Original Author: ChandlerZ, Foresight News

Bitcoin's hash rate has increased about 10 times since 2020, but it has recently experienced a more noticeable decline in the past few months.

Data shows that the Bitcoin network's hash rate has dropped by approximately 15% from its October peak, with miners capitulating for nearly 60 days. The average network hash rate has declined from around 1.1 ZH/s in October to about 977 EH/s, indicating that miners are shutting down machines or giving up as profitability decreases.

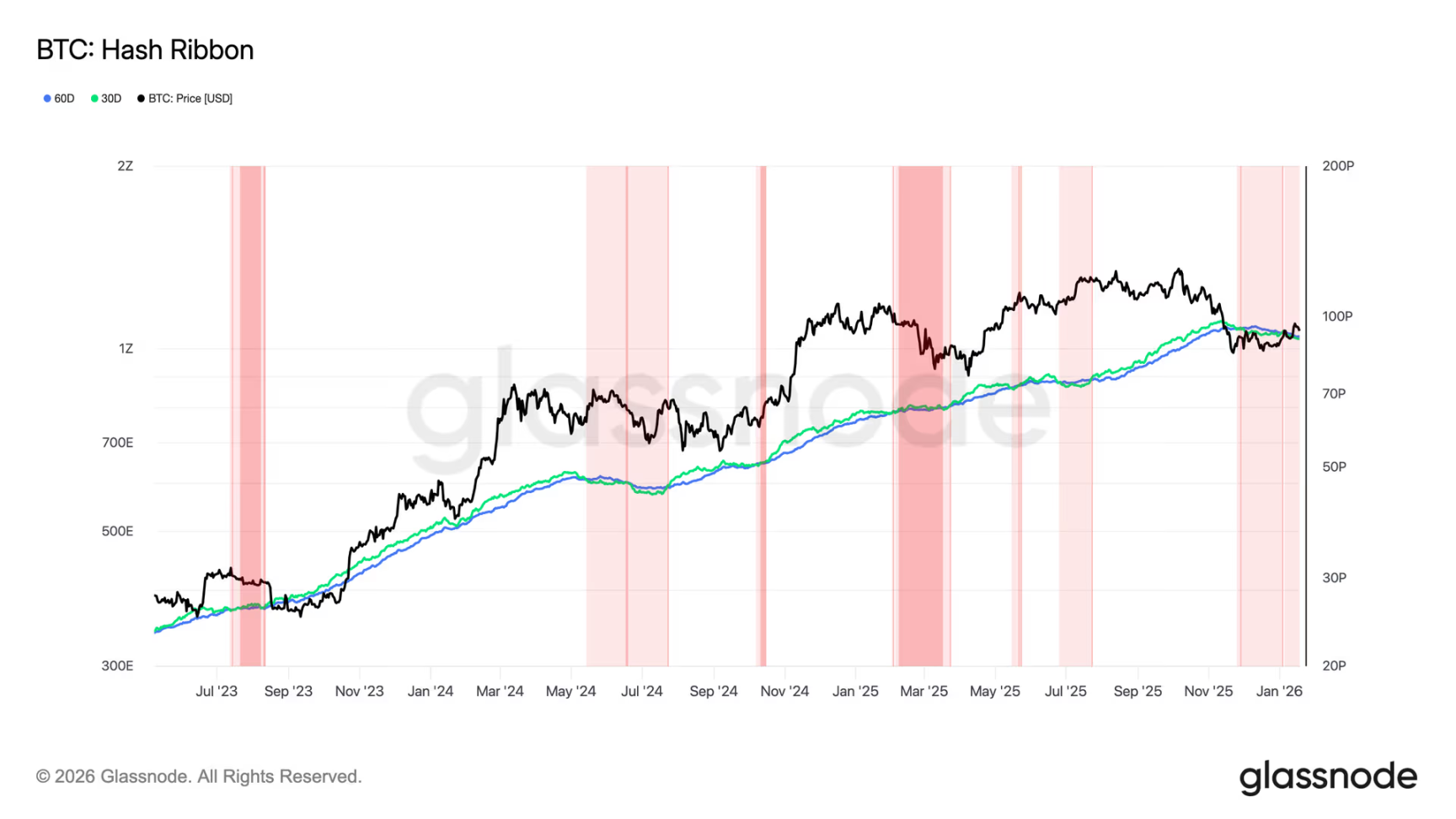

In addition, Glassnode's Hash Ribbon indicator reversed on November 29. This indicator reflects miner capitulation by tracking short-term and long-term hash rate trends. Currently, short-term supply pressure in the Bitcoin market may further increase. The Bitcoin mining difficulty is expected to decrease for the seventh time out of the past eight adjustments, dropping to around 139 T on January 22.

Mining profitability has continued to decline for five consecutive months.

JPMorgan stated that the Bitcoin network's hash rate decreased by approximately 3% to 1,045 EH/s in December 2025 compared to the previous month. Miner competition has somewhat eased, but mining profitability continues to decline.

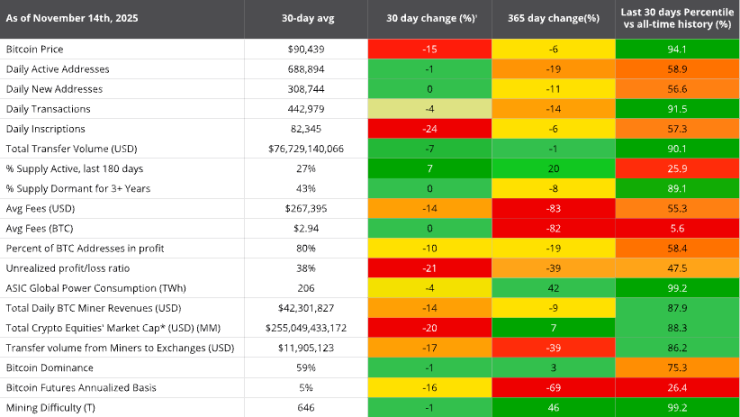

However, the data shows that in December 2025, the average daily block reward income per EH/s for miners was $38,700, a 7% decrease from November and a 32% decrease from the same period last year, reaching a historical low.

According to a VanEck report, the Bitcoin mining industry is currently experiencing significant pressure. On one hand, the periodic halving of block subsidies causes a "stepped" decline in miners' revenue. On the other hand, since 2020, the network's total hash rate has expanded at a compound annual growth rate of approximately 62%. To avoid being eliminated, miners must continuously invest in CAPEX to increase their hash power. If the price of Bitcoin cannot offset the rising unit costs caused by the reduction in subsidies and the growth in hash rate, miners' profits will be systematically compressed.

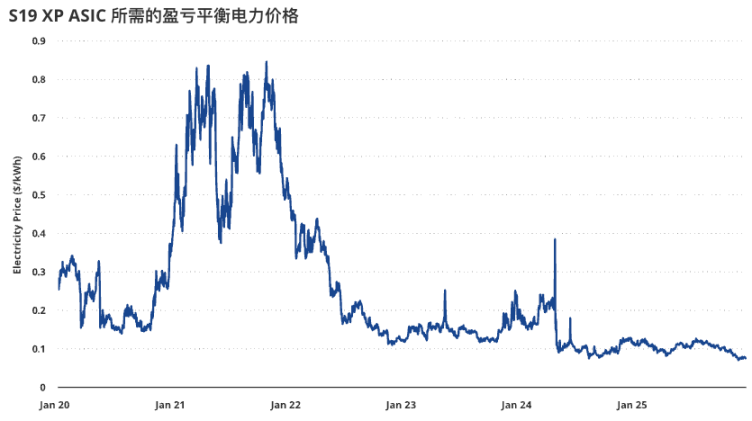

The deterioration of miners' profitability can be intuitively observed from the breakeven electricity price. Taking the 2022-generation mining machine S19 XP as an example, its breakeven electricity price has dropped from about $0.12 per kWh in December 2024 to approximately $0.077 per kWh in December 2025. This indicates that, against the backdrop of a recent weakening in BTC prices, the marginal economics of mining have significantly deteriorated. As a result, the industry's reliance on low-cost electricity, economies of scale, and operational efficiency has further increased.

Although the total network hash rate has increased by about 10 times since 2020, the 30-day moving average shows a decline of approximately 4% in the network hash rate over the past 30 days, marking the largest drop since April 2024. At the same time, supply-side disruptions are also affecting the hash rate. For example, mining operations in the Xinjiang region have shut down approximately 1.3 gigawatts (GW) of capacity under regulatory scrutiny, with an estimated 400,000 mining machines idled.

Mine Actively Transforms into an AI Data Center

According to a report by GF Securities, in the third quarter of 2025, the mining costs (including depreciation) for U.S.-listed cryptocurrency companies will rise to $112,000, exceeding the current price of Bitcoin. Cryptocurrency mining companies already have power-connected, high-bandwidth computing infrastructure located near major metropolitan areas, with electricity costs generally ranging from 3 to 5 cents per kilowatt-hour, making them naturally suitable for AI cloud service operations. With the growing demand for AI computing power, the transformation of cryptocurrency mining facilities into AI data centers is an inevitable choice.

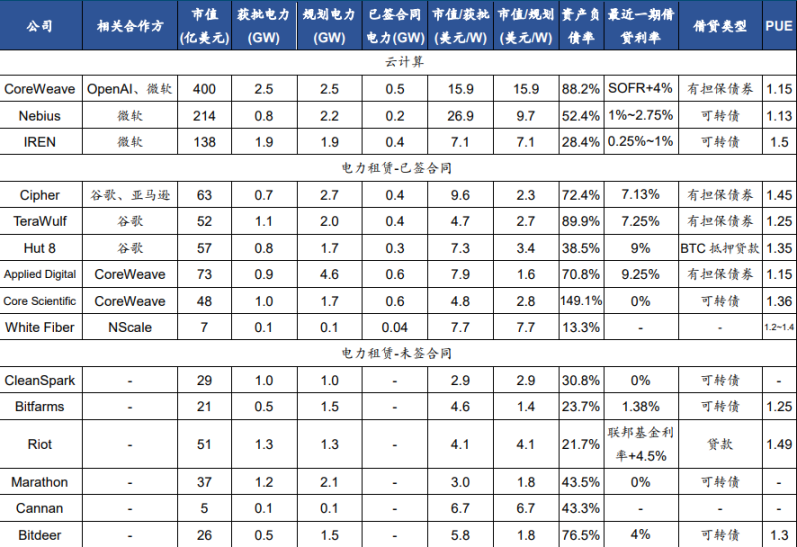

Fourteen major U.S.-listed mining companies are expected to reach an electricity capacity of 15.6 GW by 2027, with the main transition business models being cloud computing leasing and IDC (data center) power leasing.

There are mainly two business models for cryptocurrency mining farms that have been converted from AI data centers.

First, similar to CoreWeave and Nebius, they purchase chips for cloud computing leasing. Currently, IREN adopts this business model. IREN has a gross power capacity of 2.91 GW, corresponding to approximately 1.9 GW of core capacity. Its market valuation per watt is lower than that of CoreWeave and Nebius. It has already partnered with Microsoft for a 200 MW core capacity collaboration.

Second, there is a power leasing model similar to that of IDCs, where only the usage rights of the data center buildings and power capacity are rented out, while the servers and electricity costs are paid by the tenants. Currently, most cryptocurrency mining operations adopt this hosting model. Some companies have already signed lease agreements with firms like Google, Amazon, and CoreWeave, while the majority of others, having transitioned later, are still seeking partners.

VanEck: A decline in hash rate could actually be a positive factor.

However, the VanEck report also suggests that a decline in hash rate could actually be a positive factor. By comparing the 30-day Bitcoin hash rate changes with the expected returns over the following 90 days since 2014, the report found that when Bitcoin's hash rate declines, the probability of positive returns is higher than when the hash rate increases. Moreover, when the hash rate decreases, the average expected return over 180 days is about 30 basis points higher than when the hash rate increases.

When computational power compression persists for a prolonged period, positive forward returns tend to occur more frequently and with greater magnitude. Since 2014, on days when the 90-day computational power growth was negative over a total of 346 days, the probability of Bitcoin having a positive 180-day forward return was 77%, with an average return of +72%. In contrast, the probability of Bitcoin having a positive 180-day forward return was approximately 61%, with an average return of +48%.

Therefore, historically, buying BTC when the 90-day hashrate growth turns negative can increase the 180-day expected return by 2400 basis points.

Even during periods of weak economic conditions, many entities still choose to continue mining. Short-term profit pressures and fluctuations in computing power are more likely to accelerate industry consolidation and centralization, and do not necessarily indicate a long-term decline in the mining industry.