Chip Stocks Crash After Meta's AI Compute Pivot: Is This the Beginning of an AI Hardware Slowdown?

2026/07/02 11:16:00

Introduction

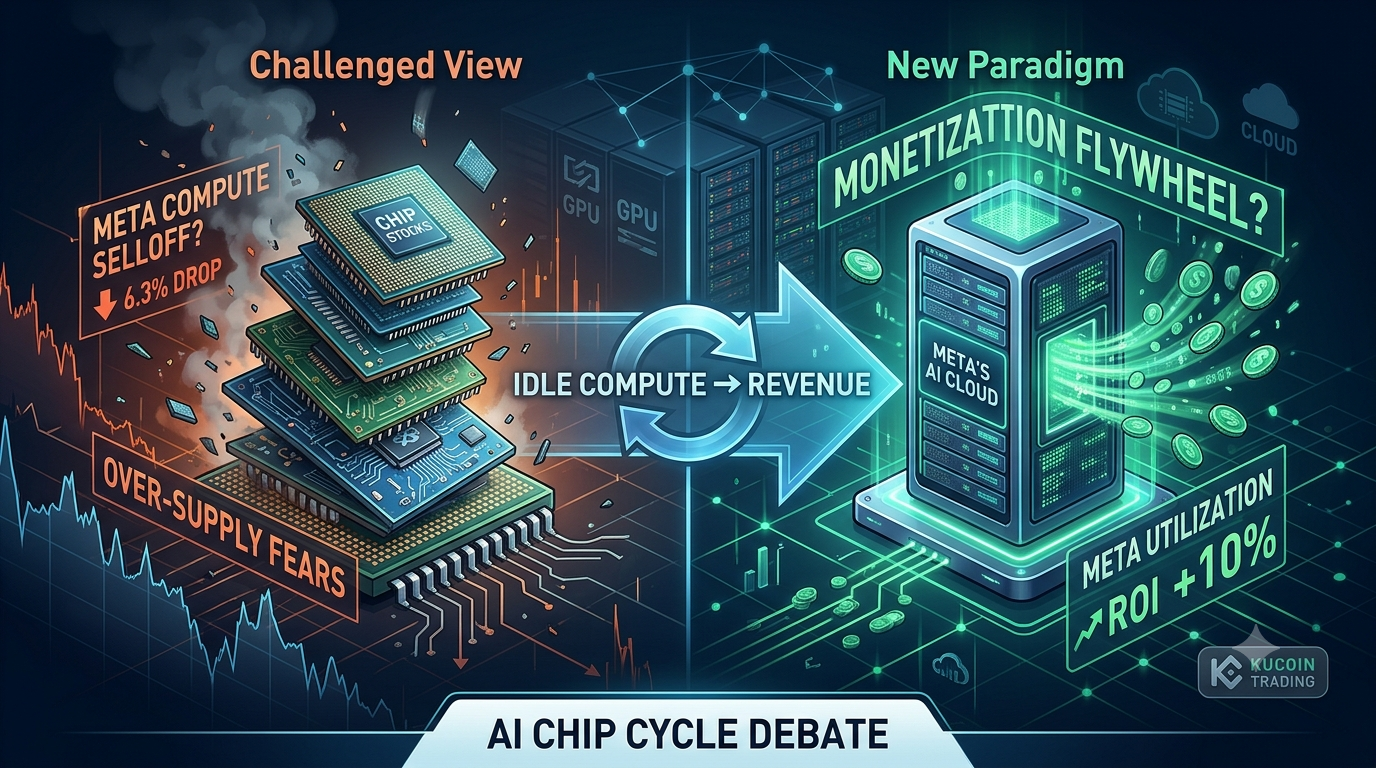

A single strategic shift erased billions of dollars from semiconductor valuations in one trading session. After reports emerged that Meta is developing a cloud business to rent out excess AI computing capacity, investors immediately questioned whether the AI infrastructure boom had moved from shortage toward oversupply.

The market reaction was violent. The Philadelphia Semiconductor Index dropped more than 6%, while multiple AI infrastructure names posted even steeper losses. Investors interpreted Meta's move in two opposite ways: either AI demand is weakening and hardware spending is peaking, or Meta has finally found a way to monetize idle assets and make future AI investment more sustainable.

This debate matters because Meta is not a marginal buyer. It is one of the largest AI infrastructure investors globally, and its capital allocation decisions increasingly shape expectations across semiconductors, data centers, networking, and cloud computing.

What Happened and Why Did Chip Stocks Fall?

The immediate answer is that investors suddenly started pricing in the possibility that AI compute supply may be catching up with demand.

Reports indicated that Meta is exploring a cloud infrastructure business that would allow external customers to rent AI compute capacity and potentially access AI models hosted on Meta infrastructure. The initiative would place Meta in competition with major cloud providers while generating returns from infrastructure that had originally been built for internal AI development.

Markets reacted as if this was a signal of excess capacity. According to recent market data, the Philadelphia Semiconductor Index fell approximately 6.3% during the session. AI infrastructure and semiconductor names broadly sold off as investors reassessed assumptions around perpetual hardware demand growth.

Among the sharpest declines discussed across markets:

| Company | Approximate Daily Move |

| Micron | -10.57% |

| Sandisk | -10.62% |

| Intel | -9.03% |

| Corning | -13% |

| ASML | More than -7% |

| AMD | More than -7% |

The logic behind the selloff was straightforward: if one of the world's largest AI spenders has idle compute available for monetization, perhaps the industry's assumption of endless GPU shortages is too optimistic. But that interpretation may be too simplistic.

Does Meta Selling Compute Mean AI Demand Has Peaked?

At least based on currently available evidence, this does not automatically mean AI demand has collapsed. The bearish argument assumes that Meta's move reveals structural oversupply.

Under this interpretation, Meta's AI model performance has not matched leaders such as Anthropic and OpenAI, causing internal compute utilization to fall below expectations. Instead of deploying all purchased infrastructure internally, Meta is attempting to recover returns through cloud services.

If that logic spreads across the market, investors begin questioning the entire AI hardware narrative. Hardware suppliers are particularly vulnerable because valuation models often assume continued double-digit infrastructure expansion. If compute becomes shareable rather than continuously purchased, future orders could moderate.

However, the current evidence remains incomplete. Reuters reported that Meta's cloud initiative is still under development and may change materially before launch. Analysts cited in coverage suggested the largest impact may fall on newer compute-rental businesses rather than established hyperscalers.

That distinction matters. Selling spare capacity is fundamentally different from stopping infrastructure investment.

Why Bulls Think Meta's Strategy Could Actually Extend the AI Cycle

The bullish interpretation is that Meta is becoming financially disciplined rather than technologically defensive. Meta spent the past several years aggressively accumulating AI infrastructure. Investors increasingly questioned whether such enormous capital expenditure could generate acceptable returns.

Recent reporting suggests Meta's annual AI infrastructure spending could reach as much as $145 billion.

Under the bullish case, compute rental creates a flywheel. The argument works like this:

-

Build AI infrastructure.

-

Use idle periods to generate revenue.

-

Improve asset utilization.

-

Increase confidence to continue buying hardware.

In this framework, compute becomes similar to airline seats or hotel rooms — unused capacity represents lost economics.

Meta's strategy could therefore make future GPU purchases more sustainable rather than smaller. Some analysts have framed the move as capital optimization rather than retreat. Meta's ability to commercialize infrastructure could reduce concerns that AI spending has become an endless cash burn.

This helps explain why Meta stock itself rallied sharply despite semiconductor weakness. According to market reporting, Meta gained roughly 9%-10% following the news as investors welcomed the possibility of monetizing previously nonproductive infrastructure assets.

Wall Street may not be rewarding lower AI ambition. It may be rewarding improved ROI.

Why Wall Street Is Rewarding Meta but Punishing Chip Stocks

Because the market is rewarding utilization and questioning expansion.

For months, one of the largest concerns surrounding AI leaders was whether infrastructure spending had become disconnected from monetization. Meta's cloud initiative introduces a new narrative.

Instead of evaluating infrastructure only through model quality or AI market share, investors can evaluate return on invested capital. Even modest monetization could change sentiment.

If excess compute generates billions in incremental revenue, investors may conclude that AI infrastructure is becoming economically productive rather than permanently speculative. That does not necessarily help chip manufacturers.

Semiconductor valuations depend heavily on future order assumptions. If hyperscalers increasingly share infrastructure, rent compute, or improve utilization rates, hardware order growth may normalize even while AI demand continues rising.

Those are two very different outcomes. AI usage can grow while hardware growth decelerates. That distinction may define the next phase of the AI cycle.

Could Other Tech Giants Follow Meta?

This is the question that matters more than Meta itself. Right now, there is insufficient evidence that the broader hyperscaler industry is preparing to reduce infrastructure investment.

But investors are watching closely. The companies receiving the most attention include Microsoft, Amazon Web Services, and Google because they collectively represent enormous AI infrastructure demand.

If these companies begin signaling:

-

lower capex growth,

-

compute monetization,

-

slower GPU purchasing,

-

utilization optimization,

Then semiconductor investors may need to revisit long-term growth assumptions. Until then, Meta remains a sample size of one. That is not enough evidence to declare the AI hardware bull market over.

History shows technology cycles rarely move in straight lines. Infrastructure booms frequently transition into monetization phases before the next investment wave begins.

Should You Trade AI Infrastructure Narratives on KuCoin?

Traditional equity narratives increasingly spill into crypto markets. AI infrastructure sentiment frequently affects sectors such as AI tokens, decentralized compute projects, data infrastructure protocols, and broader market risk appetite.

For traders who want exposure to macro technology narratives while maintaining access to digital asset markets, KuCoin provides access to spot markets, derivatives, and thematic sectors linked to AI and emerging technologies.

The key is not chasing headlines. Short-term volatility often creates opportunities, but disciplined position sizing and risk management remain more important than predicting whether a single corporate decision changes an entire investment cycle.

Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

Meta's decision to explore selling excess AI computing power triggered one of the sharpest semiconductor pullbacks of the year because it challenged a core market assumption: that AI infrastructure demand only moves in one direction.

Bearish investors see the move as evidence of compute oversupply and weaker future hardware growth. Bullish investors see something entirely different — the emergence of a more sustainable economic model for AI investment.

At this stage, neither side has enough evidence to declare victory. Meta's reported cloud initiative remains under development, and there is little indication today that major hyperscalers are abandoning AI expansion plans.

What is clear is that Wall Street rewarded financial discipline. Markets appear increasingly willing to support AI investment when spending becomes measurable, monetizable, and tied to returns.

Whether this becomes the start of a broader capital efficiency trend — or simply a temporary repricing event — will depend on what Microsoft, Amazon, and other hyperscalers do next.

FAQs

-

Why did Meta stock rise while chip stocks fell?

Investors viewed compute monetization as improving Meta's return on infrastructure spending while potentially reducing future hardware demand growth.

-

Does selling AI compute mean Meta is abandoning AI?

Not necessarily. Current reporting suggests Meta is exploring monetization rather than ending AI investment.

-

Which companies are most exposed if compute demand slows?

Semiconductor manufacturers, networking providers, optical infrastructure firms, and compute rental companies could be affected most directly.

-

Could compute rental become a standard industry model?

Possibly. If utilization economics improve, other large infrastructure owners may experiment with similar approaches.

-

Is this the end of the AI hardware bull market?

Current evidence does not support that conclusion. Investors need to monitor whether other hyperscalers follow Meta's approach before drawing broader conclusions.