Key Insights

- Crypto News, A joint survey by Coinbase and CoinTracker found that 61% of US crypto users are unaware of new 2025 tax rules.

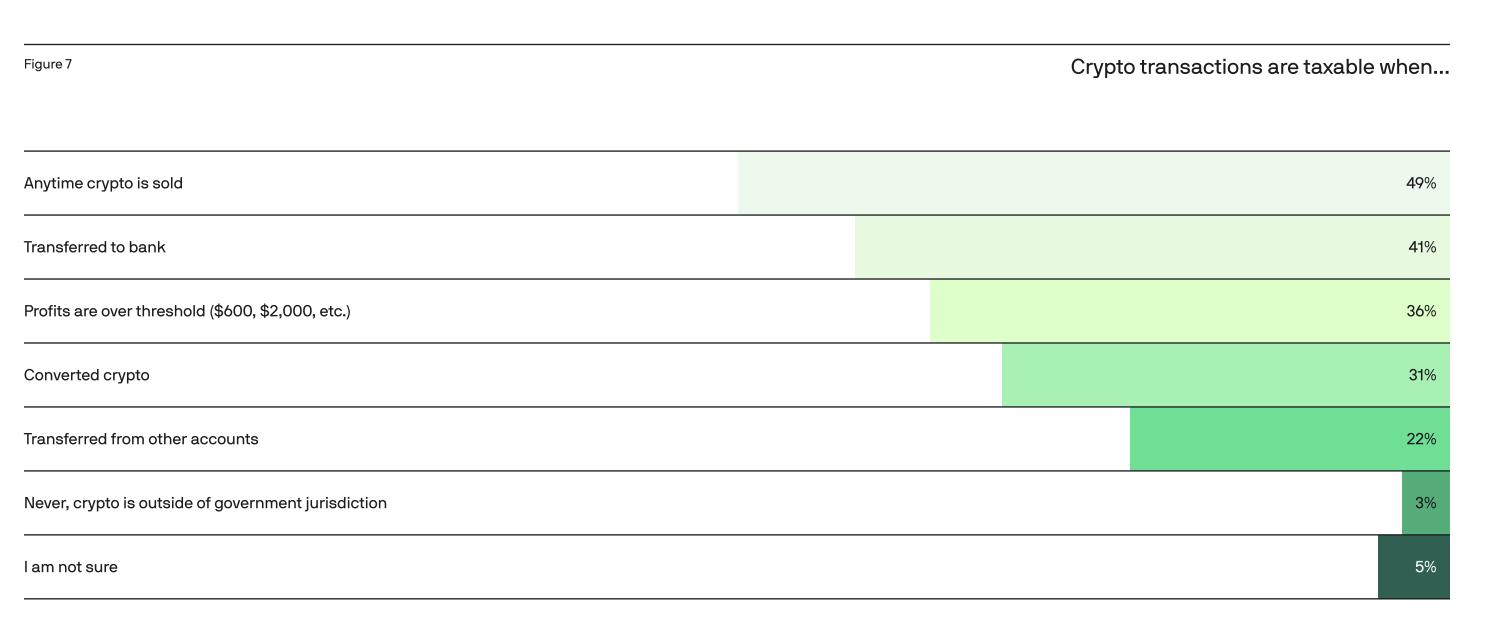

- Only 49% of respondents correctly understand that crypto is taxable every time it is sold.

- Just 8% of crypto users currently use crypto-specific tax tools.

Crypto news out of a major joint industry survey reveals a sharp gap between tax compliance intent and functional tax knowledge among US crypto users.

The 2026 Crypto Tax Readiness Report, produced by Coinbase and CoinTracker and based on a survey of 3,000 US crypto users conducted between September and October 2025.

The survey found that while 74% of respondents know their crypto activity is taxable, 61% were unaware of specific tax rules introduced for the 2025 tax year, including the new IRS Form 1099-DA.

Crypto News: Most Users Unaware of Form 1099-DA Requirements

For the 2025 tax year, the IRS introduced Form 1099-DA, which requires brokers to report gross proceeds from digital asset transactions.

Regardless of what brokers provide, users remain responsible for calculating their own adjusted cost basis across all 2025 crypto transactions, including reconciling activity across multiple platforms and wallets.

Despite this, 61% of survey respondents said they were unaware of the new rules. Among those who did rate their own knowledge, 56% described their understanding of crypto tax rules as good or excellent.

Only 17% rated their knowledge as poor or nonexistent. The taxability confusion runs deeper than new rules alone. Only 49% of respondents correctly identified that a tax event is triggered every time crypto is sold.

A large portion attributed taxability to other actions: 41% believed transferring crypto to a bank account triggers a taxable event, 36% thought profits needed to exceed a threshold, such as $600 or $2,000, and 31% believed converting crypto was the triggering action.

Another 22% thought transferring from other accounts created a tax event, and 3% believed crypto falls entirely outside government jurisdiction.

Cost Basis Tracking Remains the Central Challenge

The report identifies cost basis tracking as the most persistent practical problem facing crypto tax filers.

Respondents averaged 2.5 platforms or wallets, and 83% used self-custodial wallets at some point.

When a user transfers crypto from one exchange to another, the receiving exchange cannot access the original purchase price from the sending platform.

If the cost basis is missing when a user files, the IRS may default to treating the original cost basis as zero, resulting in significantly overstated taxable gains.

The report noted that 76% of respondents were aware that cost basis adjustments may be required, but only 35% had actually made such adjustments in the past.

An additional 41% said they knew about cost basis adjustments but had not done them, and 16% said they did not know what adjusting cost basis means.

Shehan Chandrasekera, CPA and Head of Tax Strategy at CoinTracker, described the cost basis problem as uniquely difficult to solve.

How Users Are Filing and Where AI Fits In

The report found that most crypto users rely on general tax software (78%) and accountants (52%) to file their taxes.

Only 8% use crypto-specific tax reconciliation tools, a figure the report highlighted as disproportionately low given the complexity involved in crypto tax preparation this year.

Interest in AI for tax-related tasks is rising. 47% of respondents said they would use AI to calculate taxable income, cost basis, and capital gains.

Forty-three percent said AI could provide personalized tax strategy recommendations, and 39% would use it to identify deductions and savings.

Thirty percent went further, saying they would be open to relying on AI to complete their entire tax filing process. A further 44% would use AI to build a preparation checklist, and 36% would use it to review and file a return.

The post Crypto News: 61% of US Users Unaware of Tax Rules, Survey Finds appeared first on The Market Periodical.