How to Buy USDC (USD Coin) in 2026: A Complete Step-by-Step Guide

2026/03/27 16:39:02

The landscape of digital finance has shifted dramatically. If 2021 was the year of speculative frenzy and 2024 was the year of Institutional Bitcoin, 2026 is undoubtedly the year of the Regulated Digital Dollar. At the heart of this transformation is USDC (USD Coin), a stablecoin that has evolved from a simple trading tool into a foundational layer of the global financial system.

Managed by Circle Internet Financial, USDC is no longer just a "crypto asset." Following the landmark legislative breakthroughs of 2025, it is now widely recognized as a "qualified stablecoin," backed 1:1 by highly liquid US reserves and subject to stringent federal oversight. Whether you are a business owner looking to settle cross-border invoices instantly, a saver seeking refuge from local currency volatility, or a participant in the now-mature Decentralized Finance (DeFi) ecosystem, knowing how to buy USDC safely and efficiently is a critical financial skill.

This guide provides a comprehensive roadmap for navigating the USDC ecosystem in 2026. We will cover the infrastructure, the regulatory safeguards, and the exact steps required to convert your fiat currency into the world's most transparent digital dollar.

Key Takeaways

Before we dive into the technical details, here are the essential points to remember for buying USDC in 2026:

-

Regulatory Compliance: USDC is now fully compliant with the US Stablecoin Act and Europe’s MiCA (Markets in Crypto-Assets) regulation, making it one of the safest digital assets to hold.

-

Multi-Chain Accessibility: You can purchase USDC on dozens of blockchains, but in 2026, Layer 2 networks like Base and Arbitrum, along with high-speed chains like Solana, offer the lowest fees.

-

Verification is Mandatory: Due to 2026 "Travel Rule" updates, almost all entry points for buying USDC require robust Identity Verification (KYC).

-

Instant Funding: New payment rails like FedNow in the US and expanded SEPA Instant in Europe allow for near-instant fiat-to-USDC conversions.

-

Storage Matters: While exchange security has improved, self-custody via hardware wallets remains the gold standard for large holdings.

What is USDC? Why Buy It in 2026?

To understand why you should buy USDC, you must first understand what it represents in the current financial climate. USDC is a digital stablecoin pegged to the United States Dollar. For every one USDC token in circulation, a corresponding dollar (or dollar-denominated asset like short-term US Treasuries) is held in custody by regulated financial institutions.

In 2026, the "Why" has shifted from speculation to utility. First, programmability has become a mainstream requirement. Unlike traditional bank deposits, USDC can be integrated into "smart contracts," allowing for automated payments, escrow services, and real-time streaming of salaries. If you are working in the gig economy or running a global startup, USDC allows you to bypass the 3-5 day delay of the legacy SWIFT banking system.

Furthermore, the yield environment has stabilized. In 2026, on-chain credit markets allow USDC holders to earn "real world yield" by lending their stablecoins to verified businesses or participating in tokenized Treasury bill funds. This offers a transparent alternative to traditional savings accounts, often with superior liquidity. Finally, USDC serves as a crucial hedge. For users in emerging markets facing high inflation, holding a digital dollar that can be moved or traded 24/7 provides a level of financial sovereignty that was previously inaccessible.

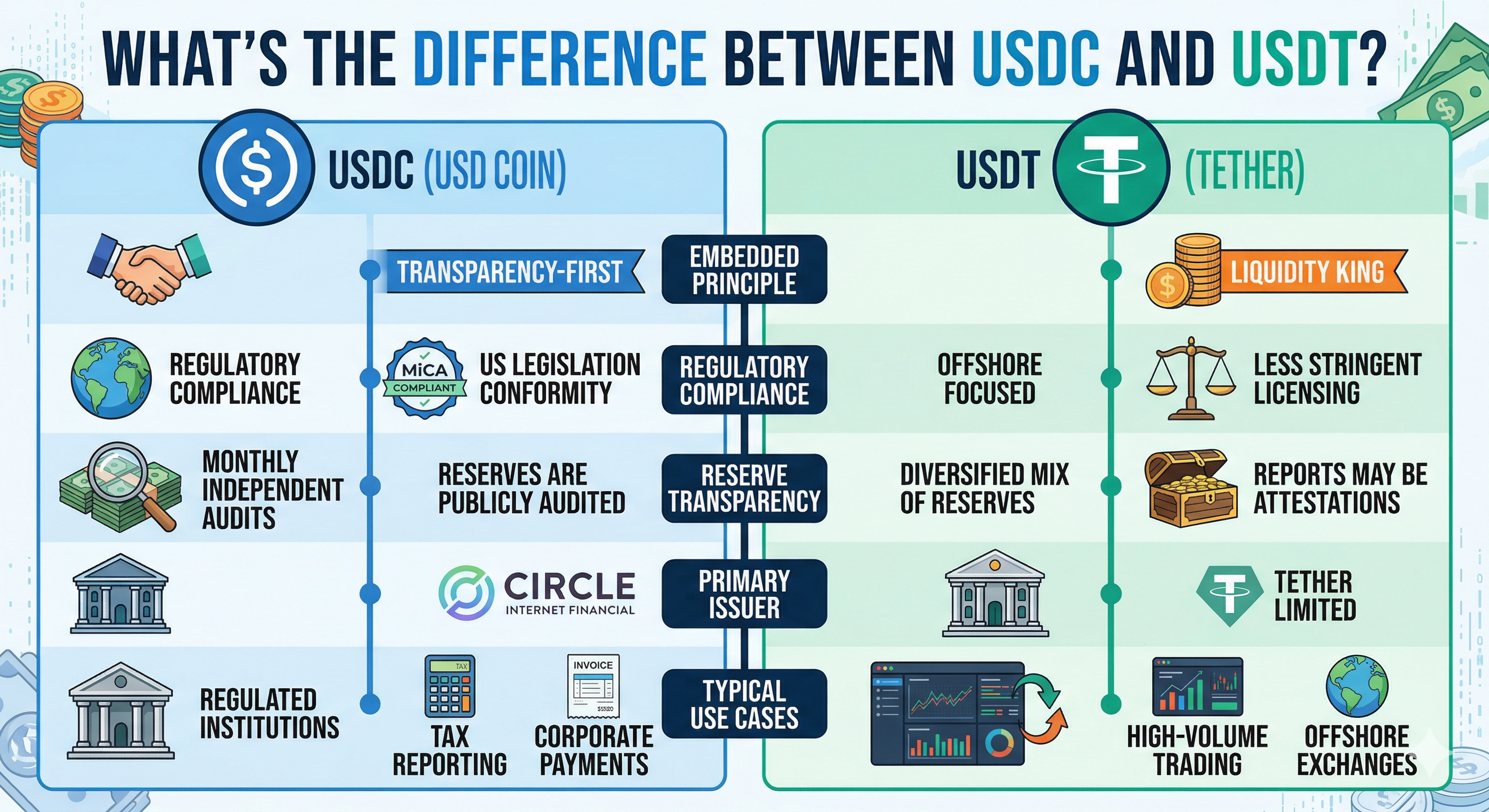

What's the Difference Between USDC and USDT?

As a buyer, you will inevitably encounter the two giants of the stablecoin world: USDC and its primary competitor, Tether (USDT). While both aim to maintain a $1.00 peg, their philosophies and regulatory standings in 2026 differ significantly.

USDC: The Compliance-First Model USDC is built on a foundation of transparency. Its reserves are audited monthly by top-tier accounting firms, and these reports are a matter of public record. In 2026, USDC is often the preferred choice for Western institutions, publicly traded companies, and regulated fintech apps. If you are operating in a jurisdiction with strict crypto laws, such as the US or the EU, USDC is frequently the only stablecoin allowed for direct fiat-to-crypto on-ramping due to its adherence to the latest stablecoin laws.

USDT: The Liquidity King Tether (USDT) remains the most traded cryptocurrency in the world by volume. It is the lifeblood of offshore exchanges and is deeply integrated into the Asian and Latin American markets. However, its reserve composition remains more diverse—including corporate bonds and other assets—which some conservative users find less appealing. In 2026, USDT is excellent for high-volume trading on international platforms, but USDC is generally considered the safer "parking spot" for long-term capital and formal business transactions.

Choosing between them often comes down to your location and your goal. If you want maximum ease of use with a US bank account or need to comply with corporate tax reporting, USDC is the clear winner. If you are trading high-frequency pairs on a non-US exchange, you might find yourself using USDT out of necessity.

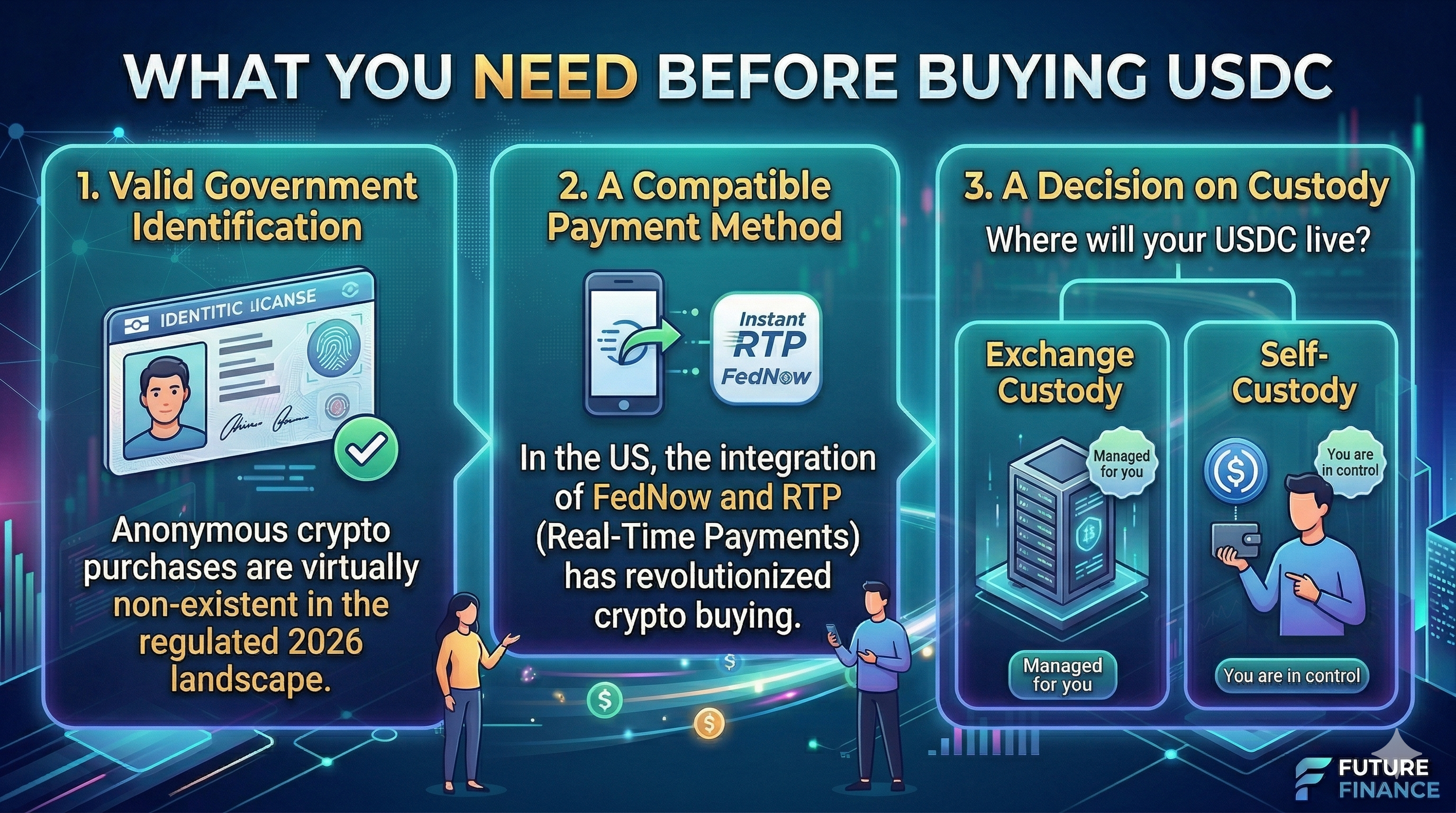

What You Need Before Buying USDC?

The process of buying crypto has become much more streamlined by 2026, but it still requires a few "pre-flight" checks to ensure your transaction is secure and legal.

-

Valid Government Identification Anonymous crypto purchases are virtually non-existent in the regulated 2026 landscape. You will need a valid passport, driver’s license, or national ID card. Modern exchanges use automated "Liveness Checks" (biometric facial scanning) to verify your identity within minutes. Ensure your documents are not expired, as the updated 2026 verification systems are extremely sensitive to document metadata.

-

A Compatible Payment Method In the US, the integration of FedNow and RTP (Real-Time Payments) has revolutionized crypto buying. You can now link your bank account for instant transfers that settle in seconds rather than days. In Europe, SEPA Instant remains the standard. While credit cards are an option, they often carry high "cash advance" fees from the card issuer, making bank transfers or digital wallets (like Apple Pay or Google Pay) the more economical choice in 2026.

-

A Decision on Custody Where will your USDC live? You have two primary options:

-

Exchange Custody: You leave your USDC on the platform where you bought it (e.g., Coinbase). This is convenient for beginners and allows you to use the exchange’s security features like vault delays and white-listed addresses. In the context of choosing a high-performance platform to execute your USDC strategy in 2026, KuCoin has emerged as a particularly strong contender for users who prioritize deep liquidity and advanced trading features.

-

Self-Custody: You move your USDC to a private wallet (e.g., a Ledger hardware wallet or a software wallet like MetaMask). This gives you total control but places the responsibility of security entirely on your shoulders. In 2026, "Smart Contract Wallets" have become popular, offering social recovery features that make self-custody much less intimidating for non-technical users.

How to Buy USDC Step-by-Step in 2026

Once you have your ID and funding ready, follow these steps to complete your purchase. This workflow reflects the standardized process across major 2026 platforms.

Step 1: Choose Your Platform

For the majority of users, a Centralized Exchange (CEX) is the most efficient entry point. In 2026, the market has consolidated into a few highly regulated winners. Coinbase remains the dominant player for USDC due to its partnership in the Centre Consortium. Kraken is preferred for its deep liquidity and professional trading tools, while Binance (under its new global compliance framework) offers the widest range of blockchain network options.

Step 2: Account Registration and Security

Sign up using a secure email address. Immediately after registering, you must enable Two-Factor Authentication (2FA). In 2026, we strongly advise against SMS-based 2FA due to the prevalence of SIM-swapping attacks. Instead, use a hardware security key (like a YubiKey) or an authenticator app (like Authy or Google Authenticator). Many 2026 platforms now mandate passkeys for login, which use your device's biometrics for a passwordless, highly secure experience.

Step 3: Completing the KYC Process

Navigate to the "Verify Identity" section. You will be asked to upload photos of your ID and perform a quick facial scan. Most 2026 platforms process this in real-time. Once verified, you will be granted "Fiat-to-Crypto" limits, which typically start at $5,000 to $10,000 per day for new accounts.

Step 4: Funding Your Wallet

Navigate to the "Deposit" or "Add Funds" section. Link your bank account via a secure provider like Plaid or use your local instant payment rail. In 2026, most major exchanges offer "Zero-Fee Transfers" for USDC if you use a direct bank link, as they want to encourage users to hold the stablecoin within their ecosystem.

Step 5: Executing the Purchase

Go to the "Trade" or "Buy/Sell" tab and select USDC. You will see two main options:

-

Market Order: You buy USDC instantly at the current rate (usually $1.00 plus a small spread).

-

Limit Order: You set a specific price. While USDC is a stablecoin, you might set a limit order for $0.9995 to ensure you aren't paying a premium during times of high market volatility.

Step 6: Selecting the Outbound Network

This is where many beginners make mistakes. USDC exists on many different blockchains. If you intend to withdraw your USDC to a personal wallet, you must select the correct network. In 2026, Ethereum (ERC-20) is the most secure but often carries fees of $5–$20. Solana (SPL), Base, and Polygon are significantly cheaper, often costing less than $0.05 per transaction. Always ensure your receiving wallet supports the network you select on the exchange.

USDC Price Analysis: Stability and De-pegging Risks

A common question from new buyers is: "Why does the price of USDC change if it’s supposed to be $1?"

In a perfect world, USDC is always exactly $1.00. However, on crypto exchanges, the price is determined by supply and demand. If a massive amount of people try to sell USDC for Bitcoin at the same time, the price might "wobble" to $0.999. Conversely, in 2026, during periods of extreme market fear, USDC often trades at a slight premium (e.g., $1.002) as investors rush out of volatile coins and into the safety of the digital dollar.

It is also important to discuss De-pegging. Historically, USDC saw a significant de-peg in early 2023 due to the failure of Silicon Valley Bank, where a portion of its reserves were held. The peg was quickly restored once the US government guaranteed deposits. Since then, Circle has diversified its reserves across various systemic banks and primarily into the BlackRock-managed Circle Reserve Fund, which consists mostly of short-term US Treasuries. In 2026, the risk of a permanent de-peg is considered extremely low by financial analysts, provided the US government continues to honor its sovereign debt. When you buy USDC, you are essentially betting on the stability of the US financial system, delivered via a digital medium.

The Future of USDC: What to Expect by 2030

Looking ahead, the role of USDC is expected to expand far beyond the "crypto" niche. By 2030, analysts predict several key milestones for this asset class.

Integration with Central Bank Digital Currencies (CBDCs) Rather than competing with a "Digital Dollar" issued by the Fed, USDC is likely to act as the private-sector bridge. We expect to see "Hybrid Stablecoin" models where the government provides the regulatory framework and the private sector (Circle/USDC) provides the innovative technology and user interface.

The "Invisible" Stablecoin By 2030, you may be using USDC without even knowing it. When you send money from a US-based app to a relative in the Philippines, the backend of the transaction will likely involve converting USD to USDC, sending it over a high-speed blockchain like Solana or Base, and converting it to Philippine Pesos on the other end. The cost will be pennies, and the time will be seconds.

Standardized Institutional Use We are already seeing the beginning of this in 2026, with major payroll providers offering "Pay in USDC" options. By 2030, it is highly probable that B2B trade finance—the $20 trillion industry that moves goods across oceans—will settle using USDC smart contracts to eliminate the risk of payment delays and currency fluctuations. For the individual buyer today, acquiring USDC is not just a trade; it is an early adoption of the future plumbing of global finance.

Conclusion

Buying USDC in 2026 is a straightforward process that reflects how far the industry has come in terms of regulation and user experience. By following the structured approach of choosing a compliant exchange, verifying your identity, and selecting the most efficient blockchain network, you can secure your digital dollars with minimal risk and cost.

As we move toward a more digitized global economy, the distinction between "crypto" and "traditional finance" will continue to blur. USDC stands at the center of this convergence. Whether you are using it for trading, saving, or transacting, you are participating in a system that offers more transparency and speed than any legacy bank can currently provide. Always remember to prioritize security, keep your private keys safe, and stay informed about the evolving regulatory landscape.

FAQs

Is my USDC insured by the FDIC?

Generally, no. USDC is not a bank deposit; it is a digital asset. While the reserves backing USDC are often held in FDIC-insured banks or in US Treasuries, the token itself does not carry individual FDIC insurance. However, under 2025 regulations, qualified stablecoin issuers must adhere to strict capital requirements to protect users.

Can I buy USDC without a bank account?

In 2026, it is difficult but possible. You can use Bitcoin ATMs that support USDC or P2P (Peer-to-Peer) marketplaces, but these methods often carry significantly higher fees (5%–10%) and still require some form of ID verification due to global Anti-Money Laundering (AML) laws.

How do I convert USDC back into cash in my bank account?

The process is simply the "How to Buy" steps in reverse. You send your USDC to a regulated exchange, sell it for your local fiat currency (USD, EUR, GBP), and then withdraw that balance to your linked bank account via FedNow, ACH, or SEPA.

What is the "gas fee" when sending USDC?

Whenever you move USDC from your private wallet, you must pay a fee to the blockchain network to process the transaction. This is called a gas fee. In 2026, many wallets offer "gasless transactions" by allowing you to pay the fee in USDC itself rather than the network's native token (like ETH or SOL).

Is USDC legal in all countries?

While USDC is legal in most major economies, some countries with strict capital controls or blanket crypto bans (such as China) may restrict its use. Always check your local regulations before making a significant purchase.