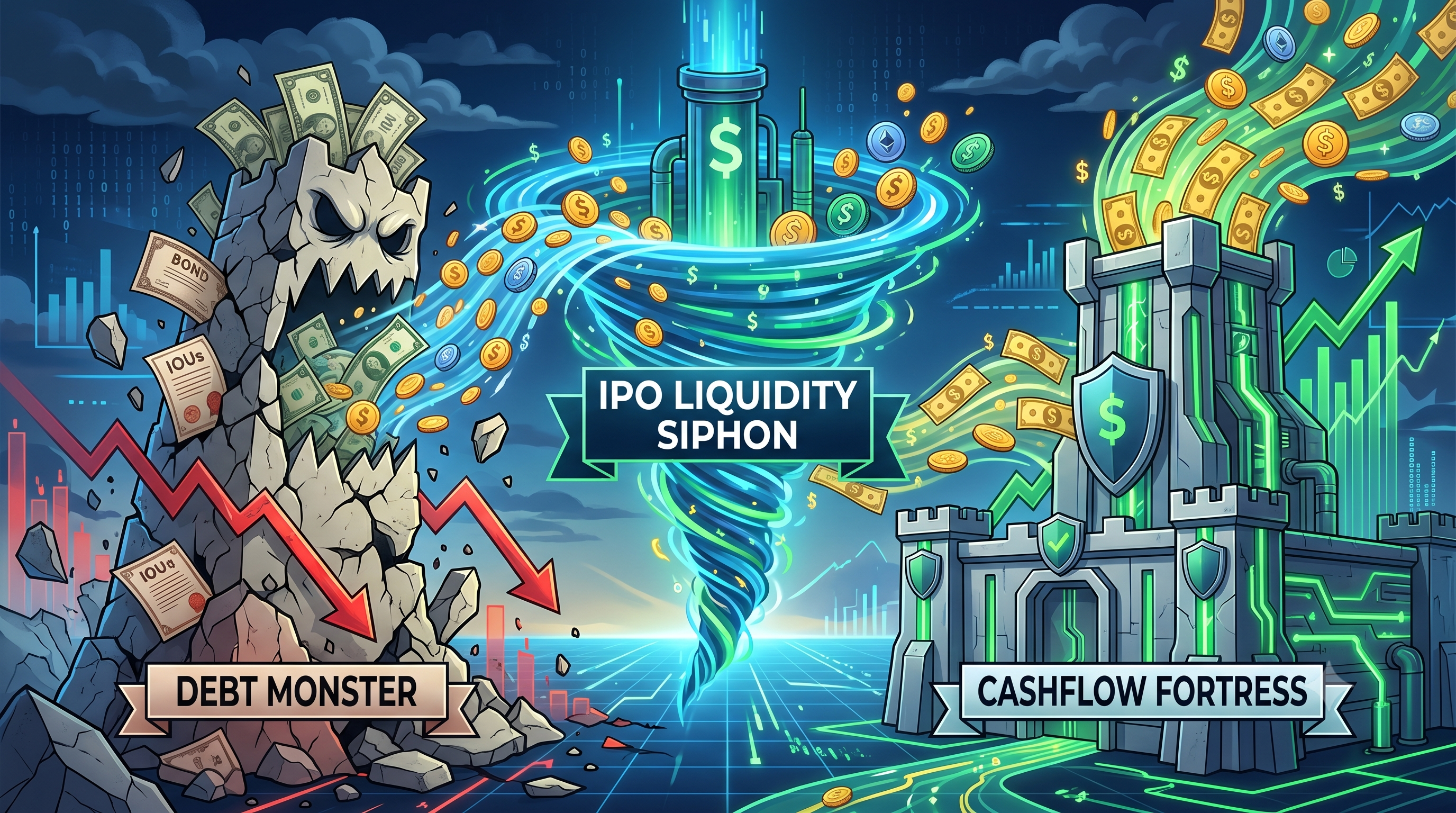

Debt Monster vs. Cashflow Fortress: Who Collapses First Under the $3.5T IPO Liquidity Siphon (MicroStrategy & Bitmine)

2026/06/11 17:32:00

The cryptocurrency corporate treasury landscape faces its most severe existential threat in 2026: the $3.5 trillion IPO liquidity siphon. With massive upcoming public debuts from SpaceX, OpenAI, and Anthropic absorbing available market liquidity, highly leveraged crypto treasuries are enduring unprecedented pressure. On one side stands the "Debt Monster," MicroStrategy (MSTR), which relies heavily on convertible debt to fund its staggering 845,256 Bitcoin reserve. On the other side stands the "Cashflow Fortress," Bitmine Immersion Technologies (BMNR), which utilizes staking yields from its massive 5.5 million Ethereum stash to weather market drawdowns. As institutional capital rotates aggressively out of digital assets and into these mega-IPOs, both treasury models are being stress-tested. Who collapses first under this immense macroeconomic squeeze? This article explores the vulnerabilities of both titans, contrasting rigid debt obligations against organic staking yields amid the relentless 2026 liquidity drain.

💡 Tips: New to crypto? KuCoin's Knowledge Base has everything you need to get started.

Key Takeaways

-

The $3.5T Liquidity Siphon: The unprecedented mega-IPOs of SpaceX, OpenAI, and Anthropic are actively draining capital from the crypto markets in mid-2026.

-

The Debt Monster (MicroStrategy): Holding over 845,000 BTC, MSTR faces immense structural risk due to its $6.7 billion convertible debt load and $15.5 billion in preferred stock obligations against minimal operating revenues.

-

The Cashflow Fortress (Bitmine): BMNR controls 5.5 million ETH and uses its Made-In-America VAlidator Network (MAVAN) to generate roughly $230 million to $297 million in annual staking cash flow.

-

The Verdict: MicroStrategy is structurally more likely to collapse first under a prolonged liquidity crunch because its fixed debt and dividend obligations require constant external capital or asset sales.

-

Market Outlook: Institutional capital is expected to return to crypto assets only after the massive mega-IPO wave concludes in late 2026.

MicroStrategy Collapses First Under Prolonged Liquidity Siphoning

MicroStrategy is significantly more vulnerable to a structural collapse than Bitmine under the $3.5 trillion IPO liquidity siphon because its debt-heavy balance sheet lacks organic crypto yield. MicroStrategy operates as a "Debt Monster," funding its 845,256 Bitcoin (BTC) treasury primarily through convertible debt and preferred stock issuances. In a severe liquidity crunch where external capital dries up, MicroStrategy’s minimal software revenues cannot service its massive obligations. Conversely, Bitmine operates as a "Cashflow Fortress," generating continuous, organic revenue by staking its Ethereum (ETH) reserves, allowing it to service costs without necessarily selling its core assets.

The fundamental divergence between these two corporate models becomes glaringly obvious during a macroeconomic liquidity drain. The 2026 financial environment is marked by an exorbitant cost of capital and shifting institutional focus. When major public offerings absorb the market's "risk-on" capital, asset prices drop. For MicroStrategy, a drop in Bitcoin's price compresses its net asset value (NAV) premium, cutting off its primary mechanism for raising new debt. It is forced to rely on its legacy software business—which generated a meager $124.3 million in Q1 2026—to support $6.7 billion in debt and $15.5 billion in preferred stock.

Bitmine Immersion Technologies (BMNR), on the other hand, actively monetizes its digital assets. By holding 5.5 million ETH and staking over 85% of it through its MAVAN platform, Bitmine generates up to $297 million in annualized staking revenue. This native cash flow provides a buffer against temporary price depreciations. Bitmine can use this yield to fund operations, pay dividends, or accumulate more assets, whereas MicroStrategy recently had to sell 32 BTC for $2.5 million just to meet preferred stock dividend obligations—a glaring crack in its "never sell" philosophy. Therefore, if the liquidity siphon persists, the rigid debt architecture of MicroStrategy will fracture long before the yield-generating fortress of Bitmine.

The $3.5T IPO Liquidity Siphon Explained

The $3.5 trillion IPO wave in 2026 is the primary catalyst aggressively draining liquidity away from the cryptocurrency sector and threatening leveraged treasuries. Driven by the mega-IPOs of SpaceX (valued at roughly $1.75 trillion), OpenAI ($852 billion), and Anthropic ($965 billion), institutional and retail investors are systematically liquidating crypto holdings to rotate capital into these generational tech equities. This massive capital rotation is creating a liquidity vacuum, suppressing digital asset prices and starving companies like MicroStrategy and Bitmine of the cheap external capital they relied on in previous years.

This IPO siphon operates as a zero-sum game in the high-interest-rate environment of mid-2026. Unlike the zero-interest-rate era of 2020–2021, margin borrowing is highly expensive today. Consequently, fund managers cannot artificially inflate their purchasing power; they must physically sell existing high-beta assets—like Bitcoin, Ethereum, and crypto proxy stocks—to fund their allocations in SpaceX and OpenAI. This dynamic has triggered consecutive weeks of multi-billion-dollar net outflows from major U.S. Spot Bitcoin ETFs throughout May and June 2026.

As $3.5 trillion in market value prepares to hit the Nasdaq and NYSE, the ripple effects are brutal for crypto corporate treasuries. A company built on continuous capital raising, such as MicroStrategy, suddenly finds Wall Street's wallet closed. The "FOMO" (Fear Of Missing Out) surrounding orbital data centers and artificial general intelligence has overshadowed the digital scarcity narrative. Until these mega-IPOs conclude and the locked-up capital is digested, the cryptocurrency market will remain starved of buy-side momentum, placing extreme stress on any firm carrying billions in debt backed by depreciating digital collateral.

MicroStrategy: The Inherent Vulnerabilities of the "Debt Monster"

MicroStrategy’s overarching vulnerability lies in its massive reliance on external debt and equity markets, making it incredibly fragile when macroeconomic liquidity vanishes. The company has essentially transformed from a software vendor into a leveraged Bitcoin ETF, accumulating a $64 billion digital treasury funded by $6.7 billion in convertible debt and $15.5 billion in preferred stock. When the IPO liquidity siphon drives Bitcoin prices down, MicroStrategy's collateral shrinks while its fixed financial obligations remain unchanged, creating a precarious imbalance that threatens corporate solvency.

This debt-driven model relies entirely on a continuous "financial flywheel" where Bitcoin goes up, MSTR stock trades at a premium, and the company issues more debt to buy more Bitcoin. However, the $3.5 trillion IPO wave has broken this flywheel. Investors are dumping MSTR shares to buy into space and AI narratives. As of early June 2026, MicroStrategy shares had declined substantially from their highs, and the company’s net asset value premium began to compress.

The danger of this strategy is the total lack of organic cash flow derived from the Bitcoin itself. Because Bitcoin is a non-yielding asset, holding 845,256 BTC produces exactly zero operational revenue. To service the interest on its convertible notes and the massive $1.7 billion in annual dividend obligations for its preferred equities, MicroStrategy must either rely on its traditional software business, issue more dilutive stock, or sell its Bitcoin. The software business is vastly undersized for this task. Consequently, any prolonged disruption in capital markets forces the company into cornered decisions, validating its reputation as a "Debt Monster" waiting for a margin call.

Staggering Debt Load Amid Dropping Bitcoin Prices

MicroStrategy’s $6.7 billion convertible debt pile is an existential threat precisely because it must be serviced and eventually repaid or converted, regardless of where Bitcoin is trading. As the IPO liquidity siphon drags Bitcoin closer to MicroStrategy’s average purchase price (hovering around $66,384 to $75,537 depending on recent tranches), the company’s balance sheet moves closer to negative territory. The firm was already forced to execute a $1.5 billion debt repurchase at an 8% discount in May 2026 just to manage its liabilities.

The most alarming signal for investors emerged during the week of May 26, 2026, when MicroStrategy sold 32 Bitcoin for $2.5 million to help fund preferred-stock distributions. While the dollar amount is trivial compared to their total stash, the philosophical implication is massive. Michael Saylor built the brand on an absolute "HODL" (Hold On for Dear Life) premise. Selling core collateral to meet a dividend obligation explicitly confirms that the software revenues are insufficient and that the debt obligations dictate treasury management.

If Bitcoin breaches the critical $66,000 support level and stays suppressed due to the capital flight toward SpaceX and OpenAI, rating agencies may further downgrade MicroStrategy’s credit. S&P Global Ratings previously assigned the company a junk-level credit rating due to risks arising from convertible debt maturities. If MSTR’s equity premium evaporates, it cannot issue new shares favorably. It will be trapped holding a depreciating asset against fixed, unyielding debt.

The Q1 2026 Warning Sign

The devastating impact of price volatility on a debt-heavy treasury was laid bare when MicroStrategy posted a staggering $12.5 billion net loss for the first quarter of 2026. This monumental deficit was almost entirely driven by a $14.46 billion unrealized markdown on its Bitcoin holdings. This earnings report proves that MicroStrategy’s financial health is entirely at the mercy of short-term market sentiment, making it a highly unstable entity during broader market liquidity drains.

While the loss is "unrealized" on paper, it heavily impacts the company's ability to maneuver. A $12.5 billion loss terrifies traditional institutional investors and credit rating agencies, driving up the cost of any future debt issuance. During this exact same quarter, the core software analytics business generated just $124.3 million in revenue. The disparity is terrifying: the company’s operating base is essentially a rounding error compared to the volatility of its digital assets.

This financial structure leaves zero room for error. Wall Street analysts have increasingly noted that MSTR’s small operating revenue base is actively increasing balance sheet risks. If the $3.5 trillion IPO wave keeps Bitcoin depressed for 12 to 18 months, MicroStrategy will burn through its USD reserves (which stood at $871 million in late May) just paying dividends and interest. Once the fiat reserves are gone, the "Debt Monster" will have no choice but to initiate large-scale liquidations of its Bitcoin treasury, potentially triggering a broader market crash.

Bitmine (BMNR): The Resilience of the "Cashflow Fortress"

Bitmine Immersion Technologies (BMNR) is vastly better equipped to survive the 2026 liquidity siphon because it organically generates massive cash flows from its treasury, rendering it far less dependent on external debt. By pivoting from traditional Bitcoin mining to becoming the world's leading Ethereum treasury company, Bitmine has amassed 5.5 million ETH (nearly 4.6% of the global supply). Because Ethereum is a yield-bearing asset under Proof-of-Stake, Bitmine operates as a "Cashflow Fortress," generating internal capital to weather the macroeconomic storm.

Unlike MicroStrategy's idle Bitcoin, Bitmine's digital assets are actively working. The company has staked approximately 4.72 million ETH through its institutional-grade MAVAN (Made-In-America VAlidator Network) platform. This strategic deployment generates an estimated $230 million to $297 million in annualized staking revenue at yields hovering near 3%. This organic, predictable cash flow fundamentally alters the corporate treasury paradigm. Even if the price of Ethereum drops drastically due to the $3.5T IPO liquidity drain, Bitmine still collects a massive influx of new ETH tokens daily.

This steady revenue stream provides a formidable defense mechanism. While MicroStrategy must scramble to raise debt or sell assets to cover expenses during a bear market, Bitmine can simply liquidate a portion of its freshly generated staking yield to cover operational costs, fund preferred dividends, and reinvest in infrastructure. The firm's $13.1 billion portfolio of crypto and cash includes hundreds of millions in pure cash reserves, alongside strategic stakes in AI companies. This diversified, yield-generating model acts as a financial fortress, capable of absorbing severe market shocks without fracturing its core holdings.

Staking Yield as a Survival Mechanism

The continuous staking yield generated by Bitmine’s Ethereum reserves is the ultimate survival mechanism against the $3.5 trillion IPO liquidity siphon. While capital flight starves non-yielding assets, Bitmine’s MAVAN platform acts as a perpetual cash-printing engine. By earning approximately $230 million to $297 million annually in native token rewards, Bitmine possesses a self-sustaining financial moat that insulates it from the credit market freezes threatening its peers.

This yield generation is critical during the 2026 market environment. When SpaceX and OpenAI drain retail and institutional dollars, equity markets punish companies that need to raise money. Bitmine does not urgently need to issue dilutive convertible debt because its assets pay a dividend internally. The 2.9% to 3% yield on 4.72 million staked ETH means Bitmine is constantly receiving thousands of new ETH tokens every week.

Furthermore, Bitmine’s staking infrastructure caters to third-party institutional investors, creating a secondary revenue stream akin to Software-as-a-Service (SaaS). As regulatory clarity improves in 2026, Bitmine is perfectly positioned to capture enterprise staking demand. This operational reality means that even if Ethereum’s fiat price drops 27% in a single month (as it did in May 2026), Bitmine’s actual token count and functional revenue continue to grow, reinforcing the fortress walls.

Weaknesses in the Fortress: Expanding Financial Losses

Despite its superior cash flow mechanics, Bitmine is not invincible, and its recent expanding financial losses highlight the risks of aggressive scaling during a liquidity crunch. Bitmine reported a staggering net loss of approximately $3.82 billion for fiscal Q2 2026, driven heavily by the depreciation of Ethereum against the US Dollar. Furthermore, the company recently issued a highly dilutive 9.50% Series A Perpetual Preferred Stock offering to raise capital, proving that even a cashflow fortress occasionally needs expensive external bailouts.

The $3.82 billion Q2 loss underscores a critical vulnerability: staking yields are paid in ETH, meaning the fiat value of that revenue shrinks precisely when the company might need cash most. During the broad cryptocurrency market downturn in early 2026, Ethereum significantly underperformed Bitcoin. As the value of its 5.5 million ETH stash plummeted, Bitmine’s balance sheet took a massive hit. The firm's quarterly revenue from traditional operations was only $11.04 million, revealing a disconnect between its core business size and its gargantuan crypto exposure.

Moreover, the decision to issue 3,000,000 shares of 9.50% preferred stock in June 2026 was punished severely by the market, driving the BMNR share price down over 10% in a single day. Layering in a high-cost perpetual security indicates that Bitmine is still heavily reliant on Wall Street to fund its ambitious "Alchemy of 5%" goal (aiming to own 5% of all ETH). If the IPO liquidity siphon continues to depress equity valuations, servicing a 9.50% dividend will drag heavily on Bitmine’s cash reserves, potentially forcing it to un-stake and sell ETH.

Comparative Analysis: Debt Servicing vs. Asset Yield

When comparing the two models directly, Bitmine's asset yield model mathematically outlasts MicroStrategy's debt servicing model during a prolonged capital drought. The core metric determining survival under the $3.5T IPO liquidity siphon is the ratio of unavoidable cash outflows to organic cash inflows. MicroStrategy suffers from massive, unavoidable cash outflows (debt interest and preferred dividends) with almost zero organic inflows from its treasury. Bitmine benefits from massive organic inflows (staking rewards) that can be dynamically adjusted to meet its outflows.

To illustrate this disparity, we can look at the basic balance sheet architectures of both companies in mid-2026.

| Metric | MicroStrategy (MSTR) | Bitmine Immersion (BMNR) |

| Core Asset | 845,256 Bitcoin (BTC) | 5.5 Million Ethereum (ETH) |

| Asset Yield Strategy | Non-yielding (Idle Reserve) | Staked (~85% active) |

| Organic Crypto Yield | $0 | ~$230M - $297M Annualized |

| Primary Risk | $6.7B Convertible Debt Maturity | ETH Price Depreciation |

| Recent Capital Move | Sold 32 BTC for Dividends | Issued 9.50% Preferred Stock |

This table clearly demonstrates why the "Debt Monster" is more fragile. MicroStrategy's enterprise value is artificially propped up by a net leverage amplification strategy. If the music stops and Wall Street stops buying MSTR stock at a premium, the debt still requires payment in fiat currency.

Bitmine, conversely, operates closer to a digital real estate holding company. Its assets generate "rent." While the value of the underlying real estate (Ethereum) may drop due to the mega-IPOs draining market liquidity, the tenant (the Ethereum network) continues to pay rent reliably. Therefore, while both stocks will suffer severe price drawdowns during the 2026 liquidity squeeze, MicroStrategy faces a tangible risk of forced liquidation to satisfy creditors, whereas Bitmine merely faces a period of reduced fiat-denominated profitability.

Navigating the turbulent waters of the 2026 crypto market requires agile strategies and access to top-tier liquidity. Whether you align with the Bitcoin maximalist vision of MicroStrategy or prefer the yield-generating Ethereum strategy of Bitmine, trading these volatile swings is essential for modern investors. KuCoin offers an unparalleled gateway into this dynamic ecosystem, providing deep liquidity, advanced charting tools, and access to hundreds of digital assets. Why watch institutional titans battle it out from the sidelines when you can actively hedge your portfolio? By utilizing KuCoin's staking features, margin trading, and real-time market insights, you can build your own digital cashflow fortress and thrive even while mega-IPOs siphon capital elsewhere. Join the millions of global users adapting to the new macroeconomic reality today.

Conclusion

The $3.5 trillion IPO liquidity siphon in 2026 is brutally testing the structural integrity of the cryptocurrency sector's largest corporate treasuries. As massive public offerings from tech giants like SpaceX and OpenAI aggressively drain risk capital from the market, both MicroStrategy and Bitmine Immersion Technologies are facing severe financial headwinds. However, our analysis concludes that MicroStrategy, the "Debt Monster," is far more likely to collapse first under prolonged pressure. Its absolute reliance on continuous external debt funding and a non-yielding asset (Bitcoin) leaves it dangerously exposed to margin pressures and forced liquidations.

Conversely, Bitmine’s "Cashflow Fortress" is inherently more resilient. By leveraging its 5.5 million Ethereum stash to generate nearly $300 million in organic, annualized staking revenue, Bitmine can internally fund its operations and ride out the macroeconomic storm without necessarily cannibalizing its core holdings. While both companies have recently suffered multi-billion-dollar paper losses and resorted to defensive financial maneuvers, yield generation remains the ultimate shield. Ultimately, until the 2026 mega-IPO wave subsides and institutional liquidity returns to digital assets, cash flow—not just asset accumulation—will dictate which crypto titans survive.

FAQs

What exactly is the $3.5T IPO Liquidity Siphon?

The $3.5T IPO Liquidity Siphon refers to a macroeconomic event in mid-2026 where several highly anticipated tech companies, including SpaceX, OpenAI, and Anthropic, are launching Initial Public Offerings. Because these companies carry enormous valuations totaling over $3.5 trillion, institutional and retail investors are selling off other high-risk assets, like cryptocurrencies, to raise the cash needed to buy into these new IPOs. This massive capital rotation drains liquidity from the crypto market, causing widespread price drops.

Why did MicroStrategy sell Bitcoin in June 2026?

MicroStrategy sold 32 Bitcoin for $2.5 million in early June 2026 specifically to help fund preferred-stock dividend distributions. This was a highly notable event because the company’s founder, Michael Saylor, has historically promoted a strict "never sell" philosophy. The sale indicated to the market that MicroStrategy’s traditional software revenue was insufficient to cover its financial obligations, forcing the company to liquidate a small portion of its core treasury to satisfy its investors.

How does Bitmine generate money from its Ethereum holdings?

Bitmine generates money through a process called "staking." The company holds 5.5 million Ethereum tokens and locks up (stakes) over 85% of them on the Ethereum network using its proprietary MAVAN platform. In exchange for helping secure the blockchain network, Bitmine earns rewards in the form of newly minted ETH. This process acts like a high-yield savings account, generating an estimated $230 million to $297 million in annualized revenue for the company based on mid-2026 yields.

What is a convertible debt note, and why is it risky for crypto companies?

A convertible debt note is a type of short-term loan that a company must repay with interest, but it gives the lender the option to convert the debt into company stock at a later date. It is highly risky for crypto companies like MicroStrategy because they use this borrowed fiat currency to buy highly volatile digital assets. If the value of the digital asset crashes, the company still owes the original fiat debt amount, which can lead to insolvency if they cannot raise new funds to pay off the maturing notes.

Will the cryptocurrency market recover after the 2026 mega-IPOs?

Market analysts widely predict that the cryptocurrency market will recover once the mega-IPO wave concludes. The current price suppression is largely a mechanical issue of capital availability rather than a fundamental flaw in blockchain technology. Once the IPOs are fully launched and trading normalizes, the locked-up capital will be digested, and excess institutional liquidity is expected to flow back into discounted "risk-on" assets, including Bitcoin and Ethereum, likely stabilizing corporate treasuries in the process.

Discliam: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency investments carry significant risk. Always conduct your own research before trading.