Author: David, Shenchao TechFlow

At the start of 2026, AI frightened the capital markets.

It's not that AI isn't capable—it's that AI is too capable. Every time a new product is launched, a whole industry's stocks crash.

For example, throughout February, Anthropic, Claude’s parent company, rolled out four major updates to its AI products. When AI could automate enterprise workflows, SaaS stocks crashed; when AI could automatically scan for code vulnerabilities, cybersecurity stocks plummeted; when AI could help banks rewrite legacy code from the last century, IBM plunged 13% in a single day, losing $31 billion in market value—the largest single-day loss since the 2000 dot-com bubble.

One month, several industries, named one by one.

Fear is contagious.

Duolingo, an online education platform, saw its stock price fall from a historical high of $544 in May last year to below $85 by the end of February this year, erasing more than 80% of its value. The iShares Software ETF is down 22% year-to-date and 30% from its peak...

Traders told Bloomberg that software stocks have been under selling pressure, with a media headline claiming “AI will disrupt XX” triggering a mini flash crash.

Money has flowed out of these companies, but it has to go somewhere.

Following AI investments is one path—for example, buying NVIDIA, computing power, or infrastructure—but this path is already crowded and becoming increasingly expensive.

Someone began to wonder about another question: Is there a type of company that no matter how AI evolves, it can never be killed?

HALO, firing the first shot against AI anxiety

In early February, a person named Josh Brown wrote an article on his blog.

This person is the CEO of a U.S. asset management firm and a regular guest on CNBC, essentially a finance influencer. In his article, he coined a term:

HALO.

Heavy Assets, Low Obsolescence.

It's simple: buy companies that AI can't replace, no matter how it evolves.

This guy also provided a simple way to identify them: the criterion for a HALO stock is just one thing—“Can you type a few words into a search box and create this company’s product? If not, it’s a HALO stock.”

He gave an example.

Delta Air Lines and Expedia are both in the travel industry. This year, Delta rose 8.3%, while Expedia fell 6%. What’s the difference?

AI can help you find the cheapest flights, but you still have to get on the plane. Delta has planes; Expedia only has a search box.

He also said that this is the simplest investment logic he has ever seen.

For the past 15 years, Wall Street has favored asset-light businesses. Software companies have no factories, no inventory, and the cost to replicate code is zero, resulting in astonishingly high profit margins. But now AI has arrived, and what AI is best at replacing are precisely those companies that profit from code and information asymmetry.

The tide has turned; now the “heavy” ones are valuable.

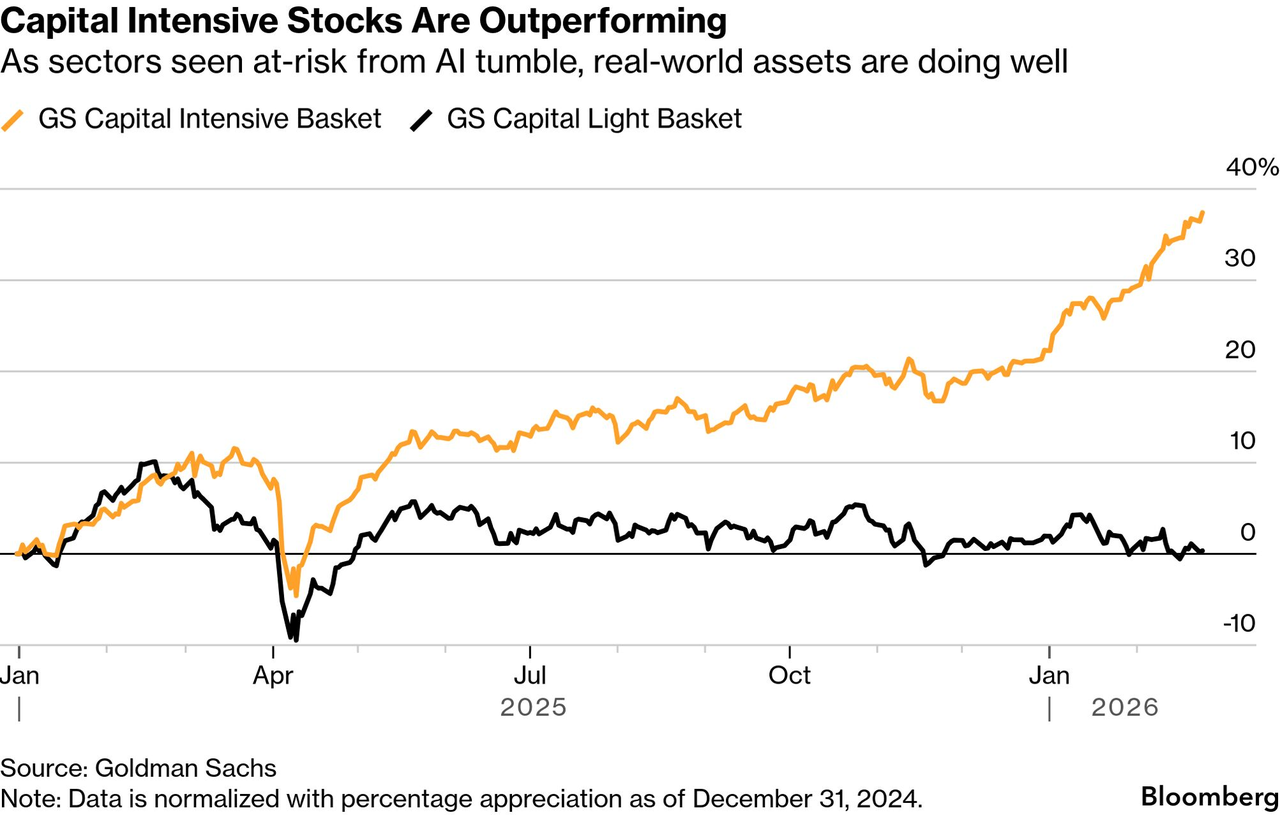

Within weeks of HALO's emergence, Goldman Sachs released an official research report titled "The HALO Effect"; the data showed that since early 2025, Goldman Sachs' heavy-asset stock portfolio has outperformed its light-asset portfolio by 35%.

Soon after, Morgan Stanley’s trading desk began using HALO to recommend assets to clients; Barclays and Bank of America research notes also began mentioning the term. Axios, The Wall Street Journal, and CNBC ran concentrated reports...

A term made up by a blogger became the biggest trading theme on Wall Street in 2026.

What does this mean? It’s not that Brown is that impressive—it’s that everyone is truly panicked. Panicked enough to need a word to reassure themselves:

Don't worry, AI has disrupted many things, but there is still one type of company that is safe.

The world is a massive asset-intensive system.

Do you think HALO is just a narrative? The capital markets have already started voting.

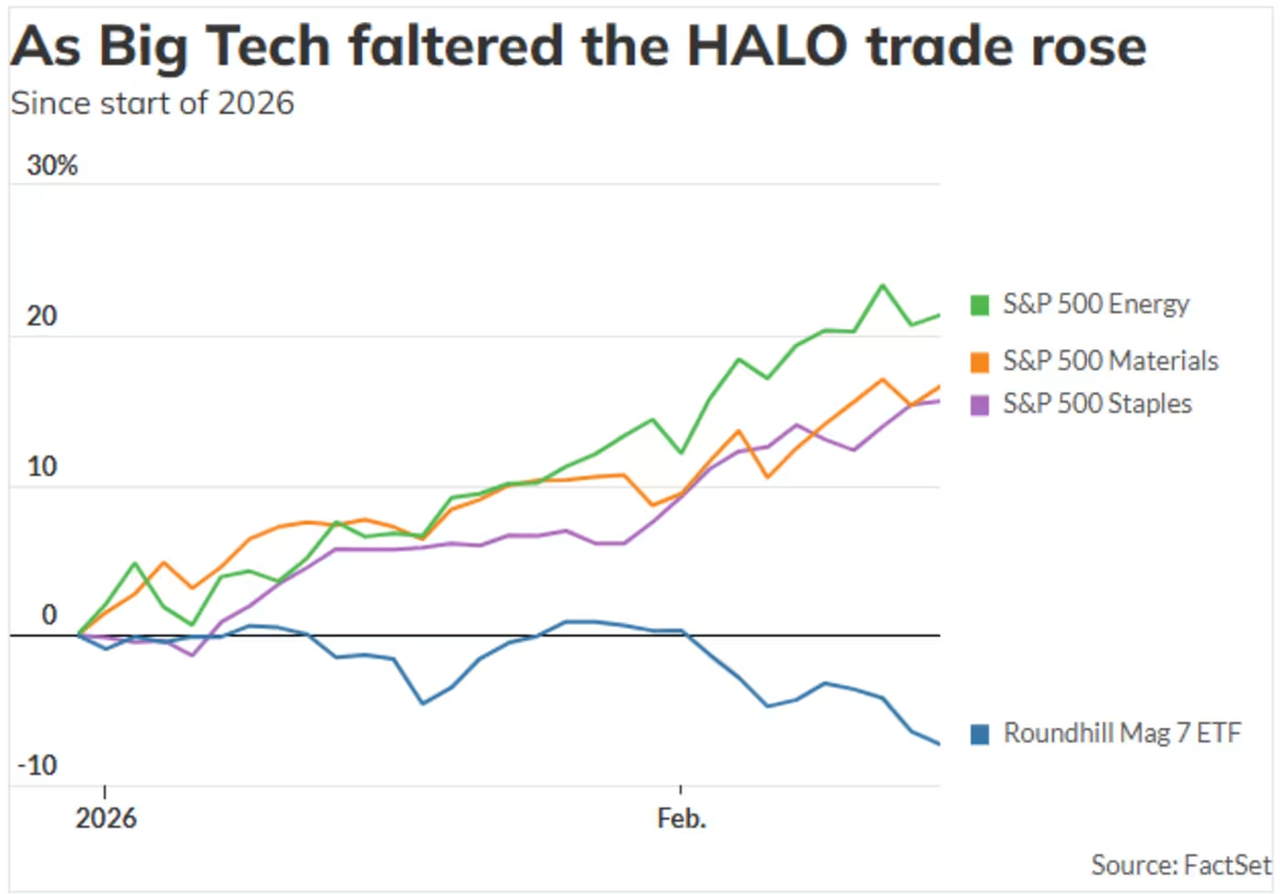

From the start of 2026 through the end of February, the energy sector of the S&P 500 rose over 23%, materials increased by 16%, consumer staples rose by 15%, and industrials gained 13%.

At the same time, the information technology sector dropped nearly 4%, and finance dropped nearly 5%.

Meanwhile, the seven major U.S. tech stocks all fell silent. Of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla, only two are up this year.

Investors are concerned whether these companies can recoup their investments given that they spend hundreds of billions of dollars annually building computing power.

Which specific companies are rising?

McDonald's, Walmart, ExxonMobil... selling burgers, running supermarkets, refining oil. AI can write poetry, code, and even argue in court—but it can't fry french fries or drill for oil.

Budweiser has also risen 48% since last year, after all, you can't drink AI.

Thus, HALO represents a reversal in capital market valuation logic under AI anxiety—a reversal last seen in 2000.

Back then, investors fled from tech stocks en masse, pouring into "boring" sectors like energy, industrials, and consumer goods. The Nasdaq dropped nearly 80% from 2000 to 2002, while the S&P energy sector rose nearly 30% during the same period.

But there is a key difference. The dot-com bubble occurred because the internet wasn’t profitable, and the story could no longer be sustained. This time, things are a bit different:

AI is too capable, capable to the point of being frightening.

Fear caused by AI technology failing is uncommon; now it is fear triggered by AI technology succeeding. This is almost unprecedented in the history of capital markets.

More ironically, AI companies themselves are also becoming heavier.

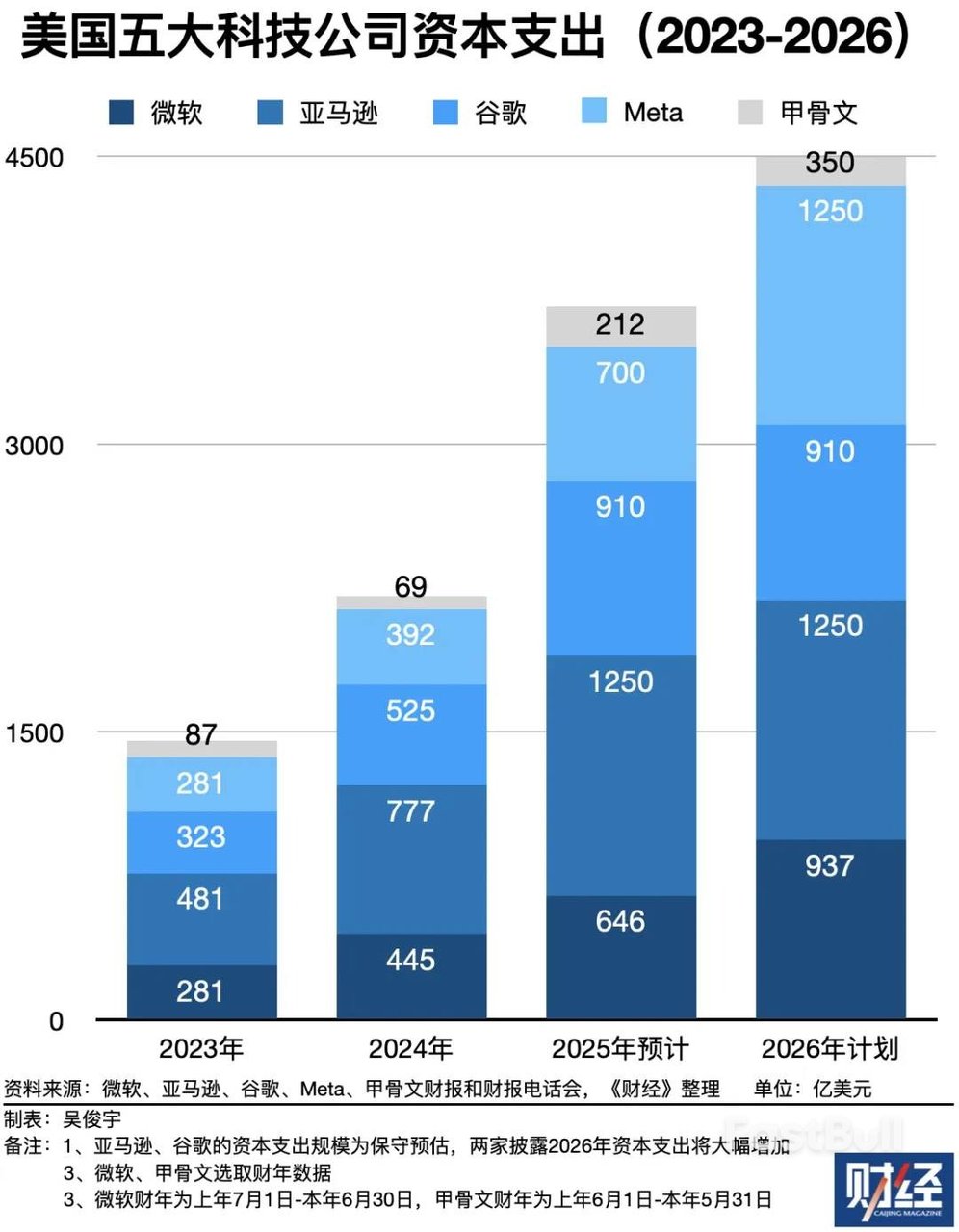

Goldman Sachs specifically noted in its report that companies which most strongly embraced the asset-light model over the past few years are now becoming the largest capital spenders in history.

The five major tech giants are projected to spend $1.5 trillion on capital expenditures from 2023 to 2026, with over $450 billion spent in 2026 alone—more than their entire historical spending prior to the AI era.

Image source: Finance

Where did this money go? Data centers, chips, cables, cooling systems, power generation facilities. All heavy and expensive physical-world assets.

So you will see an absurd scene:

AI shattered others' light-asset models and became heavy-asset itself.

Companies that claimed they would overthrow the old world eventually found they needed exactly the same things as the old world: factories, electricity, plumbing...

Wall Street chased the "light" for 15 years, only to find that even AI cannot escape the "heavy".

In the U.S., people hide at McDonald's; in China, people use Qwen to place orders.

At the same time, we on the other side gave a completely opposite answer.

In late February, Bloomberg published a report with a headline roughly meaning: The Chinese market is resisting global AI panic trading. One summary sentence in the article I found particularly insightful:

The U.S. market focuses on what AI can take away, while the Chinese market focuses on what AI can help achieve.

The same technology, two completely opposite emotions.

While U.S. investors were coining the term HALO and hiding out at McDonald’s and Walmart, Chinese investors were snapping up AI application stocks.

In February this year, JPMorgan gave buy ratings to MiniMax and Zhipu, while Goldman Sachs initiated new buy recommendations for BiRen Technology and Muxi Integrated Circuit; Bank of America analysts stated that AI agents and their commercialization could be the largest investment theme in China's market in 2026.

Companies like Tencent and Alibaba are not feared as being killed by AI; people are concerned instead about whether they can use AI to earn more money.

In its January report, Goldman Sachs stated that Tencent is the biggest beneficiary of AI applications in China's internet sector, with each of its business lines—gaming, advertising, fintech, and cloud—being accelerated by AI.

Why do the two sides react completely differently to the same wave?

U.S. tech stocks have become overvalued over the past decade, so much so that even a slight shift in their profit margins from AI could make their valuations unsustainable. In contrast, Chinese tech stocks have just emerged from a low point of the past two to three years and are inherently undervalued; for them, AI represents an opportunity, not a threat.

But stock price alone doesn't explain everything—the bigger difference lies in the soil.

At the same time that the HALO narrative was dominating U.S. equities, China just celebrated the most AI-rich Spring Festival in history:

Volcano Engine has become the exclusive AI cloud partner for the CCTV Spring Festival Gala, while Doubao has secured exclusive partnership rights; Qwen has secured title sponsorship deals with four major TV networks: Oriental, Zhejiang, Jiangsu, and Henan; Tencent Yuanbao is distributing 1 billion yuan in red packets, and Baidu Wenxin is distributing 500 million yuan. Alibaba is going even further with its “Spring Festival Treat” plan worth 3 billion yuan—Qwen helps you order bubble tea, delivering 1 million orders in just three hours...

Image source: Sina News | Data Studio

The four tech giants spent over RMB 4.5 billion combined on AI marketing during the Spring Festival.

Ten years ago, WeChat and Alipay competed for red packets on the Spring Festival Gala. Now, it’s Doubao and Qwen. AI companies aren’t treating the Spring Festival Gala as an advertising space—they’re using it as a stage to introduce AI to the mainstream public.

The same fire is a disaster when it burns dry wood, but a source of warmth when it ignites damp wood.

In the same AI wave, American capital is fleeing companies disrupted by AI and pouring into companies that AI cannot kill; Chinese capital is chasing companies that can effectively use AI.

While one side is chasing and the other is fleeing, the author feels that the fleeing side may be overpriced.

The current situation is that AI’s capabilities are fairly priced, but its destructive potential is overpriced. Money is flooding into HALO stock as investors imagine who AI might kill and flee ahead of time.

They’ve gone to McDonald’s, Budweiser, Walmart, and so on—these companies are certainly solid, but how much of their gains this year is due to fundamentals, and how much is due to fear premium?

The pendulum of Wall Street has always swung to extremes. In 2000, everything .com was valuable; in 2002, everything .com was a scam. Now, people believe beer and tractors can withstand AI.

When this consensus becomes crowded enough, the next overcorrection won’t be far away.

As for me, this is how I see it:

AI is indeed getting stronger, and there's no arguing that. But the gap between "getting stronger" and "killing an industry" is much wider than most people realize.

Every technological revolution follows the same script: first panic, then overreaction, and finally the realization that what was fled from didn’t die—it became cheaper because of the panic.

The internet didn’t kill Walmart; Walmart learned e-commerce. Mobile payments didn’t kill banks; banks learned to build apps.

The companies that will truly be killed by AI are those that shouldn’t exist in the first place—products with no moat, growth entirely dependent on funding, and survival based solely on information asymmetry.

These companies don’t need AI to kill them—the economic cycle will.

So the question may never have been “Will AI disrupt the world?”—each of us must ask ourselves: Does the company you invested in have the ability to turn AI into its weapon, not its obituary?

The person who can answer this question doesn't need HALO.