Real World Asset (RWA) Tokens with Potential Massive Upside in H2 2026

2026/07/15 15:42:00

Introduction

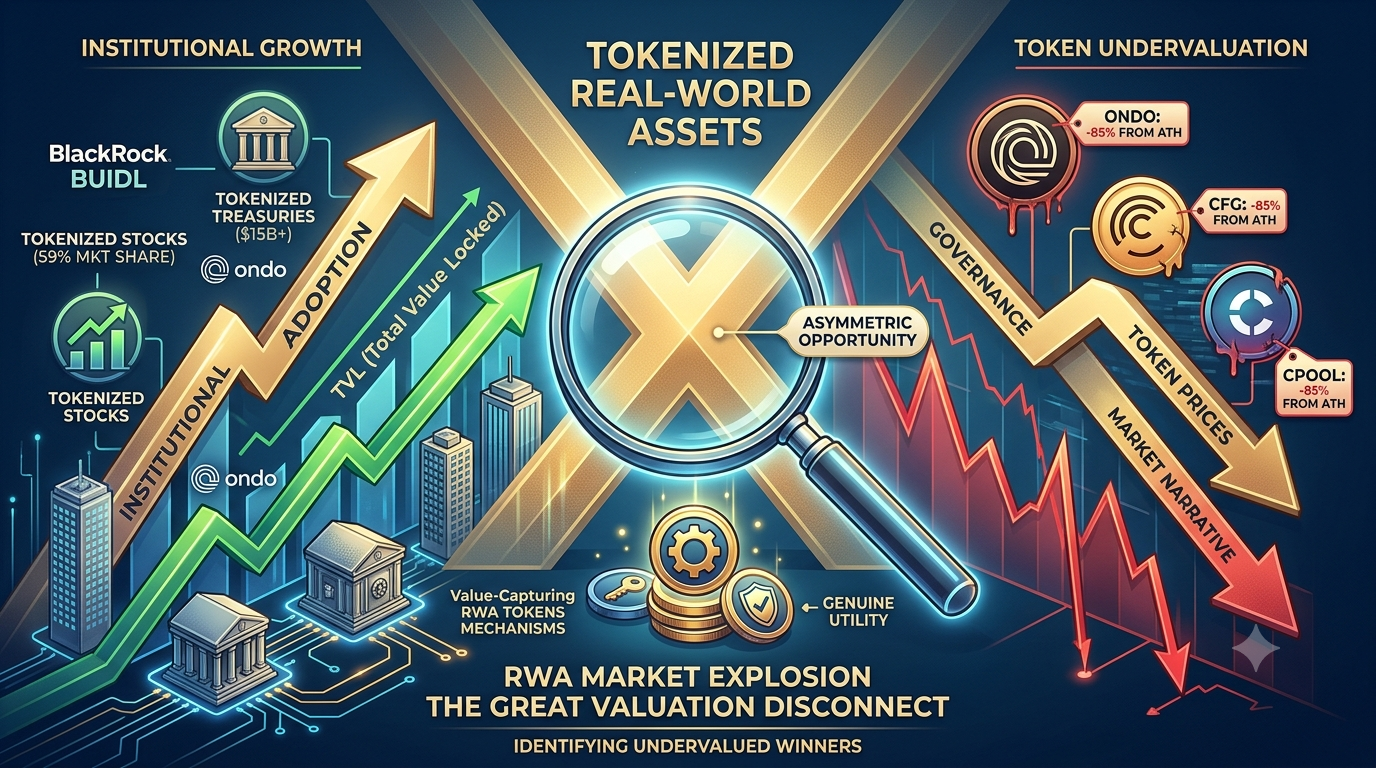

The tokenized real-world asset (RWA) market hit $26 billion in early 2026. BlackRock's BUIDL fund alone holds $2.9 billion in tokenized U.S. Treasuries. Ondo Finance commands 54.4% market share in tokenized stocks. JPMorgan, Mastercard, and Fidelity are all building on-chain.

Yet here is the paradox: while institutional RWA adoption is accelerating faster than ever, the governance tokens powering these protocols are trading at historic discounts. ONDO is down 85% from its all-time high even as its TVL hit a new all-time high above $2.5 billion. Centrifuge (CFG) trades near $0.17 despite being one of the only live bridges between real-world invoice financing and on-chain liquidity.

This disconnect—between booming platform fundamentals and deeply depressed token valuations—is what creates asymmetric opportunity. This article breaks down the RWA landscape across three core verticals (tokenized Treasuries, real estate, and stocks), identifies the most undervalued tokens with genuine institutional traction, and provides a framework for separating the next cycle's winners from governance tokens that will never capture value.

The RWA Market in Numbers: Why This Sector Is Inevitable

Before diving into specific tokens, understand the macro force driving this sector. Tokenized RWAs are not a crypto-native narrative—they are a Wall Street infrastructure upgrade.

|

RWA Category

|

Tokenized Value (2026)

|

Key Players

|

Growth Driver

|

|

U.S. Treasuries

|

$15 billion+

|

BlackRock BUIDL ($2.9B), Ondo USDY ($650M+), Franklin Templeton BENJI ($700M+)

|

Institutional yield demand, 24/7 settlement

|

|

Tokenized commodities

|

$7 billion (gold 70%)

|

Tether Gold (XAUt), Paxos Gold (PAXG)

|

Inflation hedge, on-chain portability

|

|

Private credit & lending

|

$5–8 billion

|

Maple Finance ($2.1B TVL), Centrifuge, Clearpool

|

Undercollateralized institutional lending

|

|

Tokenized real estate

|

Growing rapidly

|

Lofty, RealT, Propy

|

Fractional ownership, global access

|

|

Tokenized equities

|

$441 million (ATH)

|

Ondo Global Markets (59% share), Robinhood Chain

|

SEC framework developing, 24/7 trading

|

|

Stablecoins (fiat-backed)

|

$230 billion+

|

USDT, USDC

|

Foundation of all RWA settlement

|

The total tokenized RWA market (excluding stablecoins) is projected to exceed $50 billion by year-end 2026 and potentially $100+ billion within 18–24 months. BlackRock CEO Larry Fink has publicly stated that tokenization "will be the next generation for markets." The CLARITY Act advancing through the U.S. Congress provides a federal framework for digital assets.

The opportunity for token investors is not whether RWA tokenization will grow—it will. The question is which tokens are positioned to capture that growth versus merely existing alongside it.

Sector 1: Tokenized Treasuries & Institutional Yield

This is the largest and most mature RWA vertical. Tokenized U.S. Treasury products exceeded $11 billion in on-chain value by early 2026, up from under $1 billion in early 2024—a 10x increase in under two years.

Ondo Finance (ONDO) — The Pure-Play RWA Leader at an 85% Discount

Ondo Finance is the closest thing to a pure-play RWA infrastructure investment in crypto. It operates two distinct businesses, both growing:

1. Tokenized Treasuries (OUSG + USDY): OUSG holds $680 million in tokenized U.S. Treasuries, backed by BlackRock's BUIDL fund alongside allocations to Franklin Templeton, WisdomTree, Fidelity, and Wellington. USDY, a yield-bearing stablecoin alternative, offers ~4.8% APY and has generated over $1.5 billion in cumulative DEX volume.

2. Ondo Global Markets (Tokenized Stocks): The platform crossed $1.5 billion in TVL by May 2026 and commands approximately 59% market share in tokenized equities. Through its acquisition of Oasis Pro in late 2025, Ondo secured SEC licenses covering alternative trading system and broker-dealer operations. EU regulatory approval allows tokenized stock and ETF offerings across 30 European markets.

Why it looks undervalued:

-

Platform TVL hit an all-time high above $2.5 billion in January 2026 while the token traded 80% below its peak

-

Ondo is the single largest holder of BlackRock BUIDL through OUSG—the two are partners, not competitors

-

JPMorgan, Mastercard, and Ripple have all integrated with Ondo infrastructure

-

The July 2026 launch of SEC-aligned tokenized equities (BlackRock's IVV ETF, Micron stock on Ethereum) represents a genuine first in regulatory-compliant on-chain securities

The catch: ONDO is a governance token with limited direct value capture. Platform revenue flows to the business, not token holders. With 4.87 billion tokens circulating of a 10 billion max supply, unlock pressure continues. The bull case to $1.50–$4 by 2030 requires the DAO to deploy fee distribution or buyback mechanisms. Without that, even strong platform growth may not translate to token appreciation.

Maple Finance (SYRUP) — Institutional Lending with Revenue-Backed Buybacks

Maple Finance is the largest institutional lending venue in DeFi. Unlike Aave or Compound, which require overcollateralization, Maple connects vetted institutional borrowers (market makers, trading firms, crypto funds) with lenders through professional credit underwriters.

The key product is syrupUSDC—a permissionless, yield-bearing token that packages institutional lending yields into a format anyone can hold without KYC. Backed by over $2.1 billion in TVL, syrupUSDC offers exposure to real loan interest rather than token emissions.

Why the SYRUP token matters:

In 2025, governance approved MIP-019, redirecting 25% of protocol revenue toward SYRUP buybacks via the Syrup Strategic Fund (SSF). This directly ties token value to protocol performance. With Maple targeting $100 million in annualized revenue by 2026, the buyback mechanism creates sustained demand pressure proportional to protocol growth.

The conversion from MPL to SYRUP (at 100:1) completed in May 2025, and Binance listed SYRUP in the same month. The token now has genuine utility: governance participation and exposure to protocol revenue through the buyback program.

Sector 2: Tokenized Real Estate — Fractional Ownership Goes On-Chain

Real estate is the world's largest asset class at $280+ trillion, yet it remains notoriously illiquid, inaccessible, and burdened by intermediaries. Tokenization promises to change that—and several platforms are already live with working products.

Lofty — Daily Rental Yields on the Blockchain

Lofty tokenizes U.S. rental properties on Algorand, breaking single-family homes into $50 fractional tokens. Investors receive daily rental payouts in stablecoins, with historical yields ranging from 8–12% depending on the property.

By mid-2025, Lofty had onboarded 150+ properties across 40 U.S. markets, generating $50 million in tokenized value. The platform offers a functioning secondary market for token trading—an important liquidity feature that competitors lack.

The investment angle: Lofty does not have a tradeable governance token. Exposure comes through holding property tokens directly. For crypto investors seeking yield outside of DeFi's volatility, Lofty's daily rental distributions offer a genuine alternative. The platform's planned DeFi yield farming partnerships for 2026 could boost tokenized holdings to 12–15% APR.

RealT — The Pioneer with Current Headwinds

RealT is the longest-running tokenized real estate platform, operating since 2019 on Gnosis and Ethereum. It tokenizes U.S. residential rental properties with minimum investments starting at ~$50, distributing rental income weekly.

Caution is warranted in 2026. RealT has suspended almost all weekly distributions amid Detroit portfolio litigation issues. The platform's legal structure is being tested, and the outcome remains uncertain. While RealT's operational history provides credibility, current investors should treat distributions as paused until operational clarity returns.

Parcl (PRCL) — Real Estate Price Exposure Without Property Ownership

Parcl offers a different approach: instead of tokenizing individual properties, it creates synthetic exposure to real estate price indices for major cities (New York, Miami, San Francisco) on Solana. Users can long or short city-level housing markets without owning physical property.

With a $16 trillion+ addressable market for tokenized real estate speculation, Parcl represents a bet on price discovery infrastructure rather than property management. The Polymarket partnership launched in 2026 adds prediction market dynamics to real estate exposure.

The investment angle: PRCL token trades at a fraction of its launch valuation. If tokenized real estate speculation gains traction, Parcl's first-mover position in city-index trading could be valuable. The risk is that the product is complex and user adoption remains limited compared to direct property tokenization platforms.

Sector 3: Tokenized Stocks & Equity Infrastructure

This is the newest and most explosive RWA vertical. Ondo Global Markets' $1.5 billion TVL in tokenized stocks was built in months, not years. Robinhood Chain's July 2026 mainnet launch added immediate momentum with stock tokens for NVDA, GOOG, and AAPL trading on-chain 24/7.

Chainlink (LINK) — The Oracle Infrastructure Powering All RWAs

Chainlink is not an RWA token in the narrow sense. But it is the critical infrastructure layer that makes virtually all RWA tokenization possible.

Every tokenized Treasury product, every stock token, every real estate price feed on-chain requires an oracle to bring off-chain price data on-chain securely. Chainlink's Data Streams and Proof of Reserve products are the industry standard.

Key RWA-specific integrations:

-

Robinhood Chain: Chainlink is the official oracle for all stock token price feeds

-

Ondo Finance: Chainlink oracles power OUSG and USDY pricing

-

BlackRock BUIDL: Price verification and proof of reserve

-

JPMorgan: Chainlink's CCIP (Cross-Chain Interoperability Protocol) used for tokenized asset settlement

At $8.39, LINK is down significantly from its 2024 highs near $50. But unlike speculative altcoins, Chainlink generates real protocol revenue from oracle services and has a $15 billion+ secured value that grows as RWA adoption expands. The recent rebrand and v0.2 staking upgrade create additional demand drivers for the token.

Sector 4: Private Credit & Undercollateralized Lending

This is where DeFi meets real-world lending—without requiring borrowers to post 150% collateral in crypto. Instead, lending decisions are based on creditworthiness, real-world cash flows, and off-chain assets.

Centrifuge (CFG) — Invoice Financing on Chain

Centrifuge is one of the oldest and most operationally proven RWA protocols. It enables businesses to finance real-world assets—invoices, real estate mortgages, revenue-based financing—by tokenizing them on-chain and using them as collateral in DeFi lending pools.

Why CFG at $0.175 is deeply undervalued:

-

Centrifuge has actual loans originated and repaid over multiple years—rare in the RWA space where most projects are still building infrastructure

-

The protocol bridges traditional invoice financing (a $3 trillion global market) with on-chain liquidity

-

Tinlake pools allow investors to earn yield from real-world business cash flows, not speculative token appreciation

-

CFG is the governance token for protocol parameters, collateral types, and fee structures

-

At $0.175, CFG has retraced approximately 99% from its all-time highs near $15+

The catch: Like most RWA tokens, CFG has limited direct value capture. The protocol generates fees, but fee distribution to token holders has been minimal. The bull case requires governance to evolve toward revenue sharing as protocol volume scales.

Clearpool (CPOOL) — Institutional Credit with $937M Originated

Clearpool is an institutional DeFi lending protocol that has originated over $937 million in loans to borrowers including Jane Street, one of the world's largest market makers. The protocol has paid out $10 million+ in lender yield and maintains $51 million in TVL.

Key 2026 developments:

-

PayFi launch: Credit for stablecoin payments, targeting real-world fintech flows

-

cpUSD: A yield-bearing stablecoin backed by institutional lending pools

-

XDC Network validator: Clearpool joined as a validator in May 2026, deepening RWA sector ties

-

H2 2026 expansion: Planned network expansion targeting untapped institutional capital

Why CPOOL at $0.0023 is asymmetric:

-

The token is down 99.9% from its ATH near $2.50, yet protocol fundamentals (loan originations, lender yield, institutional borrower base) remain operational

-

$18 million market cap vs. $937 million in loans originated creates a loans-to-market-cap ratio of 52:1—extraordinarily high

-

Sequoia, Arrington Capital, Hashkey Group, Wintermute, Jane Street, and Flow Traders are all investors or partners

-

Exchange delistings (BloFin removed CPOOL/USDT in March 2026) have created a liquidity crunch that suppresses price below fundamentals

The risk: CPOOL's liquidity is thin. The H2 2026 expansion and any new exchange listings are critical catalysts. Without them, the token can remain depressed regardless of protocol growth. This is a high-conviction, small-position bet.

The Valuation Disconnect: Why RWA Tokens Are Undervalued

Here is the central paradox of RWA investing in 2026:

|

Metric

|

Platform Level

|

Token Level

|

|

Tokenized Treasury market

|

$15B+ and growing

|

ONDO down 85% from ATH

|

|

Ondo TVL

|

ATH above $2.5B

|

ONDO near cycle lows

|

|

Maple TVL

|

$2.1B

|

SYRUP below launch price

|

|

Clearpool loans originated

|

$937M

|

CPOOL down 99.9%

|

|

Centrifuge operational history

|

Multi-year

|

CFG down 99%

|

|

RWA total market

|

$26B → $50B+ projected

|

Most RWA tokens at historical lows

|

This disconnect exists for three reasons:

1. Governance tokens lack value capture. Most RWA protocols grew by offering institutional-grade products where revenue accrues to the business entity, not the token. Ondo's platform processes billions. ONDO token holders receive nothing directly. This is changing—Maple's buyback program is a template—but it requires governance action.

2. Token unlock pressure. ONDO has 4.87 billion circulating of 10 billion max. Many RWA tokens launched with long vesting schedules that are now unlocking into thin liquidity, creating persistent sell pressure regardless of fundamentals.

3. Narrative rotation. Crypto markets rotate narratives. In 2024, RWA was the hot meta. In 2025–2026, AI agents and meme coins captured attention and capital. RWA protocols kept building—and their TVL kept growing—but token prices followed the narrative, not the fundamentals.

The opportunity for patient investors is that the fundamentals and the prices are moving in opposite directions. When narrative attention returns to RWA—and it will, as $50B+ in tokenized assets demands market attention—the re-rating could be swift.

Conclusion

The RWA sector is experiencing something rare in crypto: institutional adoption is accelerating while token valuations compress. BlackRock, JPMorgan, Fidelity, and Mastercard are not building on-chain for fun—they are doing it because tokenized assets settle faster, trade 24/7, and reduce intermediary costs. That is a secular trend, not a cycle.

For investors willing to look past the current narrative drought, several tokens offer compelling asymmetry:

-

ONDO at $0.32 — the RWA sector leader with $3.5B+ TVL, trading at an 85% discount despite hitting all-time highs in platform usage

-

CFG at $0.175 — a multi-year operational track record in invoice financing, down 99% from highs

-

CPOOL at $0.0023 — $937 million in loans originated against an $18 million market cap

-

LINK at $8.39 — the oracle monopoly that every RWA protocol depends on

The framework is clear: favor protocols with live institutional integrations, favorable tokenomics, and real value accrual. Avoid governance tokens with no economic link to platform growth, regardless of how impressive the technology is.

The RWA megatrend is not coming. It is here. The only question is whether your portfolio is positioned before the market reconnects token prices with the fundamentals that have been building all along.

FAQs

What are RWA tokens in crypto?

RWA (Real World Asset) tokens are cryptocurrencies that power protocols tokenizing traditional financial assets on the blockchain. These include tokenized U.S. Treasuries (Ondo, BlackRock BUIDL), real estate fractionalization (Lofty, RealT), private credit (Maple, Centrifuge, Clearpool), and stock tokenization (Ondo Global Markets, Robinhood Chain). RWA tokens typically serve governance functions and, in some cases, capture protocol revenue through buybacks or fee sharing.

Why are RWA tokens so undervalued in 2026?

RWA tokens are undervalued due to three factors: (1) most governance tokens lack direct value capture mechanisms, creating a disconnect between platform growth and token price; (2) scheduled token unlocks create persistent sell pressure into thin liquidity; and (3) narrative rotation toward AI agents and meme coins has drawn capital and attention away from RWA despite accelerating institutional adoption. Ondo TVL hit all-time highs while ONDO traded 80% below its peak—a textbook fundamentals-price disconnect.

Is Ondo Finance a good investment at $0.32?

Ondo represents the most operationally mature pure-play RWA protocol, with $3.5B+ TVL, 54.4% market share in tokenized stocks, SEC licenses, and integrations with BlackRock, JPMorgan, and Mastercard. At $0.32 (down 85% from $2.14 ATH), the risk/reward is favorable for patient investors. The primary upside catalyst is governance deploying a value capture mechanism (fee sharing or buybacks). Without this, the token may lag platform growth. The 10 billion max supply with 4.87 billion circulating creates ongoing unlock pressure to monitor.

What is the difference between RWA tokens and tokenized RWA products?

Tokenized RWA products (like Ondo USDY, BlackRock BUIDL, or Lofty property tokens) are the on-chain assets representing real-world investments. RWA tokens (like ONDO, CFG, CPOOL) are the governance tokens of the protocols that create and manage these products. The distinction is critical: tokenized products can grow massively while governance tokens remain flat if there is no value accrual mechanism linking protocol revenue to token demand.