SEC DeFi Front-End Exemption Explained: What the 5-Year Guidance Means for DEXs and Wallets

2026/04/15 14:06:02

The decentralized finance (DeFi) ecosystem moved into a new era of regulatory pragmatism on April 13, 2026, as the U.S. Securities and Exchange Commission (SEC) released landmark staff guidance regarding "Covered User Interface Providers." In what is being hailed as the "Five-Year DeFi Truce," the Division of Trading and Markets established a conditional safe harbor that allows decentralized exchange (DEX) front-ends and self-custodial wallets to operate without registering as broker-dealers.

This move represents a fundamental shift from the "regulation by enforcement" era that dominated the early 2020s. By carving out a specific category for software-only interfaces, the SEC has finally acknowledged the technical distinction between a centralized intermediary that executes trades and a passive software tool that merely facilitates user-initiated transactions. However, this is not a permanent green light; the guidance is an interim staff position set to expire—or "sunset"—in April 2031 unless it is codified into formal rulemaking.

For developers and investors alike, the stakes of this guidance cannot be overstated. With Ethereum’s Total Value Locked (TVL) currently hovering around $118 billion and cross-chain activity reaching all-time highs, the sudden removal of "broker-dealer" registration threats provides the breathing room necessary for the next wave of institutional DeFi adoption. This article explores the nuances of the "Covered User Interface" definition, the four non-negotiable conditions for compliance, and the strategic implications for the global digital asset market in 2026.

Defining the Covered User Interface Provider

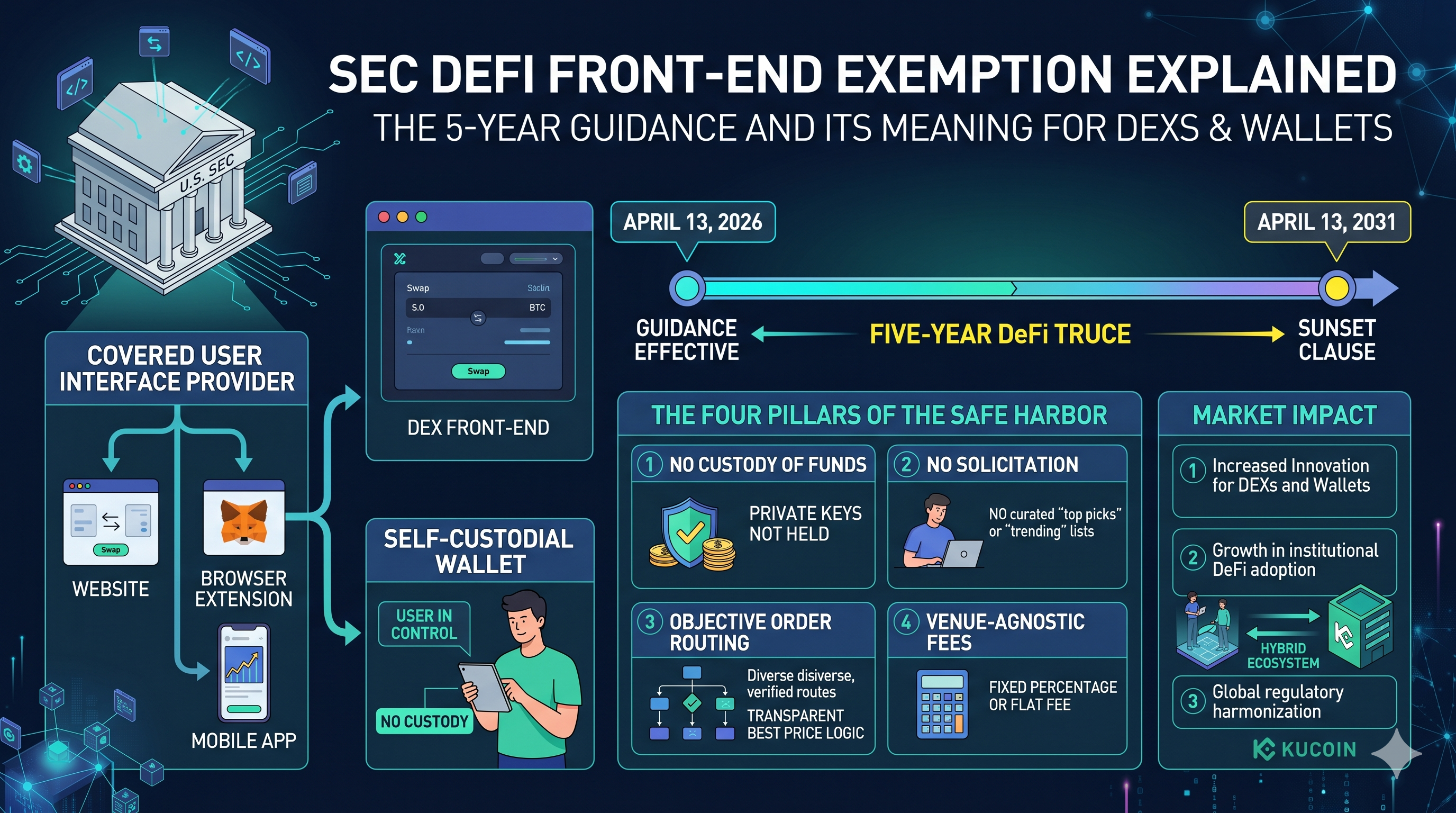

The core of the SEC’s April 2026 guidance lies in the newly minted term: "Covered User Interface Provider." The Commission defines this as any website, browser extension, or software application—including mobile apps—designed to assist users in preparing transactions in crypto asset securities through a self-custodial wallet. This definition is intentionally broad, covering everything from the primary domain of a major DEX like Uniswap to the dApp browsers integrated into mobile wallets.

The primary distinction being made here is between "active" and "passive" software. Under previous interpretations, the mere act of displaying a "swap" button or providing a price feed could have been construed as "effecting transactions" or "soliciting securities," both of which require a broker-dealer license. The 2026 guidance clarifies that if the software is truly an interface for a self-custody wallet, it is a tool, not a broker.

Crucially, the SEC has excluded centralized platforms and custodial services from this relief. If a platform holds user keys or stablecoins, it remains squarely within the traditional regulatory net. This reinforces the "not your keys, not your coins" mantra as a legal safeguard, not just a security best practice. By drawing this line, the SEC is incentivizing a shift toward pure non-custodial architecture, rewarding projects that relinquish control over user assets.

The Four Pillars of the DeFi Front-End Safe Harbor

To qualify for the non-enforcement promise, interface providers must adhere to four strict operational conditions. These pillars are designed to ensure the provider remains a neutral software vendor rather than an investment fiduciary or a market maker. The first condition is the absence of custody. The provider must not, at any point, take possession of user funds, private keys, or the stablecoins used to facilitate trades.

The second condition addresses solicitation. The interface must not recommend specific "crypto asset securities" or provide curated "investment advice." This means that "trending" lists or "top pick" badges on a DEX front-end could be legally hazardous. Compliance requires a neutral display where users must initiate the search or selection process independently.

The third pillar focuses on the logic of order routing. The guidance mandates that if an interface helps route a trade, it must use "objective and independently verifiable" market-data logic. In other words, a front-end cannot prioritize a specific liquidity pool simply because it has a back-end revenue-sharing agreement with that pool's developers. Transparency in how the "best price" is calculated is now a regulatory requirement.

Finally, the fee structure must be "venue-agnostic." The SEC will not recommend enforcement against providers that charge a transparent, fixed-percentage fee, provided that fee does not change based on which protocol or liquidity provider the user selects. This ensures that the interface provider has no financial incentive to steer a user toward a specific trade, maintaining the "passive" status of the software.

The Five-Year Sunset and the Path to 2031

Perhaps the most discussed aspect of the April 2026 release is the five-year "sunset" clause. This is not a permanent law but a staff interpretation that will be considered withdrawn on April 13, 2031. This "ticking clock" serves two purposes: it gives the industry immediate relief while forcing a long-term conversation about formal rulemaking and congressional action, such as the pending CLARITY Act.

The five-year window serves essentially as a probationary period for DeFi. The SEC is closely monitoring whether this "software-only" model might lead to increased market manipulation, or if it can successfully foster innovation while safeguarding users. For developers, the next five years represent a critical race to establish robust industry standards that can eventually be codified into law.

Many industry observers note that this window provides a vital bridge. While centralized exchanges continue to operate under their own stringent regulatory frameworks, the newfound clarity for decentralized front-end interfaces paves the way for a healthier "hybrid" ecosystem. This allows users to seamlessly transition between the high-liquidity, high-service environments of traditional centralized platforms and the permissionless, self-custodial world of DEXs—armed with a much clearer understanding of the distinct legal protections each provides.

Market Reaction and the XRP Ledger Precedent

While the SEC did not name specific assets in its guidance, market analysts were quick to apply the new rules to existing ecosystems. For example, the XRP Ledger (XRPL), which features a native decentralized exchange, saw a 4% price surge within 24 hours of the announcement. Traders viewed the guidance as "constructive" for XRPL-based interfaces, which have long struggled with the ambiguity of their native DEX functionality.

The logic is that if an interface for the XRPL DEX adheres to the four pillars—no custody, no solicitation, objective routing, and agnostic fees—it can now operate in the U.S. without the shadow of a "Wells Notice" looming over it. This has led to a flurry of development activity as teams begin to "de-permission" their front-ends to fit the new SEC criteria.

However, the SEC's Division of Trading and Markets was careful to note that this guidance does not settle the question of whether specific tokens themselves are securities. It only settles the question of whether the interface used to trade them makes the provider a broker. This distinction is vital: you can still be in trouble for selling an unregistered security, but you are less likely to be sued simply for providing the "swap" button that lets a user buy it on their own.

Implications for Crypto Wallets and Mobile dApp Browsers

Hardware and software wallet providers are perhaps the biggest winners of this 2026 guidance. For years, the "Buy/Sell" and "Swap" buttons inside popular wallets existed in a legal gray area. Critics argued that by integrating these features, wallet providers were essentially acting as unregistered brokers.

Under the new 5-year guidance, as long as the wallet remains self-custodial and uses neutral routing, these features are protected. This is expected to trigger a wave of "super-app" development within the wallet space. We are already seeing wallets integrate more sophisticated DeFi features, such as automated yield rebalancing and cross-chain bridging, all designed to fit within the "objective routing" pillar.

The impact on mobile dApp browsers is equally significant. By providing a clear definition of a "Covered User Interface," the SEC has given Apple and Google the regulatory "green light" to allow more robust DeFi apps on their respective stores. Previously, the fear of hosting an "unlicensed broker" led to the removal or crippling of many DeFi-related applications. With the 2026 guidance, the path to the "DeFi-on-Mobile" revolution is finally clear.

The Global Regulatory Domino Effect

The U.S. does not act in a vacuum. Historically, when the SEC provides a clear framework—even an interim one—other jurisdictions follow suit. Markets in Europe, already operating under MiCA, and Hong Kong, with its recent Stablecoin Ordinance, are looking at the SEC's "passive software" distinction as a way to harmonize global DeFi standards.

This harmonization is essential for global platforms that serve diverse user bases. Major centralized exchanges, for instance, benefit significantly when there is a consistent global understanding of where "software" ends and a regulated "financial service" begins. This regulatory clarity allows for more seamless integration between centralized liquidity and decentralized utility, ultimately creating a more robust "liquidity fly-wheel" for the entire digital asset industry.

As we look toward the 2030s, the "DeFi Front-End Exemption" will likely be remembered as the moment the U.S. government accepted that it cannot regulate code in the same way it regulates companies. By shifting the focus to "activity-based regulation"—where the activity of custody and solicitation is what triggers the law—the SEC has created a sustainable path for decentralized innovation.

Conclusion: Building on a 5-Year Foundation

The SEC’s April 2026 guidance is a rare moment of compromise in the often-adversarial relationship between regulators and the crypto industry. By providing a five-year safe harbor for DeFi front-ends and wallets, the Commission has acknowledged the unique nature of non-custodial software. While the four conditions for compliance are rigorous, they provide a much-needed roadmap for developers who want to build in the U.S. without fear of retrospective enforcement.

The challenge now lies with the developers. The industry has five years to prove that this "passive software" model is safe for retail investors. If the DeFi community can maintain high standards of transparency and security while adhering to the SEC’s pillars, the 2031 sunset might lead to a permanent, codified exemption. For now, the "Five-Year DeFi Truce" is the most significant regulatory victory the space has seen in a decade, setting the stage for a period of unprecedented growth and institutional integration.

FAQs

Q1: Does the SEC DeFi exemption apply to all DEXs?

No. It only applies to "Covered User Interface Providers" that meet four specific conditions: no custody of funds, no solicitation of specific transactions, the use of objective routing logic, and the charging of venue-agnostic fees. DEXs that manage their own order books or have custodial elements are not exempt.

Q2: Is this a permanent rule change?

No. This is staff guidance that is set to expire on April 13, 2031. It is intended to provide a temporary window of relief while the Commission considers formal rulemaking or waits for legislative action from Congress.

Q3: Can a wallet still offer a "Swap" feature under this guidance?

Yes, provided the wallet provider does not take custody of the assets during the swap and the routing of the swap is based on objective market data rather than an agreement to favor one specific liquidity provider.

Q4: Why is this called the "Five-Year DeFi Truce"?

It is referred to as a "truce" because it effectively pauses the SEC’s enforcement actions against passive DeFi software interfaces for a period of five years, allowing the industry to develop and prove its safety protocols.

Q5: What happens if an interface provider violates one of the four pillars?

If a provider takes custody, recommends specific tokens, uses biased routing, or charges discriminatory fees, they lose the protection of the safe harbor and may be subject to enforcement action for operating as an unregistered broker-dealer.