Original Author: RockFlow

Original article link:

Highlight the key points

① Over the past two decades, the internet has reshaped the world, but it has also led investors into the trap of "bits devouring atoms." For a long time, non-ferrous metals have been regarded as a "traditional industry." However, by 2026, industrial metals are no longer merely cyclical stocks at the mercy of market forces, but rather "priority beneficiaries" as the physical foundation of AI.

② We are at the singularity of a major energy medium transition: copper, as the "vascular system" of computing power, faces grade deflation; aluminum, as "solidified electricity," enjoys substantial premiums; tin, through semiconductor packaging miniaturization, becomes a silent tax; and nickel regains valuation sovereignty with the return of high-nickel batteries. A "perfect storm" has already formed on both supply and demand sides. The production lag caused by a decade-long capital expenditure gap is causing existing mineral resources to generate even greater value.

③ By 2026, the key to success in investing in non-ferrous metals will no longer be capturing short-term price fluctuations, but rather securing scarce resources. Freeport-McMoRan (FCX) sets an ultra-low cost benchmark comparable to early energy giants, while Alcoa (AA) fully capitalizes on energy arbitrage. Against the backdrop of fluctuating U.S. dollar credit, heavily investing in the physical world and embracing non-ferrous metals is not only a must for asset hedging, but also a ticket to participating in the AI revolution.

In the narrative of the past two decades, most investors have been immersed in the illusion that "bits" would consume "atoms," firmly believing that software defines everything and that algorithms are sufficient to reconstruct the world.

However, as of 2026, reality has led more investors to realize again: the foundation of AI is not just code, but electricity; and the foundation of electricity is not only energy, but also non-ferrous metals such as copper, aluminum, tin, and nickel.

As the computing power competition among tech giants intensifies, major commodities such as copper, aluminum, tin, and nickel are quietly initiating a long-overdue revaluation of their value. What we are experiencing is not merely another super cycle for industrial metals, but rather a battle for pricing power over industrial commodities.

In this article, the RockFlow investment research team will outline the 2026 non-ferrous metals allocation strategy for U.S. investors, covering topics such as paradigm shifts in the non-ferrous metals sector, in-depth value analysis of copper, aluminum, tin, and nickel, and multi-dimensional analysis of major non-ferrous metal companies.

1. In-depth Analysis of the Four Major Non-Ferrous Metals: Searching for Physical Alpha in the AI Era

For a long time, non-ferrous metals have been regarded as a "traditional industry." The market has become accustomed to focusing on real estate commencement rates, infrastructure growth rates, and home appliance shipments to retroactively estimate demand.

But by 2026, holding an old map will no longer help us find new routes. We are currently experiencing a "energy medium migration": shifting from chemical energy based on "molecules" (carbon, hydrogen) to physical energy based on "atoms" (copper, aluminum, tin, nickel).

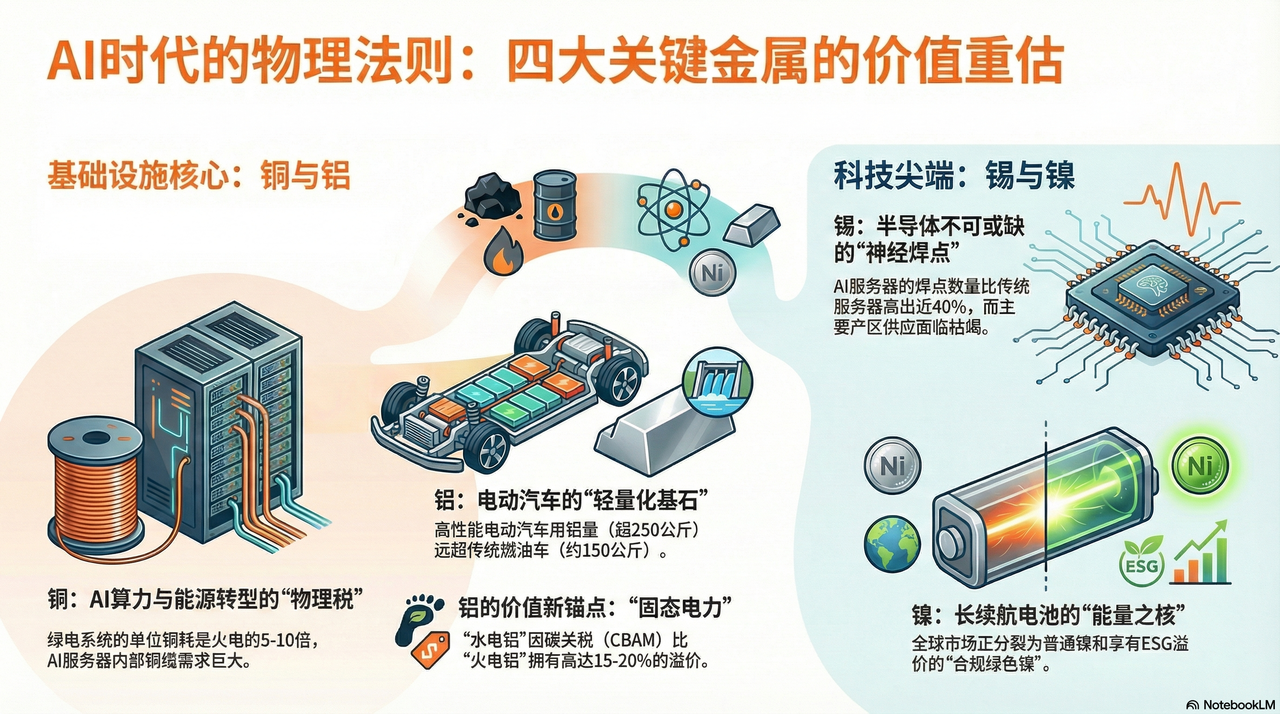

If copper is the irreplaceable "blood vessel" of this migration, then aluminum, tin, and nickel respectively form the skeleton, nerves, and heart of the modern industrial system.

Copper: The "Physical Infrastructure Tax" of AI and the Energy Transition

If everyone is competing for GPUs in 2024 and 2025, then in 2026, global giants will be vying for shares of copper mines.

The development cycle of a copper mine can last 10 to 15 years. Currently, major global copper mines (such as Escondida in Chile) are facing an inevitable decline in ore grade. Twenty years ago, one ton of ore could yield 10 kilograms of copper, but now it only yields 4 kilograms. This means mining companies must extract twice as much ore to maintain the same level of production—this is a deflationary challenge at the physical level that cannot be resolved.

If oil is the blood of the industrial era, then copper is the nerves and blood vessels of the digital age. It is the only material that is widely available, cost-effective, and highly conductive, making it a critical and increasingly difficult bottleneck in the AI computing power and new energy revolutions.

In the past, the market believed that data centers were undergoing a transition from "copper to optical," assuming that long-distance optical transmission would inevitably replace copper cabling. However, in the face of NVIDIA's Blackwell (GB200) and even subsequent architectures, the laws of physics are beginning to push back.

To achieve ultra-low latency and reduce cooling power consumption, server racks are increasingly returning to the use of DACs (Direct Attach Cables) for internal connectivity on a large scale. At very short distances, the latency and energy consumption caused by optical-electrical conversion have become a bottleneck for AI inference. Inside each GB200 NVL72 rack, the total length of copper cabling can reach several miles.

This means that for every high-performance chip that a tech giant purchases, they are not only paying NVIDIA, but also effectively paying a "physical foundation tax" to global copper mine owners. The stronger the computing power, the more pronounced the "black hole effect" of copper becomes.

Aluminum: "Solid Electricity" in the Decarbonization Era and Structural Premium

If the demand for copper stems from its conductivity, then the long-term bullish logic for aluminum is rooted in its dual attributes as the "foundation of lightweighting" and an "energy carrier."

Under the global carbon reduction narrative by 2026, the demand curve for aluminum has completely decoupled from real estate. To offset the heavy weight of batteries and improve driving range, electric vehicles (EVs) are undergoing a comprehensive "aluminumization" revolution.

According to relevant data, traditional internal combustion engine vehicles use about 150 kg of aluminum per vehicle, while high-performance electric vehicles have exceeded 250 kg. In particular, Tesla's pioneering "gigacasting" technology integrates dozens of steel components in the vehicle chassis into a single large aluminum alloy casting. This is not only a technological advancement, but also a cross-dimensional substitution of aluminum for steel. By 2026, the increased demand for aluminum in the automotive industry alone will be sufficient to offset the decline in traditional construction sectors.

On the supply side, aluminum production is an extremely electricity-intensive process, requiring about 14,000 kilowatt-hours to produce one ton of aluminum. Therefore, aluminum is also called "solidified electricity."

In 2026, global electricity prices experience significant fluctuations due to geopolitical tensions and the energy transition. At this time, aluminum companies (such as Alcoa, AA) with self-sufficient clean energy (e.g., hydropower) build formidable moats. Against the backdrop of the implementation of carbon border adjustment mechanisms (CBAM), each ton of "hydropower aluminum" commands a premium of approximately 15%-20% over "thermal power aluminum."

The rise in aluminum prices essentially reflects a cost adjustment following the disappearance of cheap electricity globally.

Tin: The "Nerve Endings" Behind the Semiconductor Boom

If copper is the blood vessel, then tin is the solder joint acting as the nervous system in the electronic world. It is the indispensable "adhesive" for all electronic components, a characteristic that makes it a direct beneficiary of the semiconductor cycle.

Fifty percent of the world's tin is used in electronic solder. In the first year of AI inference (2026), the increasing complexity of hardware architecture will lead to a "second surge" in tin consumption. Taking high-performance servers as an example, NVIDIA's Blackwell architecture employs Chiplet packaging technology, which causes the density of logical interconnections on a single processor to increase exponentially.

According to research, the number of solder joints inside AI servers is nearly 40% higher than that in traditional general-purpose servers. This means that no matter how underlying architectures evolve, as long as electromigration continues, tin remains that unavoidable "silent tax."

At the same time, the supply of tin is highly concentrated in Indonesia, Myanmar, and Peru. By 2026, the Wa State region in Myanmar—once a major hub supplying 10% of the global tin production—will experience a drastic decline in output due to resource depletion from long-term over-mining. Meanwhile, Indonesia, following the example of its nickel export ban, will strictly restrict the export of raw tin.

Under this mismatch of "historically low inventory plus a surge in demand due to product replacement," tin prices are experiencing a sharp rise that has decoupled from the macroeconomic cycle. It is currently the metal with the tightest supply-demand balance and the greatest upward potential among non-ferrous metals.

Nickel: The "Energy Core" of Power Batteries

The nickel narrative hit a low in 2024-2025 due to oversupply from Indonesia, but in 2026, nickel regained its valuation dominance as demand for high energy density returned.

Although LFP (lithium iron phosphate) batteries are popular in the mid-to-low-end market, high-nickel ternary batteries (such as NCM811) will remain the "pillar for long-range performance" in the global premium passenger vehicle market by 2026.

In order to achieve a single-charge driving range of 1,000 kilometers, automakers must continuously increase the proportion of nickel. Behind every long-range electric vehicle lies a consumption of 50-70 kg of high-purity first-grade nickel. This extreme pursuit of "energy density" has effectively eliminated the downward potential for nickel demand.

In 2026, the pricing power for nickel ore is undergoing a second shift.

Western giants (such as Vale) are using ESG criteria to build non-tariff barriers. The governments of Europe and the United States have started imposing carbon tariffs on nickel from Indonesia that relies on coal power and causes high environmental pollution. This has led to the global nickel market splitting into two parallel worlds: one is low-cost, high-carbon primary nickel, and the other is "compliant green nickel" that commands a premium and enters the supply chains of Europe and the United States.

This structural shortage has given compliant manufacturers with top-tier mining rights unprecedented bargaining power.

2. Dissecting the Commodity Giants: Who Holds the "Physical Moat"?

At the special juncture in 2026, where resource inflation intertwines with the AI computing power revolution, investing in non-ferrous metals is no longer simply a matter of "betting on the cycle." The RockFlow investment research team believes that we need to deeply understand the industry giants and seek out true Alpha opportunities that possess a "physical moat."

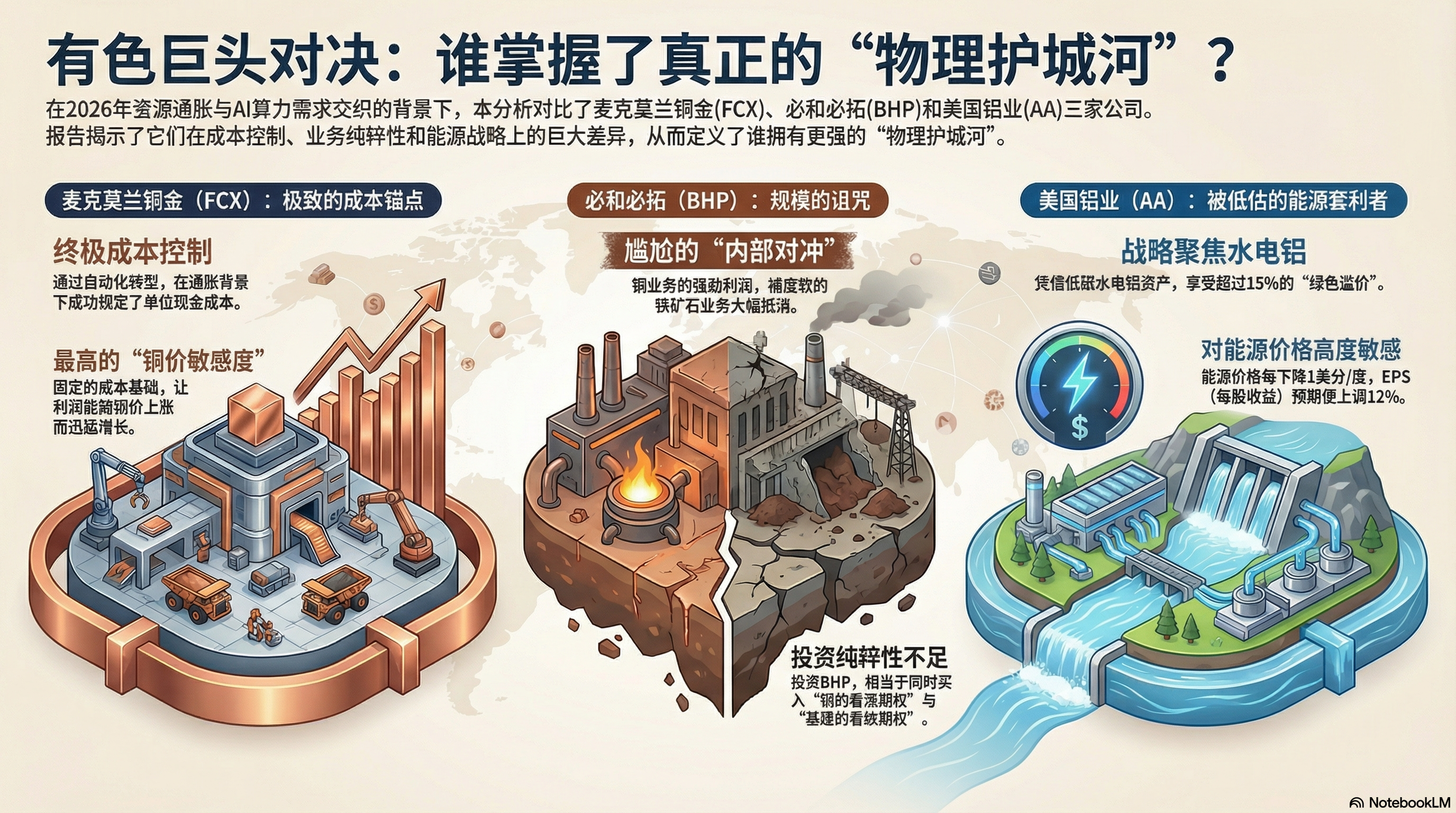

Freeport-McMoRan Copper & Gold (FCX) vs. BHP Billiton (BHP)

In the U.S. copper industry portfolio, FCX and BHP are two unavoidable major players. However, through an in-depth analysis of their 2025 fiscal year annual reports and 2026 Q1 outlooks, we find that their underlying logics have significantly diverged.

FCX: Ultimate "Cost Anchor" and Operating Leverage

The core reason the market is aggressively chasing Freeport-McMoRan (FCX) in 2026 is not because it has extracted more copper, but because of its demonstrated ability to control costs amid inflationary pressures.

Grasberg in Indonesia is one of the world's largest gold and copper mines. In 2025, Freeport-McMoRan (FCX) completed the transition from open-pit mining to fully automated underground mining. This transition has led to a significant reduction in energy consumption per unit and labor costs.

According to the financial report, FCX has successfully locked in its unit net cash cost. Against the backdrop of rising global labor and energy costs in 2026, this is essentially a form of "inflation hedge."

Due to its fixed cost structure, FCX's operating profit margin is expected to surge rapidly when copper prices rise. It is currently the U.S. stock with the highest "copper price sensitivity" and the cleanest balance sheet.

BHP: The Curse of Scale and the Burden of Iron Ore

As the world's top mining company by market value, BHP's financial report reveals an awkward form of "internal hedging."

Although BHP's copper business is expanding continuously in Chile and Australia, its iron ore business, which accounts for about 50% of its revenue, is facing a systemic crisis. The excess profits generated by BHP's internal copper operations are largely offset by the weak performance of its iron ore profits.

For investors seeking the premium of "AI computing power fuel," buying BHP is equivalent to purchasing a "copper call option" plus a "traditional infrastructure put option." This impurity makes BHP significantly underperform FCX in terms of alpha returns.

Alcoa (AA): An Undervalued "Energy Arbitrage" Giant

The key to success or failure for aluminum companies lies in energy costs.

In 2025, AA made a highly strategic move: it decisively shut down inefficient smelters located in regions with high electricity prices and instead increased its investment in hydropower-based aluminum production bases in Iceland, Norway, and Australia. Against the backdrop of the Carbon Border Adjustment Mechanism (CBAM) being officially implemented in 2026, low-carbon aluminum (produced using hydropower) commands a green premium of 15% to 20% over aluminum produced using thermal power.

According to the financial outlook, AA's performance shows a high sensitivity to energy prices. The financial model indicates that for every 1 cent per unit decrease in average energy prices, its expected EPS (Earnings Per Share) would increase by 12%. As the cost of integrating renewable energy into the global grid continues to decline, AA is quietly benefiting from an "energy dividend."

3. 2026 Positioning Strategy: A Shift from "Paper Assets" to "Tangible Sovereignty"

By 2026, industrial metals are no longer merely cyclical stocks at the mercy of market trends; they have become "priority beneficiaries" of the physical infrastructure underpinning AI. Under the dual pressures of U.S. dollar credit volatility and a surge in physical demand, investors' strategies should shift from "speculating on price differentials" to "securing scarce resources."

In the view of RockFlow's investment research team, the recent rise in non-ferrous metal prices is not a replay of the previous cycle. There are three long-term bullish reasons:

1. A Decade-Long Gap in CapEx (Capital Expenditure): Over the past ten years, mining companies have been focused on repairing their balance sheets, resulting in exploration spending at only 30% of the 2011 level. The lag in physical production has a rigid and irreversible 3-5 year time frame.

2. Physical hedging against the dollar hegemony: Central banks worldwide are undergoing a process of "tangible assetization." Metals are no longer merely industrial raw materials; they are regaining the attributes of reserve currencies.

3. The Reverse Moat of ESG: Strict environmental approvals make it nearly impossible to start new mining operations. This means that existing compliant mines have become rare assets, and their premium will persist in the long term.

We recommend the following U.S. stock allocation strategies:

Core Configuration (Ballast Stone): FCX + RIO

- FCX (Freeport-McMoRan): A pure-play copper leader, enjoying an absolute premium driven by data computing infrastructure.

- Rio Tinto (RIO): Although it also has iron ore assets, RIO conducted large-scale mergers and acquisitions of secondary copper and lithium assets in 2025. Its extremely strong cash flow and high dividend policy make it the best choice for hedging against macroeconomic volatility.

Target of attack: AA

- Alcoa (AA): Benefiting from energy arbitrage opportunities and the surge in demand for lightweight materials, its profit elasticity ranks first among the non-ferrous metal sector.

Defensive target: VALE

- Vale (VALE): The market still views it primarily as an iron ore producer. However, Vale holds the world's top-tier nickel resources. With the resurgence of high-nickel batteries in long-range solutions, Vale is approaching a singularity of value re-estimation.

Conclusion: Embrace "Atoms," Invest Heavily in the Physical World

Storage investments have taught us a lesson: whoever controls the bottleneck controls the premium. Storage chips are the bottleneck in the digital world, while non-ferrous metals are the bottleneck in the physical world.

By 2026, non-ferrous metals have already become the "HBM" (High Bandwidth Memory) of the physical world. The RockFlow investment research team believes that being optimistic about non-ferrous metals and heavily weighting investments in the physical world will become a major investment theme this year. They not only serve as a hedge against inflation but also represent the entry ticket to the AI revolution.