Organized & Compiled by Schain TechFlow

Hosts: Josh Kale; Ejaaz Ahamadeen

Podcast source: Limitless Podcast

Forget NVIDIA: This 24-Year-Old’s $4.5 Billion Bet on AI’s Real Problem (Leopold Aschenbrenner)

Broadcast date: March 4, 2026

Key Points Summary

Everyone’s talking about Leopold Aschenbrenner lately—24 years old, running a $5.5 billion AI hedge fund, the poster child of U.S. equities. But most discussions stop at “He’s amazing” and “He made so much money,” with very little actual breakdown of his investment logic.

Two months ago, the Limitless Podcast did an episode analyzing his 13F filing transaction by transaction:

Why sell out NVIDIA? Why allocate 20% of the portfolio to a fuel cell company? Why buy up a bunch of Bitcoin mining firms? Why short Infosys? At the time, this episode received almost no attention. Looking back now, most of those calls have played out accurately—worth revisiting and reanalyzing.

Key Insights Summary

Regarding Leopold Aschenbrenner's investment performance

- Last year, he managed $1 billion in assets... Today, just one year later, that $1 billion has grown to $5.5 billion.

- His fund was established at the end of 2024 with an initial size of $255 million. Within just six months, his fund outperformed the S&P 500 by eight times.

- He wrote a 165-page article titled "Situational Awareness," in which he essentially predicted that we will reach artificial general intelligence (AGI) by 2027.

Shift in Investment Paradigm: From Chips to Infrastructure

- He sold off NVIDIA, Broadcom, TSMC, and Micron—all leading AI infrastructure companies.

- By the end of 2025 or early 2026, he believes the market has essentially fully reflected the value of GPUs.

- He shifted his focus to the primary bottlenecks that investors have not yet adequately addressed—energy and infrastructure.

- The existing power grid was designed for humans, not to meet the massive AI demands we face today. That’s where his current investments are focused.

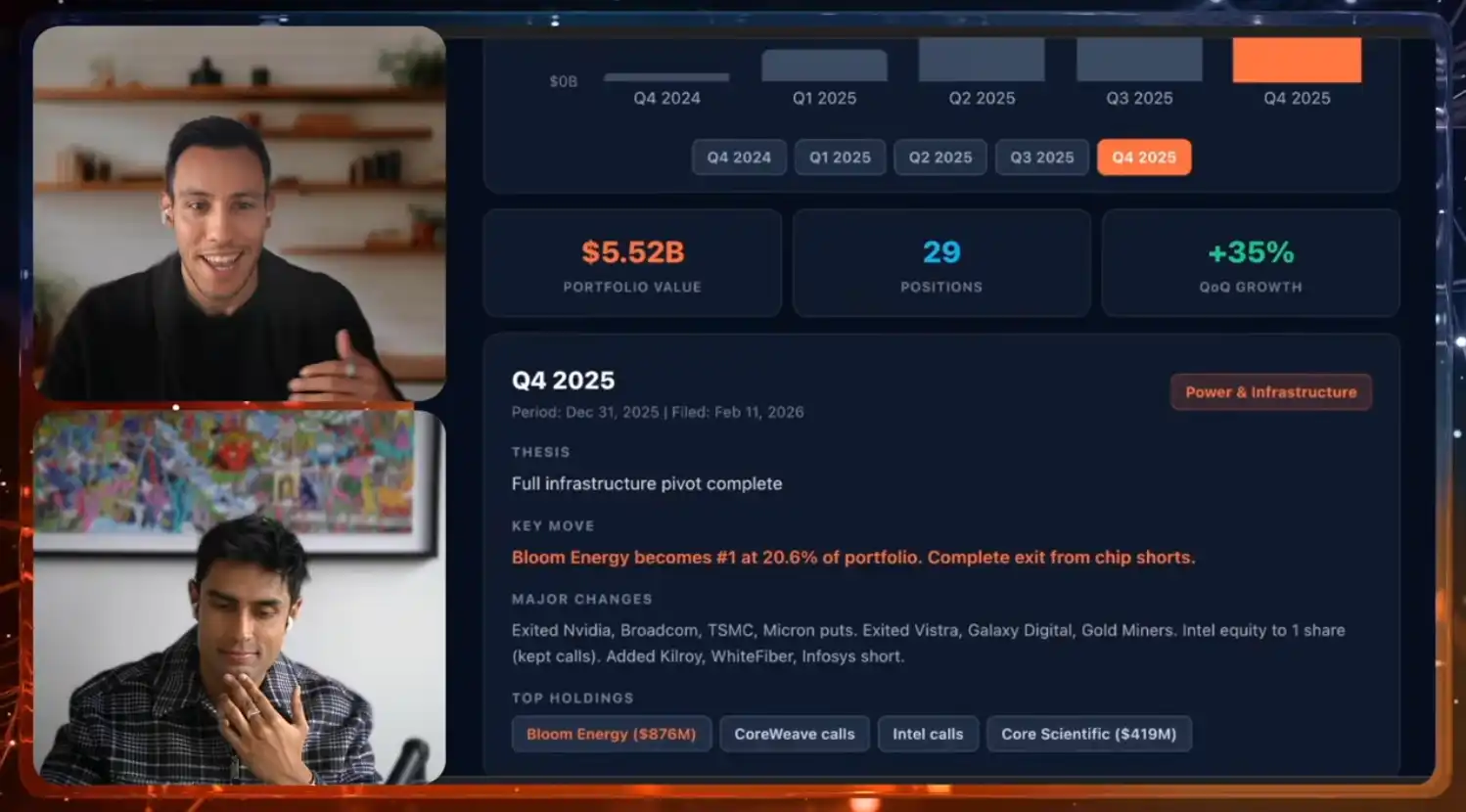

Core Holding: Bloom Energy

- Bloom Energy is his largest current investment, accounting for 20% of his entire portfolio... He has built a substantial position in the company, amounting to $855 million.

- Bloom Energy has developed a device called an oxide fuel cell... that directly converts natural gas into electricity usable by data centers. It is modular and can be deployed quickly.

- Their backlog of customer orders exceeds $20 billion. Revenue increased by approximately 34% in 2025, and they anticipate a further 40% revenue growth in 2026.

- If you use products like Bloom Energy’s natural gas turbines, you won’t need to rely on the grid at all—just install them next to your AI data center.

Infrastructure and the "Shortcut" to Bitcoin Mining

- Leopold made a major investment in CoreWeave, deploying his largest leveraged investment in core GPU infrastructure and energy supply.

- He invested in many Bitcoin mining companies... because these companies possess the two key elements needed to build AI infrastructure: land and electricity.

- He acquired these companies to obtain their licenses and grid access rights. Typically, securing these licenses can take months or even years.

- It’s like taking over a bar that already has a liquor sales license, rather than applying for a new one and waiting for years—this is a very smart shortcut.

Short-selling logic and the end of IT outsourcing

- He holds a short position in a specific company, Infosys... Their business model relies entirely on providing labor that is cheaper than that in Western countries.

- He realized that these models had become powerful enough not only to automate simple tasks but also to handle critical IT processes, so he made a large short position in the company.

Investment Philosophy: A Return to the Physical World

- Companies that rely solely on software will find it increasingly difficult in the future. His shift is not just about building architecture, but also about investing in the physical world—such as manufacturing, factories, energy, and infrastructure.

- These are areas that cannot be built by AI but require human effort, licenses, and legislation to establish the necessary hardware and infrastructure.

- Energy is the only resource that no one can ever have enough of... It all revolves around one core idea: powering the future.

Young investment prodigy Leopold Ashbrer

Josh Kale:

A man named Leopold Ashbrer, who is 24 years old this year, was featured on one of our shows last year when he was 23, managing $1 billion focused on investing in emerging cutting-edge AI concepts and technologies. Today, just one year later, that $1 billion has grown to $5.5 billion.

This guy, who is much younger than both of us, just delivered a groundbreaking performance, earning more money in AI than any other fund in the world. More importantly, AI is currently the hottest market, meaning competition is extremely fierce. Clearly, this guy named Leopold is doing something truly different.

Last week, his new 13F filing was released, giving us our first look at his recent trading activity. We’ll now closely examine these documents to see exactly what this individual did to grow his managed assets from $1 billion to $5.5 billion.

Insights from 13F Filings

Ejaaz Ahamadeen:

He achieved all of this within 12 months. His fund was established at the end of 2024 with an initial size of $255 million. Within just six months, its performance outpaced the S&P 500 by eight times, growing to $2 billion. Since we last discussed his Q3 fund report on the show, his fund has grown by another $1.5 billion. He is now, quite literally, in a generational surge.

He is very young and has made a significant shift, but everything aligns with what he calls his “bible”—a 165-page article titled “Situational Awareness.” In this piece, he essentially predicted that we would reach artificial general intelligence (AGI) by 2027. In this sweeping article, he laid out his detailed vision of how the AI revolution would unfold. His predictions have been nearly flawless, as he successfully anticipated the surge in GPU infrastructure, and now he has proposed another crucial shift, which we will explore in depth next.

Transition from chips to infrastructure

Josh Kale:

I believe the entire investment thesis is shifting from chips to infrastructure. What we’re seeing on screen right now is very interesting. He used Claude to create a document that walks us through the entire change log from last year to this year. Perhaps we could start with the assets he sold, since the positions he exited were quite substantial—including NVIDIA, where he sold put options worth $300 million in a single quarter.

Ejaaz Ahamadeen:

You’ll notice that many of the stocks he sold are from highly popular companies that many people are currently investing in. So the question is, why is he selling $1 billion worth of shares in these companies? He sold shares in NVIDIA, Broadcom, TSMC, and Micron—all major AI infrastructure companies.

He actually profited from selling NVIDIA's stock—he held $300 million in put options, meaning he likely gained from NVIDIA's declining stock price over the past few months. So the question is, why did he do this?

In his 165-page paper, he stated that by the end of 2025 or early 2026, he believes the market has essentially fully priced in the value of GPUs. This value primarily comes from companies like NVIDIA and Broadcom, which manufacture these chips and stack them for AI labs such as OpenAI and Anthropic to use in training models.

Now, he is shifting his focus to the primary bottlenecks that investors have yet to fully address: energy and infrastructure. Currently, a major issue facing many AI labs is twofold: first, they have too many GPUs; second, the existing power grid was designed for human consumption, not to meet the massive energy demands of today’s AI workloads. This is where his current investments are focused.

Sell NVIDIA put options

Josh Kale:

I find it fascinating to see him sell NVIDIA’s put options and completely exit his investment in NVIDIA. Because whenever I chat with friends or ordinary people on Wall Street, NVIDIA is always the company on everyone’s mind—it’s the biggest investment target. Yet seeing him walk away from NVIDIA reinforces my belief that he’s always one step ahead, always anticipating future trends rather than clinging to past hotspots. In his view, the future lies in infrastructure—the shift from chips to information-based strategies.

This could be a great opportunity to explore his new investments, as these are the stocks you should be paying attention to. These are the assets he currently holds and believes will grow in the future. If his assessment is correct, we could see substantial returns from them. So, what new investments did he make this quarter?

Ejaaz Ahamadeen:

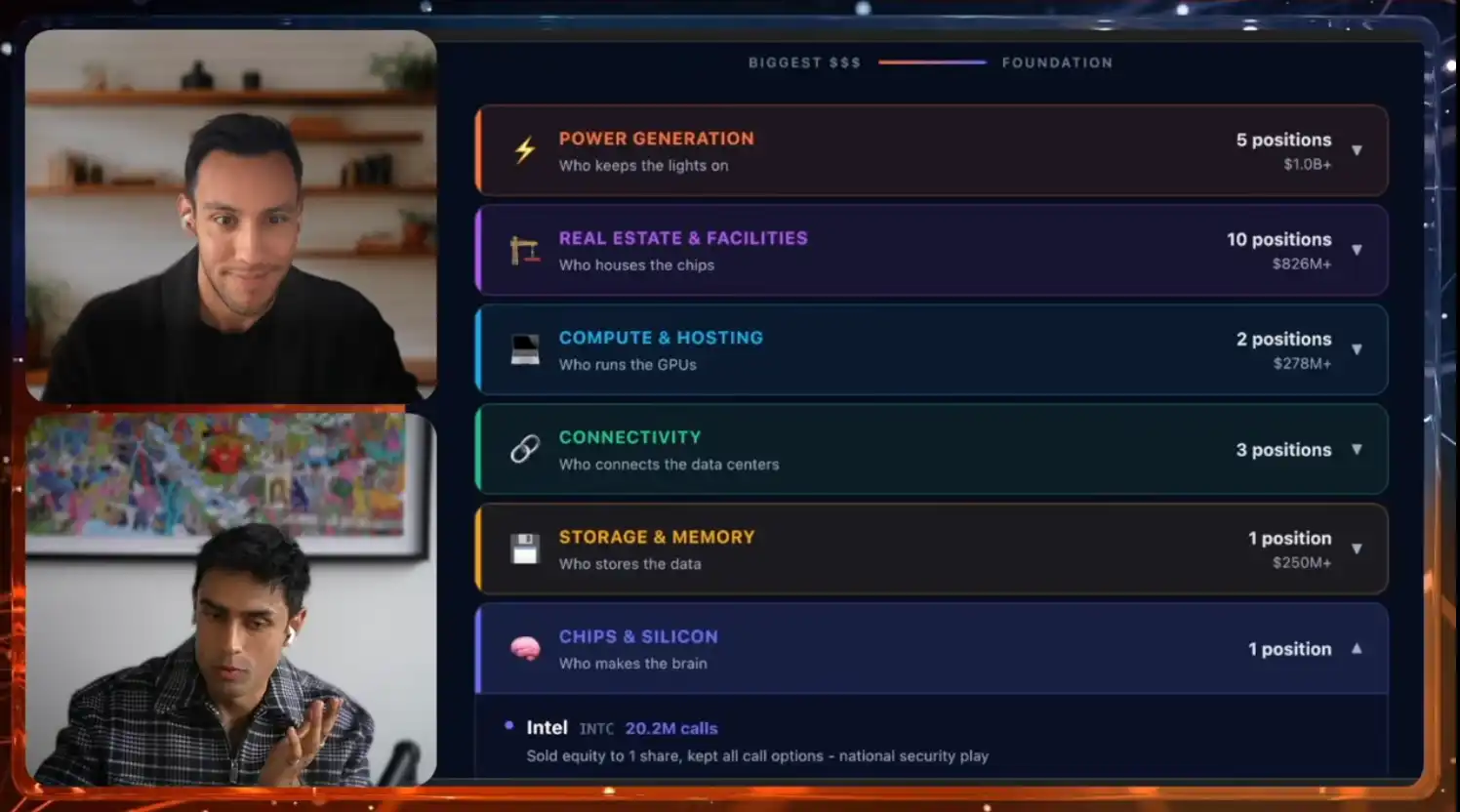

Here is a clean portfolio chart categorizing all of Leopold Ashbrer’s investments by AI technology stack. We can see the investments are divided into categories such as power generation, real estate and facilities, computing and hosting, connectivity, storage and memory, and chips and silicon.

Actually, I’d like to add to what I just mentioned—I noticed he executed a very clever trade with Intel. He sold his shares but still maintained a massive long position. Through this strategy, he freed up liquidity and redirected the capital toward other companies. The primary company he invested heavily in is Bloom Energy, a power generation firm that was nearly unknown just three months ago but specializes in manufacturing turbines designed to power AI data centers.

He built a massive position at this company, amounting to $855 million. Although $876 million is shown here, the report states $855 million.

Bloom Energy: Innovator in Power

Josh Kale:

Bloom Energy is his largest current investment, accounting for 20% of the entire portfolio. It has nothing to do with the chip sector and represents a completely different direction. I looked into their business and found it truly interesting.

Bloom Energy has developed a device called a solid oxide fuel cell, an advanced technology that generates electricity on-site from natural gas. Typically, when natural gas is delivered to a data center, it must be heated and cooled through turbines—a highly inefficient energy production process. Bloom Energy’s “fuel boxes,” however, directly convert natural gas into electricity usable by data centers. They are modular, can be deployed quickly, and appear to have no supply shortages. As far as I know, they plan to produce 2 gigawatts of power this year.

This is a very interesting way to engage with energy. I’ve been searching for the “NVIDIA of energy”—the chipmaker of the energy sector. I haven’t found a perfect match yet, but Bloom Energy might become that company.

Ejaaz Ahamadeen:

I also reviewed their recent financial statements, as they are a publicly traded company. Their backlog of orders has reached $20 billion. Revenue increased by approximately 34% in 2025, and they anticipate a further 40% revenue growth in 2026, clearly indicating that demand far exceeds supply.

You mentioned solid oxide fuel cells. Their natural gas turbines are particularly attractive because they do not rely on the existing power grid. As I mentioned earlier, today’s grid is under significant strain due to rising energy demands from both humans and AI data centers, leading to increased electricity prices in areas where AI data centers are located. By using products like Bloom Energy’s natural gas turbines, you can completely eliminate dependence on the grid. Simply install them next to your AI data center to efficiently and cost-effectively generate the power needed for training or inference with your GPUs and data centers.

Companies like Broadcom and CoreWeave will require this energy, especially large-scale cloud service providers and AI labs. This reminds me of the game Civilization—have you played it? It’s like moving infrastructure and energy production facilities to your small settlement to drive its growth; what’s happening here is very similar to that scenario.

Josh Kale:

It’s clear that there is no shortage of energy—the issue is who can produce the most. They do have a very large backlog of orders, but the question is whether they can produce enough product to fulfill them. Manufacturing capacity has become a critical issue here. In many of these investments, we’re entering an “atomic” world where manufacturing truly matters. I’d like to explore this further in the future to see if they truly have the capacity for large-scale production. But for now, this is undoubtedly a very important investment area, accounting for 20% of his portfolio. What other notable positions are in his new portfolio?

Ejaaz Ahamadeen:

He also added approximately $300 million in CoreWeave investment. Imagine being an AI lab that needs GPUs—buying them from companies like NVIDIA is only part of the job. Deploying those GPUs into rack servers, providing power, offering technical engineering support, and maintaining the GPU servers and cooling systems is an entirely different challenge. That’s why you can outsource these tasks to a company known as a “new type of cloud provider”—that’s CoreWeave, which specializes in handling exactly these operations.

Broadcom also offers similar services to some extent, but CoreWeave is a smaller company that originally focused on GPU gaming infrastructure and has since transitioned into a company exclusively serving AI. Leopold made a major investment in CoreWeave. During the third quarter we previously discussed, he invested $500 million, and now he has added another $300 million. His total investment in CoreWeave may now reach $800 million, but the story goes even deeper—he also holds approximately 10% of Core Scientific, one of CoreWeave’s key suppliers, a company that specializes in building out the energy infrastructure for CoreWeave.

If considering betting strategies in investments, Leopold has likely made his most leveraged positions in core GPU infrastructure—such as CoreWeave’s new cloud services—and energy supply—such as Bloom Energy—his two largest holdings in the current fund.

Bitcoin mining

Josh Kale:

What I find interesting is that he has already acquired a large enough stake in these companies to become an activist investor, capable of directly influencing their decision-making. I think that’s fascinating. While studying his portfolio, beyond the obvious focus on power generation, I noticed that his largest new positions were actually in real estate-related investments—he added about ten new positions tied to real estate, which relate to Bitcoin mining.

We see that he has invested in several Bitcoin mining companies. This seems unusual and counterintuitive, especially given the lackluster state of the cryptocurrency market and Bitcoin’s poor performance. So why would he buy these Bitcoin mining companies? The reason is that these companies possess two critical components needed to build AI infrastructure: land and electricity.

What is needed for Bitcoin mining? Significant energy and sufficient space to house GPU racks. While Bitcoin mining has not completely declined, the real estate and electricity resources of these companies now clearly offer better risk-adjusted returns. It appears he is betting that these Bitcoin mining companies will either sell their land rights and permits or directly transition into AI data centers.

Ejaaz Ahamadeen:

It’s important to note that his interest in these companies is not for mining purposes—he acquired them to gain access to their licenses and grid connections. Typically, obtaining these licenses can take months or even years. This is also why companies like Meta, Microsoft, and OpenAI have announced $1.4 trillion in computing partnerships, yet these collaborations have not yet fully translated into deployed models. This is one reason why GPU supply consistently lags behind the latest generation—they cannot secure these licenses in time.

Leopold instead acquired these small companies that already held licenses, bypassing the entire licensing process. He completely divested their cryptocurrency services and repurposed them exclusively for training AI models, becoming the infrastructure provider for these AI labs. It’s like taking over a bar that already has a liquor license, rather than applying for a new one and waiting for years—an extremely clever shortcut.

AGI and market trends

Josh Kale:

One of his investment principles I admire most—and the way it has been validated over the past year—is its simplicity and efficiency. For example, bitcoin mining companies clearly hold licenses and access to energy, and clearly, every AI company needs these resources. So why isn’t everyone buying these companies? I believe it’s precisely because these ideas are so simple that many are kept from investing. Yet time and again, his simple insights have proven correct.

Will Leopold’s prediction of achieving AGI by 2027 also be correct? Will we truly achieve AGI by 2027?

Ejaaz Ahamadeen:

To test this prediction, we created a prediction market on Polymarket, betting on whether OpenAI will announce that it has achieved AGI before 2027. Currently, the probability assigned by this market is 13%, suggesting that when Leopold proposed this fund, many were skeptical of his forecast. While his investment thesis may be sound, the timeline might be slightly off.

This probability is indeed very low. However, I must say that he was initially criticized for this paper, with many people considering his views too outlandish and unrealistic. About 50% of people believe AGI will be achieved within the next few months, while others think it won’t happen until 2030. Leopold is the only one who predicted 2027—and so far, his estimate is the closest to being accurate.

He predicted the importance of GPUs before the GPU boom began. Now, he has again made a prediction before the energy infrastructure boom. So I believe he remains ahead on this front.

However, his portfolio includes not only long positions but also a short position in a specific company: Infosys, an IT outsourcing firm primarily based in India. Their business model relies entirely on providing labor at a lower cost than in Western countries such as the United States or Europe. In simple terms, “Outsource all your administrative IT work to us, and we’ll take care of it.”

I believe his bet here is based on trends he has observed. He saw the rise of products like Claude Code and GPT Codex 5.3 and realized these models have become powerful enough not only to automate simple tasks but also to handle critical IT processes, leading him to make a large short position on the company.

I believe this is one of his more thoughtful investments and better aligns with the trends we’re currently seeing, demonstrating his willingness to put his money where his mouth is.

Bull market and bear market

Josh Kale:

We can discuss the reasons for a bull market and the reasons for a bear market. When entering such a portfolio, what aspects warrant criticism or require caution? First and foremost, this investor is only 24 years old—I’m unsure whether he possesses the same level of experience that many other investors have. While this may, to some extent, be an advantage, at some point, might this advantage collapse?

Another concern is that the fund’s investment thesis resembles a single-theme bet. If growth in AI infrastructure and related spending slows, or if the macroeconomic environment shifts, every position in this portfolio could face downward pressure—with little room for hedging. Thus, this strategy does have some potential vulnerabilities; however, at this point, all signals suggest the fund’s performance will only continue to rise.

Ejaaz Ahamadeen:

If you look at some of the most renowned investors of our time, their success has never been about how much they earned in a single year or quarter, but about their ability to generate consistent returns and compound growth year after year, decade after decade. Leopold has started with an impressive performance, far surpassing the average of hedge funds across any industry—not just in AI—but he still needs to prove himself over a longer time horizon. Time will tell.

I just want to say that this person, who was once fired by OpenAI, has profound insights into the future of AI and has made the boldest predictions—he is the only one whose predictions have, so far, been almost entirely accurate. He poured immense effort into his 165-page paper, stood firmly by his views, and everything so far is proving him right.

Will things change in the future? Possibly. But you can think of these reports and investments as his real-time tracking tools for identifying bottlenecks in the AI race—I want to emphasize that. Initially, his fund’s investment thesis centered on GPUs. He believed GPUs would become a demand hotspot, and the market was underestimating this opportunity. Now, his view is that this opportunity has been fully priced in by the market, and the next bottleneck he’s seeing is shifting toward energy infrastructure.

Take Elon Musk, for example—he’s launching data centers into space. Why? Because the sun provides more energy. Meanwhile, companies like Google, Meta, Broadcom, and NVIDIA are all investing in data centers or data center infrastructure to secure access to the power grid. He’s simply directing capital toward where the demand is, and I think that’s a smart move.

Josh Kale:

I recently read a great article by Naval whose core idea is that it will become increasingly difficult for companies that rely solely on software in the future, because developing and generating custom software has become incredibly easy. I believe his shift goes beyond just building architecture—it points toward investing in the physical world, such as manufacturing, factories, energy, and infrastructure. These are domains that cannot be built by AI alone but require human effort, permits, and legislation to realize—areas I believe represent the future.

Energy is the only resource that no one has sufficient access to. Whether it’s power generation or real estate investment, everything revolves around one core goal: powering the future. In the last earnings season alone, just a few companies like Google, Amazon, and NVIDIA committed $650 billion in capital expenditures, demonstrating that substantial funds are being directed toward solving this issue—and his portfolio is clearly positioned to capture the upside of this opportunity.

Ejaaz Ahamadeen:

Yes, he did make some investments that you might consider high-risk. For example, many people may have never heard of Bloom Energy unless they’re deeply familiar with the energy infrastructure sector. However, this company can be regarded as a Tier One, even top-tier, energy firm—particularly in the realm of portable energy. He connected these dots, concluded that the grid couldn’t meet current demand, and decided to invest in the company. He committed his capital with tremendous conviction—we’re talking about him allocating nearly one-fifth of his entire portfolio to this single position.

This is an extremely concentrated, high-risk, high-conviction investment approach. But if it succeeds, this is why his portfolio achieved a 4.5 to 5 times return in just one and a half years. We must respect him—for turning $1 billion into $5.5 billion in a single year is simply incredible.

Leopold's investment future

Josh Kale:

Overall, it’s truly impressive that he has achieved this, and his latest shift from hardware to infrastructure to energy appears to be on the right track with very promising prospects. If you align with his portfolio, this might be an opportunity worth noting. Of course, this is not investment advice—just an overview of this individual’s portfolio—but it does look highly promising and could perform exceptionally well this year.

Josh Kale:

I’m also curious about what our audience thinks—I’d like to know whether you believe our investment analysis is professional-grade, whether it meets Leopold’s standard, or if you think we’ve completely missed the mark and overlooked some obvious stories.

Ejaaz Ahamadeen:

Do you know what I’m looking for? I want to know what you think is the best stock of the year.

Josh Kale:

Yes, Leopold bet on Bloom Energy. I’d like to know—what is your Bloom Energy? What did we miss that could enable another fivefold growth this year?