Stablecoins Guide: How They Work, Why Matter & How to Buy

2026/04/09 12:03:02

The cryptocurrency market is legendary for its volatility. For many, the sight of a portfolio swinging 20% in a single afternoon is the primary barrier to entry. Enter stablecoins: the "liquidity glue" that holds the decentralized economy together. By bridging the gap between the speed of blockchain and the price stability of the U.S. Dollar or gold, stablecoins have transitioned from a niche trading tool to the most critical infrastructure in the digital asset space.

In this exhaustive guide, we will explore the inner workings of these "digital dollars," moving from the basic definitions to the complex mechanisms of the 1:1 price peg. We will break down the four distinct architectures—fiat, crypto, algorithmic, and commodity-backed—that define the current market.

As we look toward the regulatory shifts of 2025–2026, you will learn why stablecoins are no longer just a crypto convenience, but a global financial necessity.

What is a Stablecoin? The Bridge Between Two Worlds

At its core, a stablecoin is a digital asset designed to maintain a stable value relative to a specific asset or a basket of assets. While Bitcoin is often described as "digital gold"—a speculative store of value—a stablecoin is "digital cash."

If Bitcoin is a roller coaster, a stablecoin is the steady track beneath it. Most are pegged at a 1:1 ratio with the U.S. Dollar, meaning one token should always be worth exactly $1.00. This allows users to enjoy the benefits of blockchain—instant settlements, 24/7 availability, and borderless transfers—without the stomach-churning price swings of traditional crypto.

The Evolution of Digital Money

To understand stablecoins, we must look at the history of "on-ramps." In the early days of crypto, moving between Bitcoin and Dollars required slow bank transfers. Stablecoins solved this by allowing value to stay on the blockchain while removing price risk. By 2026, they have become more than just a trading tool; they are a global payment standard used by payment giants and central banks alike. For those looking to access these assets, major exchanges like Kucoin provide the necessary liquidity and trading pairs to swap between volatile assets and stable ones instantly.

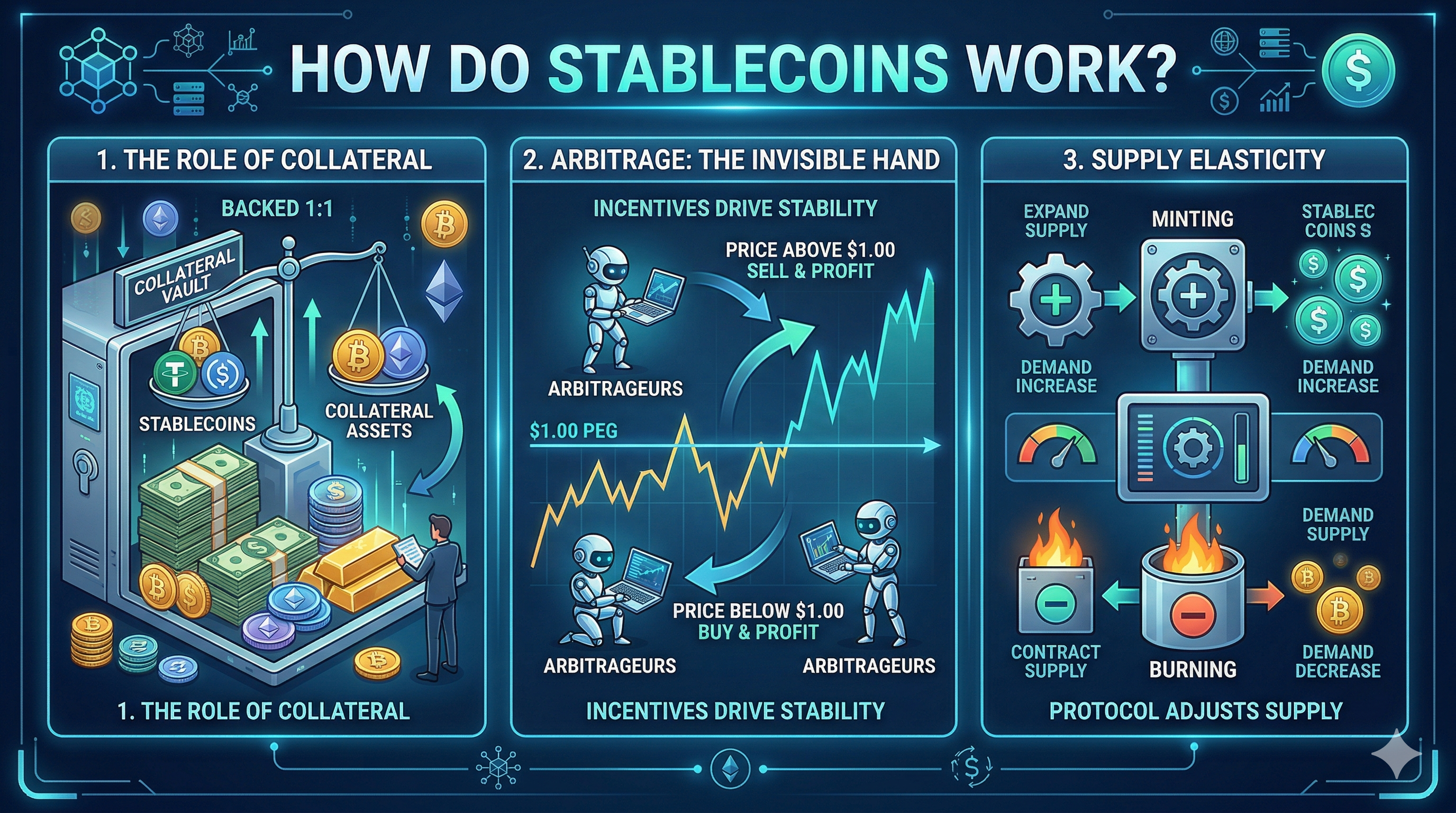

How Do Stablecoins Work? The Mechanics of the Peg

Maintaining a price of exactly $1.00 in a market that never sleeps is an engineering marvel. Stablecoins stay stable through three primary mechanisms: Collateralization, Arbitrage, and Smart Contract Governance.

-

The Role of Collateral

Think of collateral as the "vault." To ensure that a digital token is worth $1.00, there must be a backing. If a company issues 1 billion tokens, they must prove they have $1 billion (or more) in a reserve to honor redemptions.

-

Arbitrage: The Invisible Hand

Markets are driven by supply and demand. If the price of a stablecoin like USDC rises to $1.02 on an exchange, "arbitrageurs" will buy USDC directly from the issuer for $1.00 and sell it on the exchange for $1.02, pocketing the profit. This increased selling pressure pushes the price back down to $1.00.

Conversely, if the price drops to $0.98, traders will buy the "cheap" tokens on the exchange and redeem them with the issuer for a full $1.00, reducing the supply and pushing the price back up.

-

Supply Elasticity

Modern stablecoins use "rebase" or "mint-and-burn" mechanisms. When demand is high, the system mints more supply to prevent the price from rising too far above the peg. When demand is low, the supply is contracted.

The 4 Main Types of Stablecoins: A Deep Dive

The "how" of a stablecoin defines its risk profile. As an investor or user, you must understand what is happening "under the hood."

-

Fiat-Collateralized (Off-Chain)

These are the heavyweights, representing over 90% of the total stablecoin market cap. They are backed by traditional currencies (USD, EUR, GBP) held in regulated bank accounts or short-term government debt.

-

Mechanism: For every 1 token minted, $1 of fiat is deposited into a reserve.

-

Top Players: USDT (Tether), USDC (USD Coin), PYUSD (PayPal USD).

-

The Nuance: These are "centralized." You are trusting a private company to hold the money and remain compliant with regulators.

-

Crypto-Collateralized (On-Chain)

These are for those who value decentralization and censorship resistance. Instead of dollars in a bank, these are backed by other cryptocurrencies like Ethereum or Bitcoin.

-

Mechanism: Because crypto is volatile, these are over-collateralized. To get $100 of DAI, you might need to lock up $150 of ETH. This "buffer" ensures that even if ETH drops 20%, the $100 stablecoin remains fully backed.

-

Top Players: DAI (MakerDAO), LUSD (Liquity).

-

Algorithmic Stablecoins (The Code-Based Approach)

These do not rely on a vault of assets. Instead, they use mathematical algorithms to manage supply and demand, much like a central bank manages a nation's currency.

-

The Risk: These are historically the most fragile. If the market loses faith in the algorithm, it can lead to a "death spiral."

-

Top Players: FRAX (a hybrid model), USDe (Ethena).

-

Commodity-Backed Stablecoins

These are pegged to physical assets, allowing you to hold "hard assets" with the portability of a digital token.

-

Mechanism: Each token represents ownership of a specific amount of a physical good, such as one gram of gold held in a vault in London or Switzerland.

-

Top Players: PAX Gold (PAXG), Tether Gold (XAUT).

Why Use Stablecoins? Key Benefits for Investors and Businesses

Stablecoins are no longer just for "parking" funds between trades. In 2026, their utility has expanded into every corner of the global economy.

High-Yield Passive Income (The DeFi Edge)

In the world of Decentralized Finance (DeFi), you can act as the bank. By providing liquidity to protocols like Aave or Uniswap, users can earn interest rates that often dwarf traditional savings accounts. While a bank might offer 0.5% APY, stablecoin lending can yield 5%–10% or more, depending on market demand.

Frictionless Global Remittances

Sending $1,000 to another country via a bank (SWIFT) can take 3–5 days and cost $50 in fees. With a stablecoin on a high-speed network like Solana or a Layer 2 like Arbitrum, that same $1,000 arrives in seconds for a fraction of a cent.

A Lifeboat for Inflation-Struck Nations

For citizens in nations like Argentina, Turkey, or Nigeria, where the local currency is losing value rapidly, stablecoins offer a lifeline. They provide a way to "save in Dollars" without needing a local USD bank account, which is often restricted or impossible to obtain.

B2B Payments and Smart Contracts

Businesses are using stablecoins to settle invoices instantly. Because stablecoins live on-chain, they can be programmed into Smart Contracts. Imagine a contract that only releases payment to a supplier once a shipping carrier confirms delivery—no manual escrow required.

Top 5 Risks of Using Stablecoins (Don’t Ignore These)

To provide a professional and logical guide, we must address the "dark side" of stability.

De-pegging Risk: This is the "Black Swan." If a stablecoin loses its $1.00 peg, it can trigger a bank run. Investors must monitor the "reserve transparency" of their chosen coin.

Regulatory Seizure: Because centralized coins (USDT/USDC) are run by companies, they can "blacklist" or freeze your specific wallet address at the request of law enforcement.

Counterparty Risk: You are trusting that the issuer is solvent. If the bank holding the reserves fails, or the issuer makes bad investments with the collateral, your tokens could become worthless.

Smart Contract Vulnerabilities: For decentralized coins like DAI, a bug in the code could allow a hacker to drain the collateral, leaving the stablecoin unbacked.

Inflation of the Peg: While your coin stays at $1.00, the purchasing power of that dollar is still declining due to U.S. inflation. A stablecoin is a hedge against volatility, not necessarily a hedge against inflation.

Stablecoins vs. Traditional Banking – A Logical Comparison

As we move into a digital-first era, the line between a bank account and a crypto wallet is blurring.

| Feature | Stablecoins | Traditional Banking |

| Settlement Time | Near-Instant (24/7) | Days (Business Hours only) |

| Access | Permissionless (Global) | Restricted by borders/credit |

| Transparency | Real-time on-chain audits | Quarterly/Yearly reports |

| Control | Self-Custody (You own the keys) | Custodial (The bank owns the cash) |

| Insurance | Private insurance only | FDIC/Government Insured |

The Future of Stablecoins in 2025–2026: Trends & Regulation

The stablecoin landscape is rapidly shifting from experimentation to standardization, driven by three major trends in 2025–2026. First, yield-bearing stablecoins are emerging, allowing holders to earn passive income as issuers back tokens with interest-generating assets like U.S. Treasury Bills and pass yields directly to users. Second, global regulatory clarity is taking shape, led by the EU's MiCA framework, which sets the gold standard by requiring 1:1 reserves and high liquidity—effectively cleaning up the market and making stablecoins safer for institutional capital. Third, while governments advance Central Bank Digital Currencies (CBDCs) such as digital dollars, private stablecoins are likely to remain the preferred choice for the DeFi ecosystem, thanks to their superior privacy and cross-chain interoperability.

Conclusions

Stablecoins serve as the critical bridge to the future of finance, offering internet-era efficiency with dollar-like stability. For a sound strategy, prioritize caution and diversification: split holdings between regulated options like USDC and decentralized options like DAI, and always verify blockchain networks (e.g., ERC-20 vs. SPL) before sending.

Beyond simple storage, the modern investor looks to maximize the utility of their digital dollars. Once you have acquired your assets on an exchange like KuCoin, you can seamlessly transition from trading to wealth building. By leveraging KuCoin Earn, you can put your idle stablecoins to work in various savings and staking products, turning price stability into a consistent source of passive yield. By 2026, holding digital dollars—and optimizing them through professional earning tools—is no longer a crypto experiment; it's a strategic financial move.

FAQs

Q1: Is a stablecoin as safe as a bank account?

No. Bank accounts in many countries are government-insured (like FDIC). Stablecoins rely on the solvency of the issuer and the integrity of the code. Only invest what you can afford to risk.

Q2: Can I use stablecoins for daily purchases?

Yes. Many crypto debit cards (like those from BitPay or Coinbase) allow you to spend your stablecoins anywhere Visa or Mastercard is accepted.

Q3: Why would I hold USDC instead of USDT?

USDC is widely considered more "transparent" because it is issued by a U.S.-regulated company (Circle) and undergoes regular third-party audits. USDT (Tether) is the most liquid but has faced historical criticism regarding its reserve disclosures.

Q4: Do I need to pay taxes on stablecoins?

In most jurisdictions, swapping one cryptocurrency for a stablecoin is a taxable event. However, since the price usually stays at $1, your "capital gain" is often zero, making it a useful tool for rebalancing your portfolio without a massive tax bill.

Q5: How do I choose a blockchain for my stablecoins?

If you want the most security, use Ethereum. If you want the lowest fees, use Solana, Polygon, or an Ethereum Layer 2 like Base or Optimism.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Always conduct your own research before interacting with digital assets.