AI Compute Investment Enters a New Phase: Why the Smart Money Is Moving Beyond GPUs

2026/06/17 12:49:00

Introduction

The artificial intelligence infrastructure landscape is undergoing a structural transformation. For the past two years, capital allocation across both equity and crypto markets followed a straightforward thesis: the entities controlling the largest GPU clusters would capture the lion's share of AI-driven value creation. NVIDIA's ascent to a $3 trillion market capitalization validated this logic, as hyperscalers including Microsoft, Google, Amazon, and Meta collectively directed over $200 billion in capital expenditure toward GPU cluster expansion during 2025.

However, market dynamics are shifting. The emergence of agentic AI — autonomous systems capable of multi-step task execution — is fundamentally altering the hardware requirements of AI workloads. Rather than concentrating value in a single component, the new architecture distributes demand across the full compute stack, creating investment opportunities in segments that remained underappreciated during the initial GPU buildout phase.

This article examines the structural transition from GPU-centric investment logic to full-stack system optimization, analyzes the implications for both traditional semiconductor equities and AI-linked digital assets, and identifies the sectors positioned to capture outsized returns in the next phase of AI infrastructure deployment.

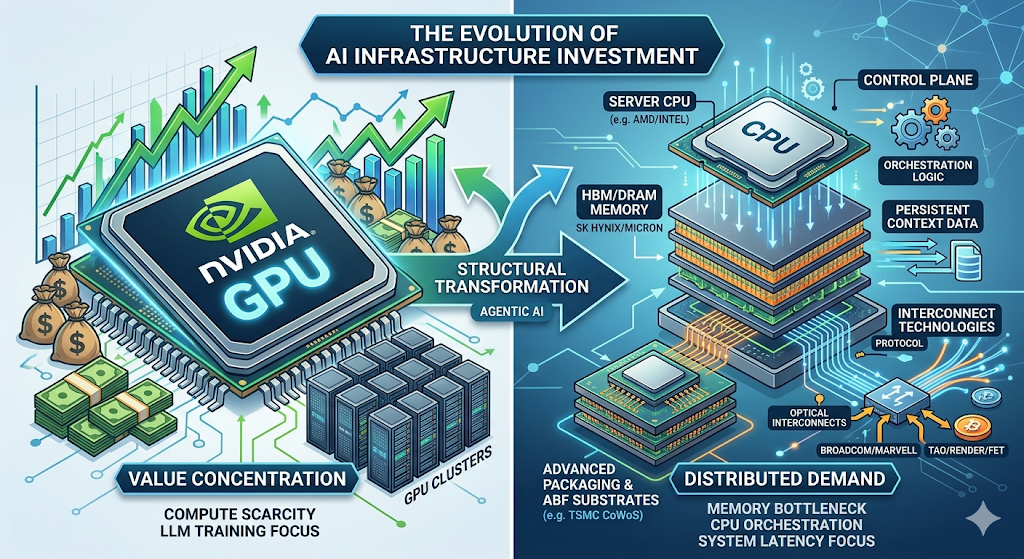

The GPU-Centric Paradigm: How Phase 1 Played Out

The first phase of AI infrastructure investment was defined by a single constraint: compute scarcity.

Training large language models at the frontier scale — GPT-4 class systems and beyond — required tens of thousands of GPUs operating in parallel for extended durations. The competitive moat was straightforward: organizations with access to greater compute resources could train larger models, and larger models produced demonstrably superior performance on benchmarks that the market cared about.

This dynamic created a self-reinforcing cycle. Capital flowed into GPU procurement. NVIDIA's data center revenue scaled from $15 billion in fiscal 2023 to over $90 billion in fiscal 2025. Cloud providers expanded capital budgets to secure GPU allocations. AI startups raised record funding rounds predicated on the assumption that compute access would remain a differentiating factor.

The investment implications were equally direct. Long NVIDIA, long memory suppliers, long anything in the GPU supply chain. It was a phase characterized by scarcity economics and concentration of value in a single chokepoint.

The Structural Shift: Why Agentic AI Changes the Infrastructure Stack

The transition from generative AI to agentic AI represents an architectural inflection point with profound implications for hardware demand.

Generative AI systems operate on a request-response model. A user submits a prompt, the model processes it through a forward pass of its neural network, and returns a generated output. The computational bottleneck is almost entirely within the GPU: matrix multiplication speed, memory bandwidth for weight loading, and interconnect bandwidth for distributed training.

Agentic AI operates on a fundamentally different paradigm. These systems do not merely generate responses — they execute complex, multi-step workflows autonomously. An agentic system tasked with market research might: access external databases, query APIs, process unstructured documents, generate analytical summaries, and iterate based on intermediate results before delivering a final output.

This architecture imposes a markedly different set of hardware requirements:

| Capability | Hardware Dependency | GPU Share of Workload |

| Neural network inference | GPU (matrix computation) | 10–50% |

| Memory/state management across sessions | DRAM/HBM (persistent context) | N/A |

| API orchestration and service routing | CPU (control plane) | N/A |

| Authentication and security handling | CPU (security modules) | N/A |

| Cross-service data consistency | CPU + interconnect | N/A |

Source: Morgan Stanley Research, "Agentic AI: From Compute to Orchestration" (April 2025)

The critical insight is that GPU workload share drops significantly in agentic architectures. While the GPU remains essential for neural network inference, the majority of system time is consumed by CPU-side orchestration tasks. Morgan Stanley estimates that CPU-side processes can account for 50% to 90% of total latency in agentic workflows — a structural shift that inverts the Phase 1 investment thesis.

The Expanded Opportunity Set: Key Sectors for Phase 2

The redistribution of hardware demand creates a broader set of investment opportunities across the AI supply chain. Below is an analysis of the sectors positioned to capture the highest marginal returns as the infrastructure buildout enters its next phase.

-

Server CPUs: The $100 Billion Control Plane

The CPU opportunity in AI infrastructure is substantially larger than consensus estimates currently reflect.

Morgan Stanley projects that the proliferation of agentic AI systems will drive incremental demand for 325 million to 600 million server CPUs by 2030, expanding the total addressable market from approximately $34 billion today to $82–110 billion. This represents one of the largest demand expansions in the history of the server semiconductor market.

The demand driver is architectural, not cyclical. Agentic systems require CPUs to serve as the control plane — managing complex workflows, maintaining long context windows, enabling cross-task state switching, and coordinating interactions between the AI model and external services. This is not a function that GPUs are designed to perform efficiently.

Key beneficiaries: AMD (currently holding ~53% cloud CPU market share, surpassing Intel), Intel, and ARM-based server chip vendors. The ecosystem extends to CPU socket manufacturers, BMC controller suppliers (Aspeed holds ~70% market share), voltage regulators, and specialized interconnect providers.

-

Memory (DRAM/HBM): The Structural Bottleneck

If one segment of the AI supply chain is positioned for the most dramatic repricing, it is memory.

Agentic AI's memory requirements are orders of magnitude greater than generative AI's. Persistent memory is what enables agentic continuity — the ability to remember past interactions, learn from them, and apply that learning to future tasks. Without sufficient memory bandwidth and capacity, even the most advanced GPU clusters will operate below their theoretical performance limits.

Morgan Stanley estimates that agentic AI will drive 15 to 45 exabytes of incremental DRAM demand by 2030. To contextualize this figure: it represents 26% to 77% of the entire DRAM industry's 2027 supply capacity. This is not incremental demand — it is a demand shock with the potential to fundamentally reset DRAM pricing dynamics for the remainder of the decade.

High Bandwidth Memory (HBM) sits at the epicenter of this demand surge. Each next-generation AI accelerator requires multiple HBM stacks, and the transition from HBM3E to HBM4 in 2026 will further concentrate supply among the three qualified producers: SK Hynix, Samsung, and Micron. The HBM market is projected to grow at a 65% compound annual growth rate through 2028.

Market performance: Micron Technology (MU) was the best-performing semiconductor stock of 2025, delivering a +236% return as AI-driven memory demand surged. As of mid-2026, MU has extended those gains with an additional +987% one-year return, reflecting the market's repricing of memory as a strategic AI resource rather than a commodity component.

-

Advanced Packaging and ABF Substrates

The ABF (Ajinomoto Build-up Film) substrate market illustrates how AI demand is creating new bottlenecks in unexpected segments of the supply chain.

ABF substrates are essential for advanced chip packaging, providing the high-density interconnect layers that connect GPU dies to HBM memory and enable chiplet architectures. NVIDIA's Blackwell and Rubin platforms, AMD's MI300 series, and Intel's Gaudi accelerators all depend on ABF substrate supply — and that supply is tightening.

Industry analysts project that the AI-driven ABF upcycle may extend through the end of this decade, with supply-demand gaps emerging around 2026–2027. Server CPU ABF substrate market size is projected to reach approximately $4.7 billion by 2030, with CPU-driven incremental demand of roughly $1.2 billion.

Advanced packaging houses face similar constraints. TSMC's CoWoS capacity — the technology that enables high-bandwidth integration of GPUs and HBM — is fully booked through 2026. Alternative providers including Amkor and ASE Group are expanding capacity, but equipment lead times and technical complexity mean supply will remain a binding constraint for years.

-

Interconnect Technologies: Scaling the Fabric

As AI clusters scale toward 100,000+ GPU configurations, the network fabric — not the individual accelerators — becomes the limiting factor on system performance.

Optical interconnects, including transceivers, active optical cables, and co-packaged optics, are experiencing demand growth that significantly exceeds supply expansion. Companies providing switch silicon and custom interconnect solutions — notably Broadcom (AVGO) and Marvell (MRVL) — are reporting order backlogs extending multiple years, providing significant visibility into forward revenue.

The interconnect opportunity is further amplified by the CPU TAM expansion. Each additional server CPU requires memory interfaces, board-level interconnects, and network connectivity. Montage Technology, with approximately 36.8% global revenue share in memory interconnects, is positioned at the critical junction between CPU and DRAM demand growth.

Investment Framework: Timing the Phase Transition

Navigating the transition from Phase 1 to Phase 2 requires a framework for understanding where value is likely to accrue — and when.

| Phase | Timeframe | Characteristics | Investment Focus |

| Phase 1: GPU Dominance | 2023–2025 | Compute supply was the binding constraint; NVIDIA and GPU supply chain captured outsized returns | NVIDIA, GPU memory, data center REITs |

| Phase 2: Bottleneck Exposure | 2025–2027 | Latency and cost constraints emerge in memory, CPU orchestration, and interconnect components | DRAM/HBM, server CPUs, advanced packaging, optical interconnects, AI tokens |

| Phase 3: Infrastructure Repricing | 2027–2028 | Full-stack optimization becomes the primary value driver; system-level plays see broad-based appreciation | Full AI supply chain, system integrators, edge AI infrastructure |

Current positioning: The market is transitioning from Phase 1 into Phase 2. Inference workloads — particularly agentic inference — impose fundamentally different requirements than training. They are more memory-bandwidth intensive, more latency-sensitive, and more dependent on system-level optimization. These characteristics favor suppliers of memory, interconnects, and system integration over pure compute providers.

For equity investors, the Phase 2 opportunity is most acute in segments where supply expansion is constrained by technical complexity and long equipment lead times: HBM (three qualified suppliers), CoWoS advanced packaging (capacity fully booked through 2026), and certain categories of optical interconnects.

For crypto investors, AI tokens with measurable protocol revenue and real infrastructure usage — TAO, RENDER, and FET — offer exposure to the same demand drivers with the additional upside optionality of crypto market liquidity cycles.

Risk Factors

No investment thesis is complete without an honest assessment of risks. Several factors could derail or delay the Phase 2 opportunity:

Macro correlation. AI tokens diverged from the broader crypto market in Q1 2026, but a severe macro shock — further geopolitical escalation, unexpected rate hikes, or a sharp contraction in risk appetite — would likely drive correlations toward 1 across all risk assets. Portfolio construction should account for this tail risk.

Valuation stretch. TAO trades at approximately 20x annualized Q1 revenue. While reasonable by tech startup standards, this premium could evaporate quickly if revenue growth stalls. The same dynamic applies to semiconductor names that have re-rated sharply: Micron's extraordinary 2025 performance embeds high expectations that any demand softness could pressure.

Narrative crowding. According to Grayscale's research, "AI" became the most frequently referenced term in crypto project whitepapers during early 2026. When every project claims AI exposure, the signal-to-noise ratio deteriorates. The tokens and equities that survive this phase will be those with revenue receipts, not pitch decks.

Technology risk. Agentic AI remains an emerging technology category. If the architecture evolves in a direction that reduces hardware requirements — for example, through more efficient model designs or novel inference techniques — the demand projections outlined above could prove overly optimistic.

How to Trade US Stocks and Bitcoin on KuCoin

KuCoin also offers exposure to trading US stock perps — meaning you can rebalance between crypto and US equity narratives without leaving the platform. Combined with the security infrastructure of a tier-one global exchange, KuCoin is positioned for investors who want flexibility across both asset classes.

Conclusion

The AI compute investment landscape is entering its second phase. The simple GPU scarcity narrative that drove returns from 2023 to 2025 is giving way to a more complex, distributed value creation model in which memory, CPU orchestration, and system-level integration play roles as critical as raw compute power.

For investors, this transition expands the opportunity set meaningfully. The equity market offers exposure through memory suppliers (SK Hynix, Samsung, Micron), CPU designers (AMD, Intel), interconnect leaders (Broadcom, Marvell), and advanced packaging houses (TSMC, Amkor). The crypto market offers parallel exposure through AI-linked tokens — TAO, RENDER, and FET — which demonstrated significant relative strength in Q1 2026 and continue to benefit from measurable protocol revenue growth.

The critical insight for positioning: infrastructure value flows to the slowest-expanding links in the chain. GPU supply has scaled rapidly. Memory, advanced packaging, and certain interconnect technologies have not. These bottlenecks possess pricing power and competitive moats that will sustain margins even as AI adoption broadens and matures.

The Phase 2 window is opening now. The investors who recognize the structural shift — and position across both traditional equities and digital assets ahead of the full market repricing — stand to capture the next wave of AI-driven infrastructure returns.

FAQs

What is agentic AI, and why does it require different hardware than generative AI?

Agentic AI refers to systems that autonomously plan and execute multi-step tasks — researching, using tools, and iterating toward goals without continuous human input. Unlike generative AI (chatbots that respond to single prompts), agentic systems require persistent memory for continuity, CPU orchestration for service coordination, and high-bandwidth interconnects for data movement. This shifts the hardware bottleneck from raw GPU compute to system-wide efficiency. Morgan Stanley Research estimates CPU-side processes account for 50–90% of latency in agentic workflows.

Which semiconductor stocks are best positioned for the Phase 2 transition?

Morgan Stanley identifies memory and GPU companies as the purest AI-enabled exposures: NVIDIA (forward P/E of 18x for FY2027), Broadcom (AVGO), and Micron (MU) (forward P/E of 5–9x). While AMD and Intel benefit from CPU TAM expansion, Morgan Stanley notes their stock performance is more closely tied to GPU and foundry narratives respectively, making them less pure plays on the CPU orchestration thesis. Micron's +236% return in 2025 and continued outperformance in 2026 underscore the market's repricing of AI memory demand.

How should investors think about risk management in AI infrastructure plays?

AI infrastructure investments carry specific risks: macro correlation can drive all risk assets lower simultaneously; valuation premiums (TAO at ~20x revenue, memory stocks post-strong run-ups) can compress quickly on demand softness; and narrative crowding means distinguishing genuine infrastructure plays from rebranded projects is essential. A prudent approach limits AI token exposure to 5–10% of a crypto portfolio and maintains position sizing discipline across equity exposures.