KuCoin Ventures Weekly Report: Zcash Trust Crisis & Macro Pressures on Risk Assets

2026/06/09 11:29:00

1. Weekly Market Highlights

A Review of the Zcash "Counterfeiting" Incident: AI Breaches the Privacy Moat—How Capital Reprices "Trust"

Recently, the veteran privacy coin Zcash (ZEC) suffered a sudden plunge, with its price dropping over 30% in a single day. The trigger for this storm was a disclosure by Taylor Hornby, a security researcher at Shielded Labs (an independent support organization within the Zcash ecosystem): Orchard, Zcash's latest generation shielded pool, contained an extremely critical vulnerability. Attackers could generate an unlimited amount of counterfeit ZEC out of thin air without leaving any on-chain traces.

Although the Zcash ecosystem completed soft and hard fork upgrades with extreme efficiency within just a few days to patch the vulnerability, market panic did not subside. In what is being called the most severe black swan event in the privacy sector in recent years, the market sell-off was not merely a panic over a technical bug, but a complete repricing of the most core proposition of crypto assets—the "credibility of the total supply."

This is the most thorny aspect of the incident for the market—the inherent paradox of cryptographic privacy mechanisms.

In conventional public chain security incidents, such as cross-chain bridge hacks or smart contract private key leaks, the stolen amount and fund flows can always be accurately traced on-chain. However, in Zcash's Orchard shielded pool, because transaction amounts and flows are completely hidden, the Zcash community can only plug the future loophole with a code patch; they cannot cryptographically prove whether someone has already exploited the vulnerability to mint counterfeit coins over the "past" four years.

Amidst rampant market rumors, analysis by Dragonfly partner Haseeb pointed straight to the core: the substantive risk of this crisis was physically "isolated" by Zcash's underlying architecture. Haseeb argued that it would be extremely difficult for the counterfeit coins to directly impact the liquidity of mainstream exchanges. This is because Zcash has a cross-pool accounting mechanism called the Turnstile. It strictly records how much transparent ZEC has entered the Orchard shielded pool. If a hacker minted 10 million counterfeit coins in the shielded pool and attempted to transfer them out to a transparent address (for example, planning to transfer them to an exchange's transparent address to cash out), the Turnstile mechanism would directly trigger a circuit breaker and intercept the transaction the moment the outflow exceeded the historical legitimate inflow. Based on this, the Zcash Foundation emphasized that the total supply cap of 21 million ZEC across the network has not been breached.

However, Shielded Labs also admitted that while the Turnstile auditing mechanism protected the broader market, there is currently no technology that can definitively prove whether counterfeit assets have been mixed into the internal Orchard pool.

The market's panic stems exactly from this: the core of the problem is not "how many counterfeit coins have been discovered," but rather that "no one can definitively confirm that counterfeit coins have never appeared." In capital markets, when uncertainty cannot be quantified, the fastest choice is to exit and avoid risk.

Another industry-shocking signal released by this incident is the breakthrough capability demonstrated by Large Language Models in top-tier cryptographic auditing. On May 28, Anthropic had just released Claude Opus 4.8; merely one day later, on May 29, researcher Taylor, with the in-depth assistance of this model, discovered and wrote the exploit for this zero-knowledge proof vulnerability that had been lurking for nearly four years.

It is worth noting that Opus 4.8 is not even a model custom-built for cybersecurity (like the long-rumored, yet-to-be-publicly-tested Mythos Preview), but rather a general-purpose model. This marks a precipitous drop in the cost of discovering high-value, complex cryptographic vulnerabilities due to AI intervention. Although the guidance and judgment of top security experts remain central, the combination of "Human Expert + AI" has already completely reshaped the attack and defense rhythm of Web3 underlying protocols.

Data Source: https://x.com/zodl_co/status/2063262232184795323

Faced with a crisis of trust, another core ZEC development team, ZODL, rolled out the ultimate self-rescue plan: the Ironwood upgrade. The core logic of Ironwood is to directly deprecate the old Orchard shielded pool and establish a new Ironwood pool that has undergone strict formal verification. Funds from the old pool can only enter the new pool unidirectionally through "Turnstile" clearance.

Public information shows that ZODL, founded by former ECC CEO Josh Swihart, completed a seed funding round of over $25 million in March this year, backed by top-tier industry capital consortiums such as Paradigm, a16z crypto, Winklevoss Capital, and Coinbase Ventures. ECC was previously one of the core companies responsible for ZEC's underlying technology development. To break the former governance gridlock, Josh led the core team to leave and found ZODL, which provided ample execution power for handling this crisis.

This Zcash turmoil is an expensive lesson in decentralized security. The incident profoundly demonstrated that core trust in the crypto market does not stem from faith, but from verifiable mathematics and technology. On the other hand, it heralded the arrival of a new era of "AI Attack & Defense" and "Formal Verification," which will pose a massive challenge to underlying projects that have historically relied purely on manual code audits.

2. Weekly Selected Market Signals

Strong Nonfarm Payrolls and Geopolitical Risks Pressure Valuations; Tech Stocks Pull Back from Highs, Crypto Underperforms, ETF Outflows and Stablecoin Contraction Signal a More Defensive Market

Last week, the key variables for global markets were the rising fragility of the U.S.–Iran ceasefire/nuclear negotiation framework and stronger-than-expected U.S. employment data, both of which pushed interest rates and risk premiums higher. U.S.–Iran tensions came under renewed pressure as both sides still lacked a stable consensus on inspections, sanctions relief, and security commitments. Together with the risk of further spillover from the Middle East, markets began to reprice the possibility of energy supply disruptions and renewed inflationary pressure. Meanwhile, U.S. nonfarm payrolls increased by 172,000 in May, well above market expectations, while the unemployment rate remained at 4.3%, indicating continued resilience in the labor market. The combination of geopolitical risk and strong employment data shifted the market narrative from “earnings supporting risk appetite” back to a framework in which inflation, interest rates, and geopolitical risk jointly constrain valuations.

This shift was first reflected in energy and precious metals markets. Driven by Middle East risks, both Brent and WTI crude returned to above USD 90 per barrel. Elevated oil prices mean that energy costs may continue to feed into inflation data, while also limiting the Fed’s room to pivot toward easing. Gold still benefited from some safe-haven demand amid geopolitical uncertainty, but stronger nonfarm payrolls pushed the U.S. dollar and Treasury yields higher, weakening the appeal of non-yielding assets. Spot gold at one point fell nearly 3% last Friday. This shows that the market is not simply trading a safe-haven narrative, but is instead oscillating between “Middle East risks supporting gold and oil” and “higher real rates pressuring gold and risk assets.”

Strong nonfarm payrolls further amplified pressure on asset pricing. The employment data forced markets to reassess the resilience of the U.S. economy and the stickiness of inflation, while reducing the need for the Fed to shift toward easing in the near term. Long-term U.S. Treasury yields moved higher, increasing discount-rate pressure on high-valuation assets. For markets, the central question has shifted from “when will rate cuts begin” to “whether high rates will last longer, and whether there is even a tail risk of renewed rate hikes.” In this environment, technology stocks, crypto assets, and other growth-oriented assets that previously relied on liquidity expectations and elevated valuations all faced renewed repricing pressure.

In equities, U.S. stocks pulled back from elevated levels last week, while Japanese and Korean markets reflected the transmission of the global tech selloff into Asia’s AI supply chain.

At the start of last week, AI and technology stocks still helped keep major U.S. indices near highs. However, after the strong nonfarm payrolls data, markets quickly priced in renewed rate-hike risk and higher long-term yields, with technology and semiconductor stocks becoming the core areas of adjustment. On a weekly basis, the Nasdaq fell around 4.7%, marking one of its weaker weekly performances this year; the S&P 500 declined around 2.6%, ending its previous winning streak; and the Dow was relatively resilient, falling only around 0.3%. This suggests that the U.S. equity pullback was not simply a collapse in risk appetite. Rather, the market began shifting from “AI narratives and earnings expectations” toward testing revenue delivery, margins, returns on capital expenditure, and valuation resilience in a high-rate environment.

South Korea and Japan had both benefited from the semiconductor and AI supply-chain rally, but volatility increased sharply amid a stronger U.S. dollar, foreign outflows, and the correction in U.S. technology stocks. After the U.S. tech pullback last week, pressure on Asia-Pacific markets rose at the start of this week. South Korea’s KOSPI at one point fell more than 8% and triggered a circuit breaker, while Samsung Electronics dropped as much as 10% in early trading. Japan’s Nikkei 225 also fell around 3%–4%. This suggests that the medium- to long-term industrial logic for Japanese and Korean markets has not changed, but when global capital reprices rates and risk premiums, previously strong semiconductor and AI heavyweights can become key targets for profit-taking and liquidity release.

In crypto, BTC fell sharply last week under the combined pressure of macro rate repricing, ETF outflows, and weakening institutional holding signals.

Data Source: TradingView

BTC started last week around USD 73,000, but later fell to around USD 63,000, down roughly 14% for the week. ETH was also weak, retreating to the USD 1,600–1,700 range. Although the Nasdaq 100 also pulled back from elevated levels, reflecting a valuation stress test for AI and technology stocks, BTC and Strategy (formerly MicroStrategy) fell more sharply. This indicates that crypto-market pressure came not only from macro rates and broader risk-asset repricing, but also from deterioration in crypto’s own funding conditions. Continued ETF outflows, stablecoin supply contraction, and Strategy’s rare BTC sale all weakened market confidence in institutional buying and the corporate treasury narrative.

Strategy disclosed that it sold 32 BTC between May 26 and May 31 to pay dividends on its STRC perpetual preferred stock. Although the size of the sale was small relative to its overall holdings, this marked the company’s first disclosed net BTC sale since 2022, breaking the market’s perception of Strategy as a “buy-only” corporate treasury vehicle. It also forced investors to reassess the sustainability of the BTC treasury model under high interest rates, share-price pressure, and rising financing costs. Overall, BTC still has institutional allocation attributes, but during periods of ETF outflows, stablecoin contraction, and cooling corporate treasury narratives, it is more likely to behave as a high-beta risk asset. ETH, meanwhile, has less independent support amid weak ETF flows and a lack of new ecosystem catalysts.

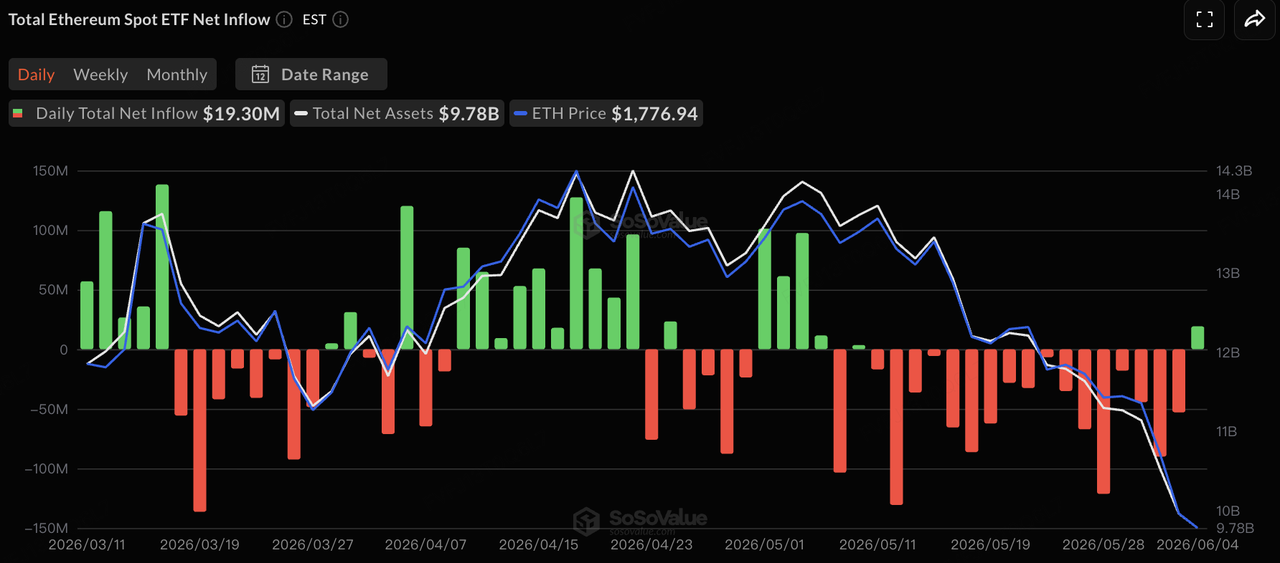

Data Source: SoSoValue

In terms of ETF flows, based on SoSoValue data, U.S. spot BTC and ETH ETFs both experienced prolonged net outflow pressure last week. After 13 consecutive trading days of net outflows totaling around USD 4.4 billion, BTC ETFs recorded a small net inflow of about USD 3.05 million in the second half of the week, temporarily easing the pressure. ETH ETFs recorded around USD 19.3 million of net inflows on June 4, ending 17 consecutive trading days of net outflows. However, single-day positive flows should be viewed more as a temporary easing of selling pressure rather than a trend reversal. On a weekly basis, BTC ETFs still recorded around USD 1.72 billion in net outflows, while ETH ETFs saw around USD 168 million in net outflows. Overall, ETFs remain the core institutional gateway for BTC and ETH, but their marginal role has shifted from “absorbing market selling pressure” to “moving in line with macro rates, risk appetite, and crypto-native funding conditions.” Against a backdrop of higher long-term yields, stablecoin supply contraction, and a cooling Strategy treasury narrative, the support ETFs provide to the crypto market has clearly weakened.

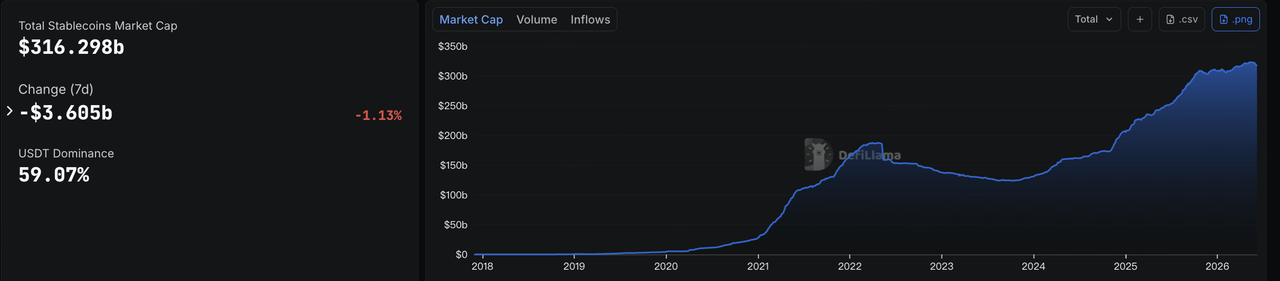

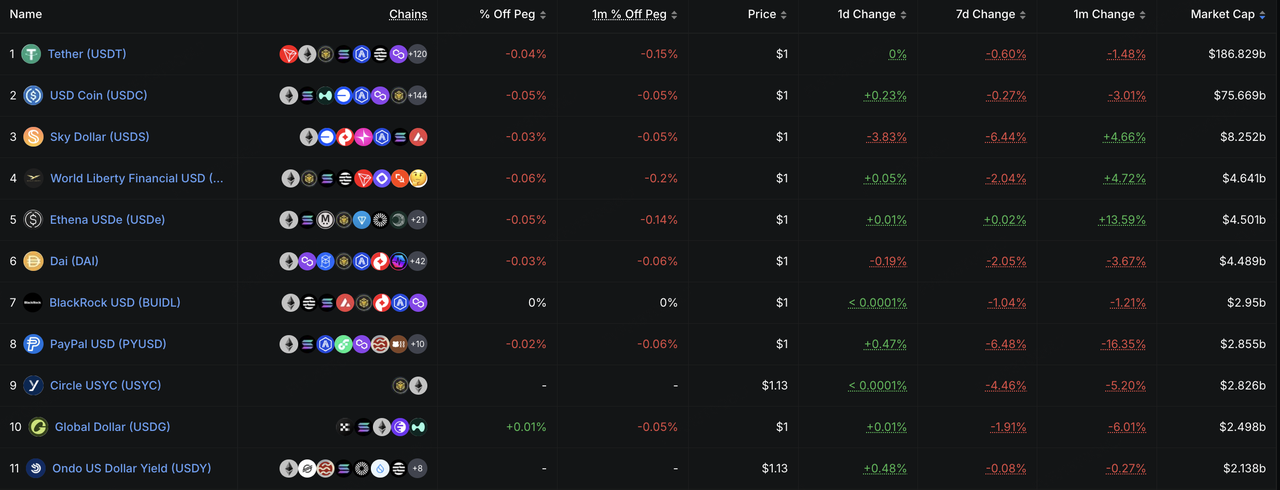

Data Source: DeFiLlama

On stablecoins, DeFiLlama data shows that as of June 8, total stablecoin market capitalization was around USD 316.3 billion, down approximately USD 3.6 billion over seven days, a decline of about 1.13%. USDT’s market share was around 59%. On-chain dollar liquidity continued to contract last week, indicating that the pullback in risk assets, ETF outflows, and lower on-chain trading activity have started to affect the market’s funding base.

Structurally, both USDT and USDC declined slightly, suggesting that the main pools of trading and settlement liquidity did not receive meaningful new inflows. Ecosystem-oriented stablecoins such as USDS, USD1, and PYUSD saw larger declines, reflecting that capital tends to exit non-core stablecoins more quickly during periods of market volatility. USDe was broadly flat over seven days but remained up over the past month, suggesting that the medium-term expansion of yield-bearing stablecoins has not fully reversed, even though short-term minting momentum slowed as risk appetite weakened. BUIDL also declined slightly, reflecting a temporary rebalancing of institutional on-chain cash management capital amid higher rates and increased market volatility. Overall, the stablecoin market has shifted from “total supply expansion with structural divergence” to “total supply contraction with capital moving toward higher-certainty dollar instruments.” On-chain capital has not fully exited, but risk appetite has clearly weakened.

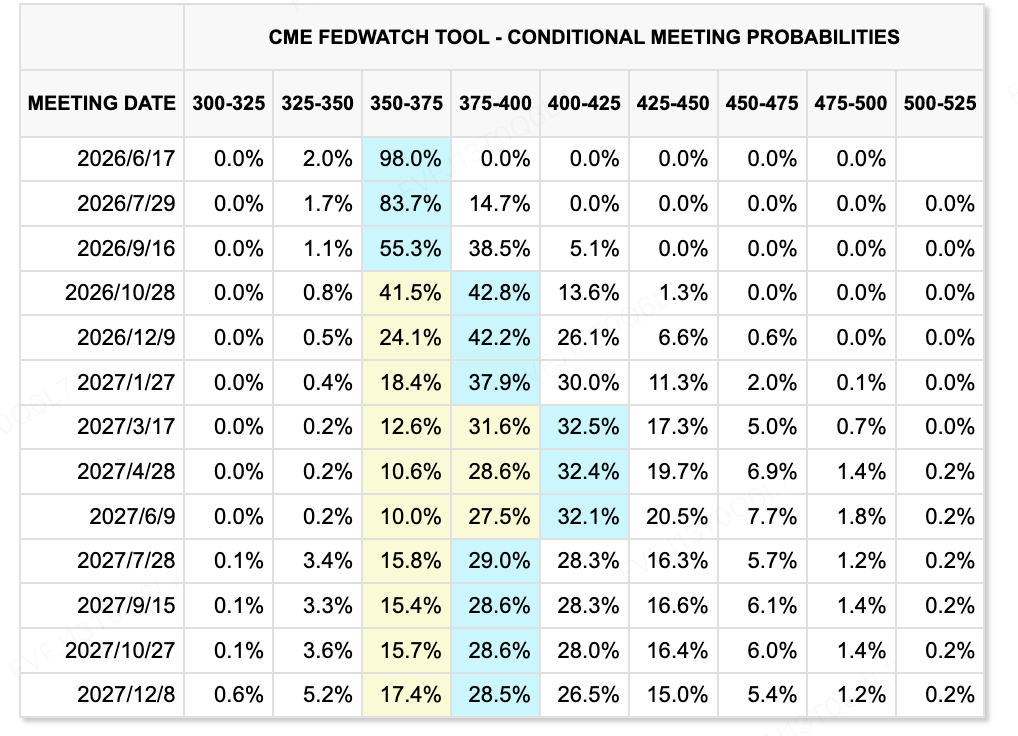

Data Source: CME FedWatch Tool

Key Macro/Financial Events to Watch Next Week

-

U.S. inflation data and Fed repricing: On June 10–11, the U.S. will release May CPI and PPI data. If inflation again comes in above expectations, it will further reinforce the probability of rate hikes later this year and continue to pressure rate-sensitive assets such as technology stocks, crypto assets, and gold.

-

SpaceX IPO and a liquidity test for technology stocks: SpaceX is expected to price its IPO on June 11 and begin trading on June 12. The deal is expected to be massive and could become the largest IPO in global history. It will not only test market appetite for large-scale high-growth technology valuations, but may also create a liquidity-drain effect on secondary markets.

-

Apple WWDC and the AI delivery test: Apple’s WWDC will be an important event for the technology sector. Markets will focus on an upgraded Siri, integration with external large language models, foldable iPhone developments, and on-device AI features. For the AI trade, whether Apple can translate AI functions into real product experiences and a new hardware upgrade cycle will influence market pricing for consumer electronics and edge AI.

-

China, Japan, and South Korea macro data: China will release May trade, CPI, PPI, and financial data, while Japan and South Korea will publish first-quarter GDP data. Markets will focus on the recovery in Chinese domestic demand, export resilience, PPI recovery, and the contribution of semiconductor exports to economic growth in Japan and South Korea.

-

ECB and Bank of Canada rate decisions: The ECB may signal further rate hikes, while the Bank of Canada is widely expected to stay on hold. If the ECB turns more hawkish, global monetary policy divergence will intensify, continuing to support the U.S. dollar and Treasury yields while adding further pressure to risk assets.

Primary Market Observations:

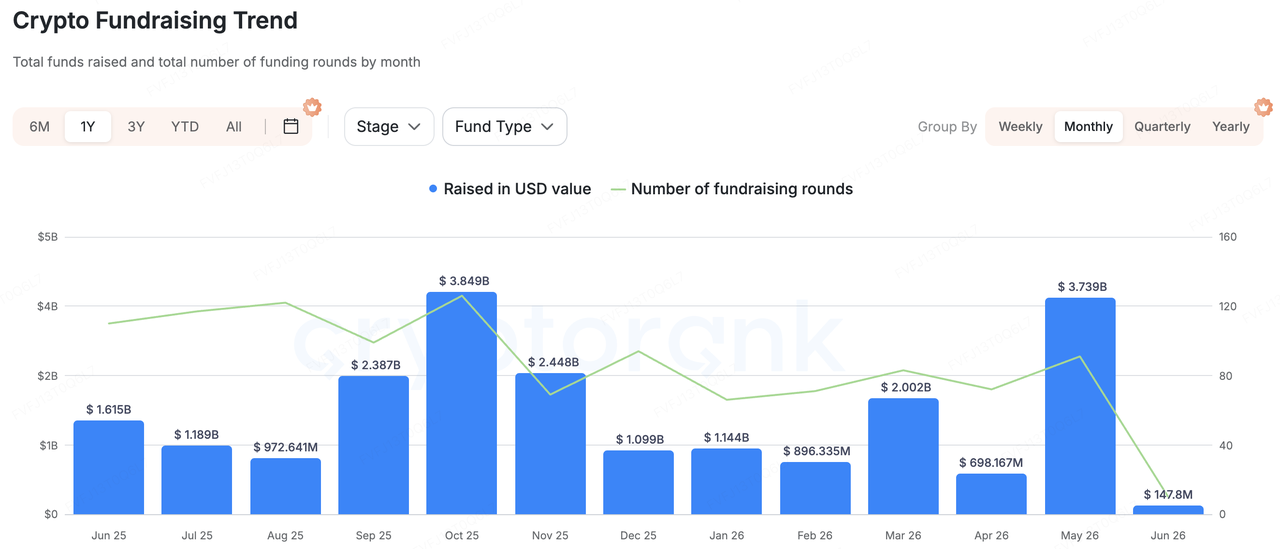

Data Source: CryptoRank

Based on CryptoRank’s broad statistical coverage and publicly available funding databases, crypto primary-market fundraising cooled noticeably last week. Overall, the market showed three key features: lower total funding, reliance on a single large deal, and active M&A consolidation. Compared with earlier weeks driven by large financings and narrative-led projects, capital last week did not clearly chase high-beta themes. Instead, it continued to flow into trading infrastructure, stablecoin payments, prediction-market tools, and institutional data/risk-control services.

Among representative deals, the largest disclosed financing last week was SignalPlus, a digital asset options trading infrastructure provider, which completed a USD 50 million Series B round. Investors included HashKey Capital, BlockBooster, and AppWorks. SignalPlus serves professional traders and institutional users with options trading tools, risk management, automated order execution, and multi-exchange connectivity. This financing shows that amid increased secondary-market volatility and rising demand for options and derivatives, institutional-grade trading tools and risk management infrastructure remain attractive to investors.

Stablecoin payments remained another key focus for primary-market capital. WasabiCard completed a USD 10 million Series A round. The project is positioned as Web3 financial infrastructure connecting stablecoins with traditional payments, offering virtual and physical crypto payment cards, cross-border remittance, settlement, and white-label card-issuing APIs. The investment logic behind this category is that stablecoins are moving beyond trading settlement into payments, remittances, corporate on/off-ramps, and merchant acquiring. Primary-market investors are still searching for payment gateways capable of capturing real-world demand for on-chain dollars.

Prediction markets and real-time trading infrastructure also deserve attention. Speed Labs completed a USD 6.5 million seed round, positioning itself as real-time prediction-market infrastructure for sports betting platforms, prediction markets, and crypto-native wagering applications. K25.ai raised USD 4 million and is positioned as a prediction-market platform combining AI, livestreaming, and blockchain. This indicates that the prediction-market narrative remains active, but capital is increasingly favoring infrastructure and embeddable use cases rather than standalone front-end trading applications.

In addition, M&A activity remained active last week, reflecting a shift toward consolidation within the industry. Cosmos Labs acquired Mintscan, strengthening Cosmos ecosystem data browsing and on-chain analytics capabilities. Kaiko acquired Amberdata, reflecting continued consolidation in institutional digital asset data. WTW acquired Redefind, showing that crypto insurance and custody-related risk protection are being incorporated into the strategies of traditional insurance and risk-management institutions. Keyrock’s acquisition of BlockFills should help expand its institutional trading, OTC, and liquidity services. Overall, against a backdrop of macro-rate pressure and ETF outflows in secondary markets, primary-market capital is leaning more toward infrastructure projects that can monetize, serve institutions, and support real business use cases.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.