Why Samsung Stock Fell After Record Earnings: The Truth Behind the Numbers

2026/07/07 15:42:00

Introduction

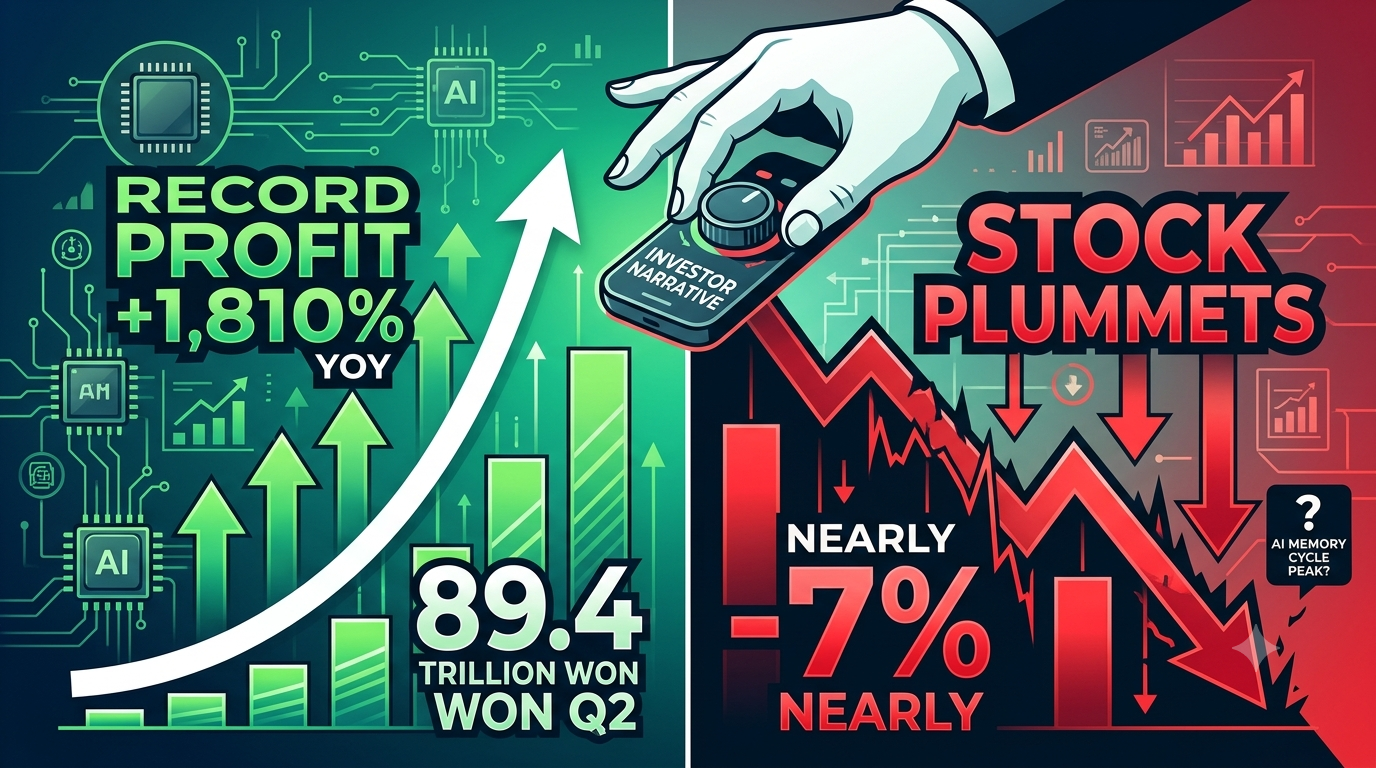

Samsung Electronics just reported the most profitable quarter in its 56-year history — and its stock immediately tanked nearly 7%. On July 7, 2026, the world's largest memory chipmaker announced Q2 operating profit of approximately 89.4 trillion won (roughly $58 billion), a staggering 1,810% year-over-year surge. Revenue climbed 129% to 171 trillion won. Yet the market responded with a brutal sell-off.

Why would the best earnings report ever trigger a sell-off? The answer reveals a critical lesson for investors: in financial markets, the narrative behind the numbers matters more than the numbers themselves.

Why Did Samsung Stock Drop After Record Profits?

Samsung's stock fell because the market is repricing the entire memory supercycle, not punishing Samsung individually. The 19-fold profit surge is almost entirely driven by DRAM and NAND price inflation — an industry-wide phenomenon that benefits all memory manufacturers equally.

When SK Hynix and Micron Technology also declined in tandem with Samsung, it signaled that investors are questioning whether the memory pricing cycle has peaked, not whether Samsung is poorly managed. According to market data from early July 2026, Samsung shares had already rallied approximately 147% year-to-date before the earnings announcement, suggesting that much of the good news was already embedded in the stock price. The post-earnings drop is a classic "sell the news" reaction — when expectations are set too high, even record-breaking results can disappoint.

Is Samsung's Profit Growth Driven by Pricing or Real Competitive Advantage?

Samsung's profit growth is primarily a pricing story, not a competitive victory. The 19-fold operating profit increase is overwhelmingly attributable to the memory price supercycle rather than market share gains or technological breakthroughs unique to Samsung. According to Reuters, DRAM average selling prices rose approximately 44% quarter-over-quarter in Q2 2026, while NAND flash prices surged roughly 53%. These price hikes are the direct result of AI data center demand creating severe supply constraints.

When manufacturers prioritize high-margin HBM (High Bandwidth Memory) production for AI servers, they naturally reduce capacity for conventional DRAM and NAND, creating a supply squeeze that lifts prices across all memory categories. This is a macro industry beta play — every major memory producer is benefiting simultaneously. Samsung is riding the same wave as SK Hynix and Micron, not outperforming them through superior execution.

What Does Samsung's Revenue Tell Us About Its Business Mix?

Samsung's revenue figures expose a structural weakness that profit numbers alone conceal. While operating profit exceeded market expectations of approximately 86 trillion won, the revenue growth rate of 129% — while impressive — reveals a volume shortfall relative to the price-driven profit explosion. When profit grows faster than revenue, it means the company is earning more per unit sold but not necessarily selling more units. This is particularly concerning because the most valuable segment of the memory market — HBM for AI servers — is where Samsung faces its most serious competitive challenge.

Samsung's Q1 2026 earnings report confirmed that the semiconductor division generated 53.7 trillion won in operating profit, representing 94% of total company earnings. However, the company also acknowledged that HBM4 qualification and mass production timelines remain critical variables. If Samsung's revenue is being carried by commodity memory price inflation rather than high-value HBM volume growth, the profit quality is inherently lower than it appears.

Is Samsung Losing the HBM Race to SK Hynix?

Samsung is trailing SK Hynix in the HBM market, which is the most strategically important battleground for AI-era memory dominance. HBM — the high-bandwidth memory stacked directly next to AI accelerator chips from NVIDIA and other vendors — commands the highest margins and the strongest demand visibility in the entire semiconductor industry. While Samsung initiated mass production of HBM4 and SOCAMM2 for NVIDIA's Vera Rubin platform in Q1 2026, SK Hynix has maintained a technological and market share lead in the HBM3E and HBM4 generations.

The fact that Samsung's Q2 profit is overwhelmingly driven by conventional DRAM and NAND price hikes, rather than HBM volume leadership, suggests the company has not yet captured the most profitable segment of the AI memory market. For investors, this is the critical distinction: Samsung is winning the memory cycle, but it may be losing the structural battle for AI memory supremacy.

Are Samsung's Earnings Inflated by One-Time Costs?

Samsung's headline profit figure contains a meaningful distortion from one-time employee compensation costs that reduce the true quality of earnings. The consensus operating profit estimate was revised downward from approximately 96 trillion won to 86 trillion won (and the actual preliminary figure came in at 89.4 trillion won) largely due to special labor-related costs negotiated during May 2026 union agreements. While these costs are technically one-time in nature, they reveal an underlying margin pressure from labor negotiations that will persist as a structural cost factor.

More importantly, when analysts strip out these one-time items, the underlying profit growth is still extraordinary — but it is driven by the same pricing dynamics that the market is now questioning. The "quality" of Samsung's earnings is therefore lower than the headline 19-fold growth rate suggests, because a significant portion of the profit boost is cyclical and non-recurring rather than driven by sustainable competitive advantages.

How Long Will the Memory Supercycle Last?

The memory supercycle is expected to persist through at least 2027, but the rate of price appreciation may be peaking. Industry analysts widely expect the current "seller's market" to continue into 2027, driven by AI infrastructure expansion that shows no signs of slowing. Samsung's own Q1 2026 guidance stated that server memory demand should remain strong in the second half of 2026 as hyperscalers accommodate increasing enterprise adoption of AI and LLM services. The company also noted that agentic AI is expected to accelerate demand growth further.

However, the critical question for investors is not whether memory prices will remain elevated — they likely will — but whether the rate of price increase can continue. When DRAM prices have already risen 44% in a single quarter and NAND prices have jumped 53%, the incremental upside from pricing becomes mathematically harder to achieve. The market is forward-looking, and it is pricing in a deceleration of price growth even if absolute prices remain high.

What Should Investors Watch in Samsung's Full Earnings Report?

Samsung's full Q2 earnings report on July 30, 2026, will reveal whether the company can address the structural concerns behind the stock sell-off. Investors should focus on three key metrics: HBM4 revenue contribution and qualification progress with major AI customers, DRAM and NAND bit growth (volume shipped) versus price-driven revenue growth, and Q3 2026 guidance for memory pricing and demand trends.

The preliminary earnings announcement provides only consolidated figures — the detailed segment breakdown will show whether Samsung's semiconductor division is gaining ground in HBM or still relying on commodity memory pricing. Additionally, management commentary on HBM4E sample deliveries and customer adoption timelines will be critical for assessing whether Samsung can close the gap with SK Hynix in the highest-margin memory segment.

Should You Invest in Samsung Stock on KuCoin?

Samsung Electronics represents one of the most direct ways to gain exposure to the AI infrastructure build-out, and KuCoin offers accessible trading instruments for investors looking to position around this semiconductor supercycle.

KuCoin provides access to a broad range of not only crypto markets, but also stock markets. Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

Samsung's Q2 2026 earnings report is a paradox: the numbers are historically extraordinary, yet the market reaction was brutally negative. This disconnect exists because sophisticated investors look beyond headline profit growth to the underlying drivers and sustainability of earnings. Samsung's 19-fold operating profit increase is almost entirely a function of memory price inflation — an industry-wide phenomenon that benefits all competitors equally.

The company is not winning market share through superior technology or execution; it is riding a macro wave that could crest at any moment. The revenue growth lagging behind profit growth, the persistent HBM competitive gap with SK Hynix, and the one-time nature of certain cost adjustments all reduce the quality of these record earnings. For investors, the key takeaway is that Samsung's stock price reflects forward expectations, not backward results.

When a stock has already rallied 147% year-to-date and the earnings beat is driven by cyclical pricing rather than structural competitive advantages, even the best quarterly report in history can feel like a disappointment. The market is asking a simple question: what comes after the supercycle? Until Samsung can demonstrate HBM leadership and volume growth that outpaces the pricing cycle, that question will continue to weigh on its valuation.

FAQs

Why did Samsung stock fall if profits were record-breaking?

The stock had already rallied 147% year-to-date, pricing in much of the good news. The market is repricing the entire memory supercycle, not just Samsung. When profit growth is driven by industry-wide price inflation rather than company-specific competitive advantages, investors question sustainability.

Is Samsung's profit growth sustainable?

The current profit level is heavily dependent on DRAM and NAND price appreciation, which rose 44% and 53% respectively in Q2 2026. While AI demand should keep prices elevated through 2027, the rate of price increase is likely peaking, making year-over-year comparisons harder.

How does Samsung compare to SK Hynix in HBM?

Samsung trails SK Hynix in HBM market share and technology leadership. While Samsung began mass production of HBM4 in Q1 2026, SK Hynix has maintained a lead in HBM3E and HBM4 generations. HBM is the highest-margin memory segment, making this gap strategically significant.

What are one-time costs in Samsung's earnings?

Samsung's profit was reduced by special employee compensation costs from May 2026 labor union negotiations. These one-time items distorted the headline figure, but even after adjusting for them, the underlying growth remains overwhelmingly price-driven.

When will Samsung release full Q2 2026 details?

Samsung will publish its complete Q2 2026 earnings report on July 30, 2026, including detailed segment breakdowns for semiconductors, displays, mobile devices, and other divisions. This report will clarify HBM revenue contribution and Q3 guidance.