KuCoin Ventures Weekly Report: Rate-Hike Re-Pricing and Institutional Expansion: Japanese Financial Groups Double Down on On-Chain Asset Management

2026/07/14 11:15:00

1. Weekly Market Highlights

TradFi On-Chain Infrastructure Enters a New Phase: Robinhood and Swift Move into the Trading Front End and Payment Back End

Last week, traditional financial institutions’ active move into blockchain infrastructure became a key market focus. Following the launch of Robinhood Chain, its long-term positioning remains centered on supporting tokenized stocks, RWA settlement, and on-chain finance. However, early on-chain activity was driven more by meme trading, DEX volume, and stablecoin liquidity accumulation. At the same time, Swift announced that its blockchain-based shared ledger is ready for initial use, with 17 international banks from six continents set to participate in a tokenized deposits pilot. The two developments represent entry points from the retail trading front end and the banking payment back end, respectively, and together suggest that tokenization is moving beyond isolated product experiments into the infrastructure layer for trading, payments, and settlement.

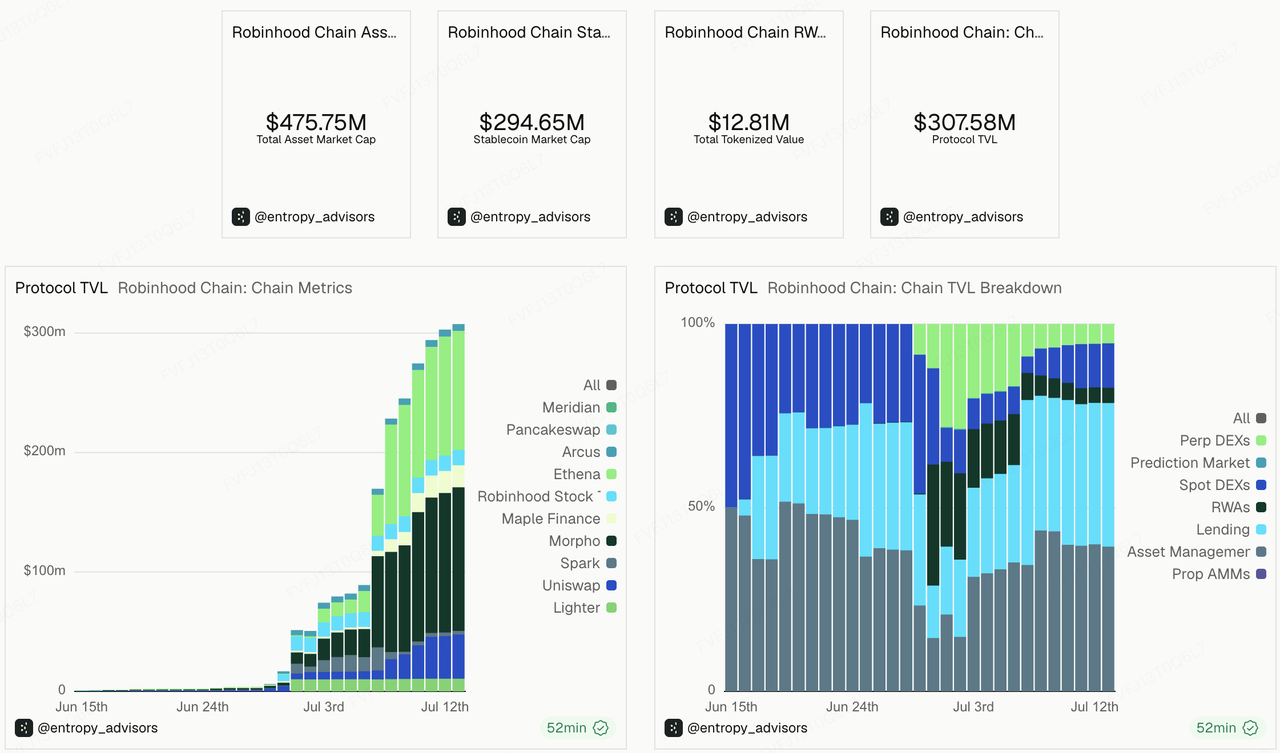

Robinhood Chain is not simply another new L2. Strategically, it is designed to serve as the on-chain infrastructure layer for Robinhood’s multi-asset trading gateway. Robinhood has already launched U.S. stock and ETF tokens and plans to gradually migrate tokenized stocks onto its own L2 built on the Arbitrum technology stack. After Robinhood Chain’s public mainnet launch, infrastructure providers including Uniswap, Chainlink, Alchemy, and BitGo were integrated to support 24/7 Stock Token trading, DeFi lending, and cross-chain liquidity. For Robinhood, building its own chain is about gradually transforming asset exposure that was previously constrained by traditional brokerage accounts, trading hours, and centralized clearing processes into on-chain financial products that can trade 24/7, move across chains, and connect with wallets and DeFi front ends.

However, first-week data shows that Robinhood Chain’s cold start still followed a crypto-native path: high-volatility assets and memes led trading activity, stablecoins and lending products provided liquidity accumulation, while RWA and tokenized assets remained in an early onboarding phase. Meme trading represented by CASHCAT quickly attracted on-chain liquidity, and Pump.fun’s integration further lowered the barriers for token issuance and trading. Data from Dune and DexScreener show that Robinhood Chain quickly accumulated DEX volume, active addresses, and TVL in its early phase, but on-chain activity was driven more by trading and speculative demand than by real RWA usage.

This does not mean Robinhood’s RWA narrative has failed. Rather, it reflects the timing gap between a new chain’s cold start and its long-term asset-use cases. Memes and high-volatility assets can quickly test user onboarding, trade execution, cross-chain liquidity, wallet interactions, and infrastructure capacity, providing an early stress test for future tokenized stocks, ETFs, and RWA products. However, the long-term value of Robinhood Chain will still depend on whether tokenized equities can generate sustained trading demand, and whether regulation, market making, clearing, asset custody, and user-rights arrangements can support the large-scale operation of real financial products. In other words, memes can lift early activity and market attention, but they cannot replace the delivery capability required for RWA products themselves.

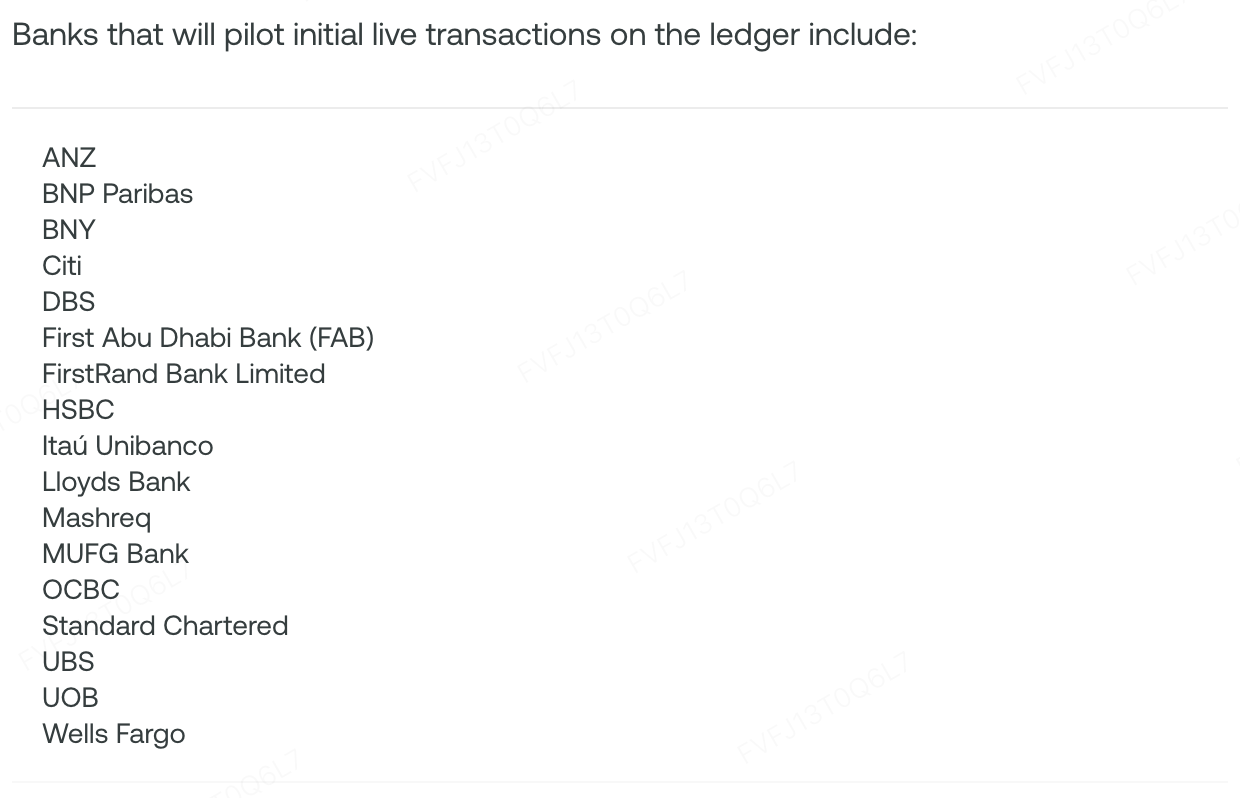

Swift’s move represents traditional banks’ active adoption of blockchain ledgers. On July 9, Swift announced that its blockchain-based shared ledger is ready for initial use, with 17 international banks from six continents set to participate in a real-time cross-border payments pilot based on tokenized deposits. The ledger is not intended to replace the existing Swift network or bank settlement system. Instead, it adds a shared orchestration layer on top of the existing financial network, allowing tokenized deposits issued or managed by different banks to move across institutions and time zones on a 24/7 basis, with final settlement still completed through existing systems. At this stage, the pilot has not disclosed actual transaction volume or funding scale, so it should be viewed more as an infrastructure test for interoperability and programmable payments between bank-issued tokenized deposits, rather than as a large-scale on-chain payment network already in operation.

This path is both competitive with and complementary to public-chain stablecoins. Stablecoins address 24/7 value transfer on open networks, while Swift’s ledger aims to solve interoperability and programmable payment needs for tokenized money within the banking system. In the short term, tokenized deposits may provide a more bank-regulated alternative for corporate cross-border payments, interbank liquidity management, and other high-compliance scenarios. Over the medium to long term, they may also become complementary to stablecoins, CBDCs, and tokenized assets, serving as an important bridge for traditional finance to access on-chain assets and programmable payments.

Overall, Robinhood Chain and Swift’s shared ledger represent two paths for TradFi to move on-chain. The former starts from the retail trading and asset front end, using high-frequency trading and on-chain liquidity to test infrastructure before gradually supporting tokenized stocks and RWA. The latter starts from interbank payments and clearing coordination, using a permissioned ledger and tokenized deposits to reshape cross-border money movement. Their common implication is that blockchain is no longer merely a tool exported from crypto-native protocols to traditional finance. It is increasingly being adopted by traditional financial institutions as part of the next generation of trading and settlement infrastructure.

2. Weekly Selected Market Signals

Structural Divergence Amid a Liquidity Recovery: Macro Tech Assets Attract Capital as Japan’s Traditional Finance Expands Its Crypto Footprint

The defining feature of global markets last week was a temporary recovery in liquidity and risk appetite, although the market structure remained unstable and highly divergent. US technology stocks regained momentum, supported by expectations around semiconductors, memory chips, and artificial intelligence. The Nasdaq gained 1.74% over the week, while the S&P 500 rose 1.23%; the Dow Jones Industrial Average fell 0.50%. At the sector level, information technology, energy, and communication services performed relatively well, while healthcare and materials lagged. Trading activity remained concentrated in large technology companies and the AI supply chain, while cyclical stocks and small- and mid-cap assets received relatively limited attention.

Data Source: Reuters

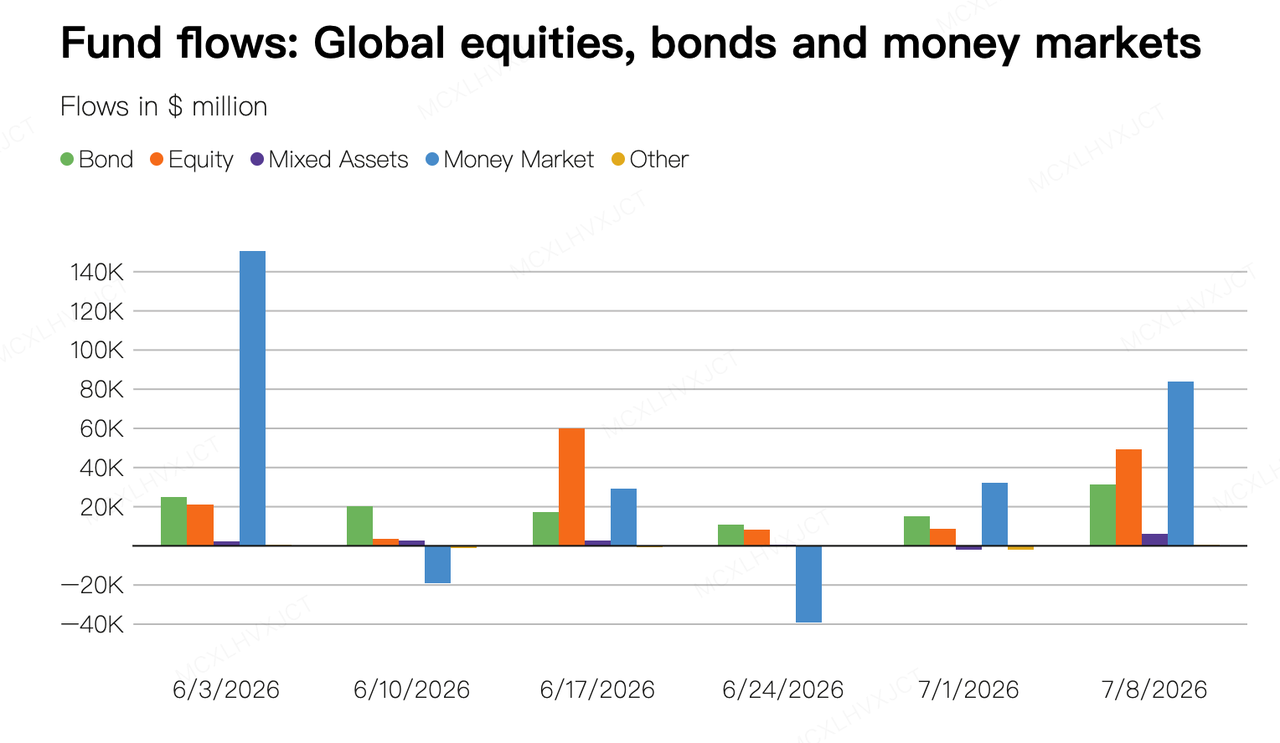

Fund flows reflected the same pattern, with both risk assets and defensive assets attracting capital. According to global fund flow data from LSEG Lipper, global equity funds recorded net inflows of US$49.23 billion in the week ended July 8. US equity funds received US$24.97 billion, while technology sector funds attracted US$11.49 billion. At the same time, global bond funds recorded net inflows of US$31.34 billion, one of the highest levels since at least 2019, while money market funds received US$83.76 billion.

This suggests that investors continued to participate in AI and technology assets while also maintaining relatively high allocations to cash and fixed income. Overall risk appetite improved, but the market did not return to a one-way pursuit of high-risk assets.

The situation in the Middle East remained a major external factor affecting inflation expectations and long-term interest rates. Although WTI and Brent crude briefly fell to US$71.83 and US$76.05 per barrel, respectively, last Thursday, giving technology stocks some breathing room, tensions in the Gulf escalated again after July 13. Both Brent and WTI rose by around 4.1% intraday, while the US dollar and Treasury yields also moved higher.

As a result, markets may need to reassess how energy prices could feed through to inflation and monetary policy. The performance of risk assets cannot be explained solely by corporate earnings and AI-related capital expenditure.

China’s macro policy has taken on a strategic tilt toward technological innovation, covering areas such as artificial intelligence, quantum technology, and life sciences. These fields may become important drivers of industrial upgrading. At the same time, the People’s Bank of China explicitly referred to “structural divergence” at its second-quarter Monetary Policy Committee meeting, acknowledging imbalances between external and domestic demand, as well as between supply and demand. However, there have so far been no clear signals of broad-based stimulus targeting the property sector and traditional parts of the economy.

In the crypto market, CryptoQuant analysis showed that around 40% of altcoins are currently trading close to their historical lows, reflecting extremely weak market conditions. When Bitcoin fell below US$60,000 at the end of June, this proportion briefly rose to 45%.

Without sustained inflows of strong external liquidity, most tokens lacking fundamental support may struggle to survive. The market continues to move deeper into a zero-sum environment characterised by an oversupply of assets and a shortage of liquidity.

Data Source: SoSoValue

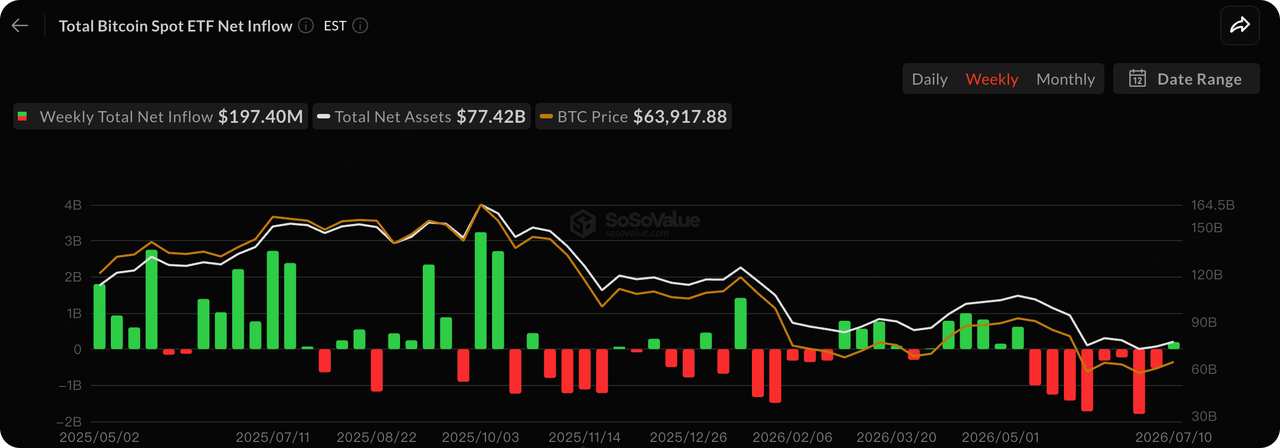

Spot Bitcoin ETFs recorded a two-way reversal, delivering their first positive weekly performance since May:

On July 10, US spot Bitcoin ETFs recorded combined daily net inflows of US$90.44 million. BlackRock’s iShares Bitcoin Trust, IBIT, led the rebound with US$86.83 million in inflows, while VanEck’s HODL fund added US$3.61 million.

Looking at the full week ended July 10, spot Bitcoin ETFs recorded total net inflows of US$197.4 million, reversing several consecutive weeks of heavy outflows. The total net asset value of US spot Bitcoin ETFs reached US$77.42 billion.

Data Source: DeFiLlama

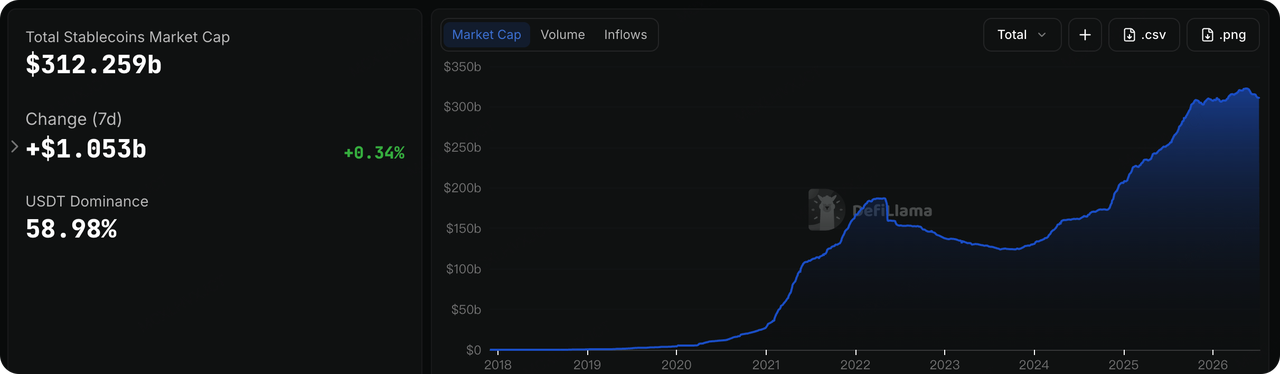

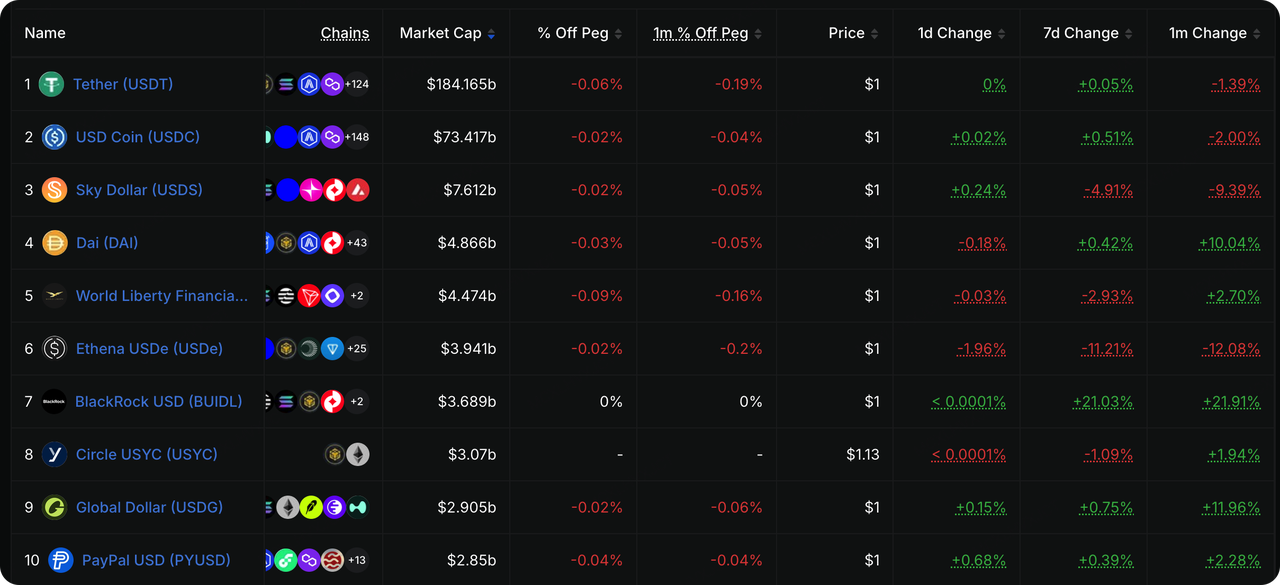

The total stablecoin market capitalisation edged higher, while Tether maintained its dominant position. DeFiLlama data showed that the stablecoin market temporarily ended its period of continued contraction, although the increase remained limited and was not sufficient to indicate a clear expansion in crypto market liquidity.

USDT maintained a market share of 58.98%. USDC’s market capitalisation reached US$73.417 billion, rising 0.51% over seven days and recording moderate weekly inflows. In the short term, it did not appear to be directly affected by the launch of OUSD. USDe’s supply fell by around 11.2% over the week, while BUIDL, a tokenised money market product, grew by approximately 21%.

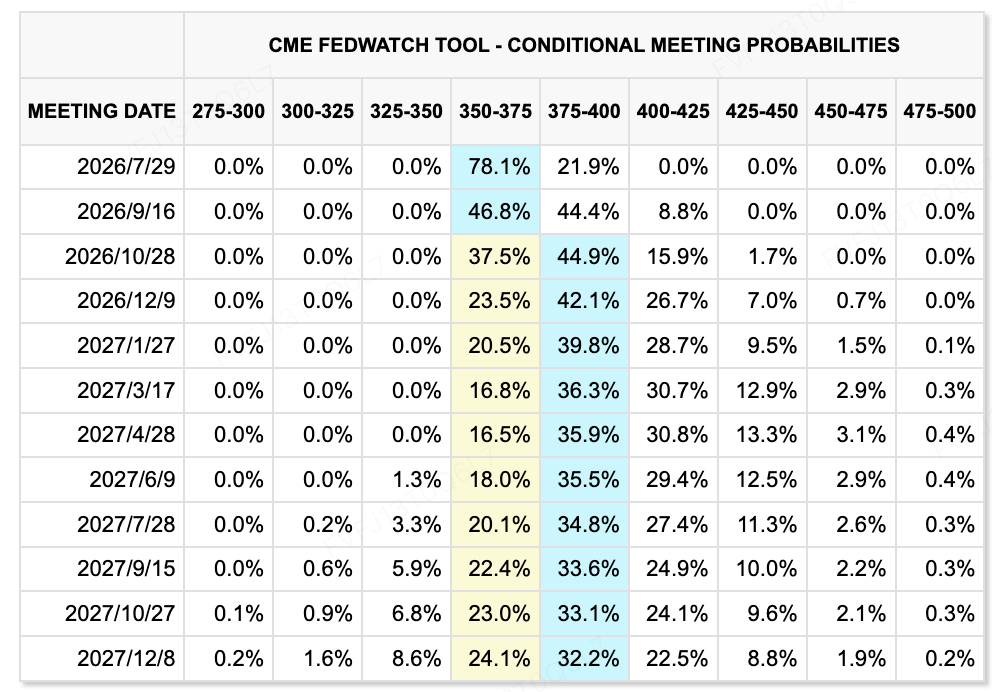

Data Source: CME FedWatch Tool

According to the minutes of the Federal Reserve’s June meeting released last week, the target range for the federal funds rate remained unchanged at 3.50% to 3.75%.

Compared with previous communications, the Federal Reserve removed language suggesting that future policy might lean toward easing. Most participants supported shortening the policy statement and avoiding clear guidance on the future direction of interest rates.

The minutes indicated that the US economy continued to expand at a solid pace, supported by AI-related investment and productivity growth. However, inflation remained above the 2% target, while energy prices, tariffs, and demand for AI infrastructure could continue to create upward price pressure.

At the time captured by the CME FedWatch screenshot, the market assigned a 64.2% probability to the Federal Reserve keeping rates unchanged at its July 29 meeting, and a 35.8% probability to a 25-basis-point rate increase. By the September meeting, the implied probability of at least one rate hike had risen to 72.1%.

The data showed that markets had significantly increased their pricing of a rate-hike scenario. This suggests that the main debate has once again shifted toward whether one or more rate hikes may be needed to bring inflation back under control. However, these expectations remain highly sensitive to oil prices and inflation data and could still change quickly.

Key Events to Watch This Week

The most important variables this week will be US inflation data and Federal Reserve Chair Kevin Warsh’s testimony before Congress. Markets will focus on how the Federal Reserve assesses energy prices, AI-related capital expenditure, tariff pass-through, and the labour market, as well as whether it continues to move away from its previous easing bias.

-

July 14–15: The US releases June CPI and PPI data, while Kevin Warsh appears before the House and Senate.

-

July 15: China’s National Bureau of Statistics holds an economic data briefing and releases first-half GDP, industrial production, fixed-asset investment, property, retail sales, and employment data.

-

July 16: US retail sales data is released.

In addition, the US banking earnings season will begin on Tuesday, followed by results from companies including Netflix and General Electric.At the macro level, markets will need to continue monitoring shipping through the Strait of Hormuz and changes in crude oil prices. If oil prices remain elevated, the impact of CPI data and Federal Reserve testimony on interest-rate expectations could be amplified. If tensions ease again, market attention may shift back toward corporate earnings and the sustainability of AI-related capital expenditure.

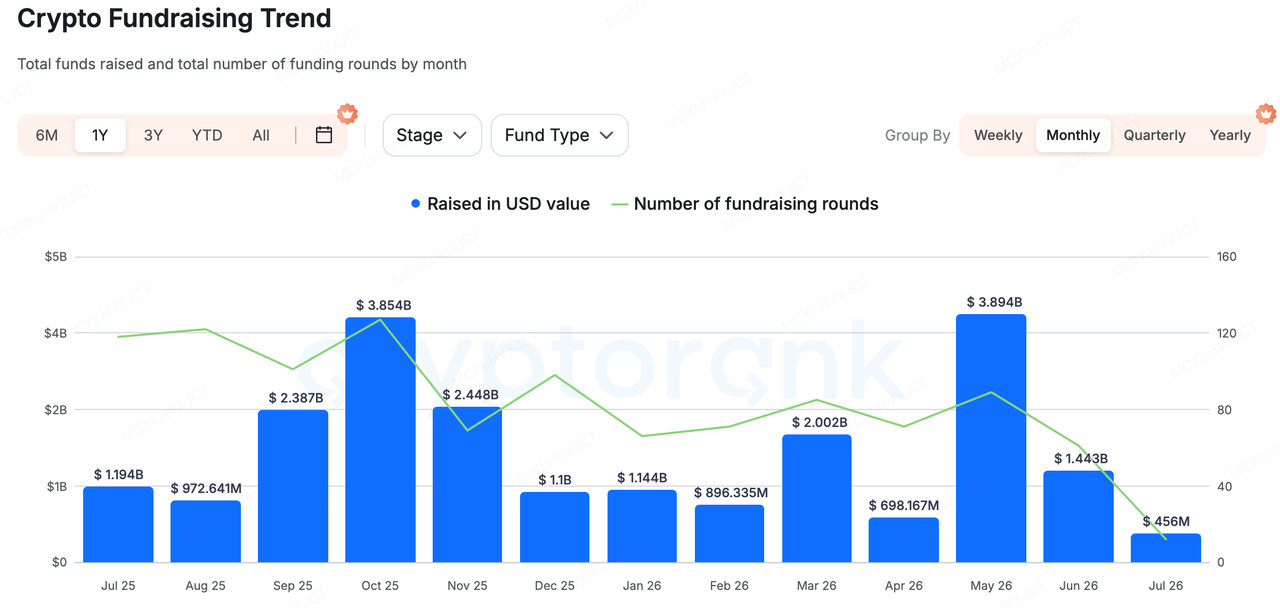

Primary Market Fundraising Review

Data Source: CryptoRank

Based on amounts disclosed by RootData, seven funding rounds announced last week raised approximately US$381 million in total. There were also two investments with undisclosed amounts and two acquisitions.

Prime Intellect, Gauntlet, and EDX Markets together raised approximately US$331 million, accounting for around 87% of the total disclosed funding. Capital was therefore heavily concentrated in a small number of mature projects and large funding rounds, rather than being distributed across a broad range of early-stage projects.

While pure application-layer and community-narrative-driven projects continued to face a difficult funding environment, capital was highly concentrated in business-to-business infrastructure, compliance and data services, and crypto security and defence.

The most notable primary market case last week was Gauntlet. In its early stages, Gauntlet mainly used quantitative models, stress testing, and agent-based simulations to help DeFi protocols set collateral ratios, borrowing limits, interest-rate curves, and incentive parameters. In essence, it operated as a risk management and asset-liability management service provider for on-chain financial markets.

As the business developed, its role expanded beyond providing risk advice to protocols. It gradually moved into on-chain yield strategies and Vault management, designing risk-adjusted yield products for financial institutions, stablecoin issuers, trading platforms, and capital allocators.The company disclosed that it currently manages or curates more than US$1.5 billion in Vault assets, while also providing risk and parameter management services across a broader range of protocols and institutional capital.

Gauntlet’s US$125 million Series C round was led by Japanese financial group SBI Holdings. The funding will be used to expand its stablecoin coverage beyond US dollar- and euro-denominated stablecoins to include currencies such as the Japanese yen and Mexican peso. It will also support the expansion of its global team and the development of new on-chain financial products.

Gauntlet’s value lies more in its attempt to package risk modelling, asset allocation, yield management, and Vault products into infrastructure that institutions can access directly. As more traditional capital moves on-chain, institutions may need more than custody and trading channels. They may also require a middleware layer capable of continuously managing collateral, liquidity, and smart contract risks.

Notably, SBI led funding rounds for both Gauntlet and EDX Markets last week. Taken together, SBI’s recent moves suggest that it aims to build a more complete digital asset financial infrastructure network.Bitbank and SBI VC Trade provide compliant accounts, trading access, and customer assets in Japan. EDX Markets covers institutional trading, central clearing, and settlement. Gauntlet adds on-chain risk management, Vault curation, and stablecoin yield products.

SBI is also advancing the Japanese yen stablecoin JPYSC while introducing US dollar stablecoins such as USDC and RLUSD. Its business scope is gradually expanding beyond traditional exchanges into stablecoins, institutional market infrastructure, and on-chain asset management.

This expansion is also consistent with recent regulatory developments in Japan. A bill submitted by the Japanese government proposes moving the main regulatory framework for crypto assets from the Payment Services Act to the Financial Instruments and Exchange Act. It would also introduce disclosure, insider trading, and investor protection requirements that are closer to those used in securities markets.

Japan’s 2026 tax reform direction also proposes applying a separate 20% tax rate to certain eligible crypto spot, derivatives, and ETF income, provided that the relevant investor protection framework is established. A working group within the ruling party has also recommended building a clearer legal foundation for crypto ETFs and Japanese yen stablecoins.We have also seen the Japanese government encourage pension funds and private capital to allocate more toward domestic and alternative assets, reflecting a broader effort to mobilise capital within the country.

More practically, as Japan’s tax, ETF, and financial product regulatory frameworks become clearer, major Japanese banks, securities firms, and diversified financial groups may become increasingly important strategic investors, acquirers, and distribution channels in the next stage of the crypto primary market.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.