Article by KarenZ, Foresight News

In Silicon Valley, Naval Ravikant’s name is itself a form of credibility.

He is a co-founder of AngelList and one of the most prominent early investors over the past decade, having backed companies such as Uber, Twitter, and Notion. Now, in the new fund, USVC Venture Capital Access Fund (USVC), Naval is not merely making a symbolic appearance. According to the supplemental disclosure filing for April 2026, he serves as Chair of the Investment Committee, overseeing portfolio construction and strategy.

This structure is important because USVC is not just selling the concept of a "low-entry fund." It is truly attempting to package and offer a capability that was previously accessible only to a select few: earlier access to private growth companies.

On the surface, USVC might seem like a "venture fund for retail investors." But when you look at the website, prospectus, and portfolio pages together, AngelList’s core message becomes clearer and more pointed: today’s most imaginative companies are going public later than ever; IPOs are increasingly becoming an exit point rather than an entry point; and ordinary investors aren’t just being shut out by risk—they’re being excluded from the most lucrative phase of growth.

The significance of USVC lies in its aim to pry open this door just a little.

The core of USVC is not selling funds, but selling access rights prior to listing.

The USVC homepage states the issue plainly: the next wave of growth is happening in the private market. The site also provides a striking comparative statistic: in 1980, the median age of U.S. companies at IPO was six years; today, it has risen to thirteen years. Those additional seven years mean that a significant amount of value creation is occurring outside the public markets.

This is precisely the core product logic of USVC. The USVC prospectus states that USVC primarily invests in VC funds, SPVs, and private growth-oriented companies. The most easily overlooked but most critical term here is "private growth-oriented companies." The document defines it directly: companies that the investment advisor believes possess significant growth potential at the time of investment.

In other words, USVC’s value proposition is not the abstract notion of “allocating to venture capital,” but rather bringing ordinary investors face-to-face with the most attractive segment of assets in the primary market. What it aims to offer is a channel to access privately held growth companies.

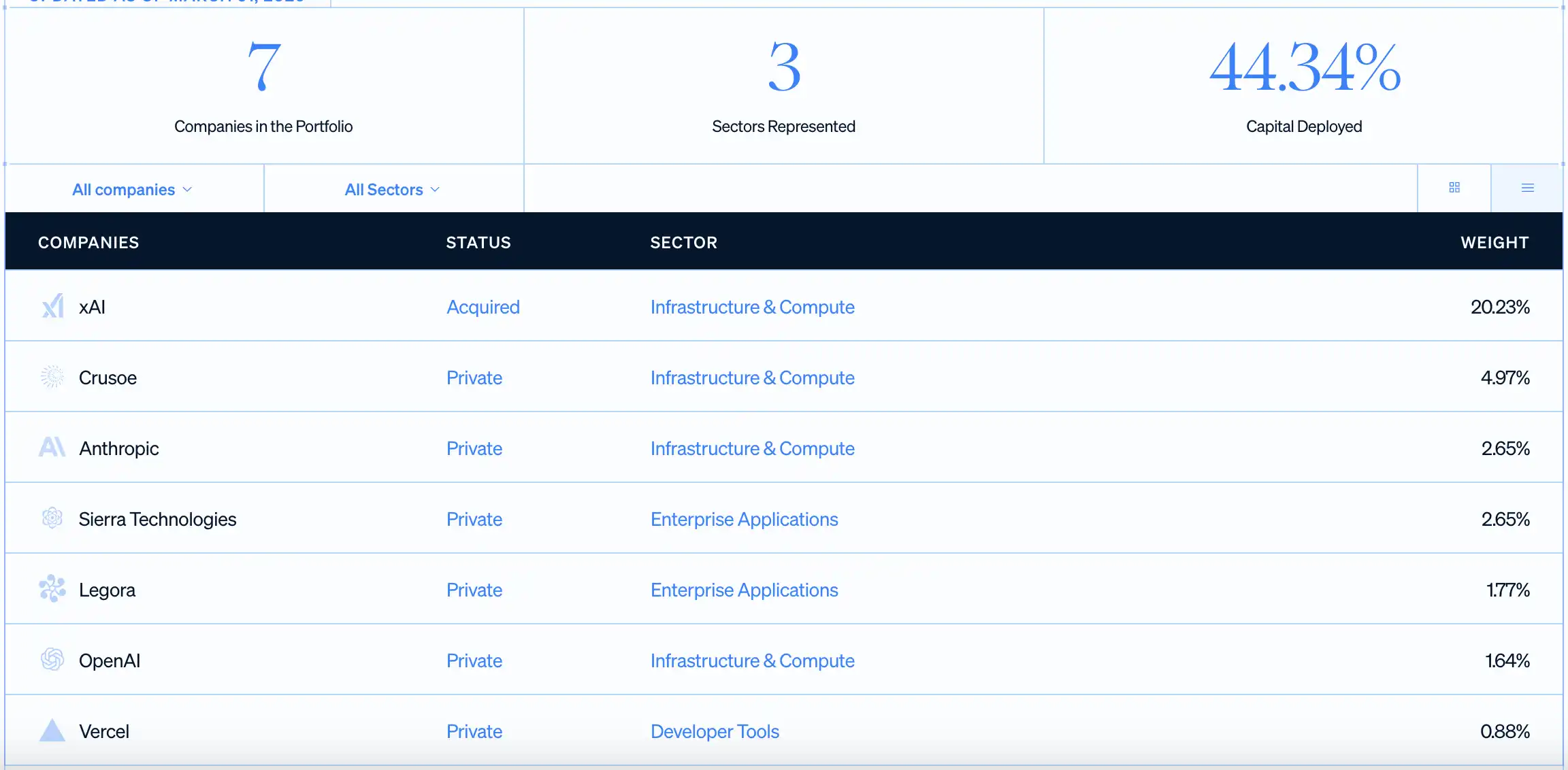

This is why it consistently highlights names like OpenAI, Anthropic, xAI, and Vercel. The portfolio page on the website shows that, as of March 31, 2026, USVC has deployed 44.34% of its capital across seven companies, with its largest single position being xAI, followed by Crusoe, Anthropic, Sierra, Legora, OpenAI, and Vercel. Regardless of how these positions ultimately perform, AngelList has made its message clear to investors: you used to only see these companies in the news—now, through this fund, you can gain exposure to them before they go public.

For retail investors, this appeal is very strong, as under traditional pathways, they typically only get the chance to buy in after a company’s IPO—by which time the earliest and most dramatic growth has likely already been captured by founders, employees, early-stage funds, and institutional shareholders.

Legally, this fund is a closed-end management investment company registered under the U.S. Investment Company Act of 1940. It was originally established on April 8, 2021, and converted to a Delaware statutory trust on August 7, 2025, and is currently raising capital through continuous offerings. The minimum initial investment is $500, with no minimum limit for subsequent contributions, and the official website even supports monthly automated investments.

This packaging is clever. On one hand, it preserves the core appeal of private markets—pre-IPO growth companies; on the other, it makes the purchasing process feel like a retail financial product. U.S. users don’t need to become accredited investors first, don’t need to enter the high-net-worth circle, and don’t have to deal with the complex tax reporting typically associated with traditional private funds—at least when it comes to the purchase entry point, AngelList aims to make it appear simple.

Being able to access private companies doesn't mean this is a simple investment.

Precisely because the USVC narrative is so compelling, what truly needs to be clearly articulated are the constraints behind it.

First, investors purchase only a fund share. The fund indirectly or directly holds these unlisted growth companies through venture capital funds, SPVs, and direct investments. In other words, investors gain exposure to unlisted growth companies, rather than the clear, readily liquidable ownership experience associated with buying stocks.

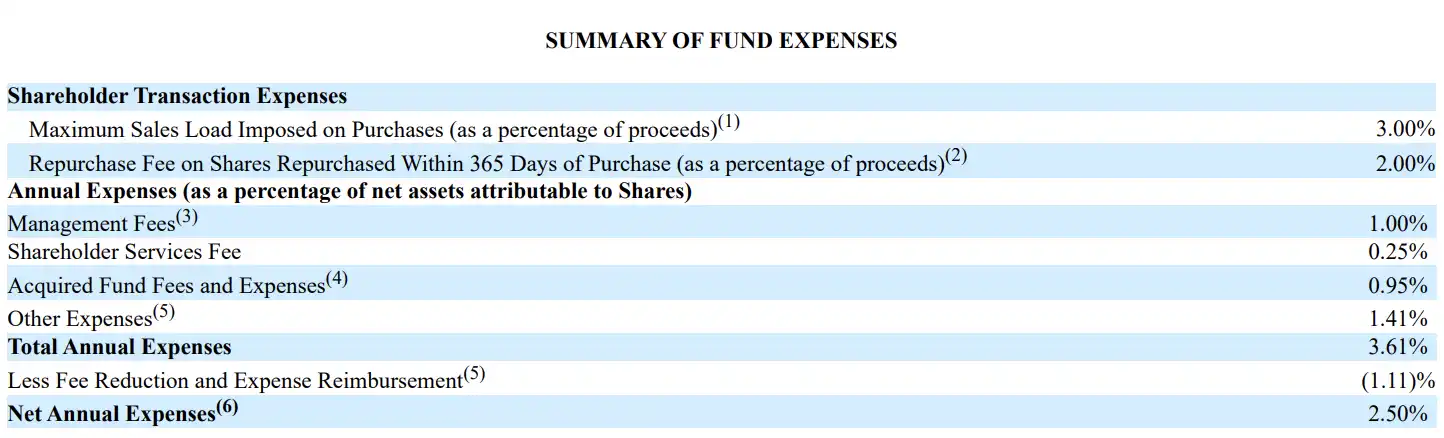

Second, this exposure comes with costs, and they are not insignificant. The fee table on page 20 of the prospectus shows that USVC has a management fee of 1.00%, a shareholder service fee of 0.25%, underlying fund fees and expenses of 0.95%, other expenses of 1.41%, and a total annual expense ratio of 3.61%. After fee waivers—expected to last at least until October 29, 2026—the net annual expense ratio is 2.50%. After accounting for the underlying VC vehicles and operational costs, investors are faced with a product whose current net expense ratio is not low.

Third, this fund does not provide retail investors with a truly liquid exit pathway. USVC is not listed on any exchange and has no public trading market; liquidity depends primarily on whether the board initiates quarterly repurchases, which typically do not exceed 5% of net asset value. The offering documents originally included a 2% repurchase fee for holdings under one year, but the board has since decided to waive this fee (subject to modification or termination). This adds a modest degree of flexibility compared to traditional VC funds, but it remains far from “entering or exiting at any time.”

Fourth, USVC does not have a fixed expiration or liquidation date like traditional 10+2 year venture capital funds, but it is still a long-term closed-end structure without a defined maturity. The realization of value from the underlying assets still depends on whether liquidity events such as IPOs, mergers and acquisitions, or private secondary transactions occur. The prospectus also explicitly notes that many portfolio investments may take several years to appreciate in value.

Even after an investment company goes public, it is often subject to lock-up restrictions, with a typical lock-up period of 180 days. During this time, the fund itself, or the underlying VC/SPV managers invested in by the fund, may not be able to sell immediately.

Why is the Web3 community paying attention to this fund?

USVC has attracted additional attention from the Web3 community due to Naval and AngelList's sustained involvement in the cryptocurrency industry over the past several years.

Naval was one of the earliest and most vocal investors in Silicon Valley to support cryptocurrency and the Web3 narrative. In 2017, during an interview with Laura Shin, he stated that his focus had already shifted significantly toward crypto; by 2021, he engaged in an in-depth discussion with a16z partner Chris Dixon on Tim Ferriss’s podcast, systematically exploring Web3, NFTs, and digital ownership.

At the platform level, AngelList has never treated Crypto as a peripheral business; since 2022, it has supported investors in making investments on its platform using USDC. AngelList’s website currently features a dedicated Crypto Solutions page, clearly stating its partnership with CoinList to support Crypto SPVs and related fund vehicles.

Meanwhile, an increasing number of cryptocurrency exchanges and Web3 projects are accelerating the launch of Pre-IPO products. USVC represents a slow-moving variable within the traditional system, while most products in Web3 Pre-IPO represent fast-moving variables driven by efficiency and are typically redeemable at any time.

Two worlds, once speaking different languages, are now competing for the same investors, the same narrative, and the same anxiety: if great companies are going public later and later, can ordinary people still get a share before the IPO?

Naval’s name can open that door. AngelList’s platform network can bring private companies closer. But the world beyond the door hasn’t become any easier.