Every time someone makes a big profit in the U.S. stock market, the first thing onlookers do is always the same: check their holdings to find the next stock to buy.

The most frequently translated report recently belongs to Leopold Aschenbrenner, a 24-year-old German.

In March this year, domestic media extensively covered him, with headlines all similar: the genius fired by OpenAI, who wrote a 165-page paper predicting AI trends and founded a hedge fund managing $5.5 billion...

But labels are just labels. What truly sets this fund apart is that it doesn’t buy NVIDIA, OpenAI, or any company building AI models. Instead, it only invests in what AI cannot live without—power generation, chip manufacturing, optical communications, data centers...

In his own words, the bottleneck for AI is not in the algorithms, but in electricity and computing power. The entire fund is betting that this statement is true.

A social media investment influencer who has been called "the son of the U.S. stock market in the AI era" or "the Warren Buffett of AI" has recently had this title resurfaced, as his predictions have become increasingly astonishingly accurate.

According to data released by the copy trading platform Autopilot on May 1, the simulated portfolio he follows increased by 61% over two months. Based on this, his fund size is now approaching $9 billion.

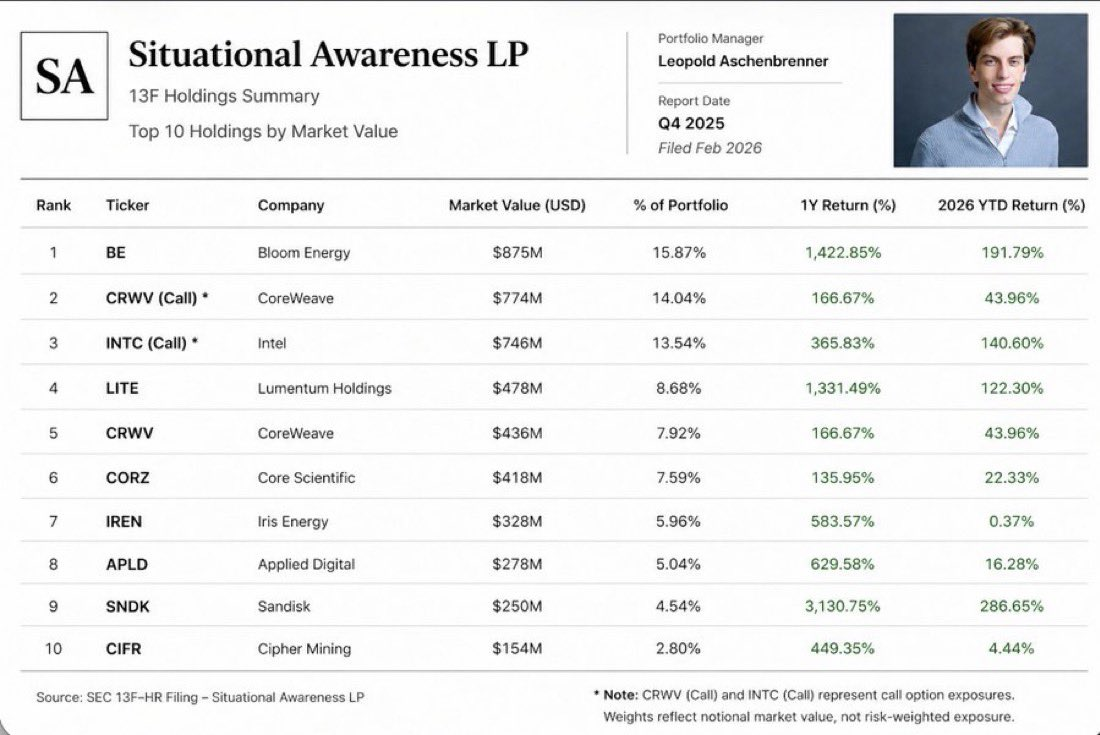

Where does the money come from? It primarily comes from two heavily weighted stocks. Bloom Energy, a fuel cell company that provides off-grid power to AI data centers, has risen 239% year to date.

According to position reports disclosed at the end of last year, he held $875 million in stock and options in this company, which has now grown to nearly $3 billion in market value.

Also Intel. According to the same position report, he purchased 20.2 million call options on Intel in Q1 2025, when Intel’s stock price was around $20, and Wall Street’s mainstream view was that Intel was not doing well.

Last week, Intel rose to $113, reaching a 25-year high. In less than a year, its price nearly quintupled, and this young investor’s options returned an even more dramatic multiple than the stock itself.

I understand the crowd's impulse. The U.S. investment site Motley Fool published four articles in one day analyzing his holdings, and overseas Reddit investment forums are debating whether to copy his portfolio. Everyone is trying to find the next Intel in his holdings report.

But you should know that position reports typically have a 45-day delay. By the time you see what he bought, the market has already moved halfway.

More importantly, even if you know his positions in real time, you still can't replicate the reason he consistently gets it right.

The circle is the greatest alpha.

First, what makes Leopold Aschenbrenner most remarkable is the paper he wrote in 2024 on AI, which nearly anticipated the current trajectory and investment trends in AI.

The core argument can be summarized in one sentence: AI model training compute increases by about half an order of magnitude per year; at this rate, AGI with human-level capabilities will emerge around 2027.

However, maintaining this growth rate hinges not on algorithmic constraints, but on electricity, chip production capacity, and physical space. The power consumption of a single training cluster will surge from megawatts to gigawatts, approaching the output of a large nuclear power plant.

This is the core logic behind his entire fund. The pace of AI development is determined by physical bottlenecks, so you should invest in the bottlenecks themselves.

This conclusion sounds like the result of extensive research and reasoning by a smart person in their study; but in reality, I believe it was the circle he was in that shaped this judgment.

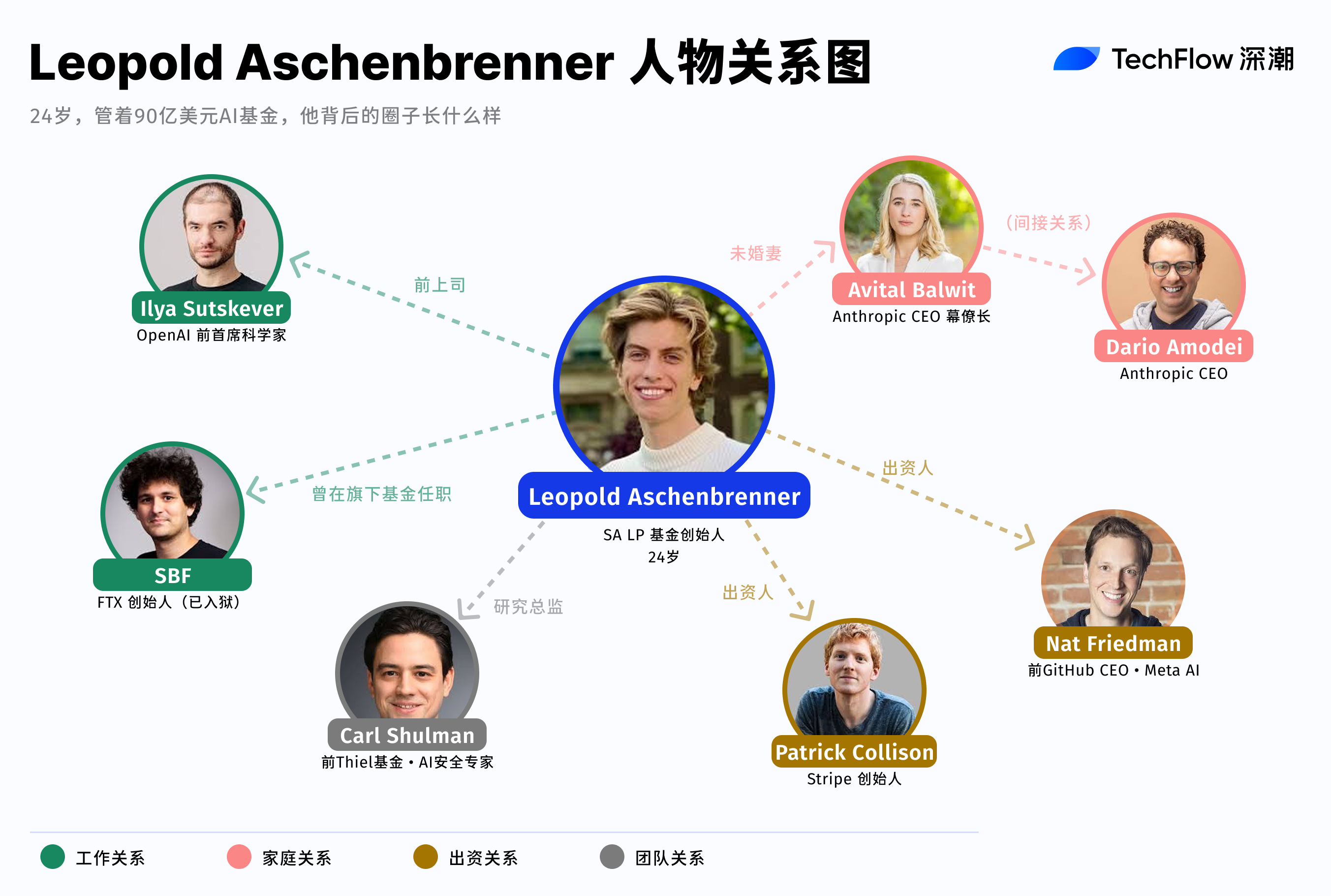

Before writing his paper, he spent a year at OpenAI’s Superalignment team, which is dedicated to researching how to control AI smarter than humans, reporting directly to Chief Scientist Ilya Sutskever.

That year, he observed internal training programs, actual power consumption, and the specific electricity and chip requirements of next-generation models. When he wrote "gigawatt-level power consumption" in his paper, his basis may have been the internal roadmap from the lab.

In April 2024, he was fired by OpenAI after sending an internal memo to the board warning that the company’s security measures were inadequate and that it faced risks of infiltration by foreign intelligence agencies.

This memo sparked tension between management and the board, and OpenAI subsequently fired him for "leaking information."

Two months later, the paper was published. Rather than being an independent study, it should be understood as the public version of his internal thinking at OpenAI.

AI papers address the question of "which direction to look." But for investing, knowing the direction alone is far from enough.

AI requires more electricity—a view many analysts were already expressing back in 2024. What truly matters is timing and positioning, such as whether you’d dare to invest $20 million in call options when Intel’s stock was at $20.

This confidence doesn't just come from believing in the broad trend of AI, but from knowing precisely which companies are signing large power purchase agreements and which data centers are expanding, along with the actual scale of demand.

Meanwhile, the fund Situational Awareness, founded by Leopold Aschenbrenner, has investors who sit right in the front row of these decisions.

The fund's LPs include the two founders of Stripe, a company that processes payment volumes for much of Silicon Valley’s tech industry and can directly sense the acceleration in infrastructure spending;

Another investor is Nat Friedman, former CEO of GitHub and current head of product at Meta AI, who is actively involved in daily decisions regarding compute resource procurement.

In addition to initial capital, they provided the fund with a continuously updated information channel.

In addition, the head of research at his fund is also a key figure on this chain. Carl Shulman, a veteran in the field of AI safety, previously worked at Peter Thiel’s hedge fund, Clarium Capital, where he specialized in translating insights from the AI community into actionable trading strategies.

His portfolio also includes an often-overlooked crypto asset.

According to last year’s position report, he established new positions in CleanSpark and Bitfarms, both Bitcoin mining companies transitioning their BTC mining facilities into AI computing centers.

Crypto mining facilities naturally have large-scale power access and cooling systems, which are precisely the most scarce resources for AI data centers.

Interestingly, he is no stranger to the crypto industry. In 2022, he worked for nine months at the Future Fund, the charitable foundation founded by SBF, and left just before FTX’s collapse.

It is unknown whether this experience directly influenced his judgment of mining companies. However, it is certain that he is among the very few who have deeply engaged with both the cryptocurrency industry and cutting-edge AI laboratories. This intersection itself represents a rare vantage point for insight and potential networking.

One additional detail: his fiancée, Avital Balwit, is the chief of staff to Dario Amodei, CEO of Anthropic—the parent company of Claude and OpenAI’s most direct competitor.

He worked at OpenAI, and his fiancée works alongside the CEO of Anthropic—two leading companies at the forefront of the AGI race, giving him both hands-on experience and daily exposure.

Last year, Fortune magazine interviewed more than a dozen insiders who had interacted with him and concluded that he is highly skilled at “packaging ideas brewing in Silicon Valley labs into compelling narratives.”

I think this description is too polite. What he actually did was more direct—he bet on public markets using insights gained from private circles. The AI papers he published are sanitized versions; his own investment fund contains the full version.

A feedback loop that outsiders cannot enter

Looking back, Leopold Aschenbrenner’s fund chose a less common structure.

Most AI funding follows the venture capital route—investing in early-stage companies in the hope that one will become the next OpenAI. He did not take this path. According to Fortune, when founding his fund, he explicitly rejected the VC model, arguing that the impact of AGI is too significant to be fully expressed outside the most liquid public markets.

This choice itself reveals a consensus within his circle: the greatest investment opportunity in the AI era may lie within established companies that already possess physical infrastructure.

It could be a fuel cell company with existing power access, a semiconductor giant with wafer fabrication lines, or a Bitcoin mining company with mines and cooling systems. These companies have been publicly traded for years and offer strong liquidity, but most analysts are still valuing them using outdated frameworks that have not seriously incorporated the variable of "AI infrastructure as a necessity."

This is his arbitrage opportunity.

People in the industry are already aware of the pace and scale of AI infrastructure expansion, while public markets are still pricing assets using outdated logic. The gap between them is the source of profit.

This informational advantage has another characteristic: it is self-reinforcing.

The better a fund's returns, the more industry insiders are willing to become LPs. The more LPs there are, the denser the access to decision-makers' insights. The denser the insights, the higher the accuracy of investments. This is a positive feedback loop, and for outsiders, the barrier to entering this loop only continues to rise.

Of course, this cycle also has its vulnerabilities. Highly concentrated positions combined with significant leverage mean the entire fund is extremely dependent on a single narrative. As long as the assumption that "AI infrastructure continues to expand" holds true, everything runs smoothly.

But if the pace of AI development slows down, or if energy bottlenecks are bypassed by some technological breakthrough, the drawdown of concentrated positions could occur much faster than their accumulation. He’s not just betting on direction, but on timing. Once the timing is off, the consensus within the community could instead become a collective blind spot.

Back to the original question.

Everyone is analyzing his holdings, trying to replicate his trades. But the returns of a legendary investor like him come with structural conditions.

The paper is public, the position reports are public, and his investment logic is clearly explained in podcasts and interviews. But even if you fully understand every one of his judgments, you cannot replicate the position from which he made those judgments.

Positions can be traced back, and returns are enviable, but the source of insight cannot be shared. This is likely the most expensive form of asymmetry in this era.

Author: Curry, Shenchao TechFlow

Source: Shenchao TechFlow