Original author: Machines & Money

AididiaoJP, Foresight News

Everyone is asking the wrong question.

Bitcoin has dropped 50% since reaching its all-time high of $126,000 on October 6, 2025.

Gold reached a historic high of $5,595 on January 29, 2026.

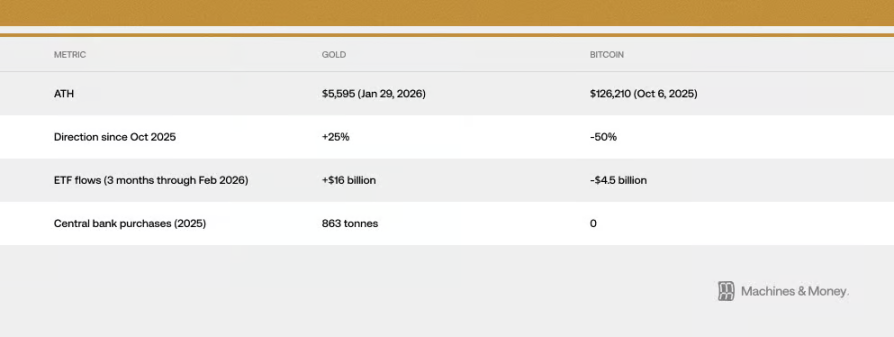

Since Bitcoin reached its peak, gold has risen over 25%, while Bitcoin's price has been halved.

The cryptocurrency market's Fear & Greed Index dropped to an unprecedented 5 on February 6, reaching an even more extreme level than during the COVID-19 pandemic or the collapse of the FTX exchange, and has only barely recovered to the teens since.

Crypto commentators have resumed their usual debate: Is Bitcoin really digital gold?

But this question is fundamentally flawed, as it assumes Bitcoin’s identity as an asset is fixed and unchanging. In reality, Bitcoin’s behavior has shifted significantly multiple times under different macroeconomic conditions: in 2017, it moved with gold; in 2021, it followed tech stocks; and since late 2024, it has become tightly correlated with software stocks.

For institutional investors, a more practical question is: What factors are truly driving Bitcoin’s price movement in today’s liquidity environment?

Based on evidence as of February 2026, the answer is: Bitcoin is currently behaving like a highly volatile software stock. Whether this is a temporary phenomenon caused by their shared sensitivity to the same macroeconomic factors, or whether Bitcoin’s role in portfolios has been permanently redefined, remains to be seen—but the data is becoming increasingly impossible to ignore.

How strong is this correlation, and how long has it lasted?

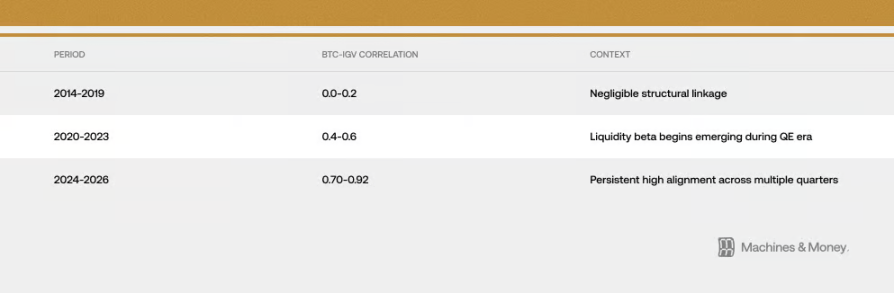

The relationship between Bitcoin and IGV (an ETF that tracks software stocks) has become increasingly close over three distinct time periods:

By late February 2026, their 30-day rolling correlation coefficient had reached approximately 0.73. More importantly, this highly correlated level above 0.5 has been maintained for over 18 months. This duration clearly exceeds the typical 3-6 month span of short-term style shifts, but is still insufficient to indicate a permanent change spanning an entire market cycle (4–7 years).

The recent downturn has made their relationship more apparent. By late February 2026, IGV had fallen approximately 23% this year, while Bitcoin had dropped 19–20%. This software stock ETF is experiencing its worst quarter since the 2008 financial crisis. Over the past month and three months, Bitcoin and IGV have moved in near-perfect sync, indicating their price movements have been very closely aligned. During this decline, Bitcoin’s volatility was about 1.1 to 1.3 times that of software stocks—lower than the 2 to 3 times many had assumed.

One thing to note: during market turbulence, short-term correlations between assets can surge even if there is no fundamental relationship, as investors’ risk appetite declines simultaneously. However, this high degree of synchronization has persisted for over 18 months, suggesting something more substantial than random fluctuations is at play. Still, this alone does not prove causation between assets or guarantee that this relationship will endure indefinitely.

2025: A Major Test of Its Status as a Safe-Haven Asset

If any year could test whether Bitcoin truly serves as a hedge against currency depreciation, it would be 2025. That year will see accelerating fiscal expansion, a weakening dollar, rising geopolitical risks, persistently high inflation, and growing market expectations for Fed rate cuts.

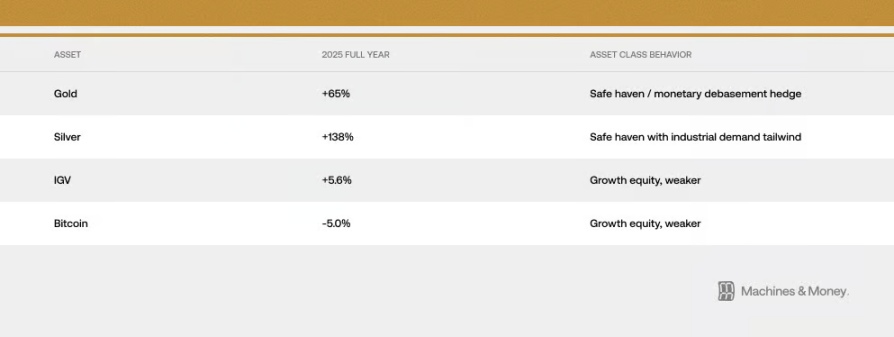

This should have been the ideal environment for Bitcoin to demonstrate its "digital gold" properties. But what has happened since October 2025 tells a different story: gold rose from $4,400 to a record high of $5,595, while Bitcoin fell from $126,000 to just over $60,000. Two assets entrusted with the same "inflation hedge" function moved in completely opposite directions at the very moment they were most needed for that role. The result?

Gold reached a historic high of $5,595 on January 29, 2026. Central banks around the world purchased 863 tons of gold in 2025, marking the third consecutive year of significant buying. However, no central bank purchased Bitcoin.

The massive disparity in capital flows is the strongest rebuttal to the "digital gold" argument: when major institutions and sovereign funds truly needed a hedge against the very macroeconomic conditions that Bitcoin is supposed to protect them from, they chose gold with a capital allocation ratio of more than three to one.

This is not to say that Bitcoin will never become a safe-haven asset in the future. Rather, at this current moment, given the existing investor structure, market conditions, and liquidity environment, it has not yet achieved that status. In 2025, both Bitcoin and software stocks delivered only meager single-digit returns, while traditional hard assets performed remarkably well. In this critical test, Bitcoin and tech growth stocks exhibited highly aligned behavior—among the strongest pieces of evidence supporting the view that the two are converging.

Why is this happening? Three structural reasons

The way institutional funds operate has changed.

The emergence of Bitcoin ETFs has fundamentally changed how it is traded at the institutional level.

As a result, Bitcoin is now grouped within the same investment decision framework as software stocks. Risk management systems treat them equally, and when portfolio adjustments are needed, institutions buy and sell both asset classes simultaneously. Performance evaluations often categorize them under the broader technology stock umbrella. When a multi-asset fund determines that growth stocks carry too much risk and decides to reduce exposure, it sells both its software stocks and Bitcoin in the same transaction.

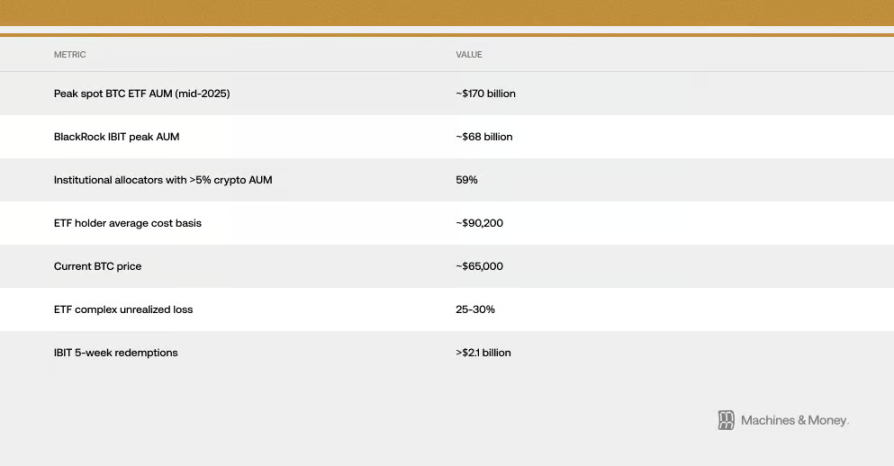

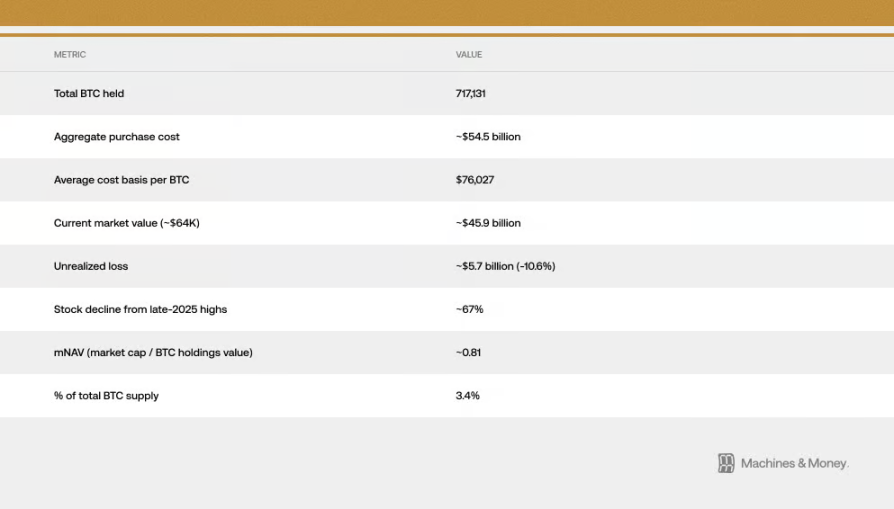

This creates a self-reinforcing cycle: because institutions classify it as a tech stock, its capital flows move in sync with tech stocks; and this synchronization, in turn, reinforces institutions’ perception of it as a tech stock. Estimates suggest that the average cost basis for U.S. spot Bitcoin ETF holders is around $90,000, meaning that with the current price near $64,000, institutional capital within these ETFs is collectively underwater by 25% to 30%. This cost gap is significant because it transforms what might have been long-term holding capital into persistent selling pressure. Those who believed buying a Bitcoin ETF would diversify risk or serve as a hedge are now watching helplessly as gold ETFs rise while their holdings continue to decline. Since early 2026, we have been able to observe in real time the chain reaction of ETF redemptions followed by Bitcoin price declines—a prolonged outflow period unmatched since the ETFs’ launch. Just BlackRock’s IBIT has seen over $2.1 billion in outflows over the past five weeks.

They are equally sensitive to the macroeconomic environment.

Bitcoin and software stocks are equally sensitive to the same macroeconomic factors: changes in real interest rates, the amount of money in the market (M2), whether the Fed is printing money or tightening liquidity, the strength of the U.S. dollar, and overall market risk appetite (as measured by the VIX fear index and credit spreads). Both are considered "long-duration" assets sensitive to interest rates. When real interest rates fall, they rise; when real interest rates rise, they fall. When money is abundant in the market, both benefit; when liquidity tightens, both suffer.

A key question is whether Bitcoin is closely tied only to software stocks or to all growth-oriented assets sensitive to liquidity. Evidence supports the latter. Bitcoin’s price movements are not driven by the profitability of software companies, but rather by the same tightening environment that has reduced valuations in software stocks—and has also withdrawn capital from speculative assets. This correlation reflects their shared sensitivity to macroeconomic conditions, not an inherent equivalence.

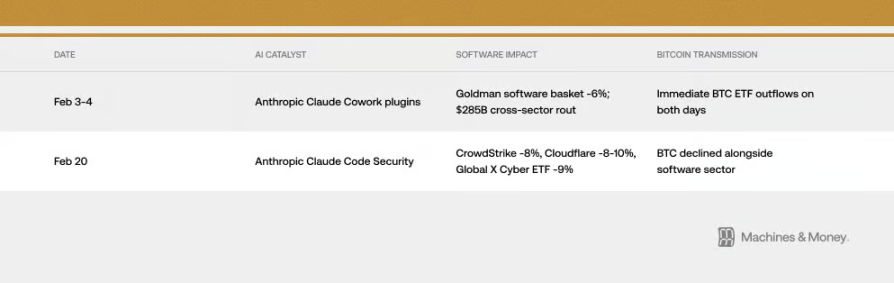

However, sometimes the transmission mechanism is surprisingly direct. In February 2026, the launch of two AI products unrelated to Bitcoin both affected Bitcoin’s price—how? Through the “institutional pipeline” mentioned above. This is how correlation manifests in reality.

The VIX fear index also provides insight. When the VIX spikes due to inflation data, both Bitcoin and software stocks tend to decline. However, when the VIX falls from low levels, neither asset benefits significantly. This behavior is entirely consistent with high-volatility growth stocks, not with safe-haven assets.

It’s important to understand this distinction. If the correlation is merely due to both being sensitive to the same macroeconomic factors, then once the macro environment shifts, Bitcoin could diverge from tech stocks—even if nothing significant happens to Bitcoin itself. This has happened before: Bitcoin moved in tandem with gold in 2017 and with tech stocks in 2021, but both correlations ended as the macro environment changed.

MicroStrategy's "amplifier" effect

Strategy (formerly MicroStrategy) is the publicly traded company with the largest holding of Bitcoin worldwide, and on the Nasdaq exchange, it is classified as a software/technology company. This creates a direct, mechanical link between the performance of the software sector and Bitcoin's "sentiment."

This cycle is bidirectional. When the software sector struggles, Strategy’s stock price falls. A decline in Strategy’s stock price further intensifies bearish sentiment toward Bitcoin in the market and can even create real selling pressure. During market downturns, this cycle strengthens the correlation between Bitcoin and the software index. Strategy’s stock price has already dropped approximately 67% from its peak at the end of 2025—far more than the declines seen in software stock ETFs or Bitcoin itself. Currently, the company’s market capitalization is even lower than the value of the Bitcoin it holds, effectively trading at a discount. This indicates that, beyond the correlation between Bitcoin and software stocks, there is an additional amplification effect driven by the company itself.

In January 2026, MSCI considered removing companies that hold more than half of their assets in digital assets from certain indices. If implemented, this could force significant selling pressure. This highlights how companies like Strategy, which hold large amounts of Bitcoin, are highly vulnerable to traditional financial regulations. Although MSCI ultimately paused this move, it stated it would revisit the issue in the future—meaning this risk remains ongoing.

How to view the future? Three possible frameworks

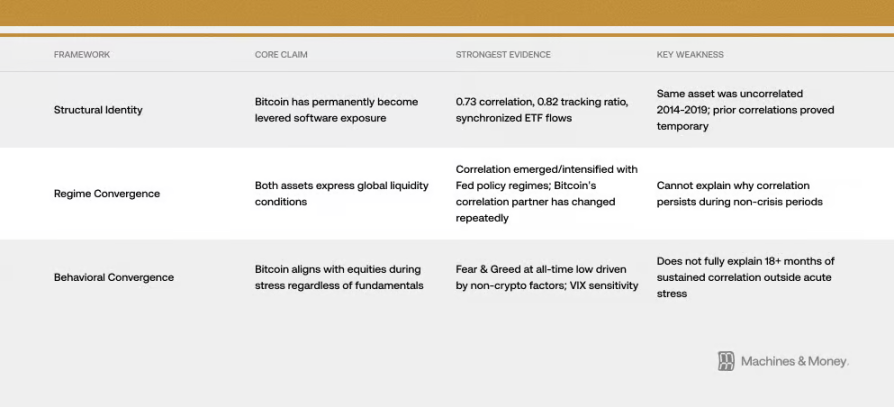

Framework One: Bitcoin has become a leveraged software stock (its identity has changed).

This perspective holds that Bitcoin has been permanently redefined. The evidence includes the aforementioned: a correlation of 0.73 with software stocks, nearly synchronized price movements, aligned ETF fund flows, and shared institutional investors. Under this framework, the ETF era has integrated Bitcoin into technology stock portfolios, permanently altering its risk profile. This correlation will persist regardless of market cycles.

The problem with this view is that history doesn’t support it. Bitcoin itself hasn’t changed, but between 2014 and 2019, its correlation with software stocks was nearly zero. There have been previous periods when it was highly correlated with other assets—such as altcoins during 2017–2018 and the Nasdaq during 2021–2022—but those correlations ultimately proved temporary. To prove permanence, we’d need to see Bitcoin survive a full interest rate hiking and cutting cycle, and we haven’t reached that point yet.

Framework Two: Both are merely reflections of whether the market has money (cyclical convergence).

This explanation is simpler: Both Bitcoin and software stocks are long-duration assets highly sensitive to liquidity. Their strong correlation is coincidental, arising from the current environment of tight liquidity. This synchronization began during the massive monetary easing in 2020, intensified as liquidity tightened in 2022, and has persisted through today’s constrained liquidity conditions.

Under this framework, once the next easing cycle begins (as the Fed resumes quantitative easing), this synchronization could be disrupted. Historically, when the Fed shifts its policy, Bitcoin tends to begin rising one to two months ahead of software stocks. Additionally, Bitcoin itself is subject to supply changes from its halving events—historical data shows that price rallies often occur 12 to 18 months after a halving—which may enable Bitcoin to chart a distinctly independent course from software stocks by the end of 2026.

Framework Three: When markets become tense, Bitcoin tends to move in tandem with stocks (behavioral convergence).

Bitcoin is fundamentally a highly volatile risk asset that, during market panic and sell-offs, behaves like stocks regardless of its intrinsic nature. At such times, either “risk-off” or “risk-on” sentiment dominates everything. When the VIX fear index spikes, both Bitcoin and stocks decline together. Sometimes, broad narratives—such as growing concerns that AI disruption could render many tech companies worthless—simultaneously impact software valuations and overall market risk appetite, further aligning their movements. On February 6 of this year, the Crypto Fear & Greed Index hit its historical low—not due to any major event within the crypto space, but because growth assets across the board were being sold off, driven by macroeconomic and technology sector concerns. Bitcoin’s most pessimistic sentiment ever was triggered by the same factors that affect software stocks.

Current evidence most supports "Framework Two" (cyclical convergence), but the mechanisms described in "Framework One"—particularly how institutional funds operate—are indeed causing this convergence to persist longer under current conditions.

What lies ahead? Several possible scenarios

To be honest, we can't yet determine which scenario will definitely occur. But we can carefully consider all possible outcomes and look for future signals that might help us rule out some of them.

Scenario One: Continued Correlation (Baseline Case). If market liquidity remains tight in 2026, Bitcoin will continue to behave like a high-volatility growth stock, maintaining a high correlation of 0.5 to 0.8 with software sector ETFs. The question of what it truly is remains unanswered. This is the most likely outcome as long as there are no major shifts in Fed policy, institutional positioning, or Bitcoin itself.

Scenario Two: Divergence. If the Federal Reserve begins to loosen monetary policy, combined with the lingering effects of the 2024 halving and reduced market concerns about AI disruption, Bitcoin could significantly outperform software stocks in the second half of 2026. Their correlation would drop to between 0.3 and 0.5. If this occurs, it would validate Framework Two (Cyclical Convergence), indicating that the current synchronization is merely temporary.

Scenario Three: Permanent Convergence. If the correlation between the two rises above 0.8 and remains elevated throughout the next full easing cycle, and major index providers officially reclassify it as part of the technology sector, it would indicate that Bitcoin’s identity has undergone a permanent transformation.

The key criterion is simple: if the correlation breaks when the Fed begins cutting rates and easing monetary policy, it indicates cyclical convergence. If they remain tightly linked despite the easing, then “identity change” becomes the primary explanation.

This question remains open until the next easing cycle in 2026–2027 provides an answer.

Conclusion

Bitcoin’s identity has never been fixed. It has always been whatever the mainstream buyers in the market believe it to be. And now, those mainstream buyers are institutional investors who treat it as a long-term asset allocation. This may change in the future, but Bitcoin’s most fundamental characteristics remain unchanged. Yet, the market prices assets based on who holds them and why—not on their original intended purpose. Until the next major shift in market conditions, this alignment is the reality. And for anyone wondering what role Bitcoin can play in their investment portfolio at this moment, reality is all that matters.