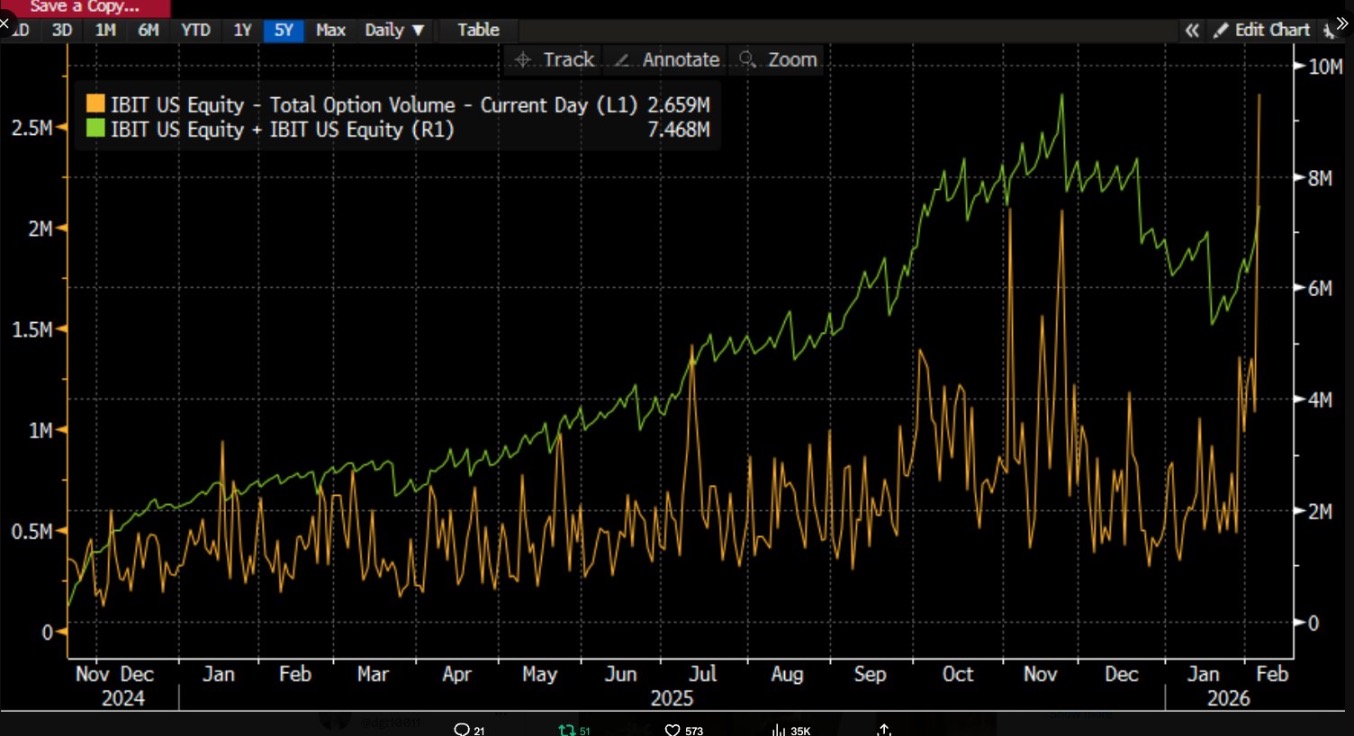

He pointed out that on February 5, IBIT saw record trading volume and options activity, with significantly higher trading size than before, and the options trading structure was biased toward put options. More counterintuitive was the fact that, according to historical experience, if the price drops by double digits in a single day, the market usually sees noticeable net redemptions and outflows of funds, yet the opposite happened. IBIT recorded net creation, with new shares driving an increase in size, and the entire spot ETF portfolio also experienced net inflows.

Jeff Park believes that this combination of "plummeting and net creation" weakens the explanatory power of the single path that ETF investors' panic redemptions cause the decline, but instead fits more with deleveraging and risk reduction within the traditional financial system, where traders, market makers, and multi-asset portfolios are forced to reduce risk under derivative and hedging frameworks, the selling pressure comes more from position adjustments and hedging chain compression in the paper money system, and finally transmits the impact to the Bitcoin price through IBIT's secondary market trading and options hedging.

There is a lot of discussion in the market that easily connects institutional liquidation of IBIT directly to a sharp market decline in one sentence, but this causal chain, if not broken down into its mechanistic details, is very likely to reverse the sequence. Secondary market trading of ETFs targets ETF shares, while the creation and redemption in the primary market correspond to changes in custodied BTC. Directly linearly mapping secondary market trading volume to an equivalent amount of spot selling lacks several essential explanatory links in logic.

The so-called "IBIT triggering large-scale liquidation," the debate is actually about the transmission path.

The controversy around IBIT mainly concerns which layer of the ETF market and through what mechanism the pressure is transmitted to the price formation of BTC.

A more common narrative focuses on the net outflow from the primary market. Its intuition is simple: if ETF investors redeem in panic, the issuers or authorized participants need to sell the underlying BTC to meet the redemption consideration, the selling pressure enters the spot market, the price drops further triggering liquidations, forming a stampede.

This logic sounds complete, yet it often ignores a fact. Ordinary investors and the majority of institutions cannot directly subscribe to or redeem ETF shares; only authorized participants can create and redeem shares in the primary market. The commonly mentioned "daily net inflow or outflow" in the market generally refers to the change in the total amount of shares in the primary market. No matter how large the trading volume is in the secondary market, it only changes the holders of the shares, and will not automatically change the total amount of shares, nor will it automatically lead to an increase or decrease in the BTC held by the custodian side.

Analyst Phyrex Ni said that the liquidation Parker mentioned is actually the liquidation of the IBIT spot ETF, not the liquidation of Bitcoin. For IBIT, only the IBIT token is traded in the secondary market, with the price pegged to BTC, but the trading itself is only transferred within the securities market.

The part that actually touches BTC only occurs in the primary market, that is, the creation and redemption of shares, and this channel is executed by APs (which can be understood as market makers). When creating new IBIT shares, APs need to provide corresponding BTC or cash consideration. BTC will enter the custody system and be subject to regulatory constraints, and the issuer and relevant institutions cannot arbitrarily use it. When redeeming, the custodian side will hand over the BTC to the AP, who will then handle the subsequent disposal and settle the redemption funds.

ETF is essentially a two-tier market. The primary market is mainly about buying and redeeming Bitcoin, and this part is almost entirely provided by APs for liquidity. Fundamentally, it is the same as generating USDC with USD. Moreover, APs rarely circulate BTC through exchanges, so the biggest use of buying spot ETF is to lock up the liquidity of Bitcoin.

Even if redemptions occur, AP's selling behavior does not necessarily need to go through the open market, especially not through the exchange spot market. AP itself may hold inventory BTC and can complete delivery and fund arrangements in a more flexible way within the T+1 settlement window. Therefore, even during the large-scale liquidation on January 5th, the BTC redeemed by BlackRock's investor outflows was less than 3,000, and the total BTC redeemed by all U.S. spot ETF institutions was less than 6,000, meaning the maximum amount of Bitcoin sold by ETF institutions to the market was 6,000. Moreover, these 6,000 may not all be transferred to exchanges.

But the liquidation of IBIT that Parker mentioned actually occurred in the secondary market, with a total trading volume of about 10.7 billion U.S. dollars, which is the largest trading volume in the history of IBIT. It did indeed trigger some institutional liquidations, but it should be noted that this part of the liquidation was only for IBIT, not for Bitcoin, and at least this part of the liquidation did not spread to the primary market of IBIT.

So the sharp drop in Bitcoin only triggered liquidations of IBIT, but did not result in BTC liquidations caused by IBIT. The underlying asset of the secondary market trading of the ETF is essentially the ETF itself, and BTC is merely the price anchor of the ETF. The maximum impact on the market would be liquidations caused by selling BTC in the primary market, not IBIT. In fact, although BTC's price fell more than 14% on Thursday, BTC's net outflow from the ETF only accounted for 0.46%. On that day, BTC spot ETFs held a total of 1,273,280 BTC, with a total outflow of 5,952 BTC.

Transmission from IBIT to Spot

@MrluanluanOP believes that when IBIT's long positions are liquidated, there will be concentrated selling in the secondary market. If the natural buying demand in the market is insufficient to absorb the selling pressure, IBIT will trade at a discount to its implied net asset value. The larger the discount, the greater the arbitrage opportunity, and the more incentive arbitrageurs and market participants will have to buy the discounted IBIT, as this is part of their routine profit-making strategy. As long as the discount is sufficient to cover the costs, theoretically, there will always be professional capital willing to take the position, so there is no need to worry about "no one to take the selling pressure."

After taking on the shares, the issue shifts to risk management. After AP takes over the IBIT shares, it cannot immediately redeem and liquidate these shares at the current price, as the redemption involves time and procedural costs. During this period, the prices of BTC and IBIT will still fluctuate, and AP faces net exposure risk, so it will immediately hedge. The hedging methods may include selling physical inventory or opening short positions in the futures market.

If the hedge falls on the spot sell, it will directly depress the spot price; if the hedge falls on the futures short, it will first manifest as changes in the price spread and basis, and then further affect the spot through quantification, arbitrage, or cross-market trading.

After the hedging is completed, the AP holds a relatively neutral or fully hedged position, allowing for more flexibility in deciding when to handle this batch of IBIT at the execution level. One option is to choose redemption back to the issuer on the same day, which would be reflected as redemptions and net outflows in the official inflow and outflow data after the close. Another option is to choose not to redeem immediately, waiting instead for the secondary market sentiment to recover or for a price rebound, and then directly sell the IBIT back to the market, thereby completing the entire transaction without going through the primary market. If the IBIT recovers to a premium or the discount converges the next day, the AP can sell the position in the secondary market to realize a spread profit, while closing out the previously established futures short position or replenishing the previously sold inventory.

Even if the final share processing mainly occurs in the secondary market and there is no significant net redemption in the primary market, the transmission of IBIT to BTC is still possible, because the hedging actions taken by APs when taking on discount positions will transfer the pressure to the BTC spot or derivatives market, thus forming a channel where the selling pressure from the IBIT secondary market overflows into the BTC market through hedging activities.