Author: David, Shenchao TechFlow

When Silicon Valley VCs finally allow ordinary people to join the table, it usually means one thing.

The game is almost over.

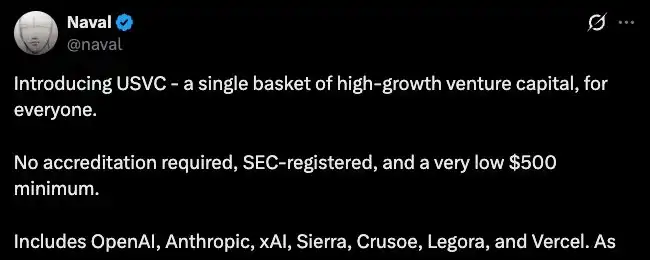

Yesterday, AngelList launched a fund product called USVC. AngelList is Silicon Valley’s largest venture capital infrastructure platform and, according to its website, manages over $125 billion in assets and has served more than 25,000 funds.

It now opens the door to all U.S. investors, allowing them to directly hold shares in seven AI companies—including OpenAI, Anthropic, and xAI—with a minimum investment of $500, without requiring accredited investor status.

Naval, co-founder of AngelList, endorses this product. Through his book "The Almanack of Naval Ravikant," he has become one of the rare figures in Silicon Valley with both a proven investment track record and significant public influence.

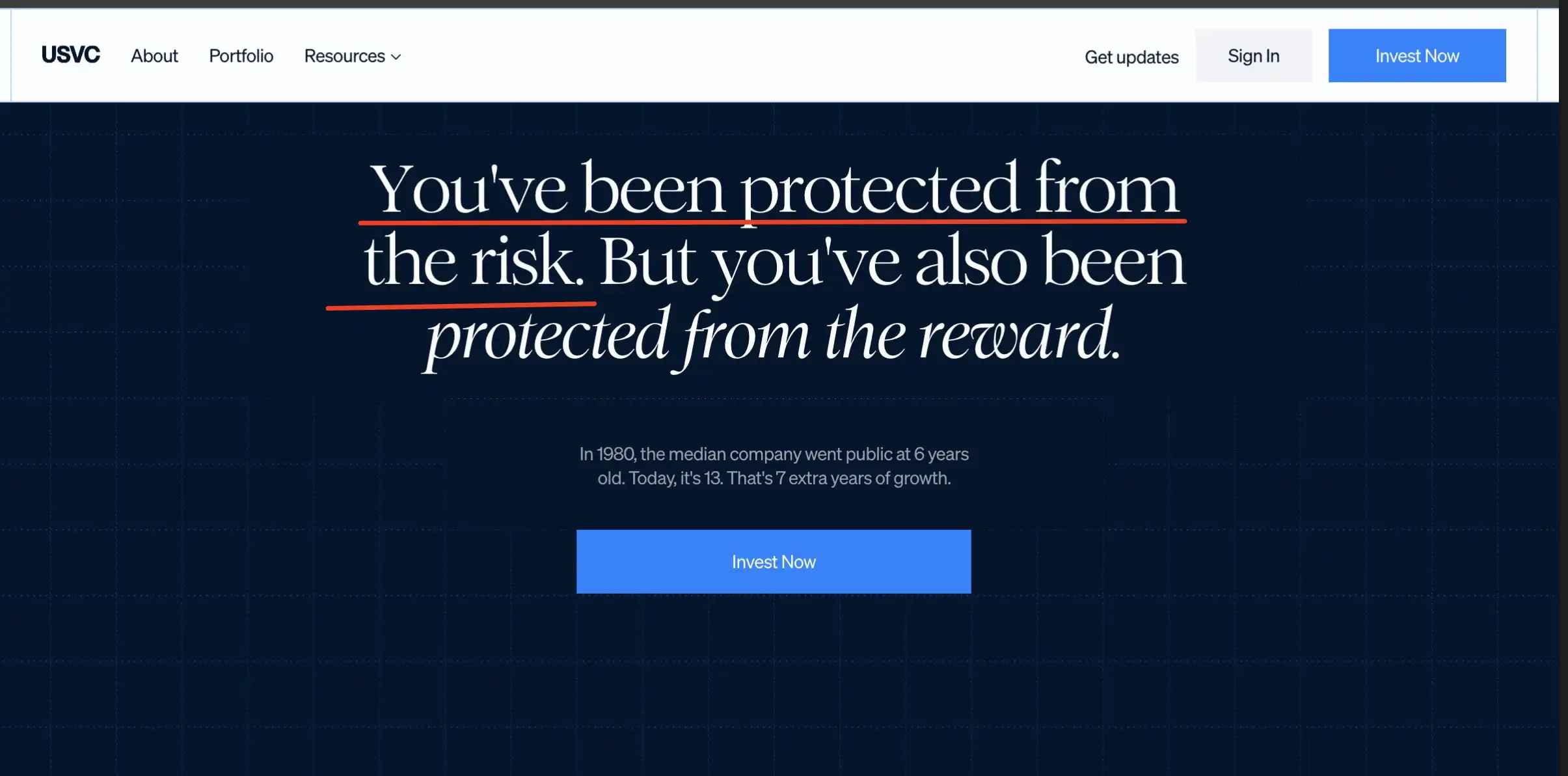

He posted a long article on X promoting USVC, arguing that early-stage tech investing is the "venture capital" of this era, but ordinary people have always been shut out—by the time some groundbreaking AI companies go public, the growth is already over. USVC aims to open that door.

Within hours of the tweet being posted, comments already included a question that made the atmosphere less pleasant:

The valuations of these tech companies have been pushed to astronomical levels; all the explosive growth has occurred in the primary market. Now, inviting retail investors to participate—what’s the difference from seeking an exit for liquidity?

USVC holds stakes in seven companies, with the largest position in xAI. According to Decrypt, as of the end of March, approximately 44% of USVC’s funds had been allocated to these seven companies.

However, none of these companies are publicly traded—so where did the shares come from?

According to the prospectus, USVC has three ways to acquire underlying assets: investing in emerging fund managers, participating in growth-stage financing rounds of companies, and purchasing secondary shares through AngelList’s network.

The first two are easy to understand; the third is the key point.

Secondary shares mean that the company has not issued new shares to you; instead, existing shareholders are transferring their shares to you. Who is transferring? Early-stage angel investors, VC funds, and early employees.

These individuals may have joined the company when it was valued at tens of millions of dollars, and now that the company is worth tens or even hundreds of billions, they want to turn their paper gains into real cash before the IPO. However, unlike stock exchanges, the primary market doesn’t have ready buyers lined up to take over.

USVC perfectly solves this problem by raising funds from retail investors and using those funds to purchase shares from insiders looking to exit.

AngelList indeed has a natural advantage in doing this. According to its official website, the platform hosts over 4,500 active fund managers managing more than 25,000 funds and investing in over 13,000 startups.

A large volume of sellers and selling shares flow through this network, with AngelList positioned right at the center. This is precisely what USVC repeatedly emphasizes as the "exclusive channel."

The channel is indeed exclusive, but the trading direction does not appear to favor retail investors.

In this transaction, the seller entered when the company was valued at tens of millions, while the buyer entered when the company was valued at hundreds of billions. The seller locked in returns of tens or even hundreds of times their initial investment, while the buyer is betting that these already fully priced companies can still rise further.

Meanwhile, the terms received by retail investors also reveal certain issues.

According to the USVC prospectus, the fund is not listed on any exchange and no secondary market is expected to exist. The fund may repurchase up to 5% of net asset value per quarter, entirely at the discretion of the board, with no guarantees provided. Additionally, the estimated annualized total expense ratio is 3.61%, significantly higher than the 1% management fee prominently displayed on the promotional page; the difference arises from layered fees of underlying funds.

You cannot sell, and exiting requires waiting in line—annual fees alone consume nearly 4% of your principal. For a product with a $500 minimum investment aimed at everyday people, this cost is not low.

So, the complete picture might look like this.

On one side, insiders looking to exit received liquidity and locked in their profits. On the other, new retail investors received shares that cannot be traded, require waiting in line to exit, and carry actual fees far higher than advertised. The direction of capital has always been the same: from later entrants to earlier ones.

The stock version of "low circulating supply, high FDV"

Breaking down the USVC model, insiders accumulate positions at low valuations; once asset prices rise, they create a channel accessible to retail investors, allowing later entrants' capital to absorb the exits of early participants.

This logic has already been fully practiced by the crypto industry between 2021 and 2024.

During those years, VC-backed token projects followed a standard template: seed round valuations in the millions of dollars, private rounds rising to tens of millions, and fully diluted valuations soaring to billions—or even tens of billions—by the time the token launched on exchanges. However, only 2% to 5% of the total supply was released into circulation, with the remainder locked up in the hands of VCs and the team, to be gradually unlocked according to a schedule.

Low circulating supply, high FDV.

What USVC is doing is essentially the same as low circulating supply with high FDV. Insiders entered when the company was valued at tens of millions, and after the company’s valuation rose to hundreds of billions, they transferred their stakes through a product aimed at retail investors.

Naval’s own journey is also fascinating. In October last year, he tweeted on X: “Bitcoin is insurance against fiat currency; Zcash is insurance against Bitcoin.” This tweet caused ZEC to surge over 100% within a week. Shortly after, the community uncovered that, according to public reports, Naval had invested $715,000 in Zcash’s development company as early as 2015 and had even served on the board of the Zcash Foundation.

The community's conclusion is simple: he is using his personal influence to promote his early investments. However, Naval has not responded to these concerns.

From Zcash to USVC, the pattern remains unchanged: celebrities leverage their credibility to create demand and direct that demand toward assets in which they hold positions.

Of course, there also appears to be no illegal activity in the USVC matter.

USVC is a registered fund, and the risk disclosures in the prospectus are comprehensive; Zcash's tweet does not constitute investment advice.

But there is always a gray area between what is legal and what is reasonable. A platform managing a trillion-dollar venture network raises retail funds with the narrative of "letting ordinary people invest in the future," then uses those funds to buy out insiders from within its own network who wish to exit...

All aspects of this matter are compliant. However, when combined, they can easily trigger painful memories for merchants.

On the same day USVC launched, Robinhood also announced that its fund had invested $75 million in OpenAI, making the opportunity available to retail investors as well. In the same week, both companies did the same thing: using their networks of retail investors to create an exit pathway for insiders in the primary market.

Each time the financial industry suddenly begins to care about ordinary people's investment rights, it is not because ordinary people's circumstances have improved, but because insiders' exit routes have narrowed.

Just as the crypto industry opened its doors to retail investors in 2021, so too will Silicon Valley do so in 2026. The timing of when the door opens is never decided by those who wish to enter.

For the average person, there’s a simple way to tell if an investment opportunity is meant for you.

Look at the people who entered before you—are they adding to their positions or selling? If they’re selling and you’re being encouraged to buy, you need to ask yourself: are you bringing capital, or just liquidity?