KuCoin Ventures Weekly Report: RWA Strides into TradFi Back-Office Infrastructure; Semiconductors Underpin Broader Risk Assets, MSTR Strategy Restructuring and Fed Leadership Turnover Trigger Liquidity Revaluation

2026/05/12 06:45:02

1. Weekly Market Highlights

From Asset Issuance to Process Transformation: RWA Enters the Deep End of Institutional Finance

The narrative focus of real-world asset tokenization (RWA) is moving deeper. Market attention is no longer limited to “how many assets have been brought on-chain,” but is increasingly shifting toward whether core back-office processes in traditional finance — including custody and registration, ownership verification, transfer and redemption, collateral management, and cross-border settlement — can be transformed through blockchain infrastructure. These processes have rarely been the center of market narratives, yet they determine whether tokenized assets can evolve from display-oriented products into financial tools that institutions can use on a daily basis. In other words, tokenization is moving beyond asset representation toward a systematic restructuring of financial workflows.

This shift is first reflected in the systematic adoption of tokenization by traditional market infrastructure providers. On May 4, DTCC announced progress on its DTC Tokenization Service, which has attracted participation from more than 50 financial institutions. The service is expected to begin limited production transactions in July and officially launch in October. Rather than simply introducing another category of on-chain assets, the initiative seeks to bring securities custody, ownership verification, investor protection, and on-chain interoperability into a unified market infrastructure framework. For institutional capital, whether an asset can be tokenized is only the first step. Whether it can complete registration, clearing, redemption, and rights verification within a compliant framework is what determines whether it can enter balance sheets and liquidity management systems. As a result, the competitive focus of RWA is shifting from the issuance layer to the back-office layer — from “how large the on-chain asset base is” to “whether these assets can be practically used by the traditional financial system.”

Developments around Canton Network follow the same logic. On May 7, 21Shares launched the 21Shares Canton Network ETF (TCAN) on Nasdaq, the first U.S. ETF to provide direct exposure to Canton Coin, opening a public-market access point to an institutional-grade privacy blockchain. Supported by institutions such as Nasdaq, Visa, and Moody’s, Canton Network is mainly designed for tokenized real-world assets, privacy-preserving interoperability, and compliant asset movement. In parallel, Mizuho, Nomura, and JSCC are advancing a proof of concept (PoC) for tokenized Japanese government bond (JGB) collateral on Canton Network, with a focus on testing whether government bond collateral can balance privacy protection, compliant access, and real-time mobilization. Collateral management for government bonds requires an extremely high level of ownership certainty, settlement finality, and cross-institution coordination. If on-chain infrastructure can gain a foothold in such scenarios, RWA will no longer be positioned merely as an investment product, but will increasingly become part of the operating system for institutional finance.

Bullish’s acquisition of Equiniti adds another key piece to the puzzle from the perspective of equity assets. Bullish announced a $4.2 billion acquisition of Equiniti, a transfer agent serving nearly 3,000 issuers and around 20 million shareholders, with approximately $500 billion in annual payment processing volume. The significance of the deal is not simply that a crypto institution is acquiring a traditional financial services provider, but that Bullish is attempting to enter the transfer agency infrastructure that tokenized securities rely on. In past discussions around stock tokenization, the market often focused on 24/7 trading and global accessibility. Yet for securities assets, shareholder registers, corporate actions, dividends and voting, transfers, and compliance list management are the underlying links that determine legal validity and investor rights. Future competition in tokenized equities will not remain limited to front-end trading platforms, but will extend into registration, custody, and investor servicing systems.

Redemption and cash settlement represent the key dividing line between RWA that is merely “displayable” and RWA that is truly “usable.” This week, Ondo Finance, Kinexys by J.P. Morgan, Mastercard, and Ripple completed the world’s first near-real-time, cross-bank and cross-border redemption pilot for tokenized U.S. Treasuries. After the redemption was triggered on XRP Ledger, instructions were routed through Mastercard’s Multi-Token Network, bank-side settlement was processed by Kinexys, and U.S. dollars were ultimately transferred to Ripple’s Singapore account. The pilot validated a connection path between on-chain fund shares, bank payment networks, and cross-border U.S. dollar settlement. For institutions, bringing assets on-chain is only the starting point. The ability to redeem efficiently when needed and return seamlessly to fiat bank accounts is what determines their real liquidity value.

Overall, the core signal this week is that RWA is moving from an “asset issuance narrative” into a “financial process transformation narrative.” The next stage is not only about whether the tokenized RWA market continues to expand in size, but whether these assets can be used continuously and efficiently across collateral, redemption, settlement, risk management, and compliance workflows. Only when assets, accounts, payments, and execution are integrated into the same programmable process can RWA move beyond on-chain asset display and truly become institutional financial infrastructure.

2. Weekly Selected Market Signals

AI Earnings Underpin Risk Assets, ETF Funds Support BTC Recovery, Inflation and Geopolitical Risks Limit Easing Trades

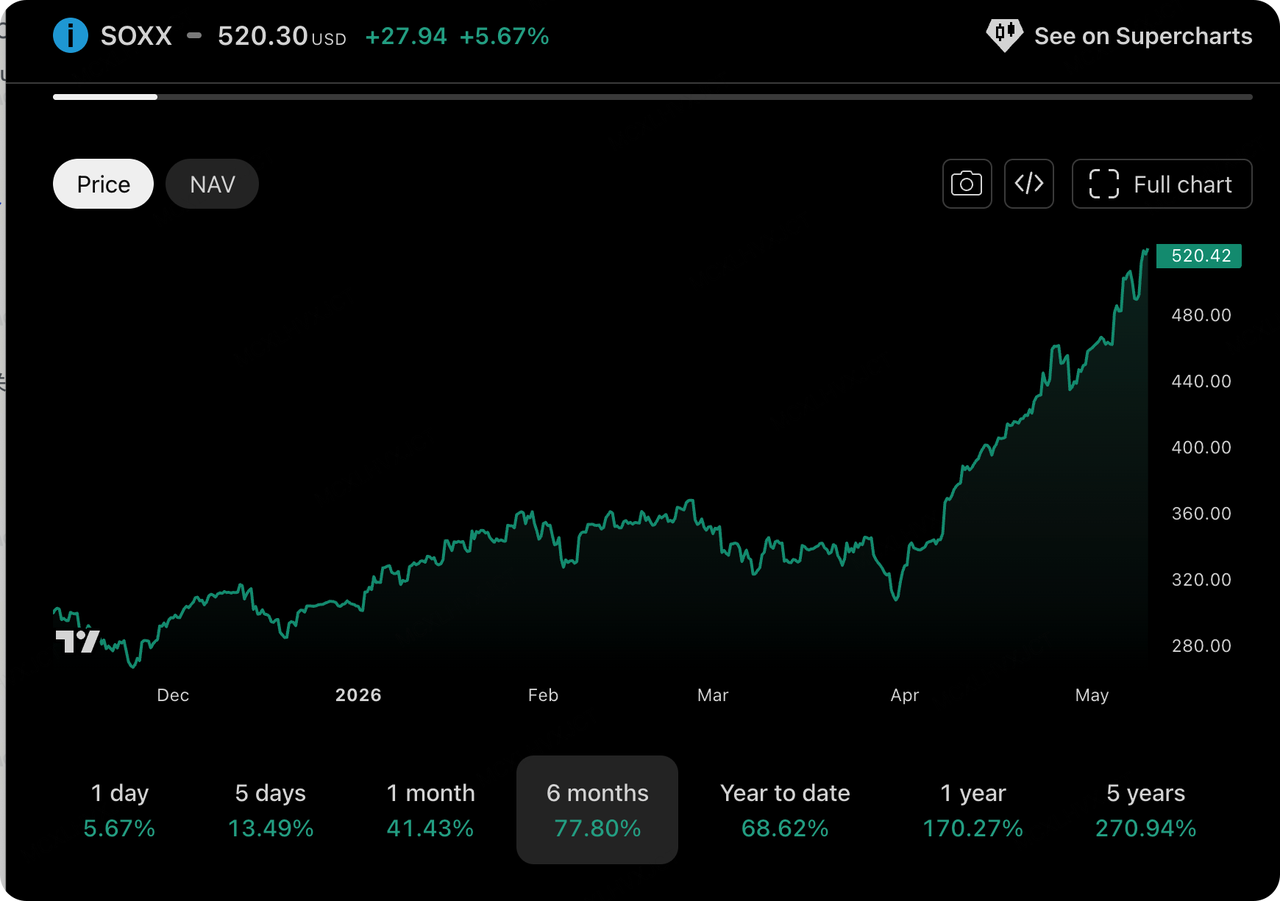

Setting aside complex macroeconomic games, capital in traditional broader markets is "voting with its feet": tech stocks, especially the semiconductor sector, continue to dictate the flow of global liquidity. Thanks to stellar Q1 earnings, North American cloud providers have completely dispelled previous market concerns about an "AI bubble" with "strong reality" capital expenditures (CapEx). The iShares Semiconductor ETF (SOXX) has recently significantly outperformed, and the Information Technology and Communication Services sectors account for nearly all of the S&P 500's gains and earnings growth.

Data Source: Tradingview

The current boom in the semiconductor industry is by no means superficial hype; rather, it exhibits three deep-seated structural evolutions, which also provide important external valuation benchmarks for the crypto market:

-

Compute inflation on the LLM side: AI large language model (LLM) companies and their affiliates, represented by OpenAI / Anthropic, have recently completed massive fundraising rounds, with the core of these funds directed entirely toward replenishing compute resources. The exponential surge in token consumption has caused demand for both domestic and North American foundational hardware to skyrocket, presenting a booming scenario in both supply and demand.

-

Explosion of memory chips and "South Korea-related" assets: The rigid demand of AI compute for High Bandwidth Memory (HBM) has directly propelled the stock prices of South Korean semiconductor giants Samsung Electronics and SK Hynix to repeated all-time highs, with staggering year-to-date gains. Related semiconductor ETFs in the broader market are experiencing extreme "FOMO" crowding, as capital spills over from pure compute chips to the entire hardware supply chain and geopolitical considerations.

-

Architecture evolution (from single-core GPU to CPU/GPU synergy): With the accelerated penetration of AI Agents on the device and edge sides, computing architectures are undergoing subtle changes. The market expects the CPU/GPU ratio to drastically increase from the previous 1:8 to 1:1, meaning that not only AI accelerators but also general-purpose CPUs are on the verge of explosive demand. This is also one of the reasons behind Intel's recent valuation re-rating.

Beyond the AI narrative, from a global macro perspective, last week's main themes revolved around "abnormal employment data" and "Federal Reserve leadership shifts." The recently released non-farm payroll data fell short of expectations (adding between 78,000 and 83,000 jobs), sparking market concerns about a slowdown in US economic momentum and causing capital to swing violently between "recession trades" and "rate cut/hike trades."

Data Source: TradingView

Looking at the crypto secondary market, this week was not as heated as the semiconductor sector. It faced significant selling pressure in the latter half of the week, frustrating the bullish sentiment accumulated at previous highs, and cracks appeared in the market's core narratives:

As the largest transparent corporate bull since the last bull market, MicroStrategy (MSTR) has recently made a major and surprising strategic pivot, likely breaking its past absolute commitment to "never sell." Michael Saylor engaged in proactive expectation management. He precisely revised his iconic "Never sell your Bitcoin" slogan to "Never be a net seller." The market has begun pricing in the possibility that the company might sell some BTC to issue dividends or optimize its cash flow and leverage model (STRC/MNAV). This shift in fundamental expectations is likely to shake the confidence of market bulls, is viewed by Wall Street as a crucial signal of a cyclical top, and is considered by the market as the core catalyst for the current pullback.

Although the company has other cash flow avenues to pay dividends, the revised expectations regarding potential Bitcoin sales mean the market must adapt to MSTR's transition from an "absolute one-way accumulator" to a complex financial model of "dynamic leverage equilibrium." Moving forward, the actual issuance volume of $STRC may become one of the market's core bellwether for monitoring the health of MSTR's positioning.

Data Source: SoSoValue

Combining the latest on-chain and market data, funding sentiment in the ETF market has shifted from euphoria to relative rationality:

-

Significant net outflows from BTC Spot ETFs: Data shows that as BTC retreated to around $80,179, it recorded a massive single-day net outflow of -$288 million, with total net assets dropping back to $106.61 billion. Momentum ETF funds chose to take tactical profits in the face of macroeconomic uncertainty and the bearish MSTR news, ending the previous trend of strong net inflows.

-

Sluggish performance in ETH Spot ETFs: In contrast, ETH spot ETFs performed relatively flatly, recording a net outflow of -$103 million on May 7, with the ETH price under pressure near $2,300. Capital's willingness to buy the dip on Ethereum remains insufficient, reflecting market reservations about the explosive potential of public chain ecosystems in the current environment.

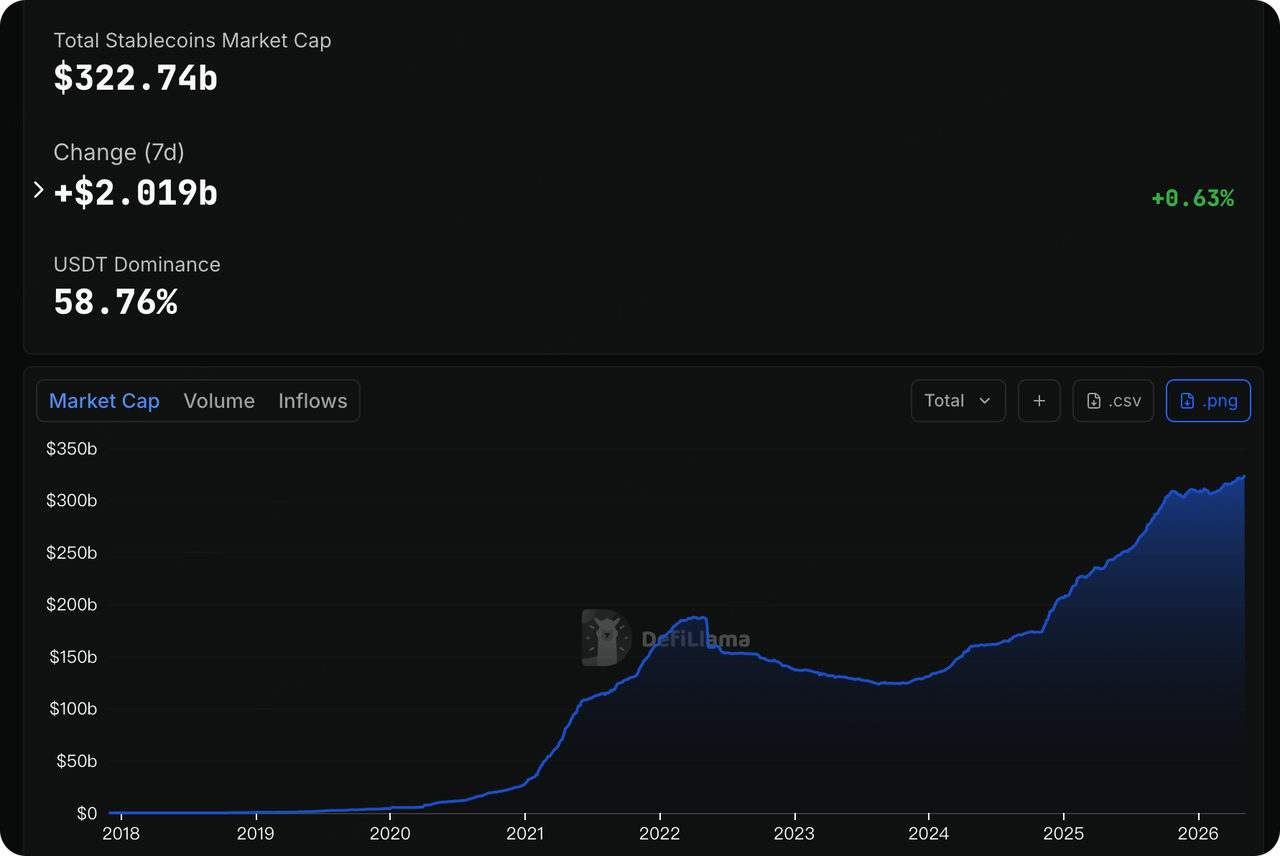

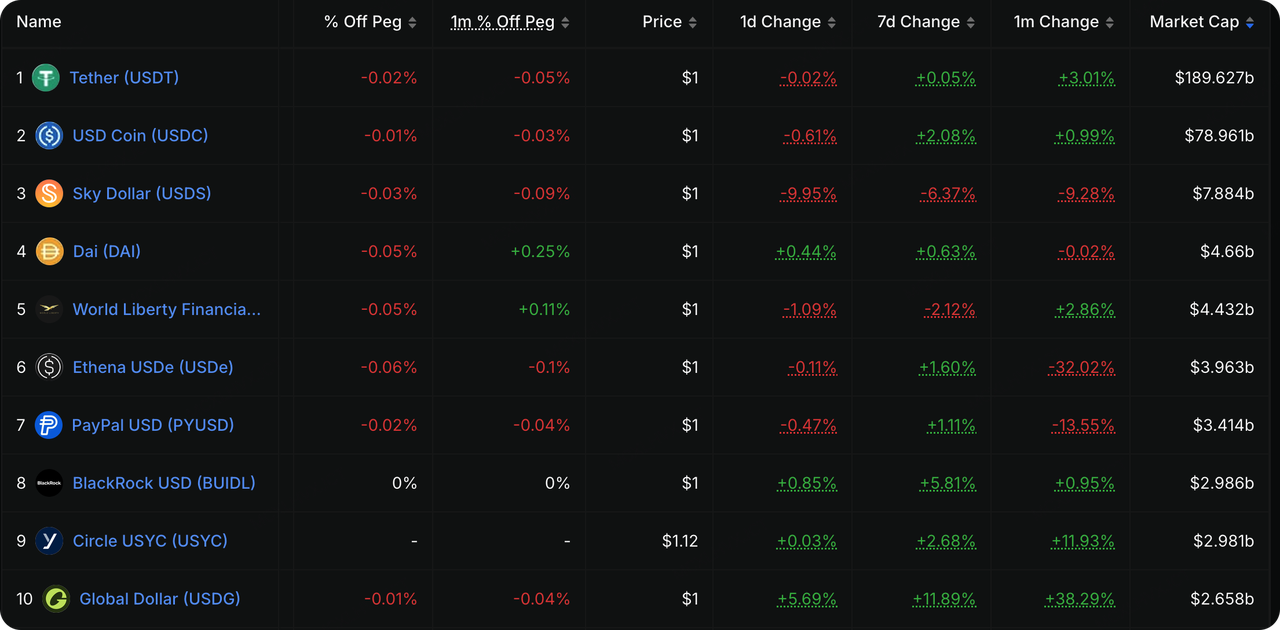

Data Source: DeFiLlama

DeFiLlama data shows that the total market capitalization of stablecoins across the network has climbed to $322.74 billion, with a net inflow of over $2 billion (+0.63%) over the past 7 days. Among them, USDT still maintains absolute dominance (58.76% market share, reaching $189.6 billion in scale), closely followed by USDC at nearly $79 billion. The compliance-oriented Global Dollar (USDG) has seen its scale surge by 38.29% over the past month, with issuance rising rapidly over the past week as well. Meanwhile, the CeDeFi-attributed Ethena USDe continues to show a trend of significant drawdown, with a 32.02% decrease in issuance over a single month. This highlights a trend of capital seeking refuge in highly compliant, low-risk assets during volatile markets.

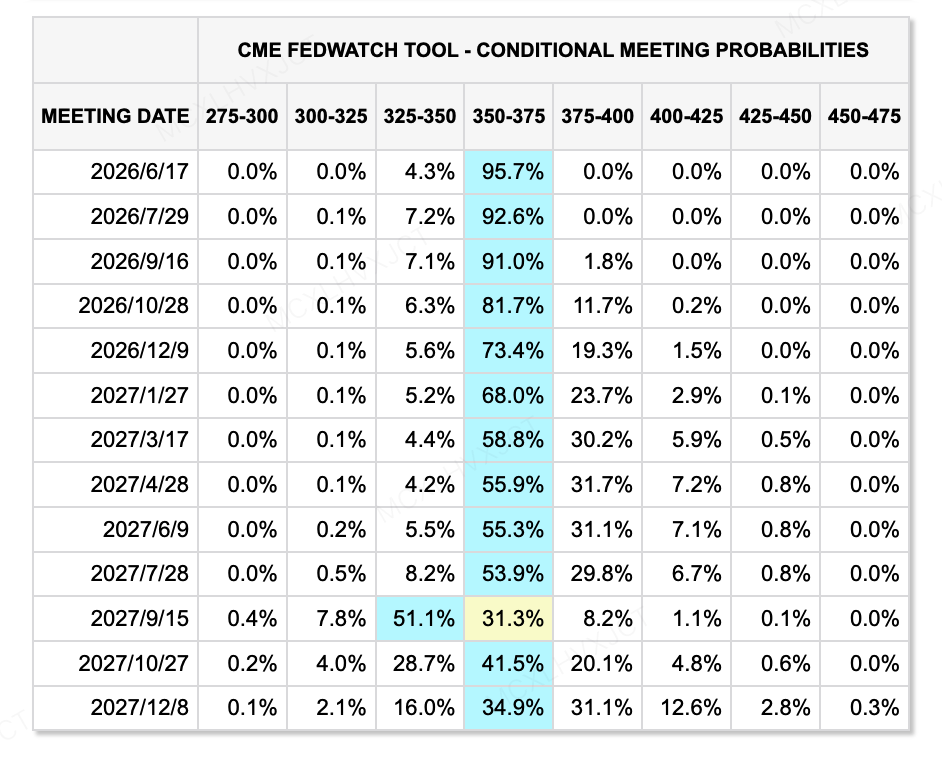

Data Source: CME FedWatch Tool

Judging from current market trading results, the probability of the Federal Reserve cutting interest rates to 350-375 basis points by the June 17, 2026, FOMC meeting has reached as high as 95.7%. However, current Chairman Jerome Powell is facing a whirlpool of public opinion regarding an early departure, while former Fed Governor Kevin Warsh is entering the countdown to taking the helm. This high-level political uncertainty makes short-term USD liquidity and risk-free interest rate pricing extremely fragile.

Survey reports from top investment banks and institutions point out that Warsh currently faces a "dilemma." Although the White House has strong demands for rate cuts, the Federal Reserve is currently experiencing its most severe internal division since 1992 (with 4 dissenters at a recent meeting). Warsh needs to quickly establish credibility in his debut to prove to the market that he is not a "political puppet," but rather a data-driven pragmatist. The June FOMC meeting will be Warsh's first policy appearance as Chairman, viewed by the market as the most important turning point for the Fed in 8 years. The market's focus is not on a single interest rate move, but rather on his first press conference and the update of the Summary of Economic Projections (SEP), to observe how he will manage internal dissent and quantify the impact of AI productivity gains on the future rate path.

Major Events to Watch This Week:

-

Monday (May 11): Release of China's April CPI and PPI data. Amid the tug-of-war between deflationary concerns and pro-consumption policies, this data set will reflect the endogenous recovery momentum of the world's second-largest economy.

-

Tuesday (May 12): US April CPI (Consumer Price Index) lands. This is the core indicator for the policy tone after incoming Fed Chairman Kevin Warsh takes office, and it is highly likely to influence market pricing of the rate cut path for June and the second half of the year. Attention should also be paid to the German/Eurozone Economic Sentiment Index on the same day.

-

Wednesday (May 13): Release of US April PPI (Producer Price Index). Combined with the previous day's CPI, this will further piece together the full picture of US inflation. Additionally, the OPEC Monthly Report and the EIA Short-Term Energy Outlook will be released consecutively; against the backdrop of currently surging energy prices, the secondary impact of crude oil supply expectations on inflation warrants vigilance. The Eurozone will release Q1 GDP data on the same day. US President Donald Trump is expected to arrive in China, kicking off a highly anticipated state visit.

-

Thursday (May 14): US and Chinese heads of state are expected to hold a formal bilateral summit. The two nations are expected to engage in in-depth negotiations surrounding a new round of trade tariffs, semiconductor and AI tech supply chains, and global geopolitical hotspots such as the Middle East/Iran. US April Retail Sales and weekly Initial Jobless Claims will be released. Combined with recent non-farm weakness, this data will serve as a crucial touchstone for verifying the resilience of US consumption and whether the economy is falling into substantive "stagflation/recession."

Primary Market Investment Observations:

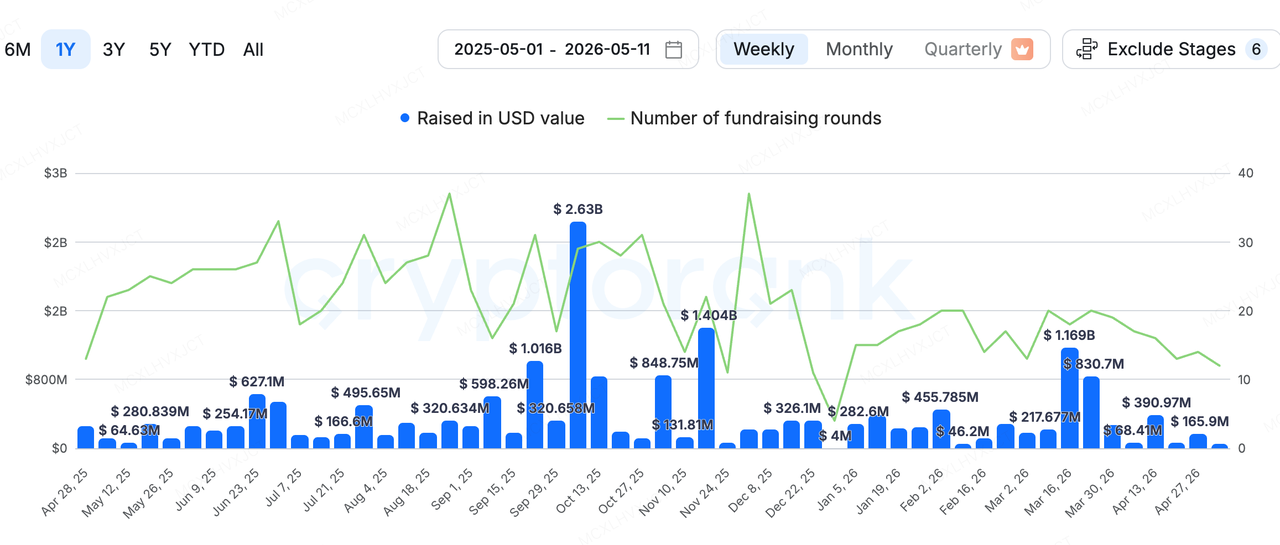

Data Source: CryptoRank

Regarding primary market financing, according to CryptoRank statistics (excluding M&A), the total crypto primary financing volume last week was $50.2 million. The most eye-catching deal last week came from Payward, the parent company of the crypto exchange Kraken, which announced the acquisition of Hong Kong-based stablecoin payment infrastructure company Reap for a staggering $600 million (in a cash and stock combo).

This $600 million acquisition is not only the largest deal of the week but also anchors Payward's own valuation at $20 billion. Reap is a platform providing "stablecoin-native" credit card issuance and cross-border payment infrastructure. Its core moat lies in successfully bridging traditional bank payment networks and credit card networks like Visa/Mastercard with the blockchain layer via a single API interface, allowing corporate clients to use stablecoins as the underlying settlement medium.

Kraken has been very aggressive in its capital market expansion in recent years. Over the past year, it has spent a cumulative total of approximately $2.7 billion on successive acquisitions, including securing derivatives platforms Bitnomial and NinjaTrader, as well as the tokenized securities (RWA) platform Backed Finance. This clearly outlines its goal: evolving from a simple CEX into a full-stack Web3 financial infrastructure giant integrating "spot, derivatives, compliant custody, RWA, and cross-border stablecoin settlement." It is evident that it is also striving to provide more narrative and fundamental support for its future IPO.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.