Author: Alex Xu

I'm not optimistic about buying Ethereum at its current price, not because I don't believe in its business development (I think there will still be growth in terms of long-term user scale and settlement transaction volume), but because its price is too high relative to its fundamentals.

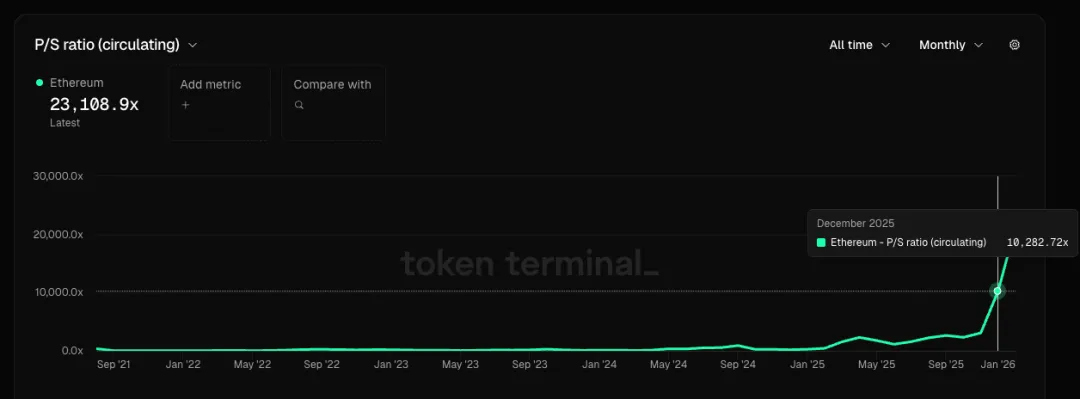

From a few images, we can create a profile of the current Ethereum:

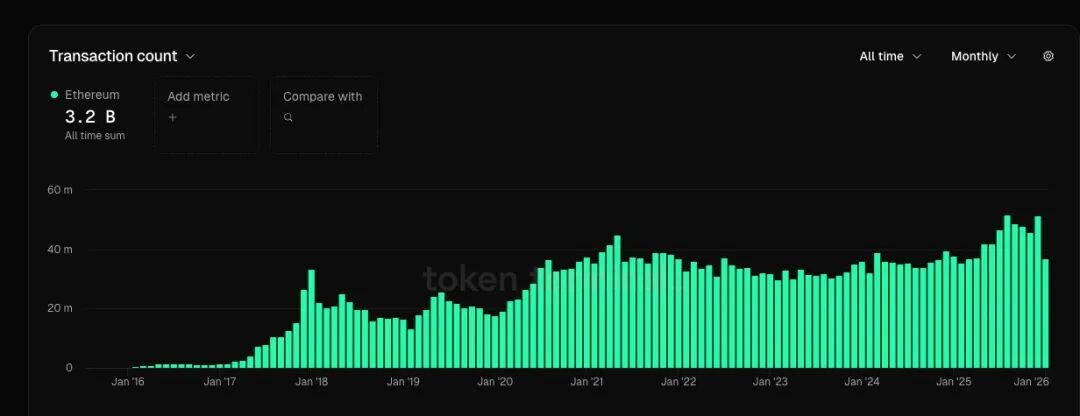

1. The number of active users has surged in a wave-like pattern to a new record (44% higher than the previous peak in the cycle), and the number of transactions has also reached a new high (13% higher than the previous peak in the cycle). However, the growth rates of these two metrics are still lower than the GMV growth rates of some leading e-commerce platforms.

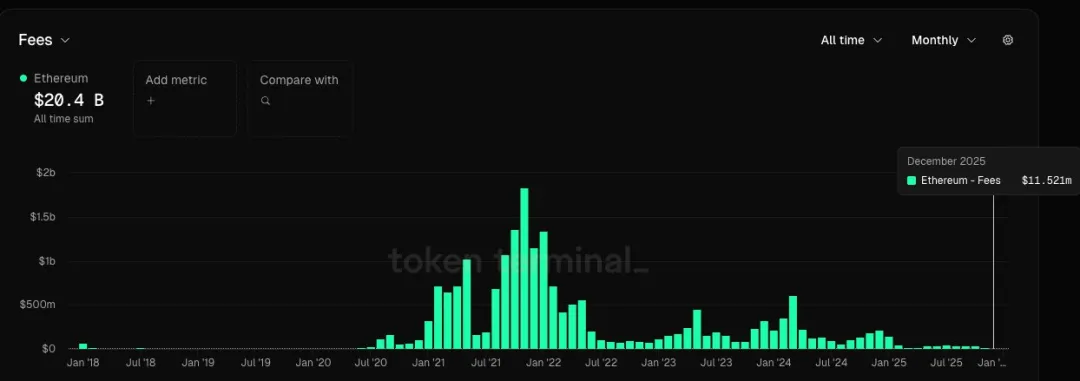

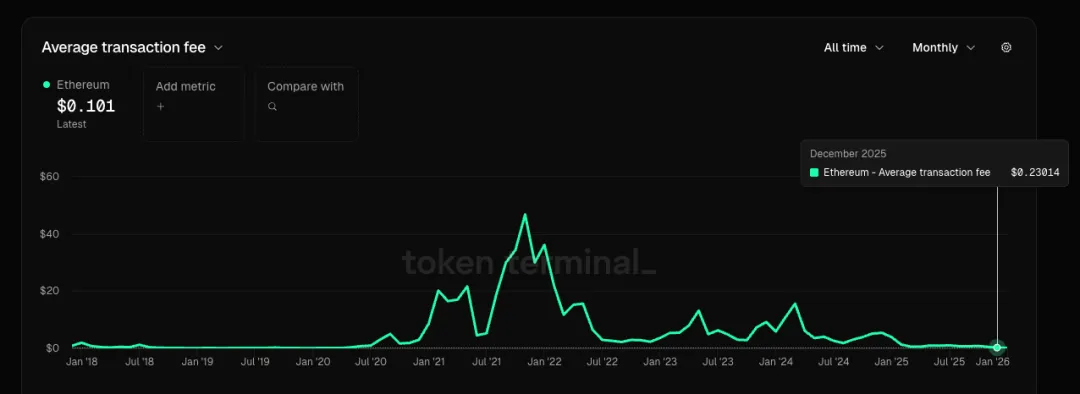

2. Currently, the monthly fee is only 0.6% of the peak level in the previous cycle, and the average transaction fee per trade is merely 0.5% of the previous peak. This means that the slow growth in its user base and transaction volume has been achieved at the cost of a sharp decline in service pricing. When the cost of growth is a drastic reduction in product and service prices, this is not a positive sign for companies in any industry.

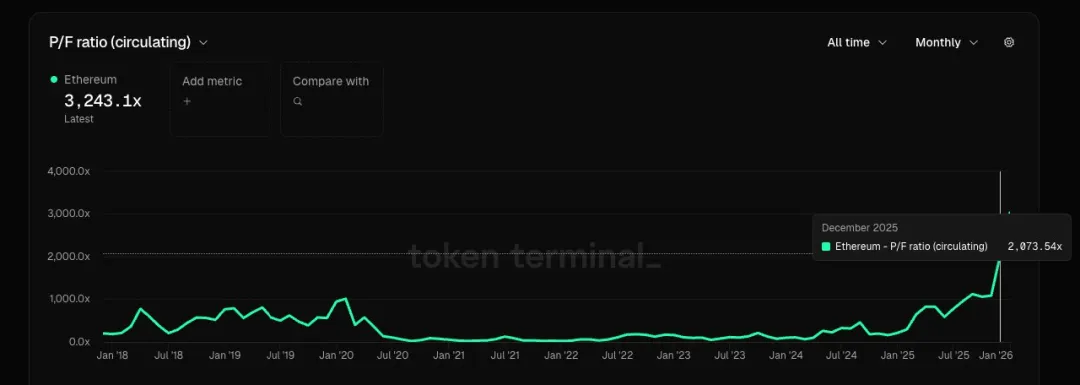

3. If we consider Ethereum as a company providing block space services, based on December data, its price-to-fee ratio (PF) exceeds 2000 times, and its price-to-sales ratio (PS) exceeds 10,000 times. Since its net profit is negative, the price-to-earnings ratio (PE) does not exist. In contrast, the typical price-to-earnings ratio (PE) for conventional cloud service companies ranges from 20 to 30, while their price-to-sales ratios (PS) are usually in single digits.

4. If Ethereum is considered not as a company but as a commodity (similar to digital crude oil), the challenge lies in the fact that other public blockchains and rollups can also offer similar block space services (like interchangeable crude oil). Some might argue that Ethereum's stronger decentralization and censorship resistance should make it more valuable as a commodity, but is it really worth that much more? Moreover, the previous wave of enthusiasm claiming that ETH could replace BTC as a store of value has almost completely faded, as the community has largely reached a consensus: compared to BTC's role as "digital gold," ETH is more akin to a technology company plus a specialized cloud service provider, and thus its commodity-like positioning is more substitutable.

5. Native applications with PMF (Product-Market Fit) are almost missing in this cycle, and few high-value applications have emerged. Insufficient demand and increased supply (continued growth in the number of rollups and public blockchains) have led to a severe oversupply of block space, causing the public blockchain sector itself to experience weak growth or even contraction.

6. Regarding the grand vision painted by Tom Lee and some domestic venture capitalists—that "Ethereum is the Wall Street of the blockchain, and in the future, everything will be built on Ethereum"—I believe there is currently a lack of data and sufficient factual evidence to support this narrative. It lacks concrete logical reasoning and seems more like a sales pitch. Our investment decisions should be based on rationality rather than faith. I'm not interested in their pie-in-the-sky promises right now. If in the future data and facts gradually support this story, I can always reconsider eating it later.