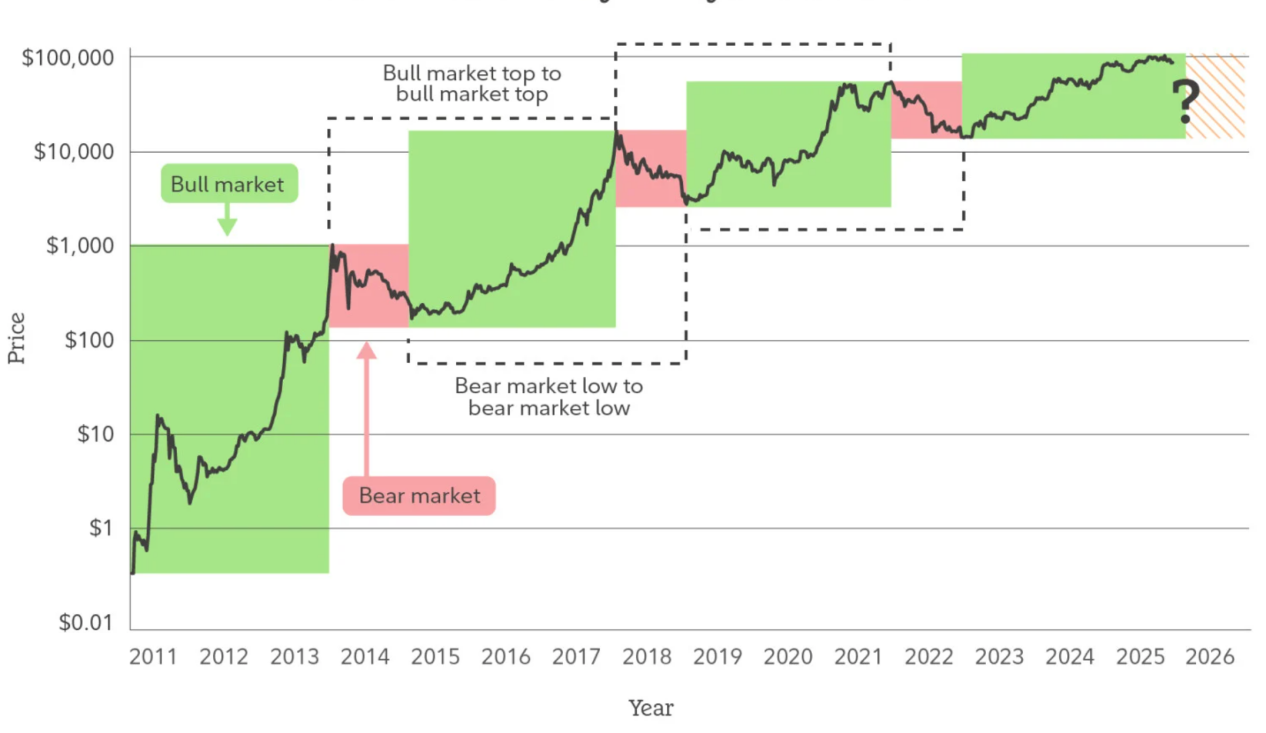

I. The Cycle Is Fading: Why We No Longer Use "Bull and Bear" to Understand the Crypto Market in 2026

For a considerable period of time, the crypto market was largely dominated by a single narrative: the "four-year bull and bear cycle." The halving events, liquidity inflection points, emotional bubbles, and price collapses were repeatedly validated as effective analytical tools, shaping the cognitive inertia of a generation of market participants. However, as the market moves beyond 2025, this once highly effective cyclical model begins to show a systematic decline in explanatory power: market sentiment no longer becomes polarized at key time points, corrections no longer come with widespread liquidity crunches, so-called "bull market launch signals" frequently fail, and price movements increasingly exhibit a coexistence of range-bound consolidation, structural differentiation, and gradual upward drift. This is not the market "becoming boring," but rather a sign that its underlying mechanisms are undergoing deep transformation.

The essence of the cyclical model relies on highly homogenized capital behavior: similar risk preferences, comparable holding timeframes, and high sensitivity to price itself. However, the cryptocurrency market around 2026 is gradually moving away from this premise. As regulatory channels open, institutional-grade custody and audit systems mature, and crypto assets are incorporated into broader asset allocation discussions, the marginal pricing forces in the market are changing. Increasingly, capital is entering the market not primarily for "timing trades," but with the goals of long-term allocation, risk hedging, or functional usage in mind. These types of capital do not chase extreme volatility; instead, they absorb liquidity during downturns and reduce turnover during upswings. Their very presence is weakening the emotional feedback loops that traditional bull and bear cycles depend on.

The essence of the cyclical model relies on highly homogenized capital behavior: similar risk preferences, comparable holding timeframes, and high sensitivity to price itself. However, the cryptocurrency market around 2026 is gradually moving away from this premise. As regulatory channels open, institutional-grade custody and audit systems mature, and crypto assets are incorporated into broader asset allocation discussions, the marginal pricing forces in the market are changing. Increasingly, capital is entering the market not primarily for "timing trades," but with the goals of long-term allocation, risk hedging, or functional usage in mind. These types of capital do not chase extreme volatility; instead, they absorb liquidity during downturns and reduce turnover during upswings. Their very presence is weakening the emotional feedback loops that traditional bull and bear cycles depend on.

More importantly, the increasing complexity within the structure of the crypto market is gradually dismantling the assumption of a unified cycle where all assets rise and fall together. The logical differences between Bitcoin, stablecoins, real-world assets (RWAs), layer-1 chain assets, and application-specific tokens are continuously widening. Their respective sources of funding, use cases, and methods of value anchoring are now difficult to be described by a single cyclical framework. As Bitcoin increasingly resembles a medium- to long-term store of value, stablecoins become the infrastructure for cross-border settlements and on-chain finance, and some application-based assets begin to be priced based on cash flows and real demand, the concepts of "bull market" or "bear market" themselves lose their meaning as a unified descriptive framework.

Therefore, the more reasonable way to understand the 2026 cryptocurrency market is not whether "the next bull market is beginning," but rather whether "the structural stages of different assets are changing." The cycle has not disappeared, but it is gradually shifting from being a core variable determining direction to a background factor influencing the pace. The market no longer experiences rapid resonance around a single central narrative, but instead evolves slowly amid multiple coexisting logics. This means that future risks will no longer be concentrated in the collapse of a single peak, but will instead manifest more in structural mismatches and cognitive lags. Similarly, opportunities will no longer come from betting on the overall market trend, but from the early identification of long-term trends and role differentiation.

From this perspective, the "failure" of cycles is not a cost of the crypto market's journey toward maturity, but rather a sign that it is beginning to move away from its early speculative nature and entering a stage of systematic assets. By 2026, the crypto market will no longer be defined in terms of bull and bear markets, but instead will need to be understood in terms of its structure, functionality, and timing to grasp its true operational state.

II. The Role Transformation of Bitcoin: From a Highly Volatile Asset to a Structural Reserve Instrument

If the cyclical logic is indeed losing its effectiveness, then Bitcoin's own role transformation is the most direct and explanatory manifestation of this change. For a long time, Bitcoin has been regarded as the most volatile asset in the crypto market, with the highest risk premium, where its price fluctuations were driven more by sentiment, liquidity, and narratives, rather than by stable usage demand or balance sheet structures. However, since entering 2025, this perception has gradually been revised: Bitcoin's price volatility has continuously declined, its drawdown patterns have become flatter, the stability of key support levels has significantly improved, and the market's sensitivity to short-term price fluctuations is diminishing. This is not a sign of waning speculative enthusiasm, but rather an indication that Bitcoin is being reclassified into a pricing framework more aligned with that of a "reserve asset."

The core of this transformation does not lie in whether Bitcoin is "more expensive," but rather in "who holds it and for what purpose." As Bitcoin gradually becomes part of the balance sheets of listed companies, long-term investment portfolios, and asset allocation discussions by certain sovereign or quasi-sovereign entities, the rationale for holding Bitcoin has shifted from profiting from price volatility to hedging against macroeconomic uncertainty, diversifying fiat currency risk, and gaining exposure to non-sovereign assets. Unlike the early market dominated by retail investors, these types of holders demonstrate greater tolerance for price pullbacks and stronger patience with time. Their behavior itself reduces the circulating supply of Bitcoin and lowers the overall market's sensitivity to selling pressure.

Meanwhile, the financialization path of Bitcoin is undergoing structural changes. Spot ETFs, compliant custody solutions, and a mature derivatives system have, for the first time, provided the infrastructure necessary for Bitcoin to be significantly integrated into the traditional financial system. This does not mean that Bitcoin has been fully "tamed," but rather that its risks are being repriced. Price discovery is no longer occurring entirely in the most emotionally extreme on-chain or offshore markets, but is gradually shifting toward deeper and more regulated trading environments. In this process, Bitcoin's volatility has not disappeared; instead, it has transformed from chaotic and disorderly swings into structured fluctuations driven by macroeconomic variables and the rhythm of capital flows.

More importantly, Bitcoin's "reserve asset" characteristics do not stem from any external credit endorsement, but rather from the repeated validation over time of its supply mechanism, immutability, and decentralized consensus. Against the backdrop of continuously expanding global debt, intensifying geopolitical tensions, and a more fragmented financial system, demand for "neutral assets" is on the rise. While Bitcoin does not need to fulfill traditional monetary functions, it is increasingly becoming, at the asset level, a value carrier that requires no counterparty credit, no policy commitments, and can be transferred across systems. This characteristic positions Bitcoin more as a structural reserve tool in asset allocation, rather than merely a high-risk speculative asset.

Therefore, by 2026, Bitcoin's value will no longer be appropriately measured by how quickly it rises in price, but rather by placing it within a longer-term framework of asset allocation and strategic positioning. Its core significance does not lie in replacing existing assets, but in offering the global financial system a new, decentralized reserve option. Precisely through this role transition, Bitcoin's influence on the crypto market is also changing: it is no longer merely the engine driving market trends, but is increasingly becoming a cornerstone of stability for the entire system. As this transformation continues to deepen, Bitcoin's mere existence may become more significant for the crypto market in 2026 and beyond than its short-term price performance.

Three, Stablecoins and RWA: The First Real Integration of the Crypto Market with the Real-World Financial System

If Bitcoin represents the "self-ownership" of assets within the crypto market, then the rise of stablecoins and real-world assets (RWA) marks the first systematic integration of the crypto market into the real-world financial system. Unlike previous growth driven by narratives, leverage, or token incentives, the core of this transformation lies not in emotional expansion, but in the continuous entry of real assets, real cash flows, and real settlement demands into the blockchain ecosystem. This shift is propelling the crypto market from a relatively closed, self-contained system toward an open structure deeply integrated with traditional finance.

The role of stablecoins has long transcended that of a "medium of exchange" or "safe-haven asset." As their scale continues to expand and use cases proliferate, stablecoins have effectively become a "blockchain mapping" of the global dollar system. They perform functions such as cross-border payments, on-chain settlement, capital management, and liquidity allocation, leveraging lower settlement costs, higher programmability, and cross-border accessibility. Particularly in emerging markets, foreign trade settlements, and high-frequency cross-border capital flows, stablecoins do not replace the existing financial system but instead address its structural shortcomings in efficiency and accessibility. This demand is not cyclical in nature, tied to bull or bear markets, but rather closely linked to global trade, capital flows, and the upgrading of financial infrastructure. Its stability and stickiness far exceed those of traditional crypto transactional demand. On top of stablecoins, the emergence of Real-World Assets (RWA) has further transformed the asset composition logic of the crypto market. By tokenizing real-world assets such as U.S. Treasury bonds, money market instruments, receivables, and precious metals on the blockchain, RWA introduces a long-missing element to the crypto market: a sustainable source of returns tied to the real economy. This means the crypto market, for the first time, is no longer entirely dependent on "price appreciation" to support asset value. Instead, it can now build value anchors closer to traditional finance through interest, rent, or operational cash flows. This shift not only enhances asset pricing transparency but also prompts on-chain capital to be reallocated based on "risk-return" considerations rather than a single narrative.

A deeper transformation is taking place: stablecoins and RWA (Real-World Assets) are reshaping the financial division of labor within the crypto market. Stablecoins provide the foundational settlement and liquidity infrastructure, RWA offer divisible, combinable, and reusable exposure to real-world assets, and smart contracts handle automated execution and risk control. Within this framework, the crypto market is no longer merely a "shadow market" of traditional finance but is beginning to independently support financial activities. The development of this capability is not an overnight occurrence but a gradual and continuous accumulation process as compliance, custody, auditing, and technical standards progressively improve. Therefore, stablecoins and RWA in 2026 should not be simply viewed as a "new sector" or a "thematic investment," but rather as a pivotal node in the structural upgrading of the crypto market. They enable the crypto ecosystem for the first time to coexist and interpenetrate with traditional finance in the long term, shifting the growth logic of the crypto market from cycle-driven to demand-driven, and from closed competition to open collaboration. In this process, what truly matters is not the short-term performance of individual projects, but the emergence of a new form of financial infrastructure within the crypto market. Its impact will extend far beyond price levels, profoundly reshaping the way global finance operates over the next decade.

Four, From Narrative-Driven to Efficiency-Driven: Collective Repricing at the Application Layer

After several cycles of narrative rotation, the application layer of the crypto market is entering a critical inflection point: valuation systems driven solely by grand visions, technical labels, or emotional consensus are systematically failing. The temporary retreat of DeFi, NFTs, GameFi, and even some AI narratives does not mean these directions lack inherent value, but rather that the market's tolerance for "future imagination premiums" has significantly declined. The application layer around 2026 is transitioning from a pricing system centered on stories to a new pricing logic focused on efficiency, sustainability, and real usage intensity.

The essence of this transformation lies in the changing structure of participants in the crypto market. As the proportion of institutional capital, industrial capital, and hedge funds increases, the market no longer focuses solely on "whether a sufficiently large narrative can be told," but instead pays more attention to "whether a real problem is genuinely solved, whether there are cost or efficiency advantages, and whether the project can sustain itself without subsidies." Under this new framework of scrutiny, many previously overvalued applications are being repriced, while a few protocols that demonstrate advantages in efficiency, user experience, and cost structure are instead receiving more stable capital support.

The core manifestation of efficiency-driven development is that the application layer is beginning to compete around metrics such as "output per unit of capital" and "contribution per user." Whether it's decentralized trading, lending, payments, or fundamental middleware, the market's focus is shifting from broad indicators like TVL (Total Value Locked) and the number of registered users toward more refined metrics such as transaction depth, user retention rate, fee revenue, and capital turnover efficiency. This means that applications are no longer just "narrative decorations" within a blockchain ecosystem, but are instead becoming self-sustaining, independent economic entities with clear business logic. For applications that cannot generate positive cash flow or are heavily reliant on incentive subsidies, the weight of "future expectations" in their valuation is being rapidly compressed.

Meanwhile, technological advancements are amplifying efficiency differences and accelerating the differentiation of the application layer. The maturation of account abstraction, modular architecture, cross-chain communication, and high-performance Layer 2 solutions has made user experience and development costs quantifiable and comparable metrics. In this environment, the migration costs for users and developers continue to decline, and applications no longer possess "natural moats." Only products that offer significant advantages in performance, cost, or user experience can retain traffic and capital. This competitive landscape is inherently unfavorable for projects that rely on narratives to maintain premiums, but it provides long-term viability for truly efficient infrastructure and applications.

More importantly, repricing at the application layer does not occur in isolation but resonates with stablecoins, RWA (Real-World Assets), and the evolving role of Bitcoin. As on-chain activities begin to accommodate more real-world economic activity, the value of applications is no longer derived from "circular games within the crypto ecosystem," but rather from their ability to efficiently handle real capital flows and genuine demand. This shift causes applications that serve payment, settlement, asset management, risk hedging, and data coordination to gradually replace purely speculative applications, becoming the core focus of the market. This change does not mean that risk appetite in the market has completely disappeared, but rather that the allocation of risk premiums has shifted—from narrative-driven diffusion to efficiency-driven realization.

Therefore, the "collective repricing" of the application layer in 2026 is not a short-term shift in market style, but rather a structural revaluation. It marks the gradual transition of the crypto market away from its heavy reliance on sentiment and narratives, toward core evaluation criteria such as efficiency, sustainability, and real-world applicability. In this process, the application layer will no longer be the most volatile component of the cycle, but may instead become a key bridge connecting the crypto market with the real economy. Its long-term value will increasingly depend on whether it can genuinely integrate into the global digital economy's operational framework.

V. Conclusion: 2026 is not the beginning of a new bull market, but the start of the next decade.

Trying to understand the 2026 cryptocurrency market by asking "When will the next bull market come" itself indicates that one is operating within an analytical framework that is already becoming obsolete. The more significant meaning of 2026 does not lie in whether prices reach new highs again, but rather in the fact that the crypto market will have completed a fundamental shift in underlying understanding and structure: it will begin to transition from a marginal market heavily reliant on cyclical narratives, emotional contagion, and liquidity-based speculation, toward a long-term infrastructure system that is integrated into the real financial system, serves genuine economic needs, and gradually establishes institutionalized operational logic.

This transformation is first reflected in the shift of market objectives. Over the past decade, the core issue for the crypto market was "how to justify its existence," but after 2026, this question is being replaced by "how to operate more efficiently, how to integrate with real-world systems, and how to support larger volumes of capital and users." Bitcoin is no longer merely a high-volatility risk asset but is beginning to be incorporated into structural reserves and macro-level asset allocation frameworks. Stablecoins are evolving from transactional mediums into key conduits for digital dollars and digital liquidity. Meanwhile, RWA (Real-World Assets) marks the first time the crypto system is genuinely integrated with the global debt, commodity, and settlement networks. These changes may not trigger dramatic price surges in the short term, but they will define the boundaries and potential of the crypto market over the next decade.

More importantly, 2026 marks the completion of a "paradigm shift," not its beginning. The crypto market is transitioning from a cycle-based game to a structural one, from narrative-driven pricing to efficiency-driven pricing, and from a closed, crypto-internal loop to a deep integration with the real economy. A new value evaluation system is emerging. Within this system, whether an asset has long-term allocation value, whether a protocol can continuously generate cash flows, and whether an application genuinely improves financial and collaborative efficiency are becoming more important than whether a narrative is "sufficiently attractive." This means that future bull markets will be more differentiated, slower, and more path-dependent. At the same time, it also means that the probability of a systemic collapse is decreasing.

From a historical perspective, what truly determines the fate of an asset class has never been the height of a particular bull market, but rather whether it successfully transforms from a speculative commodity into an infrastructure. The cryptocurrency market in 2026 is at just such a pivotal turning point. Prices will still fluctuate, and narratives will continue to evolve, but the underlying structure has already changed: crypto is no longer merely a "replacement fantasy" for traditional finance, but is becoming part of its extension, complement, and even redefinition. This transformation means that the cryptocurrency market over the next decade will more closely resemble a slow but steadily expanding main trend, rather than a series of emotion-driven, impulsive price surges.

Therefore, rather than asking whether 2026 marks the beginning of a new bull market, it is more accurate to recognize it as a "coming-of-age" moment — the first time the crypto market has redefined its role, boundaries, and mission in a way closer to traditional financial systems. The real opportunities may no longer belong to those most skilled at chasing cycles, but rather to those who can understand structural changes, adapt to the new paradigm in advance, and grow alongside this system in the long term.