Why KuCoin Earn Is a Safe Haven for Retail Investors in a Bear Market

Introduction

If you're an everyday crypto investor who got in years ago for steady growth, early 2026 hits hard: Bitcoin has dropped sharply from last year's peaks, hovering around the $60,000–$70,000 range amid ongoing market pressure. Portfolios are down, fear dominates the news, and "buy the dip" feels risky instead of rewarding. You're not alone; millions feel the same pain.

That's why many are turning to safer options, such as KuCoin Earn. It skips the volatility of trades or meme coins, letting your money generate reliable yields. Park stablecoins (like USDT), ETH, or other holdings to earn passive returns often 2–5%+ APR on USDT (flexible or fixed terms, with current offers up to ~5–15%) with daily/hourly payouts, no mandatory lock-ups, and none of DeFi's gas fees or complexity. In a down market, it's a calm, straightforward way to keep earning while Bitcoin tests lower levels.

Let us walk you through why this matters so much right now, especially if you’re not a whale or a full-time trader. We’ll look at how the current bear market got here, what KuCoin Earn actually offers, real ways people are using it, and the honest risks you should know about. By the end, you’ll see why it feels less like a product and more like a safety net when everything else feels shaky.

What the 2026 Bear Market Actually Feels Like for Regular Investors

Let’s be real for a second. A bear market isn’t just numbers on a screen. It’s that moment you open your app and see your savings down 20%, 30%, or more from last year’s peak. According to the classic definition, once prices fall 20% from recent highs and stay down for a couple of months, we’re officially in bear territory. Crypto winters hit harder and faster, though. We saw it in 2022, and now in early 2026, it’s happening again.

Bitcoin dropped sharply after its October 2025 highs. Over $200 billion got wiped from the total market cap in a short stretch. The Fear & Greed Index sank into “Extreme Fear.” Altcoins held up a little better this time, but that didn’t help most retail holders who were overweight in riskier tokens. Macro stuff piled on too, softening jobs data, uncertainty around interest rates, and even the AI sector pulling back hard, dragging everything down with it.

The four stages feel painfully familiar if you’ve been through one before:

-

Early denial (“this is just a healthy correction”).

-

Panic selling when supports break.

-

The long, slow grind where nothing exciting happens and negative headlines never stop.

-

Finally, the bottom, when weak hands are gone, and smarter money starts quietly buying.

Right now, a lot of us are somewhere between stage two and three. The 200-day moving average around $58k-60k has become the line everyone stares at. Break it on a big volume,and liquidations could cascade. That’s the environment where holding idle cash or stablecoins in a regular wallet suddenly feels like leaving money on the table. It earns nothing while inflation and opportunity slip away.

This is where KuCoin Earn steps in, not as a trading tool, but as the patient alternative. You convert some exposure to USDT or USDC, subscribe in minutes, and start collecting interest. The platform matches your funds in ways that feel safe and simple, whether you choose flexible (pull out anytime) or fixed terms for a bit more yield.

Introducing KuCoin Earn: More Than Just Another Savings Account

KuCoin has been around long enough that most crypto users know the name, but Earn is the part that shines brightest when markets turn sour. It’s their one-stop shop for wealth management. Think of it as a set of straightforward products that let your crypto generate income without you having to constantly watch charts.

There are two big categories:

-

Stable products (the safe-haven core): Simple Earn (flexible or fixed savings) and Staking. These are built for everyday people who want low drama.

-

Advanced options (higher potential, more suited to experienced users): Things like structured products, though some newer ones were phased out earlier this year.

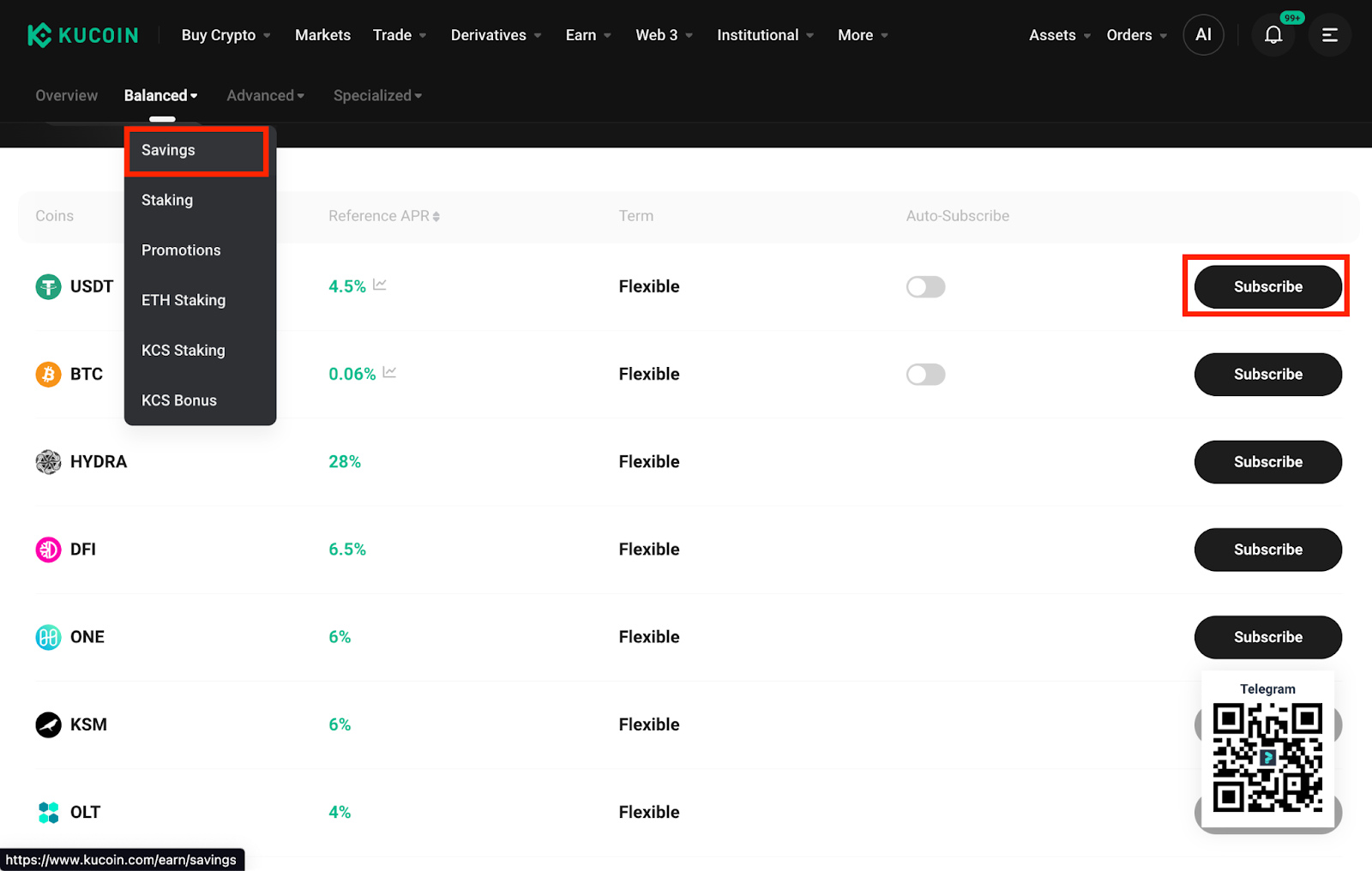

The real magic for retail investors right now lives on the stable side. Take Simple Earn. You deposit USDT, pick a term of 7 days, 14 days, 30 days, or flexible, and earn reference APRs that have been hovering in the 2-3% range lately for USDT (higher during promos, like the recent Earn Wednesday events offering up to 15% on select assets). Flexible means you can redeem anytime; fixed locks it briefly for a slightly better rate and auto-returns your principal plus earnings at the end.

Staking works similarly but ties into actual blockchain networks. ETH staking gives you around 2.1% flexible right now, with liquid tokens you can still use elsewhere. SOL is offering closer to 5%. KCS staking (KuCoin’s own token) offers daily rewards and platform perks.

Then there’s Crypto Lending Pro, which many people use alongside Earn. You lend your idle USDT or other assets to margin traders who need liquidity. Rates are adjusted hourly based on demand, and a portion of earnings is deposited into an insurance fund. In bear markets, when short sellers and leveraged players borrow more, lending demand can actually pick up, meaning better rates for patient lenders.

Newer touches like Hold to Earn let you earn up to 3% APR on assets sitting in your spot, futures, or margin accounts without locking anything. Your money stays available for trading or withdrawals while quietly growing.

The beauty is how beginner-friendly it is. Minimums are often just a few dollars. The interface shows clear APR ranges, subscription buttons, and your earnings history. Everything happens inside your KuCoin account, so no extra wallets or bridges. Rewards usually hit your funding account daily or hourly, ready to compound or withdraw.

How KuCoin Earn Changes the Game During a Bear Market

Here’s where it gets practical. In a bull run, everyone chases price pumps. In a bear market like 2026’s, the name of the game is survival plus preparation. KuCoin’s own research pieces on bear cycles hammer this home: allocate some capital to stablecoins and let it earn yield rather than sit idle. That way, you’re not just preserving value, you’re actually growing it slowly while waiting for the next cycle.

Think about the psychology. When Bitcoin is grinding lower, and every “dip buy” attempt fails, panic selling is tempting. But if part of your stack is earning 2.5-6% on stable assets, that steady drip of income takes the edge off. It gives you breathing room. Some users even set up automated strategies: earn on USDT, then use the interest to DCA into Bitcoin at lower levels without touching principal.

Real cases illustrate this better than theory. During the 2022 crypto winter, Bitcoin fell from $69k to $15k. Investors who parked stables in similar earn-style products on major platforms came out with an extra buffer. They avoided total wipeouts and had fresh capital ready when the 2023-2025 recovery started. Fast-forward to now. In February 2026, after the sharp drop below $60k, plenty of regular users quietly shifted to KuCoin’s flexible USDT savings.

One community story I saw (anonymized, of course) described a teacher who had been holding since 2021. She moved 40% of her portfolio to 30-day fixed Earn products at around 2.6-2.8%. While the market kept testing support, she collected daily interest that covered some living expenses and kept her from selling in fear. When sentiment eventually stabilizes, she’ll have both preserved capital and extra earnings to redeploy.

Another angle comes from lending. During high-volatility periods, margin borrowing demand spikes as traders hedge or short. Lenders on KuCoin’s platform saw hourly payouts rise because more borrowers needed liquidity. It’s the opposite of what happens in a bull run when everyone is long, and borrowing dries up.

Compare that to alternatives. Leaving USDT in a cold wallet earns zero. DeFi platforms on other chains entail gas fees, smart contract risks, and constant monitoring. Traditional banks? They’re not even in the game for crypto natives. KuCoin Earn sits in the sweet middle, centralized enough to be simple and secure, decentralized enough to offer real yields.

Security adds another layer of comfort. KuCoin publishes monthly Proof of Reserves showing over 100% backing. Most user funds sit in cold storage. They hold SOC 2 Type II, ISO certifications, and an AAA security rating from independent auditors. That’s not marketing fluff; it’s the kind of transparency that matters when trust is low across the industry.

Key Advantages That Make It Feel Like a True Safe Haven

Let’s break down the practical upsides that retail investors keep mentioning, especially those who've been through previous downturns and now see KuCoin Earn as their go-to when markets turn tough:

Flexibility without sacrifice

Need cash tomorrow for an unexpected bill or a sudden trading opportunity? Flexible savings and lending options let you pull out instantly or within the next hour for lent assets without any penalties. Unlike traditional bank CDs that lock you in and charge fees for early withdrawal, KuCoin's flexible products give you full control.

As of mid-March 2026, flexible USDT savings remain available with no lock-up, meaning your principal stays liquid while still earning. This is huge for retail investors who can't afford to have funds tied up during uncertain times. You preserve access to your money while it quietly works for you, striking a balance that's hard to find elsewhere in crypto or traditional finance.

Competitive, real yields that actually beat inflation

In a world where traditional savings accounts and even some high-yield banks struggle to keep pace with inflation, KuCoin Earn delivers meaningful returns on stable assets. Base rates for USDT flexible or short-term fixed options sit around 2–3% APR right now, but promotions push them much higher. For instance, the ongoing Earn Wednesday Week 109 (launched March 18, 2026) offers up to 15% APR on select USDT, ETH, and ATOM terms with reasonable subscription caps.

Staking adds another layer. ETH's flexible staking hovers at about 2.14%, while SOL delivers closer to 5% with fast redemption. These aren't speculative gambles; they're grounded yields from stablecoins that hold their peg and staking rewards from established networks. Over months in a prolonged downturn, that steady income compounds and helps offset losses elsewhere in your portfolio, turning idle capital into something productive.

Principal protection focus

One of the biggest fears in crypto is losing your main amount to price swings or platform issues. KuCoin Earn's stable products are built around this concern. Stablecoin-based savings and

lending target assets like USDT and USDC that are designed to stay pegged at $1, so your principal isn't exposed to the same wild volatility as BTC or altcoins. Crypto Lending Pro includes an insurance fund that protects against potential borrower defaults.

KuCoin also maintains strong security practices. Monthly Proof of Reserves audits show over 100% backing, with the majority of funds in cold storage. For retail investors who remember past exchange failures, this transparency and focus on capital preservation feel reassuring. You're not betting on price appreciation here; you're safeguarding what you already have while earning on top.

Low barrier for beginners

You don't need to be a DeFi expert or understand complex yield farming protocols to get started. KuCoin Earn is intentionally simple: log in, navigate to the Earn section, see clear APR ranges and terms displayed upfront, click subscribe, and you're done. Minimum deposits are often just a few dollars, making it accessible even if you're starting small. No need for external wallets, bridging chains, or paying gas fees that eat into returns.

The dashboard automatically tracks your earnings history, so you can check in once a week or once a month without constant monitoring. This setup is perfect for people with full-time jobs, families, or limited time, who want passive income without turning it into another full-time job.

Compounding power that builds quietly

Daily or hourly interest credits mean your earnings start generating their own returns almost immediately. In a bear market that drags on for months (or longer), this compounding effect becomes noticeable.

For example, a modest USDT position earning 3% base APR (or higher during promos) can grow meaningfully over time without any additional effort from you. Many users report that after six months of consistent use, the accumulated interest has covered small expenses or provided extra capital to DCA back into BTC at lower levels. It's not flashy growth, but it's reliable and snowball-like, exactly what patience looks like in tough markets.

Works seamlessly with your existing holdings

One standout feature is Hold to Earn, rolled out earlier in 2026. It lets assets already in your spot, margin, or futures accounts earn up to around 3% APR without moving them or locking them up. Your balance stays fully available for trading, transfers, or withdrawals while rewards accrue in the background.

This eliminates the common dilemma of choosing between yield and liquidity. Your capital remains productive until the exact moment you need it. For active traders who still want some passive income during downtime, or long-term holders who prefer not to shuffle funds around,

this integration makes Earn feel like a natural extension of the platform rather than a separate tool.

Warren Buffett’s old line about being “fearful when others are greedy” fits perfectly here. Bear markets redistribute wealth from the impatient to the patient. KuCoin Earn gives everyday retail investors a practical, low-drama way to stay patient: earn while you wait, protect what you have, and position yourself with extra capital when the cycle inevitably turns. In March 2026's environment, with Bitcoin still testing supports and macro uncertainty lingering, it's no wonder so many are quietly leaning on these tools to sleep a little easier at night.

The Honest Challenges and How to Handle Them

Nothing is perfect, and pretending otherwise would be unfair. Here are the real considerations:

First, it’s still crypto. While stablecoins like USDT and USDC have held strong, extreme events could theoretically test pegs (though regulations are expected to tighten by 2026). Platform risk exists, too, with no FDIC insurance like a bank. If something ever happened to KuCoin (unlikely given its track record and cold storage), it could temporarily affect access.

APYs aren’t fixed forever. They move with market demand. A promo rate today might drop next month. That’s why flexible options matter; you can adjust.

Opportunity cost is another one. If the market suddenly turns bullish and you’re locked in a 60-day fixed product, you might miss quick upside elsewhere. Solution? Keep most of your “earn” portion in flexible or short-term products and only use longer terms with money you truly won’t need soon.

Regulatory gray areas exist in some countries. Always check local rules.

How do smart users manage this? Start small, maybe 20-30% of your stable holdings first. Enable every security feature (2FA, withdrawal whitelist, anti-phishing). Check the monthly Proof of Reserves reports yourself. Diversify across a couple of products: some flexible savings, some staking, a bit in lending. Set calendar reminders to review rates every few weeks. And never put money you can’t afford to have tied up for a while.

Wrapping It Up: Patience Meets Practical Tools

The 2026 bear market has tested many people. Macro headwinds, AI sector pullbacks, and classic crypto volatility combined to create one of those periods where survival skills matter more than hype. Yet amid all that noise, KuCoin Earn has quietly helped everyday investors do two things at once: protect what they have and keep growing it, even if slowly.

It’s not about getting rich quickly. It’s about not getting poor slowly. Turning idle stable assets into earning machines gives retail users the confidence to wait out the storm instead of panic-selling at the bottom. History shows these winters end. The ones who come out stronger are usually the ones who stayed disciplined and kept their capital working.

If you’re feeling the weight of red charts right now, take a few minutes to explore the Earn section. Start with something simple like flexible USDT savings. See the rates for yourself. Many who did exactly that in past cycles say it was the decision that let them sleep better at night.

The market will turn eventually. When it does, you’ll want both preserved capital and a bit of extra from the quiet months. KuCoin Earn is one of the cleaner ways retail investors are making that happen today.

Ready to explore? Head over to KuCoin Earn and check the current offerings. While you’re there, browse their Learn section for more bear-market guides or check recent announcements for fresh promotions. If you have questions, drop them in the comments below. I read everyone.

Frequently Asked Questions

1. Is KuCoin Earn completely risk-free?

No investment is 100% risk-free, but the stable products are designed with principal protection in mind for savings and staking. There’s no price risk on stablecoins themselves, and KuCoin’s security track record is strong. Still, always use only what you can afford and enable all security settings.

2. How much can I realistically earn right now on USDT?

Flexible and short-term fixed options are currently showing around 2-3% APR, with some promos higher (up to 15% on select events). Rates change with demand, so check the dashboard daily for the latest.

3. Can I pull my money out anytime?

Yes, with flexible savings and lending, redemption is instant or within the next hour. Fixed terms require waiting until maturity, but you know the exact date upfront.

4. What if the market suddenly recovers?

That’s why flexible products exist. Many users keep the majority in no-lock-up options so they can shift back to trading quickly when signals improve.

5. Is it better than just holding in a wallet?

Absolutely, if you’re using stablecoins. A wallet earns zero. Earn turns that same USDT into a quiet income stream, often 2%+ annually.

6. Do I need to be a pro trader to use it?

Not at all. It’s built for beginners. The interface walks you through every step, and the minimum deposit is tiny.

7. How does lending compare to simple savings?

Lending often pays more when borrowing demand is high (common in volatile markets), but rates fluctuate hourly. Savings is more predictable. Many people are split between both.

8. What happens to my earnings?

They’re automatically credited daily for most savings and staking, and hourly for lending. You can withdraw them, compound them, or use them to buy the dip.

The bear market won’t last forever. Tools like KuCoin Earn just make the waiting part a lot less painful and maybe even profitable.