A few days ago, I came across a concept from Japanese philosophy: basho. A rough translation is “place,” but the philosopher Nishida Kitarō imbued it with meaning far beyond a physical location—it is more like a context: a field in which all things come to be themselves. In other words: people are not merely偶然 present in a place; they are shaped by the very environment they inhabit. Today, I will apply this framework to interpret Base.

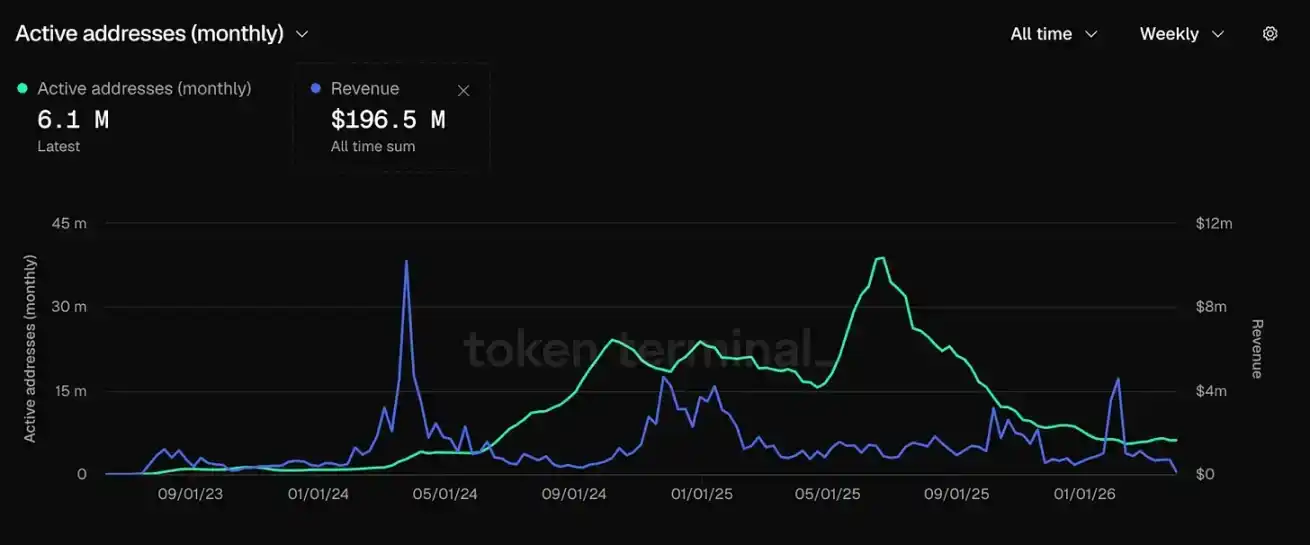

Last month, its number of active addresses dropped to a 18-month low. Reflecting on this phenomenon, I realized: Base has built only a location, but never cultivated the conditions necessary for things to grow and take shape.

When Coinbase launched Base in 2023, the crypto-native community rarely experienced a sense of belief. Many thought it could finally solve Ethereum’s oldest challenge: abundant infrastructure but no real users. With a hundred million users and unparalleled distribution capabilities, Coinbase possessed a unique advantage. The door was open, and users had already been waiting on the other side.

For a time, this confidence appeared to be validated: Base grew faster than any previous Layer 2. In October 2025, its total value locked (TVL) reached $5.6 billion, and its fee revenue surpassed all other L2s. In September 2025, Base officially announced its token issuance, as if signaling an inevitably successful experiment. Yes, a place was becoming a basho.

Then, the user left.

Viewing the data more clearly: Base’s active addresses have returned to levels seen in July 2024. The token issuance timing perfectly met the demands of airdrop hunters: collecting their final payout and then leaving.

Base’s bet on the creator economy in 2025 also failed. At its core is the Zora protocol, which automatically tokenizes content. By year-end, 6.52 million creator and content tokens had been issued on Base via Zora, but only 17,800 remained actively active throughout the year, accounting for just 0.3%. The remaining 99.7% were completely abandoned.

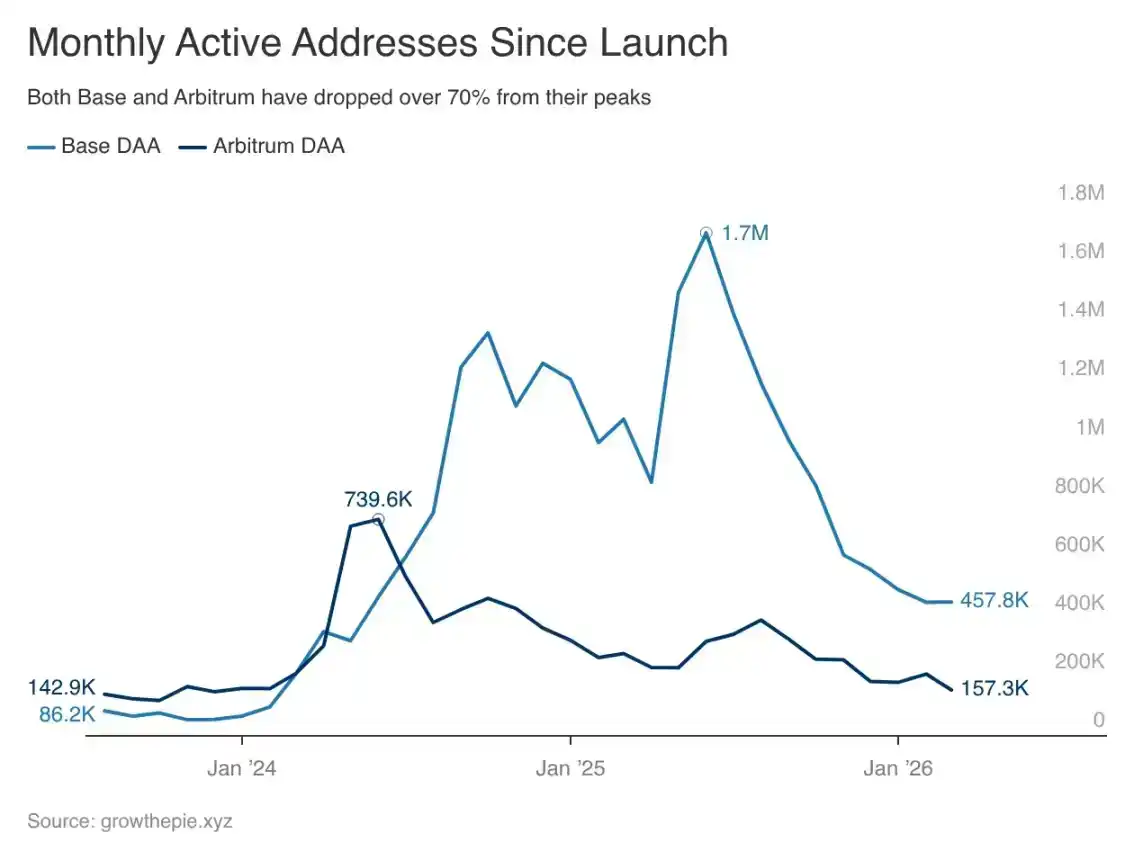

Base's daily active addresses peaked at 1.72 million in June 2025. By March 2026, they had dropped to just 458,000, a 73% decline from the peak. Within just six months after Armstrong announced in September 2025 that Base was considering issuing a token, active addresses fell by 54%, indicating that speculative capital had completely exited.

Sociologist Ray Oldenburg studied what causes people to return repeatedly to a place without financial incentive. He called these “third places,” such as bars, barbershops, and city squares. They are not spaces designed for efficient production, yet they offer a reason to return that has nothing to do with external motivation. The core insight is that the desire to return cannot be artificially manufactured—it can only grow naturally from the possibilities a place consistently offers over time. The cryptocurrency industry designs spaces to extract value from users, yet wonders why no one stays.

This is a place without a basho: people pass through, take what they need, and leave, because leaving costs nothing. Here, no identity is formed, no capability is established that cannot be replicated elsewhere within three weeks, and nothing makes leaving a loss. Are there unique relationships on this chain? We’ve never built things with this mindset, have we?

You cannot build a basho through financial incentives alone. Incentives may bring people in, but they won’t make them want to stay. The desire to stay must arise from the long-term possibilities nurtured by the place itself. Nishida Kitaro called this the “logic of place,” referring to how relational fields shape what emerges within them. The crypto industry designed a field for extraction—and was surprised to find that only extraction emerged.

Brian Armstrong publicly stated that the Base App is now focused on becoming Coinbase’s self-custody, trading version.

The vision of building social engagement and enabling users to establish meaningful on-chain identities as creators and social participants has vanished. Data shows this was a rational decision, yet it also acknowledges that this vision never truly took shape. Base has a place—it now focuses solely on serving its existing users, because that’s all it can offer.

One chain, one赛道

Base is the most prominent embodiment of the entire L2 model.

Since June 2025, overall usage of mid- and small-sized L2s has declined by 61%. Most chains outside the top three have become zombie chains: active enough to avoid shutdown, but too dormant to matter. The ratio of daily active users on L2s versus L1s has dropped from 15x in mid-2024 to just 10–11x today. Most new L2s have seen usage collapse immediately after their incentive periods end. The entire L2 ecosystem is cooling down—not just Base.

The rollup-centric roadmap was once a theory about user adoption: lowering participation costs → user influx → ecosystem formation → compounding growth. This year, the Ethereum Foundation released a 38-page vision document outlining Ethereum’s future direction. Meanwhile, the largest L2’s activity hit a bottom and departed from the OP Stack, while the second-largest L2 has seen stagnant growth.

Lowering the entry cost does not create the conditions necessary for something to take shape. The industry has solved the "entry" problem but assumes that "belonging" will automatically follow. It does not arise on its own, because belonging is not a feature that can be launched.

Farcaster is the closest thing the crypto world has come to building a basho. Because a specific group of people has cultivated a distinct culture on it: developers share their work, discuss Ethereum, and form opinions about one another over months. This takes time—competitors cannot replicate it with higher rewards. Friend.tech tried to do the same with incentives, rising to the top in a week and fading away in a month. The same mechanism, yet no culture emerged. The difference isn’t in the product, but in whether people stayed long enough for something real to take shape.

What keeps people engaged?

The chain that retains users through the winter doesn't rely on more generous incentives.

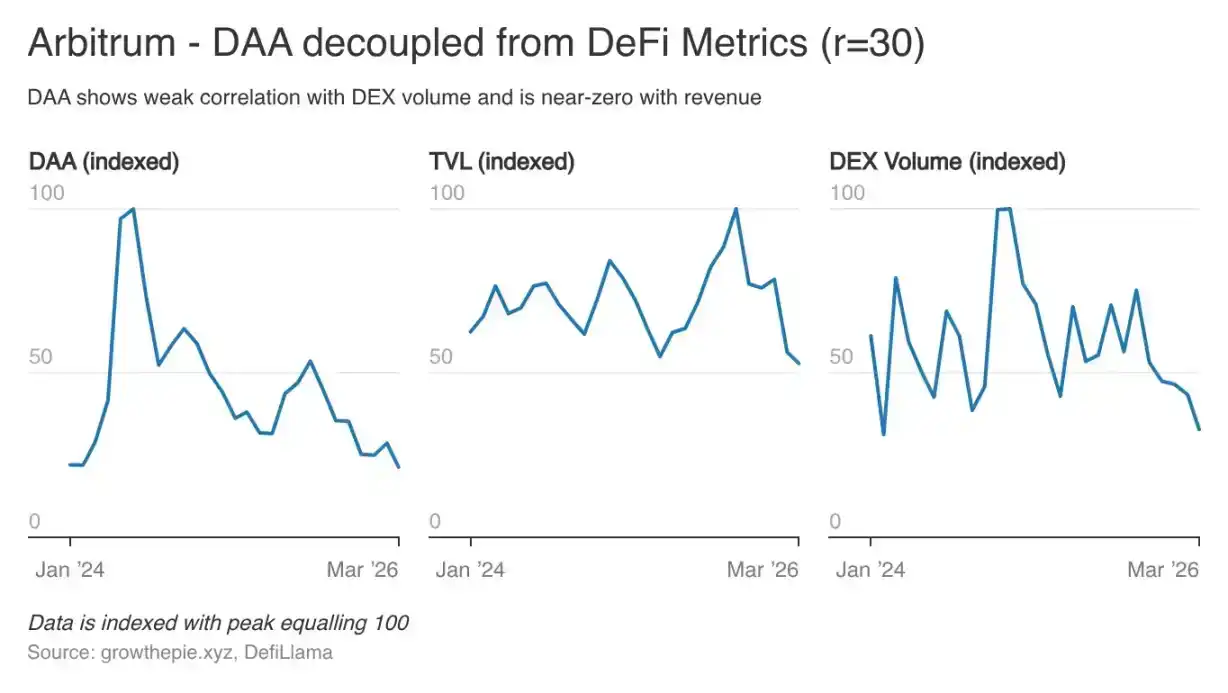

Arbitrum's daily active addresses peaked at 740,000 in June 2024 and have now dropped to 157,000, a decline of 79%. Both chains are declining, but their underlying fundamentals are entirely different.

Users on Base come to trade, and they leave when trading volume declines. In contrast, Arbitrum’s users are unaffected by fee levels, with almost zero correlation between user count and fee revenue. Base attracts tourists, while Arbitrum somehow retains its users.

Hyperliquid has held its ground because its trading experience is unique, and the community has developed an identity nowhere else found. Token incentives are almost irrelevant—being part of it has become an integral part of their behavior and identity. Things shape users, and users, in turn, shape things.

The crypto industry is still optimizing "how to attract people," while the question of "how to create the right conditions" is only remembered after data crashes—and has never been considered from the outset of chain design.

I believe Base has the strongest distribution capability in history and could have solved this problem better than any other chain.

Today, it is a trading app. This is a reasonable product direction, but it’s also what more than 40 other products are already doing. Trading apps cannot create a “basho”—they only generate sessions: users come in when they have a trading need and leave once it’s completed.

To truly become a successful app, you need to build an ongoing connection. Users must develop a relationship between visits, so that each return feels like coming home, not just arriving.

Armstrong’s transformation is largely based on the lessons Base learned from its data. Features like the social layer, creator economy, and on-chain identity—things meant to turn Base from “used” into “inhabited”—require patience, but the system did not reward patience.

The Ethereum ecosystem needs Base to be more than just a trading venue. The entire L2 narrative is grounded in the idea that blockchains can become infrastructure around which people build their lives. If the L2 with the strongest distribution capability in crypto history ultimately settles for being just a faster Coinbase, then the entire narrative falls apart.

Nishida Kitaro believed that the deepest "basho" is where the boundary between self and place begins to dissolve. You cannot fully separate "who you are" from "where you have been shaped." This may sound abstract, but on a public blockchain, it means: a user cannot imagine their financial life beyond a specific chain; a developer’s entire toolkit is built around a particular ecosystem; and their identity barely exists elsewhere.

As far as I know, something like this has never been built on any L2. It may not even be possible to build under the incentive program.

Even if you have 100 million potential users, if you don’t have anything worth keeping, you’ll ultimately be left with an empty building. Base now understands.