KuCoin Ventures Weekly Report: CLARITY Act Breakthrough and the Battle for Stablecoin Yields: A Watershed Moment for U.S. Crypto Regulation, While AI Earnings Underpin Global Risk Assets

2026/05/05 16:24:02

1. Weekly Market Highlights

Legislative Update on the CLARITY Act: Senate Markup Window Regains Market Attention

For an extended period, the market held a pessimistic outlook on the advancement of the U.S. CLARITY Act (Digital Asset Market Structure Bill). Due to conflicts between traditional banking interests and crypto-native yields, the bill faced significant resistance in Congress. The prediction market Polymarket previously priced its probability of passing at under 50%, reflecting the market's continued caution regarding the legislative timeline and final path to approval.

However, entering early May, key negotiators in the Senate Banking Committee, Thom Tillis and Angela Alsobrooks, released an updated text regarding the previously disputed "stablecoin yields" provisions. This development is viewed by the market as a positive signal for the bill to enter committee markup, making it a critical piece of marginal information in the crypto market this week. With the disclosure of the new text, the committee is expected to advance the markup process as early as mid-May 2026 or in the coming weeks.

From a market perspective, this progress has garnered attention primarily because stablecoin yield products involve a delicate balance of interests among crypto platforms, stablecoin issuers, the banking system, and user fund application scenarios. Below are the key focal points of this bill adjustment that the market is watching:

-

Prohibition of "Passive Holding Yields": The bill intends to prohibit crypto enterprises or trading platforms from paying users yields, rewards, or considerations that are solely based on stablecoin balances and are economically or functionally equivalent to interest-bearing bank deposits. Judging from the regulatory stance, the goal is not to ban all rewards; the core objective is to prevent platforms from essentially acting as "shadow banks" and absorbing deposits on a massive, unregulated scale.

-

Exemption for "Active Participation Rewards": In exchange, the bill allows crypto enterprises to provide "activity-based compensation". This means users must engage in genuine platform or on-chain interactions before crypto platforms can potentially issue stablecoin rewards. The specific definition of these interactions still awaits detailed clarification on "economic or functional equivalence" through subsequent rules from regulatory bodies like the Treasury and the CFTC.

Current public reports only indicate that relevant provisions are undergoing further discussion and adjustment; the specific scope of application, compliance requirements, and impacts on existing products remain to be clarified by the final text and regulatory interpretations. This likely means that if subsequent legislation and regulatory rules establish clearer boundaries for stablecoin yield arrangements, some USDC/USDT Rewards products offered by U.S. CEX platforms may need to reassess their product structures, user disclosures, reward sources, applicable regions, and campaign designs.

For instance, users might need to actively use stablecoins like USDC/USDT within the platform/wallet for payments, transfers, trading, platform consumption, or other genuine platform activities to earn cash back, points, or fee rebates. Market expectations suggest that stablecoin products provided by relevant institutions in the future may require adaptive adjustments in product design to align with potential positionings as "payment tools" or "bona fide business interactions," as regulators do not want exchanges packaging stablecoins into passive yield accounts resembling bank deposits.

The subsequent advancement of this bill is expected to have potential implications for the future underlying business logic and capital flows of the crypto industry:

-

Establishing Jurisdictional Boundaries: The bill draws a clear line between digital asset securities (under SEC jurisdiction) and digital asset commodities (under CFTC jurisdiction), fundamentally resolving the long-standing issues of fragmented regulation and jurisdictional ambiguity. Concurrently, it provides legal certainty for assets already ruled as non-securities by U.S. courts.

-

Reshaping Primary Market Issuance Pathways: The bill authorizes and requires the SEC to establish a new securities registration exemption rule. This rule allows specific digital asset projects to raise capital from the public without undergoing traditional full registration, with the core condition being that the project team must comply with right-sized regulatory obligations, including tailored disclosure requirements.

-

Strengthening Market Microstructure Protection: To prevent market manipulation, the bill establishes anti-evasion protections, ensuring companies cannot willfully circumvent securities laws through complex project structuring. Additionally, it implements resale restrictions for insiders to prevent "pump-and-dump" market manipulation.

Overall, the May progress of the CLARITY Act has heightened market attention regarding the formation of a U.S. digital asset regulatory framework, though it currently remains a phased change within the legislative process. Judgments on its industry impact should remain prudent, pending the final text, regulatory interpretations, and actual responses from market participants. Moving forward, we will closely track the final voting schedule for the bill in both chambers of Congress.

2. Weekly Selected Market Signals

AI Earnings Support Risk Assets, ETF Flows Help BTC Recover, While Inflation and Geopolitical Risks Limit the Easing Trade

The key theme across global risk assets this week was not simply the return of rate-cut expectations, but a more complex tug-of-war. On one hand, the U.S. economy and corporate earnings remained resilient, while AI-related earnings delivery and capital expenditure expectations continued to support risk appetite in U.S. equities. On the other hand, rebounding inflation data, Middle East tensions disrupting oil prices, and internal divisions within the Federal Reserve over the future easing path made it difficult for markets to return to a broad liquidity-driven easing trade. In other words, this week’s market performance looked more like an “earnings-driven recovery in risk assets” than a “rate-driven valuation expansion.”

On the macro front, U.S. first-quarter economic data and March PCE inflation together reinforced this contradictory environment. Growth has not shown signs of a clear loss of momentum, while inflation has picked up again. Energy prices and geopolitical risks are also creating renewed constraints on inflation expectations. March PCE rose to 3.5% year-on-year, while core PCE continued to grow on a month-on-month basis, suggesting that the Fed is unlikely to send a clear easing signal in the near term. The core shift in macro trading is that markets are no longer simply pricing in a “slowing economy — rapid rate cuts — higher risk asset valuations” path. Instead, they are repricing a combination of “resilient growth, sticky inflation, and higher-for-longer interest rates.”

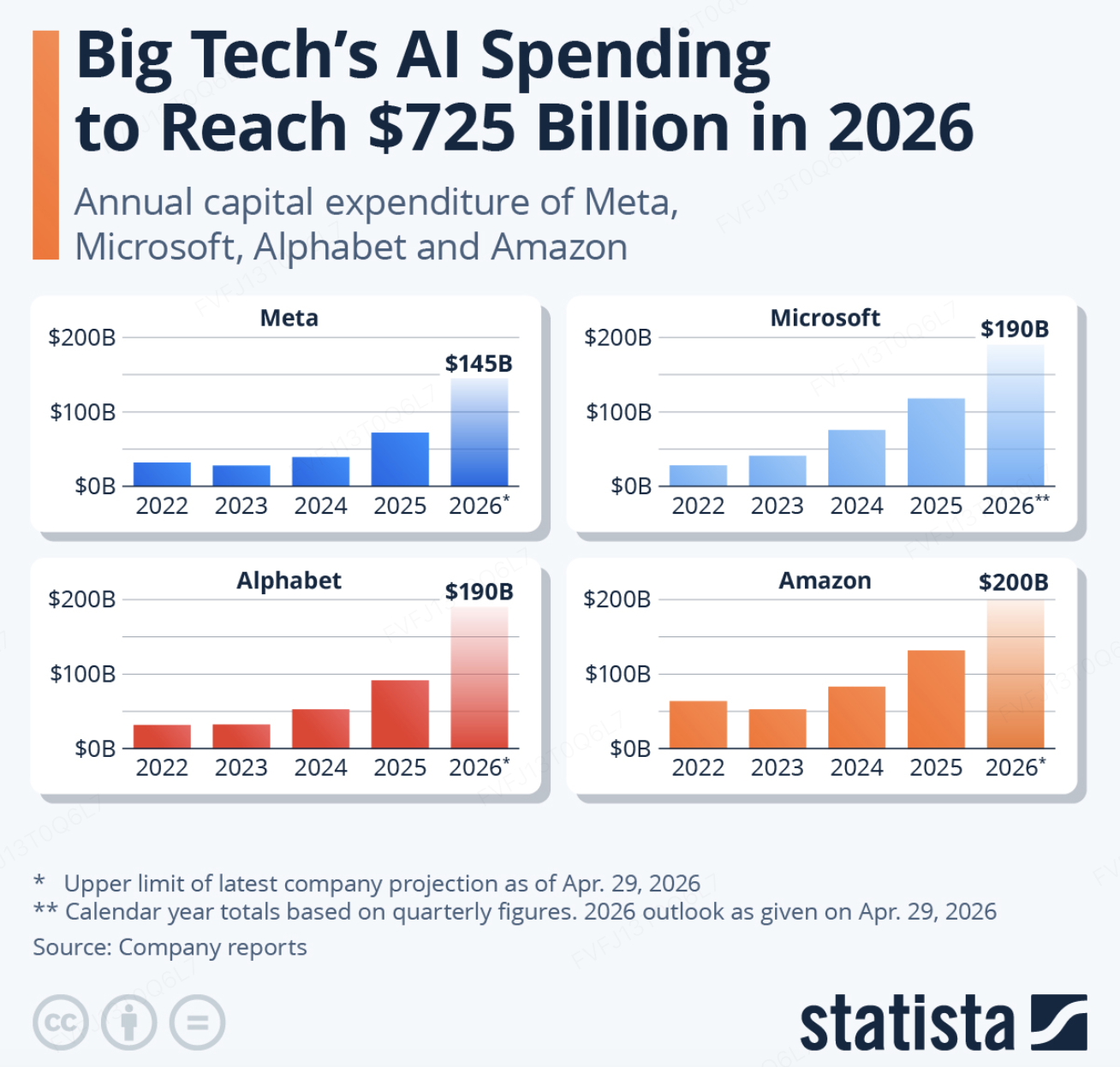

In equities, U.S. stocks continued to strengthen despite high oil prices and geopolitical risks, with the core support still coming from large-cap tech earnings and AI supply-chain momentum. The S&P 500 and Nasdaq both reached new closing highs on May 1, reflecting continued market confidence in AI capital expenditure, cloud demand, and enterprise AI monetization. More importantly, the AI trade is expanding from a competition around model capabilities into a broader contest involving compute investment, enterprise distribution, industry applications, and capital market refinancing capacity. On one hand, AI-related capital expenditure by Microsoft, Amazon, Meta, and Alphabet is expected to remain elevated in 2026. On the other hand, Anthropic has completed a $30 billion Series G round at a $380 billion post-money valuation, while recent market reports around a potential new high-valuation funding round and an AI joint venture with Wall Street institutions have further amplified expectations around the AI capital race. However, the market is not rewarding AI spending unconditionally. Meta came under pressure after raising its capex guidance, showing that investors are increasingly focused on whether AI investment can effectively translate into advertising efficiency, cloud revenue, enterprise software subscriptions, or developer tool revenue. Overall, this week’s U.S. equity rally was supported more by AI earnings and sector momentum than by a renewed sharp easing of rate expectations.

Data Source: TradingView

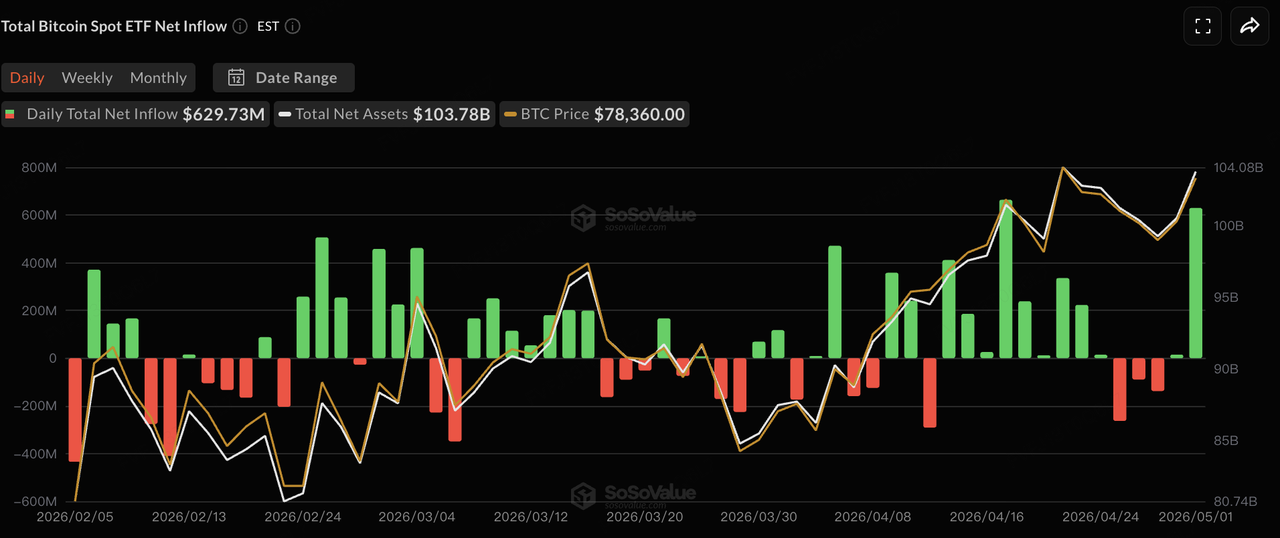

The crypto market continued its BTC-led structural recovery. BTC traded largely within the $75,000–$79,000 range this week, approaching the $80,000 level several times but failing to achieve a decisive breakout. Total crypto market capitalization was close to $2.6 trillion. Compared with equities, the crypto market’s recovery remains more dependent on fund flows and marginal improvements in risk appetite, with BTC ETF inflows still the most important variable. ETH and altcoins have not yet seen a broad-based spillover, suggesting that the market has not entered a phase of full risk appetite expansion. Capital continues to favor BTC, which offers the strongest liquidity and the clearest institutional allocation logic.

Data Source: SoSoValue

In ETF flows, U.S. spot BTC ETFs showed a pattern of initial weakness followed by recovery during the trading week. On April 27, BTC ETFs recorded a single-day net outflow of about $263 million, ending the previous nine-day inflow streak. Flows remained volatile toward the end of April, before rebounding sharply on May 1 with net inflows of about $630 million, led mainly by BlackRock’s IBIT and Fidelity’s FBTC. Looking at April as a whole, U.S. spot BTC ETFs recorded monthly net inflows of around $1.97 billion, marking one of the stronger monthly performances so far in 2026. This suggests that institutional capital has not withdrawn amid macro volatility, but is instead reallocating tactically while BTC consolidates at elevated levels.

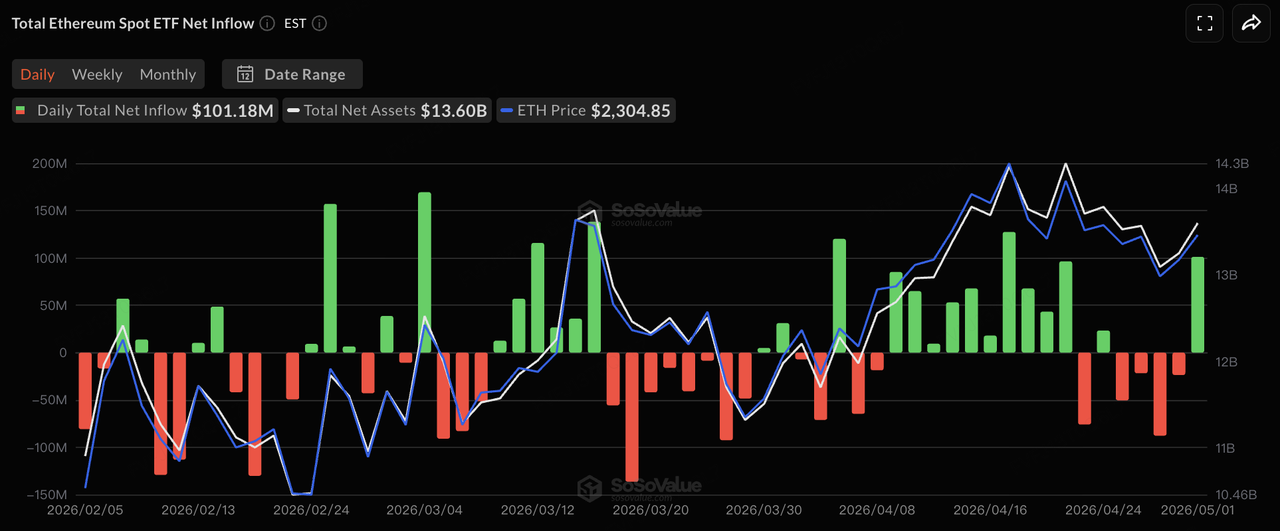

ETH ETF flows remained significantly weaker than BTC. Spot ETH ETFs saw consecutive net outflows in the first half of the week, before returning to net inflows on May 1. However, on a weekly basis, flows remained relatively weak. This reflects two issues: first, institutional allocators still prefer BTC as the core crypto exposure; second, although ETH has ecosystem, staking, and application-layer narratives, ETF flows have not yet formed the same level of sustained buying support seen in BTC. Whether ETH ETFs can shift from “trading-driven rebound flows” to “allocation-driven inflows” will still depend on ETH price performance, the progress of staking-yield products, and whether institutions reprice ETH’s native yield attributes.

Data Source: DeFillama

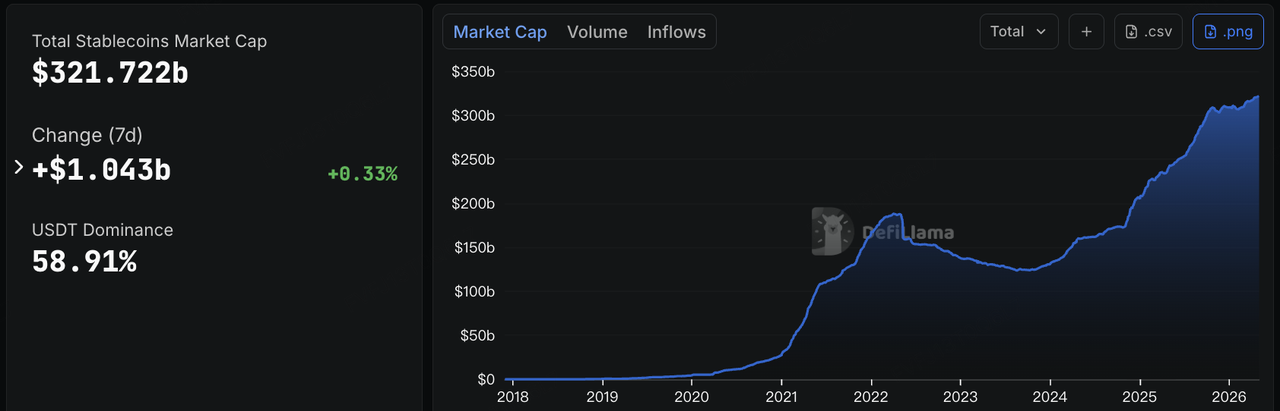

The total stablecoin market capitalization stood at around $321.7 billion, up about $1.04 billion over seven days, representing a weekly increase of around 0.33%. USDT’s market share was about 58.91%. This indicates that on-chain dollar liquidity remains in a phase of moderate expansion and has not contracted meaningfully despite macro uncertainty and geopolitical risks. Continued growth in total stablecoin supply usually suggests that the underlying liquidity pool of the crypto market is still expanding. However, the current pace is not aggressive. It reflects continued activity among existing capital and some incremental inflows, rather than a broad-based leverage expansion.

Structurally, USDT continues to dominate global trading liquidity, while USDC maintained modest growth. USDS saw a relatively notable weekly increase of around 6%, suggesting that protocol-based or yield-bearing stablecoins still have periodic appeal within specific ecosystems. It is also worth noting that USYC declined by around 11% this week. USYC is issued by Hashnote and became part of Circle’s RWA/yield-bearing asset strategy after Circle acquired Hashnote. Its scale fluctuation more likely reflects institutional reallocation among on-chain cash management, yield-bearing assets, and collateral use cases, rather than a contraction in the overall stablecoin market. Overall, this week’s stablecoin market was not characterized by rapid aggregate expansion, but by the structural continuation of “a solid base among major stablecoins, continued growth in compliant stablecoins, and greater divergence among protocol-based and yield-bearing stablecoins.”

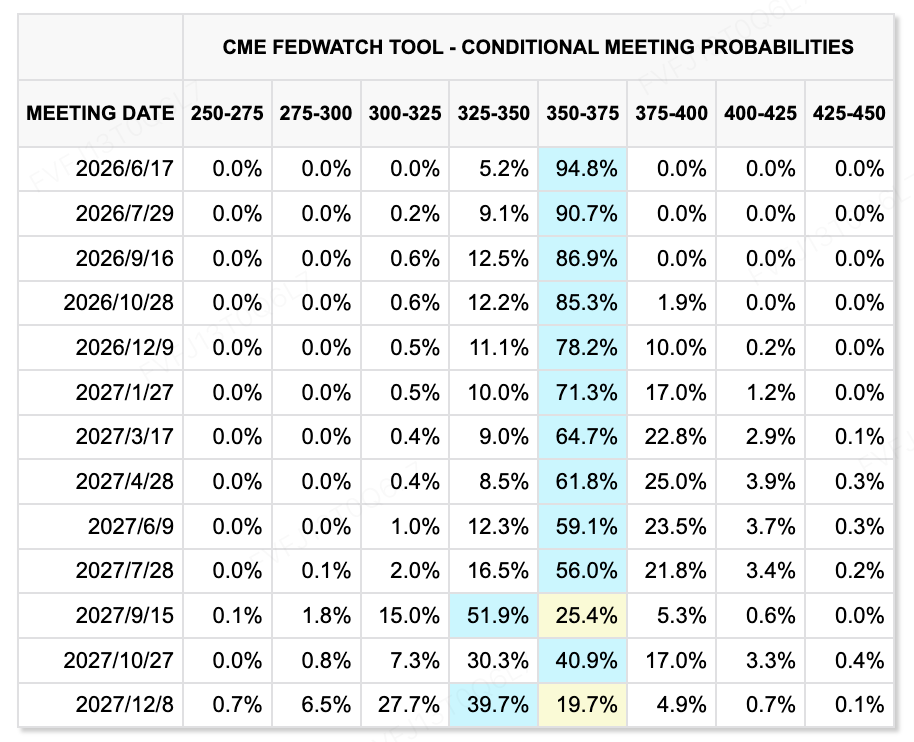

Data Source: CME FedWatch Tool

In terms of rate expectations, the Fed kept rates unchanged after its April policy meeting, while market pricing for rate cuts this year cooled significantly. Rather than focusing on specific official comments, the more important trend is that the committee appears divided over whether it should continue to retain an easing bias, while the market is increasingly accepting a policy path that does not require near-term rate cuts. The CME FedWatch Tool shows that the probability of no change at the June meeting has risen to around 94.8%, while the probability of a 25 bps cut is only around 5.2%. At the same time, several institutions have lowered or even removed their forecasts for rate cuts in 2026. As a result, the focus of rate trading has shifted from “when the first rate cut will come” to “how long rates will remain elevated,” which constrains valuation elasticity for both high-multiple tech stocks and crypto assets.

Macro Events to Watch This Week:

In the coming week, markets need to focus on three key threads:

-

Middle East tensions and developments around the Strait of Hormuz will continue to directly affect oil prices and inflation expectations. If energy prices remain elevated, the Fed’s room for easing will be further constrained.

-

U.S. employment data will be the key variable for repricing rate expectations. If the labor market remains resilient, expectations for rate cuts this year may be pushed back further. If employment cools meaningfully, markets may once again shift toward a “growth concern — policy pivot” trade.

-

The U.S. earnings season will continue to determine whether the AI trade can persist. Investors need to watch whether AI capital expenditure continues to be validated by revenue growth, and whether the market starts to more strictly differentiate between “reasonable AI investment growth” and “AI spending that erodes cash flow.”

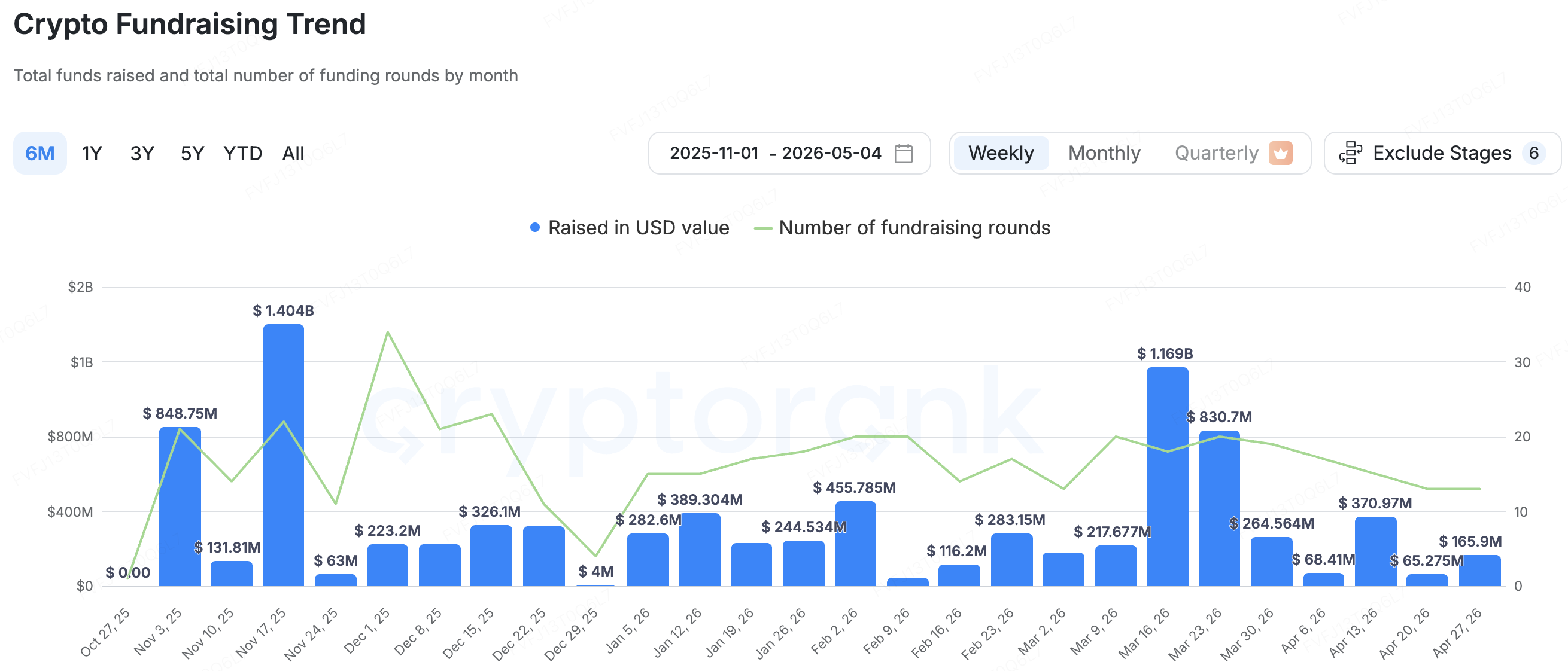

Primary Market Financing Observations:

Data Source: CryptoRank

In the primary market, according to CryptoRank’s statistical coverage, crypto VC funding cooled significantly in April. Monthly funding totaled about $659 million across 63 deals, down sharply by around 74% from $2.6 billion across 84 deals in March, marking a near two-year low. Total funding so far in 2026 reached around $5.64 billion. Structurally, the primary market has not fully frozen, but capital has clearly become more cautious. Investors are more inclined to back projects with real revenue, clearer exit paths, strong institutional backing, or explicit compliance-related use cases. Compared with the AI primary market, where high-valuation funding rounds continue, the crypto primary market remains in a phase of narrative screening and valuation compression. Early-stage projects driven purely by concepts are facing greater fundraising difficulty.

Payments infrastructure startup Fun completed a $72 million Series A round led by Multicoin Capital and SignalFire. The project provides crypto and fiat on/off-ramp infrastructure for platforms such as Polymarket, Lighter, and Aave, and processes more than $18 billion in annual payment volume. Against the backdrop of a cooling primary market, Fun’s large funding round shows that investors are still willing to pay a premium for “payment entry points built around the growth of on-chain applications.” As prediction markets, on-chain trading, and DeFi lending move toward higher-frequency and more mainstream use cases, on/off-ramp experience, payment channel stability, and anti-fraud risk controls are becoming critical infrastructure for scaling user adoption. However, the key test for this sector is not only payment volume growth, but whether these platforms can build a sustainable business loop across compliance costs, payment channel coverage, risk-control capabilities, and application-side user retention.

BlockStreet represents an M&A direction around stablecoin application layers and RWA infrastructure. The project is positioned as a multi-chain Launchpad and growth ecosystem built around USD1, aiming to promote its use across DeFi, payments, gaming, and RWA scenarios. Recently, BlockStreet was acquired by AI Financial for up to $43 million. Given that AI Financial has already established deep ties with World Liberty Financial, and USD1 is the dollar stablecoin launched by World Liberty Financial, this transaction appears less like a simple external acquisition and more like an organizational capability upgrade around the USD1 ecosystem, on-chain asset issuance, and RWA applications. Going forward, it remains important to monitor whether BlockStreet can bring real use cases to USD1, as well as potential risks related to the target company’s short operating history and the relatively strong related-party nature of the transaction.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.