Everything You Need to Know about Crypto Lending in 2026

Introduction

Crypto lending has evolved from a niche decentralized finance (DeFi) experiment into one of the most widely used passive income and liquidity solutions in the digital asset industry. In 2026, both retail and institutional investors are increasingly using crypto lending platforms to earn yield on idle assets, unlock liquidity without selling long-term holdings, and access capital in a more flexible way than traditional banking systems.

As the cryptocurrency market matures, lending products have also become significantly more sophisticated. Modern crypto lending platforms now integrate advanced risk management systems, automated liquidation engines, overcollateralization models, and stablecoin-based lending markets to reduce volatility exposure. At the same time, regulatory scrutiny around digital asset lending has intensified following several major industry collapses in previous market cycles, making platform transparency and asset security more important than ever.

For long-term holders who prefer to HODL Bitcoin, Ethereum, or stablecoins instead of actively trading, crypto lending offers an alternative strategy to generate passive income while maintaining market exposure. Borrowers, meanwhile, can access liquidity without selling their crypto assets, allowing them to participate in trading, portfolio diversification, or short-term funding opportunities.

This guide explains how crypto lending works, its benefits and risks, how to evaluate lending platforms safely, and why platforms like KuCoin Lending continue to attract global crypto users looking for flexible yield opportunities in the evolving digital asset economy.

What Is Crypto Lending?

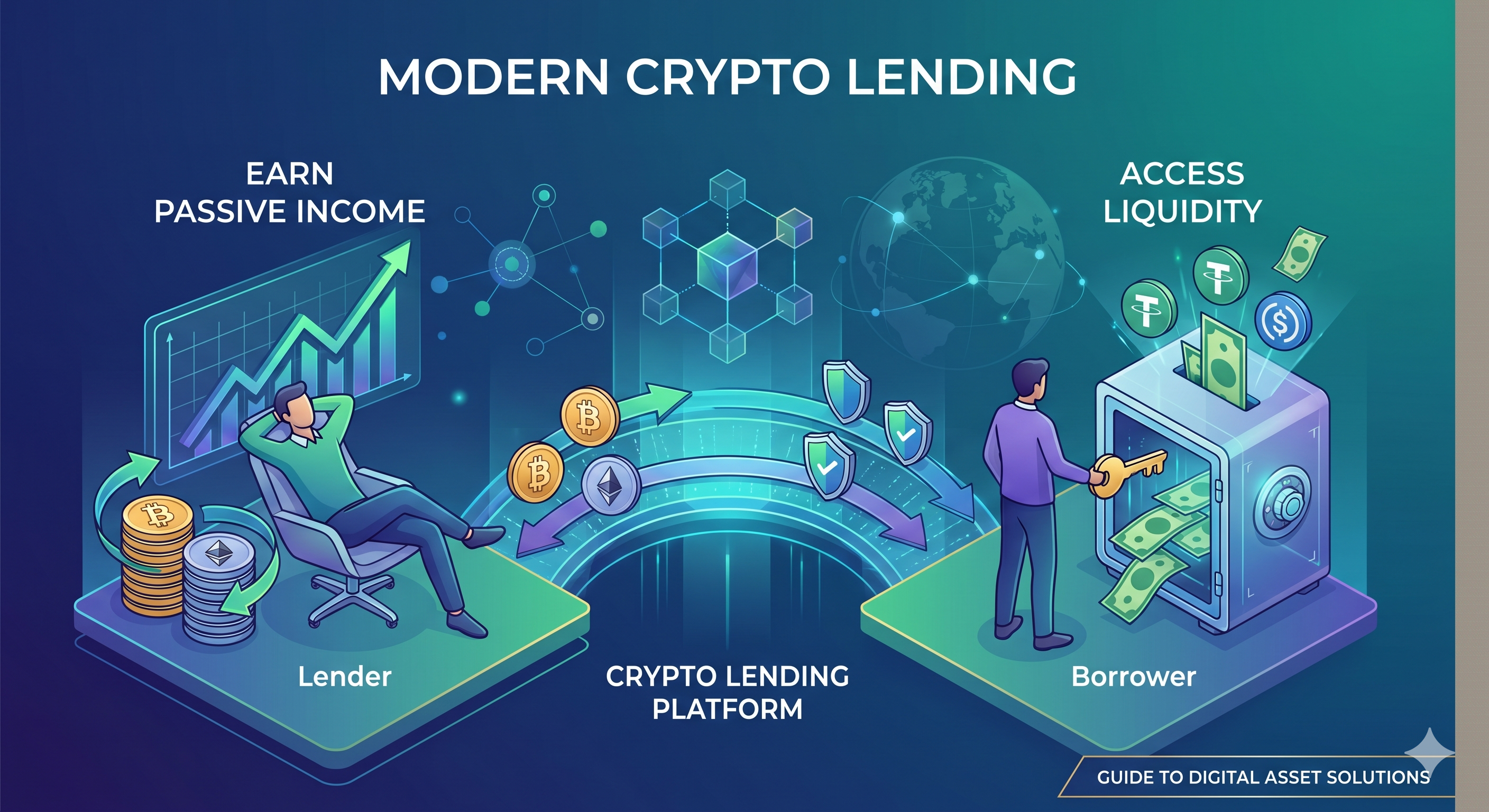

Simply put, crypto lending is an alternative investment strategy that allows investors to lend cryptocurrency to borrowers in exchange for interest. In essence, this system comprises two parties – the lender and the borrower.

Note that this is not a loan without collateral. The lender receives interest from the borrower in exchange for the loan, while borrowers deposit crypto assets as collateral to secure investors' investment. This serves as a guarantee for the lender; if anything goes wrong, they can use this collateral as a form of compensation.

How Does Crypto Lending Work?

Cryptocurrency lending mode of operation is similar to p2p lending. Lenders and borrowers get to connect via an online platform. However, instead of fiat currency, crypto lending transactions use cryptocurrencies.

Crypto lending may vary based on the platform used; however, the primary concept remains the same. Lenders make their crypto assets available at set rates. Generally, users often lend their crypto assets for two primary reasons: margin lending and personal use. Once a lender's fund is available, the borrower - who has concluded that a particular coin’s price will appreciate - will ask to lend a part of the fund available at that moment. The borrower will then repay the loaned cryptocurrency with the assigned interest rate over a certain time period.

The Evolutoin of Crypto Lending in 2026

The crypto lending industry has changed dramatically over the past few years. During the early stages of decentralized finance, many lending platforms focused primarily on offering extremely high yields with minimal transparency. However, several high-profile market collapses and liquidity crises between 2022 and 2025 forced the industry to mature rapidly.

In 2026, sustainable yield generation and risk management have become the primary focus of both centralized and decentralized lending platforms. Most major platforms now rely heavily on overcollateralized loans, real-time collateral monitoring systems, automated liquidation mechanisms, and proof-of-reserve transparency practices to improve user confidence.

Stablecoin lending has also become increasingly popular. Instead of lending highly volatile assets, many users now prefer lending stablecoins such as USDT, USDC, and decentralized stable assets to earn more predictable returns while reducing exposure to sharp market fluctuations.

Another important trend is the growing participation of institutional investors in crypto lending markets. Hedge funds, market makers, and crypto-native trading firms increasingly use digital asset lending for liquidity management, arbitrage strategies, and capital efficiency. As a result, crypto lending is no longer viewed solely as a retail DeFi activity but as a developing segment of the broader digital financial ecosystem.

At the same time, users have become more cautious when selecting lending platforms. Security architecture, platform reputation, insurance mechanisms, and reserve transparency are now considered far more important than simply chasing the highest annual percentage yields (APYs).

How to Invest in Crypto Lending

Before participating in crypto lending, investors should understand the difference between centralized finance (CeFi) and decentralized finance (DeFi) lending platforms.

Centralized crypto lending platforms are operated by exchanges or companies that manage custody, matching systems, liquidation processes, and risk controls on behalf of users. These platforms often provide a more beginner-friendly experience, simplified interfaces, customer support, and integrated security systems. However, users must trust the platform to manage their assets responsibly.

Decentralized lending protocols, on the other hand, rely on smart contracts instead of intermediaries. Users maintain greater control over their funds and can interact directly with blockchain-based lending markets. While DeFi platforms offer increased transparency and composability, they may also expose users to smart contract vulnerabilities, oracle risks, and protocol exploits.

For beginners entering the crypto lending market, it is generally recommended to prioritize platforms with strong liquidity, transparent reserve systems, advanced security infrastructure, and an established operational history. Investors should also diversify risk rather than allocating all assets to a single lending platform or protocol.

In addition, users should pay close attention to lending terms such as collateral requirements, annual yield rates, lock-up periods, liquidation thresholds, and supported assets before committing funds.

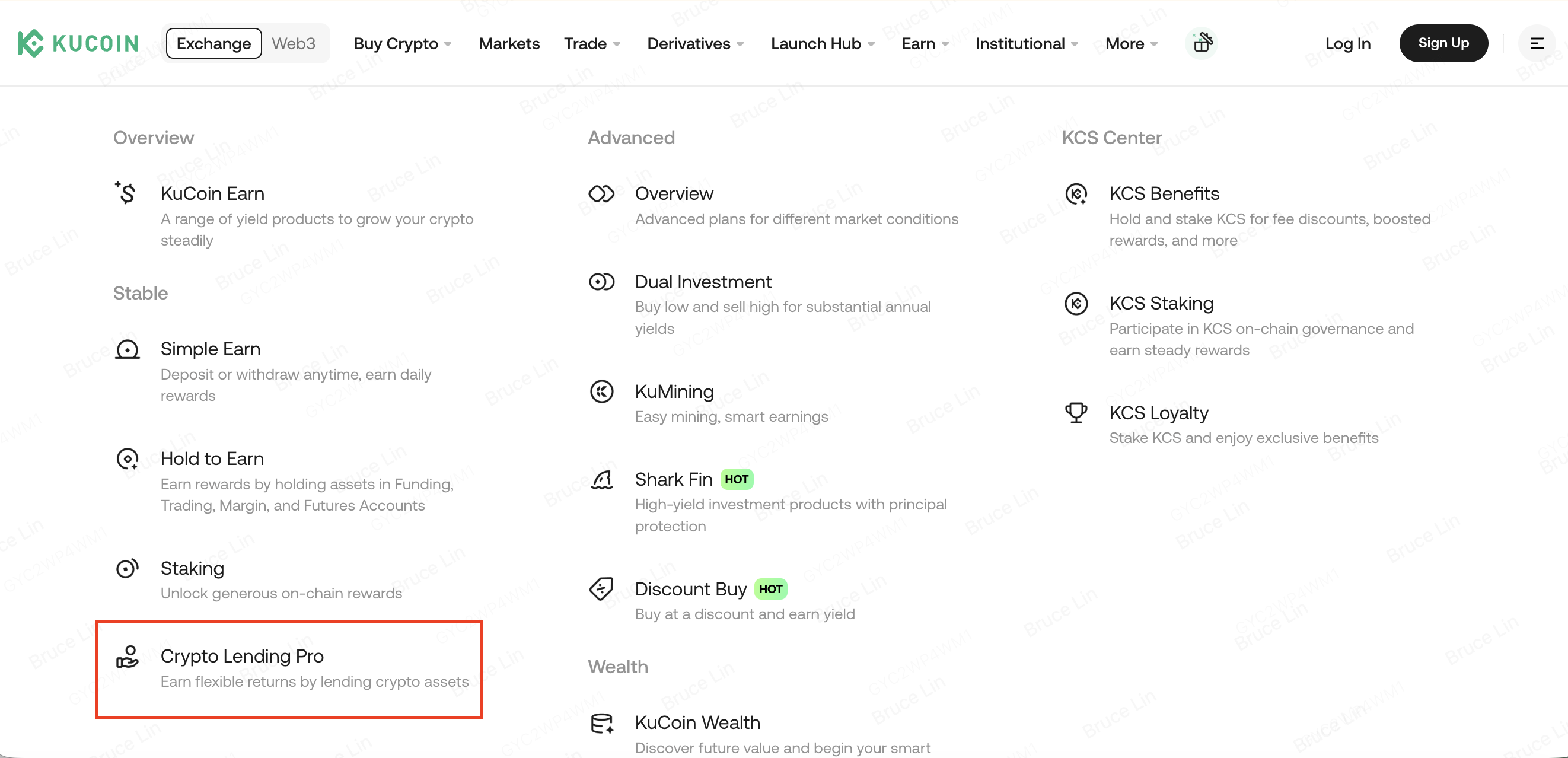

Crypto Lending on KuCoin

Among the many crypto lending platforms available today, KuCoin Lending remains one of the most recognized centralized crypto lending solutions for global users.

KuCoin Lending allows users to lend supported cryptocurrencies to margin traders and earn passive income through interest payments. The platform supports flexible lending durations and automated lending tools that help users optimize idle digital assets efficiently.

One of the key advantages of KuCoin Lending is its integrated risk control framework. The platform uses collateral management systems, automatic liquidation mechanisms, and continuous account monitoring to help reduce counterparty risk within the margin ecosystem. This infrastructure helps protect lenders even during periods of elevated market volatility.

KuCoin has also continued expanding its broader ecosystem in recent years, including trading, wealth management, Web3 services, and AI-powered trading tools, allowing users to manage multiple crypto investment strategies within a single platform.

For users seeking relatively accessible passive income opportunities without directly participating in complex DeFi protocols, KuCoin Lending offers a simplified entry point into the crypto lending market.

Crypto Lending Investment: What to Pay Attention to

The primary thing you should note as an investor is the collateral presented against the loan. The collateral's worth should be more than that of the loan, usually in cryptocurrencies such as ETH and BTC.

Several platforms implement an LTV (Loan-to-value) ratio of approximately 58%, which denotes that borrowers will get less than 58% of the offered collateral's worth.

Owing to its volatility, crypto collateral is subject to sudden depreciation, resulting in a significant loss on the lender's end.

Is Crypto Lending Safe?

One of the more commonly asked questions by people looking to delve into the crypto lending space is - is crypto lending safe? The answer to this question will greatly depend on the preferred platform.

Advantages of Crypto Lending

Multiple advantages accompany crypto lending. As a lender, it offers you an income-generating opportunity by lending your digital assets to the users, offering the ones they are not using at the moment or planning to sell. This presents a profitable opportunity as this form of lending can generate higher interest than traditional savings.

Crypto lending is also a swift process than traditional lending because creating a lenders account only takes minutes. Besides, KuCoin crypto lending platform also has tools that ensure the automatic payment of funds and interests to the lenders.

Considering the range of benefits this system offers, it seems like it is a flawless one; but it isn't. There are some risks you should expect as a lender and as a borrower.

Crypto Lending Risks

Every aspect of the finance industry has its risks - none is entirely risk-free. Although risks may be fairly low in the crypto lending system, there are some things you must be aware of before deciding to venture into the sector.

1)Absence of regulation

The regulatory structure surrounding digital assets such as Bitcoin is rapidly changing. This may complicate the process of debt collection whenever a borrower defaults on the loan.

The cryptocurrency market is well-known for its inconsistent or non-existent regulatory structure. While some countries are trying to reduce adoption by banning the use of cryptocurrencies, others are slowly trying to regulate it. Hence, there is no global regulatory agreement. Due to this issue, legal crypto-related problems often experience varying treatments depending on the country of residence or jurisdiction. Therefore, suppose any loan defaulting occurs, recovering your assets or interest may be pretty complicated.

2)Transactions with international borrowers

Crypto lending is a process that borrowers and lenders from all around the world can participate in. However, the partial or full anonymity of cryptocurrencies leaves room for potential abuse. It may be challenging to take steps towards debt-collection against individuals who do not reside in the same country. This risk may and may not affect you, as some platforms solved this problem already by implementing various functionalities.

3)BTC and other cryptocurrencies' volatility

One major downside of crypto-based loans is the overall volatility of the underlying cryptocurrency. For instance, if a borrower is to pay $1000 in Bitcoin and the lent-out BTC value doubles over the loan term, the lender will surely lose half of their investment as the borrower will only repay the $1000 worth of Bitcoin.

4) Digital theft

Several Bitcoin lending and investment platforms may require you to hold your asset on their platform. However, this method of holding funds is extremely unsafe, mainly because you do not own the private keys to your wallet. On top of that, these platforms have traditionally been targeted by hackers.

5)Platform failure

Due to the absence of legislation, multiple crypto lenders tend to depend on their loan transaction platforms. However, most of these platforms are currently weak and financially unstable, which may cause them to fail at any time. Hence, conducting comprehensive research before selecting a crypto lending platform is a necessity. KuCoin has a long and successful history of keeping its customers safe and satisfied.

Conclusion

Crypto lending has become an important component of the modern digital asset economy, offering both lenders and borrowers greater capital efficiency than traditional financial systems. For long-term crypto holders, lending can provide an additional source of passive income without requiring active trading. Borrowers, meanwhile, can unlock liquidity while maintaining exposure to their digital assets.

However, crypto lending is not without risks. Market volatility, platform security, regulatory uncertainty, and liquidity crises remain important factors that every investor should carefully evaluate. The collapse of several poorly managed lending firms in previous market cycles demonstrated that sustainable risk management and transparency are more important than exceptionally high yields.

As the industry continues to mature in 2026, investors are increasingly prioritizing reputable platforms with strong security infrastructure, transparent reserve systems, and responsible lending practices. Whether using centralized platforms like KuCoin Lending or decentralized lending protocols, users should always conduct thorough research, diversify exposure, and avoid investing more than they can afford to lose.

For investors looking to explore passive income opportunities in crypto while maintaining long-term exposure to digital assets, crypto lending remains one of the most widely adopted strategies in the evolving blockchain ecosystem.

FAQs

Is crypto lending still profitable in 2026?

Yes, crypto lending can still generate passive income in 2026, particularly through stablecoin lending and institutional-grade lending markets. However, returns are generally lower and more sustainable compared to the extremely high yields seen during earlier DeFi cycles.

What cryptocurrencies are commonly used for lending?

Bitcoin (BTC), Ethereum (ETH), USDT, USDC, and other major cryptocurrencies are among the most commonly lent digital assets. Stablecoins are especially popular because they reduce exposure to market volatility.

Is crypto lending safer on centralized or decentralized platforms?

Both centralized and decentralized platforms have different risk profiles. Centralized platforms may provide customer support and integrated risk management systems, while decentralized protocols offer greater transparency through smart contracts. Users should evaluate security, reputation, liquidity, and risk controls before choosing either option.

Can I lose money through crypto lending?

Yes. Crypto lending carries risks including market volatility, borrower liquidation events, platform insolvency, smart contract vulnerabilities, and cybersecurity threats. Investors should always assess risk carefully before participating.

What is the difference between crypto staking and crypto lending?

Crypto staking involves locking supported blockchain assets to help secure a network and earn rewards, while crypto lending involves lending digital assets to borrowers in exchange for interest payments. The two strategies operate differently and carry different risk structures.