DTCC to Launch Tokenized Real-World Assets Trading in July 2026: Equities, ETFs & U.S. Treasuries Go On-Chain

2026/05/05 16:18:02

Introduction

What happens when the backbone of American capital markets — an institution that custodies $114 trillion in assets and processes $4.7 quadrillion in securities transactions annually — decides to put real-world assets on a blockchain? Based on DTCC's May 2026 announcement, that future is arriving faster than most market participants expected.

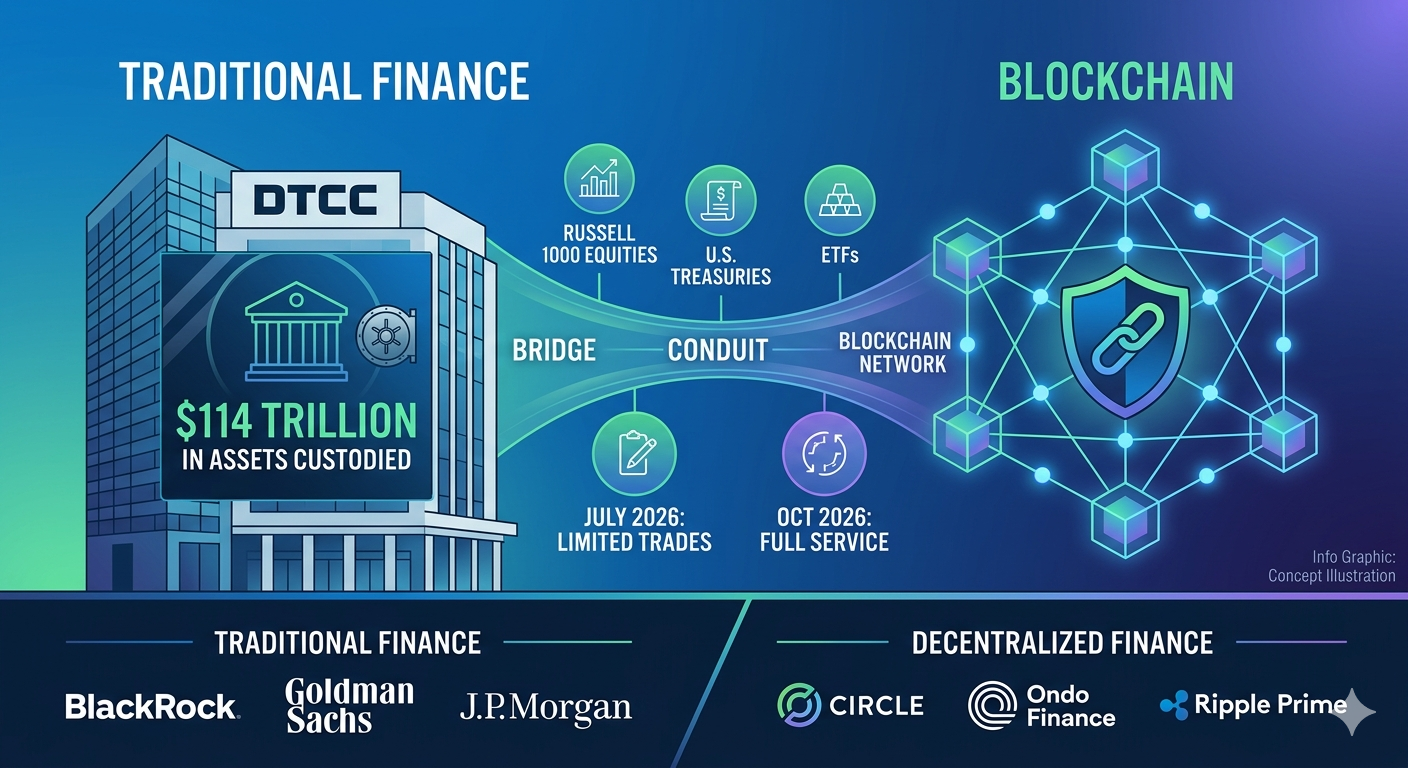

DTCC announced on May 4, 2026 that it will begin limited production trades of tokenized real-world assets in July 2026, with a full service launch in October 2026. The initiative brings together more than 50 firms spanning traditional finance and decentralized finance — including BlackRock, Goldman Sachs, J.P. Morgan, Circle, Ondo Finance, and Ripple Prime — to prove that tokenized securities can operate at systemic scale without sacrificing investor protections.

What Is DTCC's Tokenization Service and When Will It Launch?

DTCC's tokenization service will go live in two phases — limited production trades in July 2026 and a full service launch in October 2026 — bringing tokenized representations of real-world securities into the same infrastructure that underpins U.S. capital markets today. The service is built on DTCC's ComposerX platform suite and targets assets already held in DTC custody, meaning the institution is not creating a parallel market but rather digitizing the securities that already flow through its pipes.

The Two-Phase Rollout Timeline

The July 2026 launch marks the beginning of limited production trades of tokenized real-world assets. In this context, "limited" means DTCC will test operational and technical workflows in a production environment using real data and real assets, not simulated scenarios. The Industry Working Group — comprising more than 50 firms — will collaborate with DTCC to prove interoperability across multiple blockchains and validate that tokenized entitlements can move securely between whitelisted wallets.

The October 2026 full service launch represents the transition from pilot testing to operational readiness. By that date, DTC Participants will be able to elect tokenized record-keeping for eligible securities as a standard service option. DTCC has emphasized that the preliminary base version launching in July and expanding in October is intentionally scoped, with additional functionality planned for future releases following further consultation with SEC staff.

DTCC built the service on its ComposerX platform suite, which provides the technology backbone for distributed ledger integration into existing post-trade infrastructure. ComposerX enables DTC to layer blockchain functionality onto its centralized book-entry systems without requiring market participants to abandon their current operational workflows.

Why DTCC's Infrastructure Position Matters

DTC currently custodies assets valued at over $114 trillion, according to DTCC's May 2026 announcement. The institution processes approximately $4.7 quadrillion in securities transactions yearly. These figures illustrate why DTCC's entry into tokenization differs fundamentally from smaller issuer-level tokenization services: DTCC operates at the core post-trade infrastructure level, where the majority of U.S. equity and fixed-income ownership records already reside.

Unlike tokenization platforms that work with individual issuers to create new digital securities, DTCC is creating digital representations of securities that already exist in its custody. This distinction is critical because existing legal frameworks, investor protections, and settlement relationships remain intact.

Brian Steele, DTCC Managing Director and President of Clearing & Securities Services, stated in the May 2026 announcement: "DTC's tokenization service is designed to provide systemic scale where deep liquidity already lives." This quote captures the strategic rationale — DTCC is not trying to build liquidity from scratch but rather to unlock the liquidity that already sits within its infrastructure by adding programmable, on-chain transfer capabilities.

Which Real-World Assets Will DTCC Tokenize First?

DTCC will initially tokenize a defined set of highly liquid assets including Russell 1000 constituents, ETFs tracking major indices, and U.S. Treasury bills, bonds, and notes — all backed by the same entitlements, investor protections, and ownership rights as their traditional counterparts. The asset selection reflects DTCC's conservative approach: start with the most liquid, most widely held, and most systematically important securities before considering expansion.

Tokenized Equities and ETFs

The Russell 1000 constituents — the 1,000 largest publicly traded U.S. companies by market capitalization — will be among the first equities available in tokenized form. These stocks represent the core large-cap universe that institutional investors trade daily, and their inclusion ensures that the tokenization service addresses meaningful trading volume from day one.

ETFs tracking major U.S. equity indices will also be included in the initial asset set. ETFs are particularly well-suited to tokenization because they are already structured as pooled vehicles with standardized creation and redemption processes. Tokenized ETFs could enable more efficient primary market operations and faster creation unit settlements.

All tokenized assets provide "the same entitlements, investor protections and ownership rights" as assets held in traditional form, based on DTCC's service description. These protections are supported by DTC's existing resilience frameworks, including its status as a covered clearing agency under SEC oversight and its compliance with Regulation SCI for systems integrity.

U.S. Treasury Securities on Blockchain

U.S. Treasury bills, bonds, and notes are included in the initial tokenization scope. The inclusion of Treasuries is especially significant given the explosive growth in tokenized government debt markets. According to RWA.xyz data cited in May 2026 reports, tokenized stocks grew from $375.4 million in May 2025 to approximately $1.21 billion in May 2026, demonstrating rapid institutional appetite for on-chain exposure to traditional assets.

Ondo Finance, a participant in DTCC's Industry Working Group, operates USDY — a roughly $2 billion yield product backed by short-term Treasuries. DTC-tokenized Treasuries could provide on-chain verifiable collateral for products like USDY, potentially reducing counterparty risk and improving transparency in the tokenized Treasury supply chain.

How Does the DTC Tokenization Service Work?

DTC's tokenization service creates digital representations — called tokenized entitlements — of existing securities already held in DTC custody, allowing these entitlements to move between registered wallets on approved blockchains without altering the underlying legal ownership structure or investor protections. The service does not create new securities or change the legal characterization of existing holdings. Instead, it provides an alternative technology layer for recording and transferring ownership records.

Tokenized Entitlements vs. Traditional Book-Entry

The underlying assets stay in DTC custody at all times. Securities remain registered in the name of Cede & Co., DTC's nominee entity, just as they are today. The indirect holding model and legal characterization under UCC Article 8 are preserved exactly as they exist in the traditional book-entry system.

The tokens themselves are NOT the securities and are NOT security entitlements under federal securities law. They serve as an alternative method for instructing DTC to record and transfer security entitlements on DTC's official books. When a DTC Participant moves tokenized entitlements between wallets, the blockchain transaction functions as an instruction to DTC to update its centralized records accordingly.

DTC Participants can elect to have security entitlements recorded using distributed ledger technology rather than exclusively through DTC's centralized book-entry ledger. This opt-in model ensures that no firm is forced to adopt blockchain-based record-keeping until it is operationally and technologically prepared to do so.

Approved Blockchains and Security Controls

Only DTC Participants — primarily broker-dealers and certain banking entities — can register wallets with DTC. The preliminary base version restricts transfers to registered (whitelisted) wallet addresses only. No transfers to non-whitelisted wallets are permitted, eliminating the risk of unauthorized or anonymous transfers.

All wallets are screened for OFAC compliance before activation and are subject to ongoing sanctions monitoring. DTC maintains override keys for security purposes, ensuring that the institution can intervene if necessary to prevent unauthorized transactions.

The preliminary base version does not include collateral or settlement value. It is designed as a record-keeping and transfer infrastructure layer, with settlement and collateral functionality planned for future releases. DTCC has committed to using only approved technology and resilient infrastructure that meets its standards as a systemically important financial market utility.

What Market Benefits Will Tokenized Securities Deliver?

Tokenized securities are expected to deliver faster settlement cycles, reduced counterparty risk, 24/7 market access, programmable asset functionality through smart contracts, and new liquidity pools — all while maintaining the same investor protections as traditional securities. These benefits accrue across market participants from institutional traders to retail investors, though the near-term impact will be most visible in institutional workflows.

Faster Settlement and Capital Efficiency

The current U.S. standard is T+1 settlement for most equity transactions. Tokenization enables potential T+0 (instant) settlement because blockchain-based transfers can settle in minutes rather than waiting for end-of-day batch processing. This acceleration matters because faster settlement reduces the window during which counterparty default can leave trades unsettled.

Collateral mobility across jurisdictions and time zones becomes possible without regard to standard trading hours. A bank in Singapore could move tokenized Treasury collateral to a U.S. affiliate outside U.S. market hours, improving capital deployment efficiency. Banks and broker-dealers could reduce capital buffers held against settlement risk, potentially freeing billions in regulatory capital.

Just-in-time account funding becomes possible when transfers settle instantly rather than overnight. Reduced counterparty risk benefits the entire market by lowering systemic exposure to default cascades during periods of market stress.

Programmability and New Market Access

Smart contract-enabled functionality allows for programmable transfers and allocations. For example, dividend reinvestment programs could execute automatically upon dividend distribution, or corporate action responses could be pre-programmed based on holder preferences. These automations reduce manual processing and operational risk.

Potential for 24/7 trading outside standard market hours opens new trading modalities. While the initial DTCC service does not itself constitute a trading venue, the underlying tokenized entitlements could support round-the-clock trading on approved platforms. Decentralization enables market participants to access assets more directly, moving peer-to-peer between whitelisted participants while maintaining DTC's record-keeping integrity. Nadine Chakar, DTCC Managing Director and Global Head of Digital Assets, stated in the May 2026 announcement: "Tokenization is an important and critical step toward building tomorrow's digital infrastructure. DTCC is committed to remaining at the forefront of innovation and championing a scalable, interoperable and risk-managed Web3 ecosystem that harnesses the power of digital ledger technology and delivers real value to the industry." Both NYSE and Nasdaq have announced plans for tokenized trading support, suggesting that trading infrastructure will evolve alongside DTCC's post-trade tokenization capabilities.

How to Trade Tokenized Real-World Assets on KuCoin

KuCoin offers users exposure to the RWA tokenization trend through trading of crypto tokens backed by real-world assets and native RWA projects, positioning traders at the intersection of traditional finance and blockchain innovation. As DTCC's tokenization service bridges TradFi and DeFi, crypto platforms like KuCoin provide early access to RWA-related tokens and projects that stand to benefit from the mainstream adoption of on-chain assets.

Users can create a KuCoin account to explore RWA tokens, track tokenization developments, and access trading pairs linked to real-world asset trends. The platform lists tokens from projects building tokenized infrastructure for equities, fixed income, and alternative assets — giving traders a front-row seat to the convergence of Wall Street and blockchain technology. Whether you are looking to diversify into RWA-backed tokens or monitor how traditional asset tokenization impacts crypto markets, KuCoin provides the tools and liquidity to participate in this structural shift.

New users can now register at KuCoin and Get Up to 11,000 USDT in New User Rewards.

Conclusion

DTCC's July and October 2026 timeline marks a historic institutional adoption of blockchain technology in financial markets. The initiative brings together a 50-firm Industry Working Group spanning BlackRock and Goldman Sachs on the traditional side with Circle, Ondo Finance, and Ripple Prime on the crypto-native side — demonstrating that the wall between TradFi and DeFi is dissolving at the infrastructure level.

The SEC's December 2025 no-action letter provides a three-year regulatory framework that gives participants confidence to build and deploy. The initial asset coverage — Russell 1000 equities, major ETFs, and U.S. Treasuries — represents the most liquid and systemically important segments of U.S. capital markets. Core benefits including enhanced liquidity, greater transparency, and operational efficiency will be delivered while preserving the investor protections that have underpinned DTC custody for decades.

This is not a speculative experiment. It is a structural upgrade to the pipes that move $4.7 quadrillion in transactions each year. As tokenized entitlements begin flowing through DTCC's ComposerX infrastructure starting July 2026, the market will witness the first phase of a multi-year transformation in how securities are recorded, transferred, and settled. The blockchain is not replacing Wall Street — it is becoming part of it.

FAQs

What is the difference between DTCC tokenized assets and crypto tokens like stablecoins?

DTCC tokenized assets are digital representations of existing securities that remain in DTC custody with identical legal protections and ownership rights, whereas stablecoins are standalone digital assets typically backed by cash or cash equivalents. DTCC tokens derive their value directly from underlying securities held in traditional custody and serve as an alternative record-keeping method rather than new instruments. Stablecoins function as payment tokens or store-of-value instruments, while DTCC tokenized entitlements are infrastructure tools for moving ownership records of securities that already exist.

Can individual investors directly hold DTCC tokenized securities in personal wallets?

In the initial phase, only DTC Participants — primarily SEC-registered broker-dealers and certain banking entities — can register whitelisted wallets. Individual investor access depends on future arrangements between broker-dealers and their customers. DTC views the wallet holder as the entitlement holder, so retail access will be determined by how participating firms structure their client services. A retail investor's broker-dealer may offer tokenized security access through the broker's own wallet infrastructure, but personal self-custody wallets outside the DTC-participant ecosystem are not supported.

Which blockchains will DTCC use for tokenized securities?

DTCC has not publicly disclosed the complete list of approved blockchains, but the SEC no-action letter authorizes tokenization on both public and private-permissioned blockchains that meet DTC's technology and security requirements. The Industry Working Group is testing interoperability across multiple chains, suggesting a multi-chain approach rather than reliance on a single network. DTC's security standards — including whitelisted wallets, OFAC screening, and override key capabilities — will apply regardless of which underlying blockchain technology is used.

How does DTCC tokenization differ from tokenized stocks offered by crypto platforms?

DTCC tokenized securities carry full ownership rights and DTC custody protections because the underlying assets never leave DTC's infrastructure. Some existing crypto platform offerings, such as xStocks or Ondo Global Markets, are structured as loans backed by stocks rather than direct ownership representations. DTCC's model preserves the indirect holding model and UCC Article 8 characterization unchanged. Investors in DTCC-tokenized securities receive the same dividends, voting rights, and bankruptcy protections as holders of traditional book-entry shares.

What risks should investors consider with tokenized securities?

Key risks include technology risks from blockchain infrastructure, including potential smart contract vulnerabilities or network downtime. Limited initial asset coverage is restricted to Russell 1000 constituents and select ETFs, so diversification benefits are constrained during the pilot phase. Wallet transferability is limited to registered addresses, which may reduce liquidity compared to fully open token markets. Uncertainty exists around the three-year pilot program's post-pilot regulatory path — the SEC no-action letter expires after three years, and permanent regulatory frameworks are not yet established. Unproven secondary market liquidity for tokenized versions at the scale DTCC operates remains a consideration, as the service launches without integrated collateral or settlement value functionality in its preliminary base version.